A client calls after seeing a headline about high yields and asks a familiar question: why keep reaching for income in bonds or dividend stocks if Master Limited Partnerships seem to pay more? For a financial advisor, that isn't just an investment question. It's a suitability question, a tax reporting question, and often a future complaint-prevention question.

That's the right way to approach investing in MLPs. The attraction is real. So are the traps. Advisors who treat MLPs like ordinary income securities usually create work for tax preparers, confusion for clients, and avoidable exposure for themselves.

The High-Yield Allure of MLPs

A retiree reviews an account statement, sees bond income falling short, and asks why an MLP yielding more than a traditional dividend stock should not earn an immediate place in the portfolio. For an advisor, that question starts a file review, not a yield comparison.

MLPs attract attention because they can offer meaningful cash distributions along with exchange-traded liquidity. That combination stands out in an income discussion, especially for clients who want current cash flow without selling appreciated positions. It also creates a familiar advisory risk. Clients often focus on the quoted distribution rate before they understand the legal structure, the tax reporting consequences, or the range of outcomes if energy markets, credit conditions, or issuer-specific fundamentals deteriorate.

Why clients get interested fast

Part of the appeal is easy to understand. Charles Schwab's overview of MLPs notes that MLPs are publicly traded limited partnerships commonly tied to natural resource businesses, including oil, gas, coal, timber, and commodity transportation. Many clients translate that into a simple story: hard assets, fee-based operations, and above-average income.

That story is only useful if the advisor adds the missing parts. A pipeline asset may produce stable cash flow in one period and still face contract pressure, refinancing risk, regulatory developments, sponsor conflicts, or distribution cuts in another. High yield can reflect operating strength. It can also reflect market concern.

Practical rule: If the client's first question is yield, your first response should be structure, account type, and tax treatment.

That is also where advisory practice differs from retail enthusiasm. Before recommending an individual MLP, advisors should treat the review as a business investment due diligence process with a suitability overlay. The question is not whether the security looks attractive in isolation. The question is whether the client can reasonably bear the tax friction, price volatility, and administrative complexity that come with owning it.

The advisor's primary duty

For an advisor, investing in MLPs is rarely about finding the highest quoted distribution. It is about matching a complicated security to a client account that can support it and documenting why that recommendation fits.

Three issues usually determine whether the idea belongs in the conversation:

- Tax complexity: The client must be prepared for partnership reporting, basis adjustments, and the possibility that cash received is not the same as taxable income.

- Price volatility: A strong distribution history does not shield the position from sharp drawdowns or changes in market sentiment.

- Administrative burden: Clients need to understand that an “income” holding can still create extra forms, delays, and questions at tax time.

Some clients can accept those trade-offs. Many should not. An MLP recommendation can be suitable, but only if the advisor has identified the income objective, tested the client's tolerance for complexity, and created a record that explains why the recommendation belonged in that account.

