A Delaware Statutory Trust is a Delaware legal entity used to hold real estate for fractional investors, and DST offerings typically require a $100,000 minimum investment with a 3 to 10-year holding period. In practice, it's most often used as a passive replacement property in a 1031 exchange, where investors buy a beneficial interest instead of taking title to a property themselves.

This article is about the investment structure, not Daylight Saving Time. A DST is a legal entity for passive real estate investment that can qualify as replacement property in a 1031 exchange when it is structured and operated within the applicable tax rules.

If you advise clients who've just sold appreciated rental property, you've probably seen the same pressure point repeatedly. The sale closes, the qualified intermediary is in place, the identification clock is running, and the client wants tax deferral without another round of tenant issues, leasing problems, or property-level decision making.

That's where DSTs enter the conversation. They can solve a real problem, but they're not simple, and they're not interchangeable with direct ownership, a TIC, or a private real estate fund. The legal mechanics matter. The sponsor's conduct matters. The debt stack matters. For financial professionals, those details aren't side issues. They drive suitability, compliance, and litigation risk.

Disambiguating DST and Its Role in Modern Portfolios

“DST” means different things in different contexts. Here, it means Delaware Statutory Trust, not the time-change issue that shows up in software and operating system updates.

In the advisory world, the term usually comes up when a client has sold, or is about to sell, an investment property and wants to avoid an immediate tax hit by completing a like-kind exchange. The problem is familiar. The client may not want another directly owned property, may not want to manage tenants, and may not want to race through a purchase on a compressed exchange timeline.

A DST often becomes the practical answer because it lets the client move from concentrated, active ownership into a fractional interest in professionally managed real estate. Under Delaware law, a Delaware Statutory Trust is a legal entity formed by filing a Certificate of Trust with the Delaware Division of Corporations and is designed to hold title to real estate with an unlimited number of investors owning fractional interests (EisnerAmper on Delaware Statutory Trusts and 1031 exchanges).

Why advisors keep seeing DSTs

DSTs fit a narrow but recurring need. They can give an exchanger access to larger assets than the client would typically buy alone, while shifting day-to-day management to the trust's operator.

That doesn't make them a default recommendation. It makes them a structure worth understanding before the client asks whether a sponsor's offering solves a real exchange problem or just repackages one.

Many exchange failures don't happen because the tax concept was wrong. They happen because the replacement option was evaluated too late and too superficially.

Clients also compare DSTs against direct acquisitions financed with debt. If they're still weighing active ownership, a useful parallel resource is this discussion of financing rental properties and how loan structure changes the ownership experience. That comparison helps clarify whether the client is seeking passive exposure or still wants operating control.

