You're probably in one of two positions right now. You've accepted, or are chasing, a role with a broker-dealer, bank program, or insurance platform, and someone has told you that you need the Series 6 and Series 63. Or you already work in the industry and you've realized that licensing isn't just about passing exams. It's about registration status, supervision, disclosures, and avoiding mistakes that follow you from firm to firm.

That confusion is normal. New entrants hear SIE, Series 6, Series 7, Series 63, Form U4, Form U5, Blue Sky law, and FINRA inquiry, often in the same week. The risk is that people treat licensing like a checklist item when it's really the beginning of their regulatory record. If you want a practical overview of the broader career path into brokerage work, this overview on how to become a stock broker gives useful context.

A proper understanding of the Series 6 and 63 license path matters because these registrations control what you can sell, where you can sell it, and how exposed you are if something goes wrong with your firm, your paperwork, or your disclosures.

Your First Step in the Securities Industry

A new advisor often starts with the wrong question. They ask, “Which test is easiest?” The better question is, “What business am I legally allowed to conduct once I'm registered?”

That distinction matters. A bank-based representative selling mutual funds has a different licensing need than a wirehouse trainee who expects to handle individual stocks and bonds. An insurance professional adding variable products has different constraints than a fee-based planner moving toward investment advisory work. If you misunderstand that from the start, you can waste time, delay hiring, or accept a role that doesn't match your intended practice.

Where most people get stuck

The first choke point is timing. Many candidates assume every securities exam requires employer sponsorship. That isn't true across the board. Others believe that once they pass a product exam, they're ready to solicit clients. That also isn't true. Passing an exam and becoming properly registered are related, but they aren't the same event.

A second problem is treating licensing as purely academic. It isn't. Every registration step creates a compliance footprint. Firms file forms. Regulators see attempts, affiliations, and disclosures. Future employers review that history.

Start your licensing path as if a future branch manager, compliance officer, and regulator will all read the file later. Because they might.

What actually matters at the beginning

Three issues deserve your attention early:

- Product scope: Your license determines what securities business you can conduct.

- State authority: Your registration status determines where that business can occur.

- Disclosure quality: The information tied to your industry registration can become a long-term career issue if it's incomplete or inaccurate.

For most entry-level professionals focused on packaged securities, the Series 6 and Series 63 sit at the center of that framework. One addresses product authority. The other addresses state law authority. Neither should be viewed in isolation if your goal is a compliant and durable practice.

Decoding the Series 6 License

The Series 6 license is a limited, product-focused registration. It's designed for representatives who will handle packaged securities rather than the full menu of general securities products.

Under the licensing requirements summarized by AB Training Center, the Series 6 covers packaged securities including mutual funds, unit investment trusts, variable annuities, and variable life insurance products, and it does not permit the sale of individual equities or bonds, which require the broader Series 7 license. The same source states that the FINRA Series 6 exam consists of 50 scored questions to be completed in 90 minutes. A passing score of 70% is required, and candidates must first pass the Securities Industry Essentials (SIE) exam and obtain sponsorship from a FINRA-member firm (Series 6 and 63 licensing requirements).

What the license actually lets you do

For many candidates, precision is essential. The Series 6 is useful if your role centers on packaged investment products. It fits many bank programs, insurance-affiliated channels, and entry-level investment company roles.

It does not turn you into a broad-based securities representative. If your business plan includes individual stocks, corporate bonds, or a wider transaction set, the Series 6 won't get you there.

Typical uses for a Series 6 holder

- Mutual fund business: Suitable for representatives building client allocations through fund families and packaged investment programs.

- Variable product sales: Common for insurance professionals who want to offer variable annuities or variable life products.

- UIT and similar packaged offerings: Useful where the firm's platform is structured around packaged securities rather than open architecture brokerage activity.

Why sponsorship is the real gatekeeper

A lot of candidates think the exam is the main hurdle. It isn't. The bigger operational hurdle is firm sponsorship.

Your sponsoring firm files your Form U4 and establishes your eligibility to sit for the Series 6. That means employment, onboarding timing, and internal firm approval all directly affect your licensing schedule. If a firm moves slowly on paperwork, your testing date moves. If there's a registration concern, the process can stop before you ever reach the testing center.