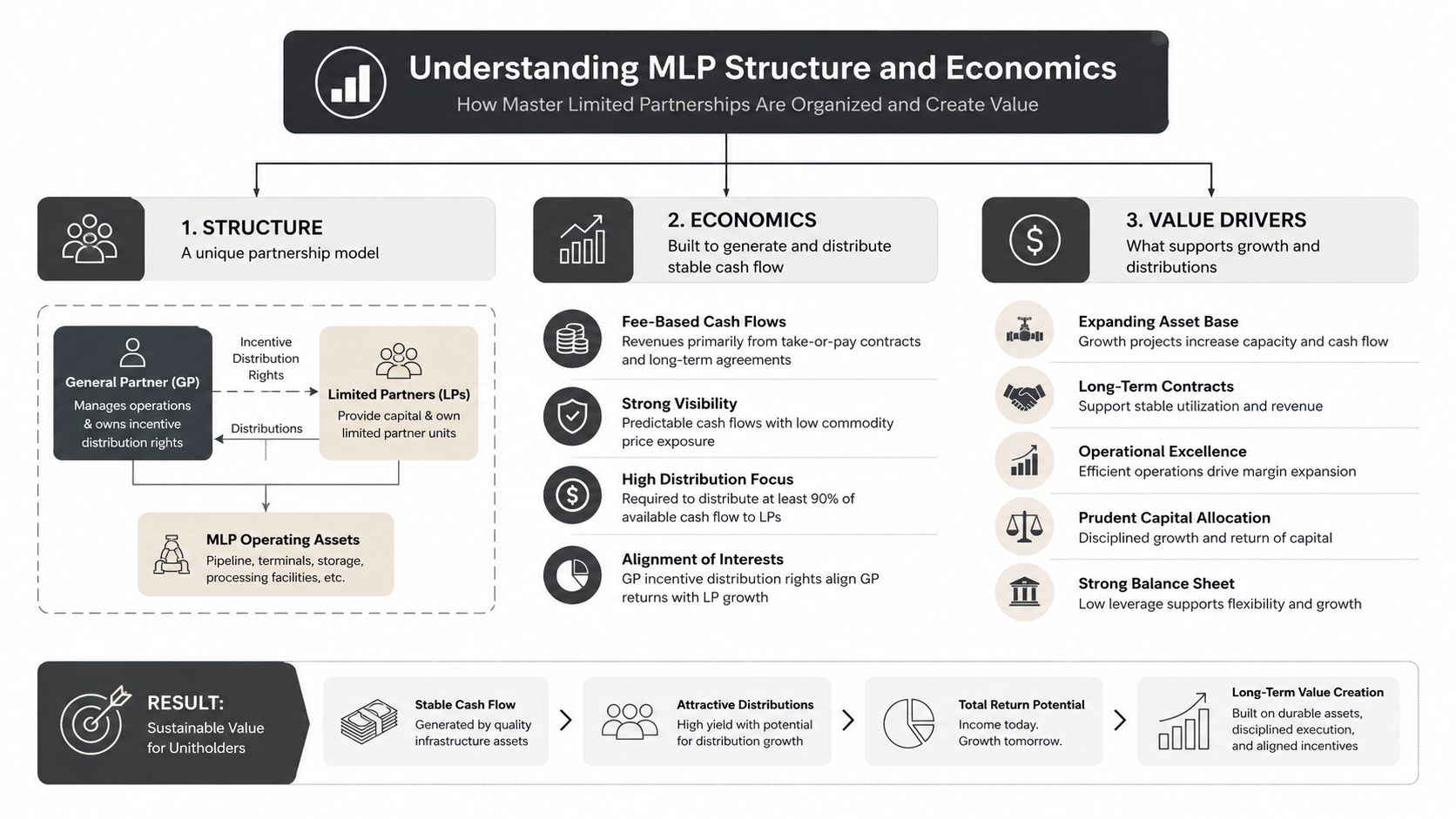

Understanding MLP Structure and Economics

At the legal level, an MLP combines partnership taxation with public trading. That's the key structural feature. The partnership generally functions as a pass-through entity, which means it avoids corporate income tax at the entity level and can distribute more cash to investors than a comparable corporation might.

Most advisors explain this best with an operating asset. Think of a pipeline system or storage network as a toll-based business. The enterprise gathers fees from moving, processing, or storing energy products. After paying operating costs, maintenance needs, and financing obligations, the remaining cash can be distributed to unitholders.

The General Partner and Limited Partner split

Every advisor recommending an individual MLP should understand the difference between the General Partner, or GP, and the Limited Partners, or LPs.

The GP controls management and operations. LPs contribute capital and receive distributions, but they don't run the business. That distinction matters because economic incentives don't always line up cleanly between control and cash flow.

A useful compliance habit is to treat GP incentives as part of due diligence, not as background noise. Governance terms can materially affect distribution policy, growth spending, and conflict management. Advisors who want a broader checklist for evaluating complex structures can borrow a disciplined process from general transaction review practices such as business due diligence principles.

Why Incentive Distribution Rights matter

Some MLPs include Incentive Distribution Rights, or IDRs. These rights increase the GP's participation in cash flow as distributions rise. That can motivate growth, but it can also burden the partnership if the payout structure becomes too expensive.

A concrete example helps. According to Latham & Watkins' MLP primer, when an MLP's quarterly distribution exceeds a certain threshold, such as $0.75, incremental cash flow is often split 50% to limited partners and 50% to the general partner through IDRs.

That waterfall can change the economics of growth materially.

Higher distributions can benefit LPs, but they can also increase the GP's take. Advisors should ask whether growth still creates value for public unitholders after the split.

What works and what doesn't

In practice, the cleaner stories tend to be easier to defend. An MLP with understandable assets, straightforward fee-based operations, and manageable governance is easier to recommend than one with layered incentive rights, sponsor conflicts, or opaque cash flow adjustments.

What usually doesn't work is selling the structure as if pass-through taxation alone solves the investment case. It doesn't. The structure can improve distributable cash flow. It can also create governance tensions that ordinary stock investors never face.

For advisors, that means structure review isn't academic. It's part of the recommendation itself.