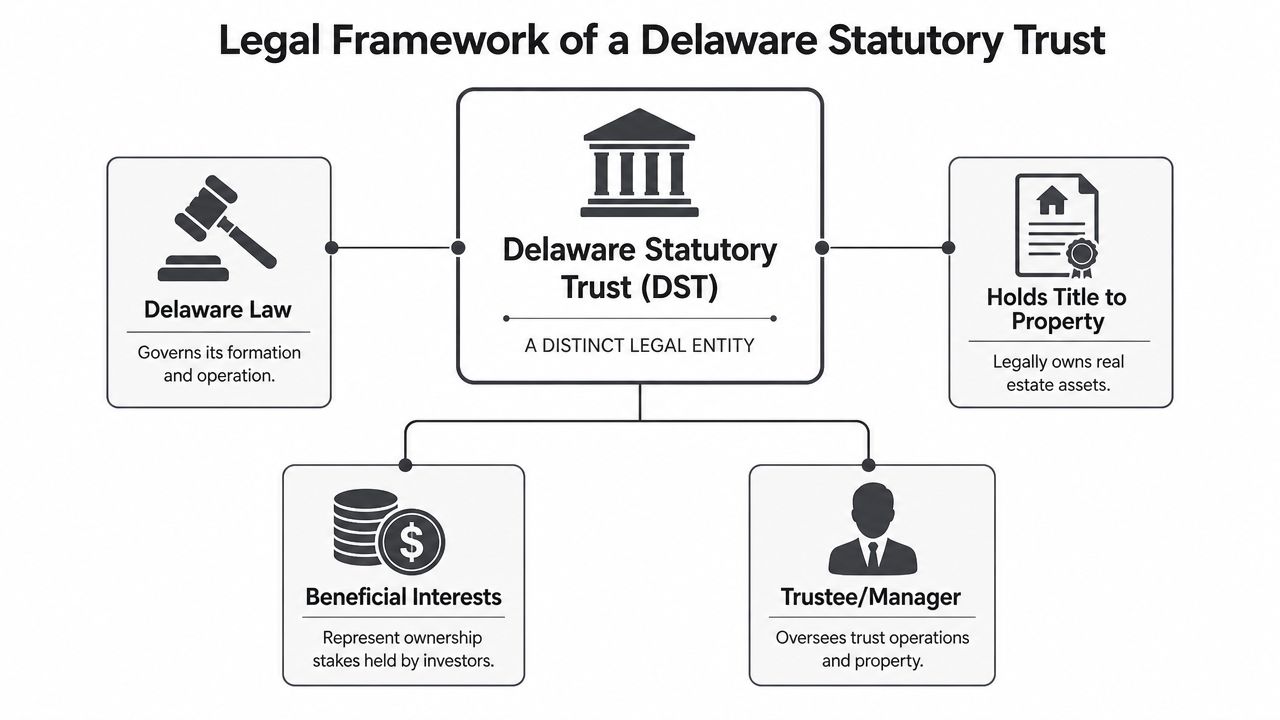

The Legal Framework of a Delaware Statutory Trust

A DST works best when you think of it as a pre-structured real estate ownership vehicle. The trust holds title to the property. Investors purchase beneficial interests in the trust. They don't step into an ownership role that includes operational authority.

This legal separation is not cosmetic. It is central to both liability allocation and tax treatment.

Who does what

A typical DST offering includes several distinct actors:

- Sponsor: The sponsor sources properties, structures the offering, prepares the offering documents, and oversees the business plan.

- Trustee or manager: The trustee holds legal title and handles management functions required under the trust structure.

- Beneficial owners: Investors buy fractional beneficial interests and remain passive. They receive economic rights, not operational control.

That final point is where many non-lawyers oversimplify the vehicle. Investors often hear “fractional ownership” and assume it works like co-owning a building with a vote on major decisions. It doesn't. In a DST, passivity is a design feature.

Formation and legal mechanics

The entity itself is relatively straightforward to form. The parties draft a private trust agreement, obtain a Certificate of Trust from the Delaware Division of Corporations, and submit it with a one-time $500 processing fee. The trust agreement remains private, and the structure allows multiple investors to hold undivided fractional beneficiary interests while professional trustees manage operations (KPI 1031 on what a Delaware Statutory Trust is).

From a business-law standpoint, the elegance of the structure is that it accommodates pooled ownership without forcing investors into active governance. It also avoids some of the friction that comes with more heavily managed entity forms.

For professionals who regularly deal with entity structuring and governance issues beyond DSTs, the broader principles overlap with the business-law issues discussed in corporate and business law matters.

Practical rule: If the client expects control rights that resemble direct ownership, they probably don't want a DST. They want a different structure.