Practical rule: Don't resign from one role or make promises to clients based on an expected Series 6 exam date until your sponsorship and registration steps are actually in motion.

Candidates who want a better sense of exam difficulty before they commit should review this discussion of the pass rate for Series 6.

What works and what doesn't

What works is aligning the Series 6 with a narrow, realistic business model. What doesn't work is using it as a placeholder while expecting Series 7-type authority. That mismatch causes frustration with clients, branch supervision, and production expectations.

If your future book will revolve around packaged securities, the Series 6 is efficient. If not, it may be a detour.

Understanding the Series 63 License

A representative joins a new firm, starts calling prospects in multiple states, and assumes the hard part is over because product training is complete. Then compliance asks a basic question: are you properly registered for the states where those contacts are happening? That is the practical role of the Series 63.

The Series 63 centers on state securities law. In practice, that means agent registration, notice requirements, prohibited conduct, and the rules that govern how you interact with prospects and clients at the state level. If the Series 6 is tied to a limited product set, the Series 63 is tied to whether your activity is lawful in the jurisdictions where you do business.

That distinction matters more than many candidates expect. I have seen representatives focus on passing exams and miss the larger risk. A license is only part of the registration picture. Your Form U4 disclosures, the states where the firm seeks registration, and any later amendments can determine whether you are cleared to act, delayed in onboarding, or facing follow-up questions from regulators.

Why the Series 63 matters in real practice

Blue Sky law affects ordinary conduct. Calling a prospect, discussing a securities transaction, changing firms, or expanding into a new state can all raise registration questions. Firms care about the Series 63 because state regulators care about the conduct behind the license, not just the exam result.

That is also why this exam deserves more respect than it usually gets.

Candidates often treat it as a box to check. From a legal and compliance standpoint, it is an early test of whether you understand the rules that later show up in branch audits, customer complaints, and regulatory reviews. The exam itself is manageable. The consequences of misunderstanding the underlying rules are not.

Why some candidates take it before joining a firm

The Series 63 can be taken without first completing the SIE or obtaining firm sponsorship. For job seekers, that creates a practical option. Passing it in advance can make you more attractive to employers because it shortens one part of the registration timeline and shows that you take compliance seriously.

Still, there is a trade-off. Passing the exam does not solve the harder issues that delay registrations in practice. If your U4 includes disclosures about financial events, terminations, customer disputes, or criminal matters, the legal review can become more important than the test score. Candidates comparing broader registration paths should also review how the state-law exam fits against a full general securities track in this guide to Series 63 vs Series 7 licensing differences.

What the exam is really screening for

The Series 63 rewards careful reading and disciplined judgment. It tests whether you can identify who must register, what conduct is prohibited, and how ethical obligations apply under state law. Product knowledge helps less here than many candidates expect.

That difference catches people off guard. Strong sales candidates sometimes move too quickly through questions and miss legal qualifiers that change the correct answer. Candidates with prior exposure to compliance, supervision, or legal review often perform better because they are trained to read the facts closely.

For a new or transitioning advisor, the bigger point is straightforward. The Series 63 is not just a state-law quiz. It is your first real introduction to the regulatory framework that can later affect your U5 wording, trigger a FINRA inquiry, or complicate a move between firms if your record is not handled carefully.

Series 6 vs Series 63 A Direct Comparison

The simplest way to think about the Series 6 and 63 license pairing is this: one governs what you may sell, and the other governs whether you're properly cleared under state law to conduct that business.

Professionally, that means these licenses are complementary, not interchangeable. One without the other often leaves a representative only partially useful from an operational standpoint. If you're trying to compare broader licensing paths, this analysis of Series 63 vs Series 7 helps frame where each exam fits.

Series 6 vs. Series 63 At a Glance

| Attribute | Series 6 License | Series 63 License |

|---|---|---|

| Primary purpose | Product authority for packaged securities | State law authority for securities agent activity |

| Focus of exam | Packaged products and representative functions tied to them | Blue Sky law, registration, ethics, fiduciary obligations |

| Who develops/administers it | FINRA-administered qualification exam | NASAA-developed, FINRA-administered exam |

| Prerequisites | Requires SIE first and firm sponsorship with Form U4 filing | No prerequisites |

| Business value | Lets you handle a limited category of securities products | Lets you satisfy state law qualification expectations tied to solicitation and business activity |

| What it doesn't do | Doesn't authorize broader general securities activity | Doesn't give product-selling authority by itself |

Why both usually matter

A representative with only a Series 6 may have product knowledge and limited product authority but still lack the state-law qualification usually expected for doing business in a jurisdiction. A candidate with only a Series 63 may understand state rules but still lack authority to sell the packaged products the role requires.