The K-1 Conundrum Navigating MLP Tax Reporting

A familiar scenario. The client likes the yield, approves the purchase, and then calls in March asking why the account produced a Schedule K-1 instead of a Form 1099. If that possibility was not addressed before the trade, the tax form becomes the problem, even when the investment thesis has not changed.

For advisors, this is not a minor operational detail. It goes to suitability, informed consent, and documentation. MLPs can serve the right client well, but only if the client understands that partnership tax reporting is part of the product.

Why distributions don't behave like ordinary dividends

Clients often assume the cash they receive will be taxed like a stock dividend. That assumption is usually wrong. MLP cash distributions are often characterized in significant part as return of capital, which generally reduces the investor's tax basis instead of creating immediate taxable income.

That can improve after-tax cash flow during the holding period. It also creates work. Lower basis can increase taxable gain on sale, and part of that gain may not receive the capital-gain treatment the client expected. Advisors should explain the tax deferral benefit and the exit cost in the same conversation.

A clean explanation helps: the account statement shows cash received, but taxable income, basis adjustments, and ultimate gain recognition often follow a different timeline.

The sale-year surprise

Disposition is where misunderstandings usually surface. A client may hold an MLP for years with little concern, then discover that the tax reporting on sale is much more complicated than the annual distributions suggested.

One point worth stating clearly is passive loss treatment. According to Baird's FAQ on taxation of MLPs, ordinary losses from an MLP are generally treated as passive losses and can offset passive income, but suspended losses may become deductible when the entire interest is sold in a taxable transaction.

That is why year-one tax impressions can be misleading. The full tax result often cannot be evaluated until disposition.

If the file does not show that these sale-year consequences were discussed, the advisor has a preventable client-relations problem and, in a bad fact pattern, a risk that later gets framed as inadequate disclosure or even securities fraud under applicable standards.

State filings and account placement

K-1 reporting also raises practical issues outside federal income tax. Because an MLP may have operations in multiple states, some clients and their preparers will need to assess whether nonresident filing obligations apply. The answer depends on the partnership's activity, the client's overall tax profile, and state-specific thresholds.

This is where advisor judgment matters. Some households will accept that burden in exchange for the income profile and tax deferral characteristics. Others will not, especially if they already have complicated returns, multiple entities, or a low tolerance for CPA coordination.

A useful pre-trade discussion usually covers:

- Tax preparer readiness: Confirm whether the client's CPA regularly handles partnership K-1s and multi-state questions.

- Basis tracking over time: Longer holding periods can improve the economics, but they make adjusted basis and sale planning more important.

- Administrative tolerance: Some clients are unsuitable for direct MLP ownership because they do not want extra forms, delayed tax reporting, or state-filing analysis.

Retirement accounts deserve extra caution

Retirement accounts require a separate analysis. Advisors should not treat an IRA purchase of an MLP as interchangeable with a taxable account purchase, because partnership income inside tax-advantaged accounts can raise issues that clients do not anticipate.

The prudent practice is to avoid slogans. An MLP is not automatically appropriate or inappropriate for retirement accounts. The account type changes the tax analysis, and that analysis may require input from the client's CPA or tax counsel before the order is entered.

The client communication standard

The best explanation is direct. This is a publicly traded security that uses partnership tax reporting. Cash distributions may not match taxable income. Basis can decline over time. Sale treatment can differ from what the client expects. State tax questions may arise.

For an advisor, the test is simple. Can the client repeat those points back in plain English and still want the position? If not, the issue is not yield. The issue is suitability.

Evaluating the Risk and Return Profile of MLPs

A client sees a double digit yield on an MLP and asks for a quick yes or no before the close. That is usually the wrong framing. The advisor's job is to determine whether the distribution is durable, whether the business can carry its debt through a weaker cycle, and whether the recommendation can be defended later if the position breaks down.

Yield is only the starting point. In practice, the better question is whether the partnership generates stable cash flow from assets and contracts the advisor can explain in plain English. If the investment case depends on optimistic commodity assumptions, repeated access to capital markets, or management's willingness to hold the payout steady despite thin coverage, the headline yield is doing too much work.

Focus on the mechanics that support the payout

Start with distribution coverage. Advisors do not need a complicated model to identify weak support. They need to see whether cash available for distribution leaves a reasonable cushion after maintenance needs, debt service demands, and ordinary operating pressure. A payout that is barely covered can become a client relations problem quickly when volumes soften, contracts get repriced, or refinancing costs rise.

Then look at the cash flow mix. Midstream MLPs are often described as fee based, but that label can hide real differences. Some systems are backed by long term contracts with stronger counterparties. Others are more exposed to throughput declines, basin concentration, producer stress, or incentive conflicts with sponsors. Those differences matter more than the marketing label.