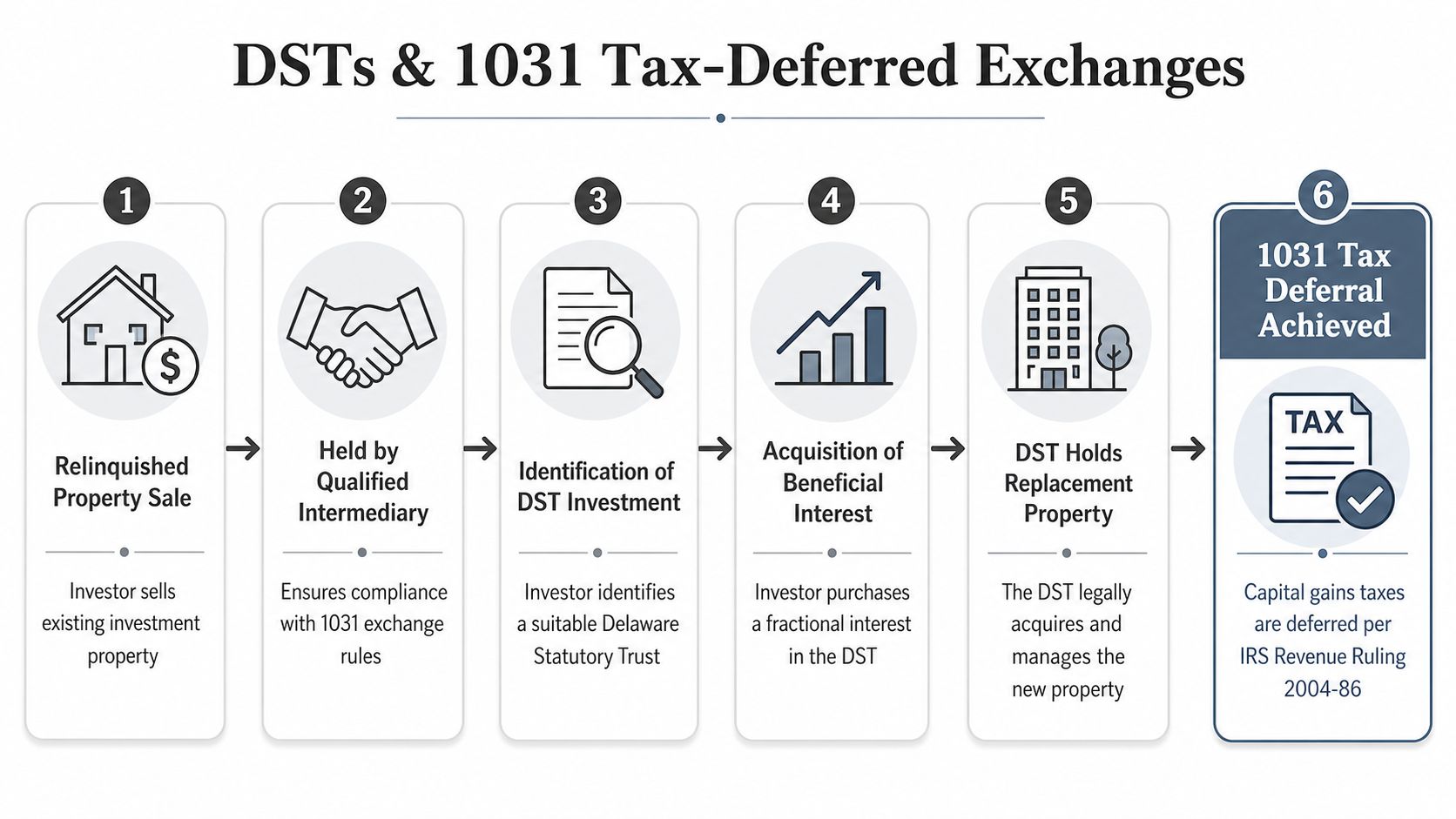

How DSTs Power 1031 Tax-Deferred Exchanges

The reason DSTs matter in practice isn't Delaware entity law by itself. It's federal tax treatment.

A DST became a major 1031 tool because IRS Revenue Ruling 2004-86 treats a properly structured DST beneficial interest as qualifying replacement property for like-kind exchange purposes. That is the legal hinge. Without that treatment, the structure would still exist, but it would not have the same significance for exchangers.

The tax logic

Under Revenue Ruling 2004-86, a beneficial interest in a DST can be treated as direct property ownership for tax purposes when the structure stays within the required passive framework. That treatment is what allows the DST interest to function as like-kind replacement property in a Section 1031 exchange. It lets an investor move from active management into passive, fractional ownership while deferring capital gains. If investors retain managerial control, the interest is reclassified as a partnership interest, which disqualifies it from 1031 eligibility (Origin Investments on DSTs and 1031 exchange investors).

That last sentence is the point many sales presentations move through too quickly. The investor's lack of control is not merely an inconvenience. It is part of what protects the tax result.

How the exchange usually works

In a standard exchange, the sequence looks like this:

- Relinquished property sells. The client disposes of the investment property.

- Qualified intermediary holds proceeds. The client doesn't take constructive receipt of the sale funds.

- DST offering is identified. The investor identifies the DST interest as replacement property within the exchange rules.

- Beneficial interest is acquired. Exchange proceeds are used to purchase the DST interest.

- Trust holds and operates the property. The client becomes a passive beneficial owner rather than an active landlord.

For many clients, this solves the management problem as much as the tax problem. A landlord exiting a small apartment building can shift into a larger institutional-quality asset without taking on tenant relations, repairs, leasing oversight, or local operational issues.

A good DST recommendation usually starts with a client who wants out of operational real estate, not a client who simply likes the phrase “tax deferral.”

Some advisors also need to frame the tax consequences of rental ownership more broadly before deciding whether a DST is the right endpoint. For that purpose, this guide for Texas real estate investors is a useful comparative resource on how property tax benefits and ownership choices interact.