That's why firms so often treat them as a pair.

A practical way to remember the distinction

- Series 6: “Can I offer this type of product?”

- Series 63: “Am I legally cleared to act as an agent under state law where I'm doing business?”

That difference becomes important in supervision, branch audits, and internal licensing reviews. Managers don't just ask whether an exam was passed. They ask whether the person is properly registered for the exact activity they're performing.

The trade-off candidates miss

Some people dismiss the Series 63 because it doesn't sound product-heavy. That's a mistake. From a risk perspective, state law failures can be as damaging to a career as product suitability problems.

Others treat the Series 6 as enough because it sounds like the “main” license for a packaged-products role. That also misses the point. Product authority without proper jurisdictional compliance can create avoidable regulatory exposure.

Think of the pair as two keys. One opens the product door. The other opens the state-law door. You usually need both before you should be speaking to clients about actual securities business.

Navigating Regulatory and Compliance Risks

Passing exams is the easy part compared with protecting your record. The significant risk starts once your registrations, affiliations, and conduct become part of the industry file that regulators and future firms can review.

Form U4 and Form U5 issues sit at the center of many avoidable career problems. New advisors often don't appreciate how much those records matter until a firm change, internal investigation, or customer issue puts them under scrutiny.

Why registration paperwork is not clerical

The Form U4 is not a harmless onboarding document. It's a regulatory filing. It ties your exam history, employment record, and disclosures to your industry registration.

The Form U5 matters just as much on the back end. When you leave a firm, that filing can shape how future employers, state regulators, and FINRA view your departure. A poorly worded termination explanation, allegations of policy violations, or unresolved compliance concerns can become the trigger for additional review.

Common pressure points

- Employment transitions: Departing under stress, especially during a recruiting dispute or internal review, often leads to disclosure fights.

- Supervisory concerns: A branch issue can become your issue if activity occurred under your rep code or login.

- Customer complaints: Even a matter that never becomes formal discipline can still create disclosure and reputational consequences.

Exam issues can become record issues

Candidates sometimes assume a failed exam is just a private setback. It isn't always treated that casually in professional settings. Testing history, registration timing, and onboarding delays can all become part of how a firm evaluates you.

The more serious problem is when someone tries to “clean up” the story by omitting facts, misstating timelines, or being careless in regulatory paperwork. A failed attempt is usually manageable. A disclosure inconsistency is much harder to defend.

A regulator can tolerate a poor result more easily than a misleading explanation.

When a licensing problem turns into an investigation

Legal risk arises from situations like a disputed Form U5, an allegation of outside business activity, a question about sales practice conduct, or an inconsistency in registration paperwork. These can trigger requests for information from FINRA or a state regulator.

If the inquiry expands, the consequences can affect far more than one license. It can disrupt a move to a new firm, delay re-registration, create disclosure obligations, and force you to explain the matter to every future employer. Conduct that looks minor inside a branch often looks different once it appears in a regulatory file. For broader context on the kinds of conduct issues that can pull a representative into deeper scrutiny, this discussion of what is securities fraud is worth reviewing.

Risk mitigation that actually works

The best defense is disciplined recordkeeping and early judgment.

Focus on these habits

- Read every filing before it goes live: Don't assume HR, compliance, or your manager captured the facts accurately.

- Document departures carefully: If you're leaving amid a dispute, preserve communications and understand how the firm intends to characterize the separation.

- Escalate before improvising: If a complaint, inquiry, or supervisory issue surfaces, get advice before sending explanatory emails or making casual statements to a regulator or firm investigator.

People get into trouble when they confuse speed with cooperation. Prompt responses matter, but accurate and strategically framed responses matter more.

Practical Next Steps for Your Licensing Journey

Most candidates benefit from a straightforward plan. Get the employment path right, keep your paperwork clean, and avoid creating delays that are entirely preventable.