Balance sheet discipline belongs in the same review. An MLP can appear stable until the financing window narrows. If the partnership depends on regular debt issuance or equity raises to fund growth and support the distribution, a tighter credit market can change the risk profile fast.

A due diligence frame advisors can defend

For client accounts, I would want the file to answer four practical questions:

- How is the partnership paid? Asset level cash flow should be understandable without resorting to broad sector slogans.

- What could impair distributions? Contract renewals, volume declines, counterparty weakness, rate sensitivity, and refinancing needs should all be considered.

- Does management allocate capital with discipline? Distribution policy, growth spending, and borrowing targets should point in the same direction.

- Can the advisor explain the downside clearly? If the risk explanation is vague, the recommendation is not ready.

That process helps with more than investment selection. It also helps with supervision and documentation. Advisors who recommend concentrated income products without a clear record of their analysis often face the same fact pattern seen in securities fraud disputes involving suitability and disclosure failures.

Risks clients often misread

Clients often hear “infrastructure” and assume bond-like stability. MLPs are still equity securities. They can be sensitive to energy production trends, contract quality, capital market conditions, interest rates, and management execution. Price volatility can be sharp even when the underlying assets seem straightforward.

Correlation risk also deserves attention. A client who already has heavy exposure to energy equities, high yield credit, or regional economic drivers may be adding more concentration than intended by buying an MLP for income. From an advisor's perspective, that suitability issue is often more important than whether the quoted yield looks attractive in isolation.

Cross-border comparisons can also confuse clients. A client reading about pooled structures overseas may assume the same legal and economic features apply here. They do not. Even a basic discussion of understanding Australian MIS shows why advisors should avoid treating different collective investment structures as interchangeable.

A simple rule works well in practice. If the advisor cannot explain where the cash comes from, what threatens it, and why this client should bear those risks, the position should stay off the blotter.

Investment Vehicles Individual MLPs vs Funds and ETFs

The investment decision isn't just whether a client should own MLP exposure. It's also how they should own it. For many advisors, the better recommendation turns less on market outlook and more on tax reporting, complexity tolerance, and operational fit.

Owning individual MLP units gives the client direct exposure to the partnership structure. That may preserve the tax features clients find attractive, but it also brings K-1 reporting and the basis issues discussed earlier. A fund wrapper can simplify administration, but simplification often comes at a cost.

The real trade-off is convenience versus purity

An individual MLP is usually the cleaner way to access the actual partnership economics. A fund can offer diversification and easier client servicing. But many packaged MLP products introduce structural drag, especially where the vehicle doesn't transmit partnership economics in a fully efficient way.

Advisors must be precise with language. “ETF” doesn't automatically mean tax efficiency. “Fund” doesn't automatically mean simpler in every respect. Some products are easier for clients to hold and report. That doesn't mean they replicate direct ownership cleanly.

Comparison of MLP Investment Vehicles

| Feature | Individual MLPs | MLP Funds (ETFs, ETNs, etc.) |

|---|---|---|

| Tax reporting | Usually K-1 based | Often easier client-facing reporting, depending on structure |

| Diversification | Single-issuer exposure unless multiple positions are built | Broader exposure in one position |

| Administrative burden | Higher | Lower in many cases |

| Tax efficiency | Can preserve direct partnership treatment | May introduce structural tax drag |

| Client education need | High | Still important, but often easier to explain |

| Best fit | Taxable clients who can handle complexity | Clients who want exposure with less direct reporting friction |

When direct ownership makes sense

Direct ownership often works best when the client has a taxable account, uses a capable CPA, and understands that partnership reporting is part of the package. These clients usually care about the underlying economics enough to accept the friction.

Advisors in that situation should still be careful about concentration and sponsor-specific issues. Simplicity at the portfolio level matters. Too many small MLP positions can create a bookkeeping problem that outweighs the investment case.

When a fund wrapper may be the better answer

Fund vehicles often fit clients who want exposure to the segment but don't want to deal with individual K-1s. That can be a perfectly sensible advisory choice. It just needs to be clearly presented. The wrapper may reduce administrative pain while changing the economic and tax profile.

For advisors who work across alternative pooled structures, it can help to compare MLP packaging to other managed structures in different jurisdictions. A concise explainer on understanding Australian MIS is useful because it highlights a broader principle: the wrapper around an asset can materially change investor rights, tax treatment, and governance dynamics.

What to document in the file

When choosing between individual units and a fund, document why the selected vehicle fits the client better than the alternatives. That note should address:

- Reporting preference: Did the client explicitly reject K-1 complexity?