Deal counsel should also watch the purchase and transfer documentation around the exchange itself. The commercial transaction issues surrounding assignment, representations, and closing mechanics often mirror the concerns that appear in a commercial real estate purchase agreement.

Key Benefits for Investors and Their Advisors

DSTs appeal to investors for practical reasons, not theoretical ones. They offer a way to stay invested in real estate while stepping back from active ownership.

For advisors, the main attraction is often administrative simplicity for the client. For the client, the attraction is usually relief. No tenants. No midnight maintenance calls. No need to negotiate a new acquisition under exchange pressure.

The operating advantages

DST investments typically require a $100,000 minimum investment and are commonly structured with a 3 to 10-year holding period. During that period, investors receive passive monthly or quarterly distributions from net rental income, and this passive design is a primary reason advisors use the structure in client wealth planning (Re-Transition on investing in a Delaware Statutory Trust).

That basic structure creates several clear benefits:

- Passive cash flow: The investor receives distributions without acting as landlord or property manager.

- Access to larger assets: Fractional ownership can open the door to institutional-grade property that a single investor might not acquire alone.

- Operational delegation: The sponsor and trust management handle leasing, maintenance, and administration.

- Portfolio flexibility: An exchanger can spread capital across multiple offerings instead of concentrating it in one directly owned asset.

The legal and planning advantages

Lawyers and advisors also pay attention to the legal design. A DST generally gives investors limited liability and separates them from day-to-day operating decisions.

That matters in two ways. First, it aligns with clients who want passive exposure rather than another operating business. Second, it creates a cleaner distinction between ownership economics and management authority than many informal co-ownership structures.

A DST can also fit certain estate and succession planning discussions. Fractional beneficial interests are often easier to discuss and allocate than a single directly owned property with family members who have different goals, different liquidity needs, or different appetites for management responsibility.

What doesn't work

DSTs are a poor fit when the client wants discretion over leasing, refinancing, capital improvements, or sale timing. They're also a poor fit for anyone who treats “real estate investor” as an operating identity rather than an asset-allocation choice.

In other words, the best DST client often isn't the most entrepreneurial one. It's the client who wants continued real estate exposure after an exit from active ownership.

Critical Risks and Due Diligence Checklist

Most DST marketing focuses on tax deferral and passivity. That's understandable, but incomplete. The more serious work starts when you ask what the client is buying economically, not just structurally.

The first underexamined issue is the use of borrowed funds. Investors often assume 50% loan-to-value debt without appreciating that it can reduce cash-on-cash return by 15–25% compared to ownership without debt, and rising interest rates can increase debt burdens and reduce distribution stability (discussion of DST debt structure risk).

That doesn't mean debt financing is always wrong. It means the advisor can't stop at “the client deferred tax and bought institutional real estate.” Debt service changes yield. Refinancing assumptions matter. Distribution expectations can deteriorate even when the property itself seems sound.

The risks advisors should treat as real

Some concerns are obvious, but they still deserve disciplined review:

- Illiquidity: There usually isn't a ready secondary market for beneficial interests.

- Sponsor execution risk: A strong property can still disappoint under weak management or aggressive assumptions.

- Concentration risk: A client may think they're diversified because the asset is large, while remaining concentrated by geography, asset type, tenant profile, or sponsor platform.

- Exit timing risk: The investor usually doesn't control disposition timing.

Other risks are more technical and often missed in client conversations. Fee layers can materially affect investor economics. Offering structure can obscure how much income supports current distributions versus how much relies on assumptions about rent growth, occupancy, financing, or eventual sale conditions.

Investment Structure Comparison

| Feature | Delaware Statutory Trust (DST) | Tenancy in Common (TIC) | Direct Property Ownership |

|---|---|---|---|

| Management | Trustee or sponsor manages the property | Co-owners often must coordinate decisions | Owner manages directly or hires a manager |

| Investor control | Passive, no decision-making control | Shared decision making can create friction | Full control rests with owner |

| Liability profile | Structured for limited liability | Depends on structure and agreements | Direct exposure tied to ownership structure |

| 1031 use | Commonly used when properly structured | Can be used, but coordination is harder | Traditional replacement property |

| Operational burden | Low for investor | Moderate to high because multiple owners must coordinate | High unless fully delegated |

| Suitability | Best for passive exchangers | Better for clients comfortable with shared governance | Best for clients who want control |

A practical due diligence checklist

Before recommending a DST, I'd want the file to show more than product familiarity. I'd want evidence of process.