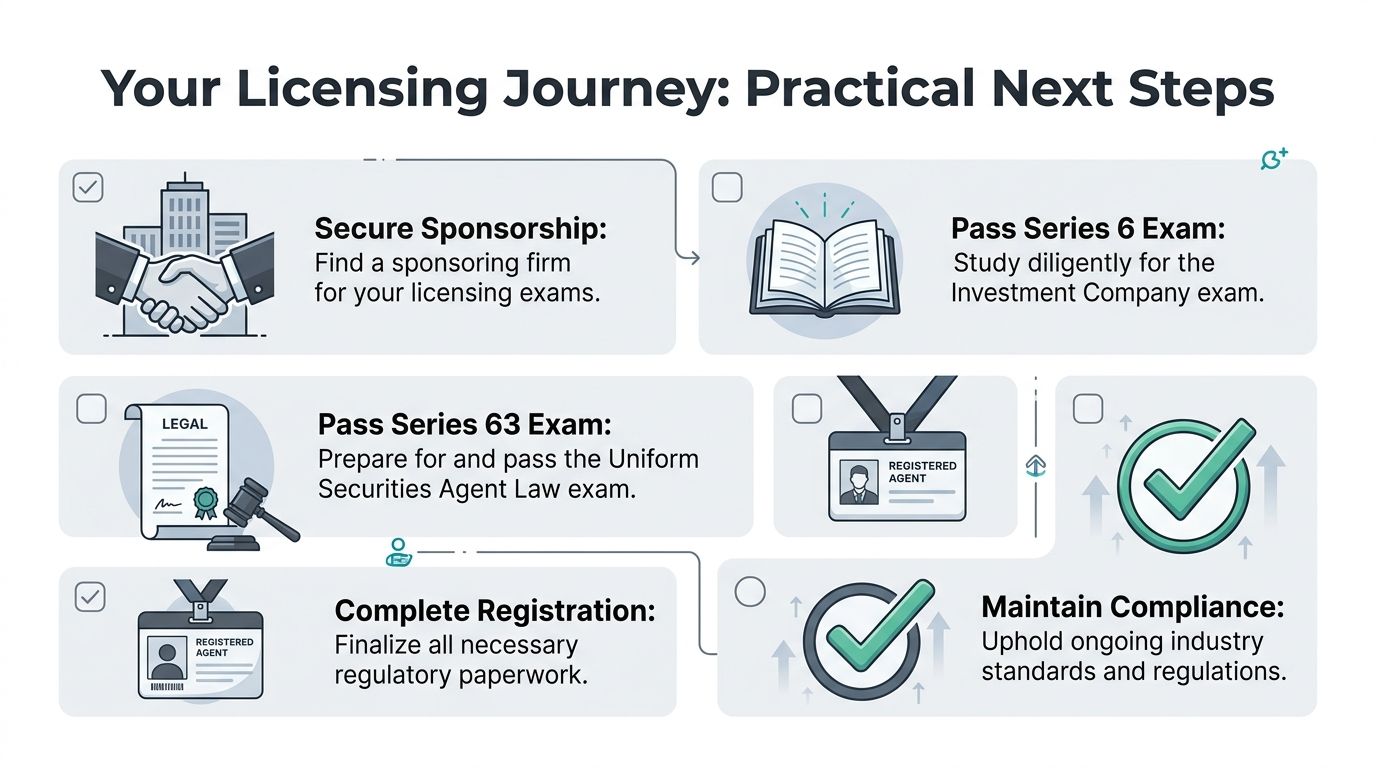

The standard path

For many new entrants, the ordinary sequence is simple:

- Find a sponsoring firm. The Series 6 requires sponsorship and U4 filing.

- Pass the SIE. It's the prerequisite gateway before the Series 6.

- Prepare for the Series 6. Focus on packaged products and the role-specific rules tied to them.

- Complete the Series 63. This addresses the state-law side of your registration profile.

That route works well if you already have an offer and the firm is organized.

The underused shortcut that can help in hiring

There's also a smart variation for candidates who are still job hunting. Achievable notes that a common but under-publicized strategy for new entrants is to pass the unsponsored Series 63 exam independently. This allows them to demonstrate commitment and regulatory knowledge to potential sponsoring firms, potentially shortening their time-to-hire by several months (Achievable discussion of unsponsored licensing exams).