- Diversification need: Was the client better served by broad exposure rather than security selection?

- Account type: Did the account structure influence the recommendation?

- Servicing practicality: Will the chosen vehicle reduce future confusion and complaint risk?

Advisors often think of vehicle selection as implementation. Regulators often see it as part of suitability.

Advisor Compliance and Client Suitability

MLPs are the kind of product that test whether an advisor's process is real or cosmetic. A recommendation can look reasonable on paper and still fail under scrutiny if the file doesn't show why this client, in this account, at this time, should have owned this product.

For brokerage professionals, that starts with FINRA Rule 2111 and the basic suitability framework. A complex, tax-sensitive, income-oriented security requires more than a risk-tolerance shorthand. It requires evidence that the advisor evaluated the client's objectives, financial profile, liquidity needs, investment horizon, and ability to understand the product's practical burdens.

The questions that should always be asked

Advisors should ask more than whether the client “wants income.” That's too broad to be useful.

The better set of questions looks like this:

- Income objective: Does the client need current cash flow, or are they seeking yield?

- Tax tolerance: Will the client accept K-1 reporting, basis adjustments, and possible state filing complications?

- Volatility capacity: Can the client hold through sharp price swings without forcing a sale?

- Time horizon: Is this intended as a long-term taxable-account holding, or is the client likely to trade around it?

If the answer to any one of those questions is shaky, the recommendation should slow down.

Documentation is part of the recommendation

A surprising number of suitability disputes don't arise because the product was indefensible. They arise because the conversation wasn't documented. If a client later complains that they never understood K-1 reporting or the possibility of price volatility, the contemporaneous note often decides the credibility battle.

A clean file should include the recommendation rationale, the account-type analysis, and the client's acknowledgment of tax complexity. Advisors operating under a registered investment adviser model should also keep current on RIA compliance practices because disclosure, supervision, and documentation standards tend to converge when products become more complex.

If you'd be uncomfortable reading your suitability note out loud in arbitration, the note probably isn't finished.

Where advisors get into trouble

Most MLP-related advisor risk comes from one of four mistakes:

- Overselling yield and understating structural complexity.

- Ignoring tax fit because the client has a general accountant.

- Using retirement accounts casually without careful analysis.

- Failing to memorialize the conversation in a way a reviewer can follow.

These aren't theoretical concerns. They're the kinds of weaknesses that appear in customer complaints, internal supervision reviews, and post-termination disputes involving product recommendations.

The suitability standard should be stricter than the sales pitch

A seasoned advisor should apply a higher standard than “the client agreed.” Consent isn't a substitute for process. If the client doesn't understand why MLP distributions, K-1s, and sale-year tax effects make this product different from ordinary dividend securities, the recommendation remains vulnerable.

The strongest practice is to treat investing in MLPs as a documented exception process. Not because MLPs are improper in themselves, but because they are easy to misunderstand and easy to oversimplify.

Implementing MLP Exposure for Clients

Once the suitability work is done, implementation should stay disciplined. MLPs generally work best as deliberate holdings, not as impulsive yield substitutions.

A practical advisor checklist

Start with the client record. Confirm that the file clearly reflects why MLP exposure fits the account and why the client can tolerate the reporting burden. If the tax conversation hasn't happened in plain language, stop there and have it before entering the order.

Then choose the vehicle. For some clients, that will mean direct ownership of an individual partnership in a taxable account. For others, a fund structure will be the better operational fit because it reduces direct reporting friction even if it changes the economics.

Next, size the position conservatively. MLP exposure usually makes the most sense as a satellite holding, not the foundation of the client's income plan. That helps keep any single product's tax and volatility profile from overwhelming the portfolio.

Set expectations before the first statement arrives

Clients should know three things before they own the position:

- Market value will move: A high distribution doesn't immunize the security from drawdowns.

- Distributions can change: Income is not guaranteed solely because it has been consistent historically.

- Tax reporting will require patience: K-1 timing and basis consequences are part of ownership.

That conversation should be written down. It's just as important as the trade ticket.

Supervision after purchase

The advisor's work doesn't end after the recommendation. Holdings like these deserve periodic review for continuing suitability, especially if the client's account type, tax posture, or liquidity needs change. Advisors involved in outside deals or heightened product scrutiny should also understand the compliance risks around private securities transactions, because product complexity and supervisory issues often intersect.

A good MLP process is straightforward. Know the structure. Respect the tax consequences. Match the vehicle to the client. Document the recommendation like someone else will read it later, because one day someone probably will.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.