- Review the PPM closely: Focus on fees, debt terms, conflicts, reserves, distribution policy, and exit assumptions.

- Stress test the financing: Ask what happens to investor distributions if interest expense or operating costs move against projections.

- Evaluate the sponsor: Experience matters, but so do governance, reporting practices, and discipline in sticking to passive operations.

- Analyze the property fundamentals: Don't let the trust wrapper distract from the underlying property. Tenant quality, location, lease rollover, and local demand still drive outcomes.

- Match structure to client objective: A DST should solve a client problem. It shouldn't be used solely because the exchange clock is creating pressure.

For professionals building a defensible recommendation process, the broader discipline involved is the same one discussed in what due diligence means in business transactions.

If your file contains only sponsor materials and a suitability form, your due diligence likely isn't deep enough.

Navigating DST Compliance and Regulatory Minefields

The compliance analysis doesn't stop once you determine that a DST is suitable as an investment. Financial professionals also have to evaluate whether the offering remains suitable as a 1031-compatible investment given how the sponsor operates.

That issue has become sharper because a key projected 2025–2026 compliance risk is the 2024 IRS clarification that DST beneficial interests may lose like-kind status if the sponsor engages in non-passive activities such as property development, and 28% of 2024 DST exchanges reportedly faced audit challenges due to sponsor activity violations (Wikipedia entry discussing Delaware Statutory Trust compliance issues).

A divergence can occur between legal form and real-world conduct. On paper, the trust may look compliant. In operation, sponsor behavior may drift into activities that threaten the passive character necessary for tax treatment.

What advisors should examine in the offering documents

The Private Placement Memorandum is not just a disclosure package. It is the roadmap for understanding what the sponsor plans to do, what discretion it claims, and where the operational boundaries sit.

Review should focus on questions such as:

- What activities does the sponsor reserve the right to undertake?

- Does the business plan look like passive ownership, or does it edge toward development or active repositioning?

- How are fees, conflicts, and related-party relationships disclosed?

- What representations are made about 1031 eligibility, and how carefully are the qualifications stated?

Compliance means more than product approval

For RIAs and brokerage professionals, a DST recommendation sits at the intersection of securities review, tax-sensitive planning, and fiduciary or best-interest obligations. That means process matters.

A defensible process usually includes documented review of the offering documents, documented analysis of the client's need for illiquid passive real estate, and documented scrutiny of compensation and conflicts. If the recommendation is driven by exchange deadline pressure, that pressure should be acknowledged, not hidden.

The compliance problem with DSTs usually isn't that the structure is obscure. It's that the advisor treated a tax-sensitive private placement like a routine product sale.

That's also why firms should align DST review with their broader supervisory framework for regulated advice. The same habits that reduce risk in other fiduciary settings are relevant here, including the disciplines discussed in RIA compliance practices.

Practical Q&A for Financial Professionals

What happens if the DST sponsor goes bankrupt

Start with the documents. The answer depends on the trust structure, the property-level arrangements, and how the sponsor's affiliates are involved. Sponsor distress doesn't automatically mean the estate disappears, but it can disrupt management, reporting, distributions, and exit execution. Advisors should understand who controls servicing, property management, and trustee functions if the sponsor fails.

How are fees and loads usually structured

The answer is offering-specific, which is exactly why the PPM matters so much. Look for organizational fees, selling compensation, asset-management compensation, property-management compensation, acquisition-related charges, disposition-related economics, and any affiliate payments. The key question isn't whether fees exist. It's whether the total structure leaves a reasonable alignment between investor risk and investor return.

How does the exit usually work

Most DSTs are designed to hold property for a defined period rather than indefinitely. The sponsor typically manages toward a sale or other liquidity event, and investors receive their share of net proceeds based on their beneficial interests. The investor generally does not control timing. That's one of the main trade-offs of passivity.

What's the most common professional mistake in DST recommendations

Treating the DST as a tax solution first and an illiquid securities product second. It is both. If the file shows tax urgency but not serious review of financial structure, sponsor conduct, liquidity limits, and client-specific suitability, the recommendation is vulnerable.

When should legal counsel be brought in

Early. Counsel can help evaluate the trust structure, offering documents, control limitations, transaction mechanics, and regulatory exposure before those issues become dispute points.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.