That strategy works especially well for candidates trying to stand out in competitive entry-level pools. It won't replace sponsorship for the Series 6, but it can remove one obstacle from the firm's onboarding process.

A practical way to organize your first months

Instead of treating this like one big academic project, break it into operational tasks.

A useful checklist

- Before accepting a role: Confirm what product line you'll handle. Don't assume “financial advisor” means the same thing at every firm.

- During onboarding: Review your U4 carefully. Names, dates, addresses, prior employment, and disclosures all matter.

- While studying: Match your exam prep to the license's purpose. Product material for the Series 6. Legal and ethical framework for the Series 63.

- After passing: Confirm that registration steps are complete before doing anything that could be viewed as solicitation or securities activity.

- In your first months at the firm: Learn escalation channels for complaints, exceptions, email review, and outside activity approvals.

The fastest path isn't the one with the earliest exam date. It's the one with the fewest registration errors, disclosure problems, and onboarding surprises.

What doesn't work

What usually fails is improvisation. Candidates guess at disclosure answers, rely on verbal statements from managers, or assume the firm will fix any registration problem later. That approach creates avoidable exposure.

A better approach is to act like a regulated professional before you're fully productive. That habit tends to carry forward when the stakes get higher.

Frequently Asked Questions for Brokerage Professionals

A candidate passes the exam, accepts the offer, and assumes the hard part is over. Then compliance reviews the U4, a prior termination needs clarification, or a state registration issue stalls the start date. That is why these questions matter. The exam itself is only part of the licensing risk.

If I have a Series 7 license, do I still need a Series 6 and 63

In most cases, no one asks a Series 7 holder to get a Series 6. The Series 7 is broader, so the Series 6 usually adds nothing from a permissions standpoint.

The Series 63 is different. A broader product license does not replace state law registration requirements. If your role involves securities business in a state that requires the Series 63 or an accepted alternative, the firm will still focus on that piece before letting you act.

The practical risk is assuming your existing license answers every onboarding question. It does not. Firms look at exam history, state registration, disclosures, and whether your approved activities match the job you were hired to do.

What happens if I fail the Series 6 or Series 63 exam

A failure usually creates a timing problem before it creates a legal problem. Start dates get pushed, training schedules change, and some firms begin asking whether the candidate is still the right fit for the seat.

Repeated failures create a second issue. They can affect how supervisors and recruiters view readiness, especially if the candidate was already under pressure to become registered quickly. I have seen firms stay patient with one failed attempt and become far less flexible when the pattern continues.

Treat the exam like part of your compliance file. It may not be a disclosure event by itself, but it can shape how your judgment and preparation are viewed during hiring and supervision.

Can I really take the Series 63 before finding a job

Yes. Because the Series 63 does not require firm sponsorship, taking it before you join a broker-dealer can make sense.

That said, passing early does not solve everything. It does not activate registration on its own, and it does not fix disclosure problems, outside business activity questions, or a messy employment record. Candidates sometimes overestimate how much one passed exam will offset a complicated U4 review. It will not.

If you expect to work with retirement clients, it also helps to understand the planning mistakes that often drive client complaints and product suitability questions. A plain-English consumer resource is Gold IRA Association's retirement advice.

What should I worry about more than the exam itself

The forms.

A sloppy U4 causes more trouble than many candidates expect. Dates that do not line up, incomplete employment history, omitted liens or judgments, unclear termination language, and half-answered disclosure questions can trigger delays or follow-up requests. If the issue is serious enough, it can also lead to internal escalation, amended filings, or regulatory scrutiny later.

The same goes for the U5. If you are changing firms and your prior departure involved allegations, customer complaints, or policy issues, get clear on what was filed before you submit new paperwork. Waiting until after a regulator or hiring firm asks questions limits your options.

Should I get legal advice during the licensing process

Sometimes, yes. This is especially true if any of the following apply: a prior firing, a resignation under review, a customer complaint, a financial disclosure issue, a criminal matter, or a proposed U5 statement you believe is inaccurate or misleading.

Brokerage professionals often wait too long because they assume the issue is minor or temporary. That is a mistake. Once a disclosure is filed and questions start coming in, correcting the record gets harder and more expensive.

If you are dealing with a FINRA inquiry, a disputed Form U5, or an employment-related registration problem, get advice before you answer casually or sign paperwork you have not reviewed closely.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.