A new client wants to move substantial assets into your practice. The account-opening conversation sounds polished. The client has multiple entities, funds are coming from different institutions, and the explanation for the source of wealth is technically plausible but hard to follow. Nothing is obviously unlawful. Still, your staff has questions, and your forms don't quite capture what matters.

That's where many independent advisors and smaller broker-dealers find themselves. Not in a dramatic crime story, but in the gray zone where incomplete diligence, weak documentation, and generic procedures create real exposure. A sound anti-money laundering compliance program gives your firm a disciplined way to handle that moment. It helps you decide what to collect, what to escalate, what to document, and when to stop treating a problem as a relationship issue and start treating it as a compliance issue.

For smaller firms, the challenge usually isn't understanding that AML matters. It's building a program that fits the business you operate. A practice serving a handful of high-net-worth households, a hybrid advisory business, and a small introducing broker don't face the same operational risks. If your controls don't match your model, regulators will see the mismatch quickly.

Why AML Compliance Is a Critical Priority for Your Practice

An advisory firm often encounters AML risk at the exact point where business pressure is highest. A new relationship looks promising. The client may bring prestige, assets, and referrals. The onboarding team wants to move efficiently. That's also when warning signs get rationalized away.

A practical AML program forces a different response. It requires your firm to ask basic but uncomfortable questions. Who is the true customer? Who controls the entity? Why does the money path look more complicated than the client's stated investment objective? If your team can't answer those questions cleanly, speed is no longer the priority.

For independent advisors, the reputational risk is personal. Clients often hire the advisor, not the brand. If a suspicious relationship later becomes the subject of scrutiny, the issue doesn't stay inside a compliance file. It affects trust, referrals, recruiting, and transitions to future firms. The broader framework of regulatory compliance for businesses matters here, but AML is where theory turns into daily judgment calls.

Where smaller firms get exposed

Large institutions can absorb friction. Smaller firms usually can't. That's why weak spots tend to show up in predictable places:

- Client acceptance pressure: Revenue goals can overpower skepticism.

- Thin staffing: One person may wear operations, supervision, and compliance hats.

- Template dependence: Firms adopt written procedures that don't reflect how accounts are really opened and serviced.

- Escalation gaps: Staff sees something odd but doesn't know who owns the decision.

A compliant process isn't the same thing as a usable process. If your front-line team can't follow it under deadline, it will fail when you need it most.

What works in practice

The firms that handle AML well usually do three things consistently. They tailor onboarding questions to their actual client base. They train staff to identify inconsistencies, not just complete forms. And they document why a risk was accepted, escalated, or declined.

That matters because AML isn't only about catching bad actors. It's about proving your firm can identify risk, respond proportionately, and maintain defensible records when examiners ask what happened and why.

Understanding the AML Regulatory Landscape

For advisory professionals, AML rules can feel fragmented because several layers of regulation operate at once. The clean way to think about it is this: the Bank Secrecy Act sets the statutory foundation, FinCEN issues and administers core AML requirements, and FINRA applies specific program expectations to broker-dealers through its own rulebook and examination process.

Start with the BSA and FinCEN

The BSA is the basic federal framework for anti-money laundering obligations. It authorizes a system of recordkeeping, reporting, and compliance controls intended to detect and deter illicit finance. FinCEN sits at the center of that framework and expects firms covered by the regime to maintain AML programs that are reasonably designed for their risks.

That legal backdrop matters because many newer firms approach AML as a policy drafting exercise. It isn't. The core issue is whether your controls, reporting lines, and review process function in a way that meets the standard regulators expect from your business model.

Where FINRA enters the picture

If you operate as a broker-dealer, FINRA Rule 3310 is the rule you need to understand operationally. It requires a written AML program approved in writing by a member of senior management and implemented in a way that fits the firm's business. Advisors working through broker-dealer structures often underestimate how quickly a mismatch between written procedures and real workflows can become an exam issue. That's especially true when onboarding, supervision, and product activity are spread across small teams.

A useful parallel appears in discussions about navigating insurance compliance requirements. Different sectors have different rule sets, but the recurring lesson is the same: generic compliance language is rarely enough when regulators examine what employees do.

A practical hierarchy for smaller firms

Use this hierarchy when building your program:

| Layer | What it does | Why it matters |

|---|---|---|

| Bank Secrecy Act | Creates the federal AML framework | Sets the legal baseline |

| FinCEN requirements | Defines core AML expectations | Drives reporting and program design |

| FINRA Rule 3310 | Applies AML program obligations to broker-dealers | Shapes exams and supervisory expectations |

| Firm procedures | Translate rules into daily tasks | Determines whether compliance actually works |

For registered investment adviser affiliates and hybrid businesses, coordination is often the hidden issue. One side of the business may have stronger onboarding discipline than the other. That inconsistency can create risk at the enterprise level, especially if clients move between channels or personnel. Firms dealing with RIA compliance obligations should pay close attention to those handoff points.

Regulators rarely care that a firm is small. They care whether the firm understood its risks and built controls that fit them.

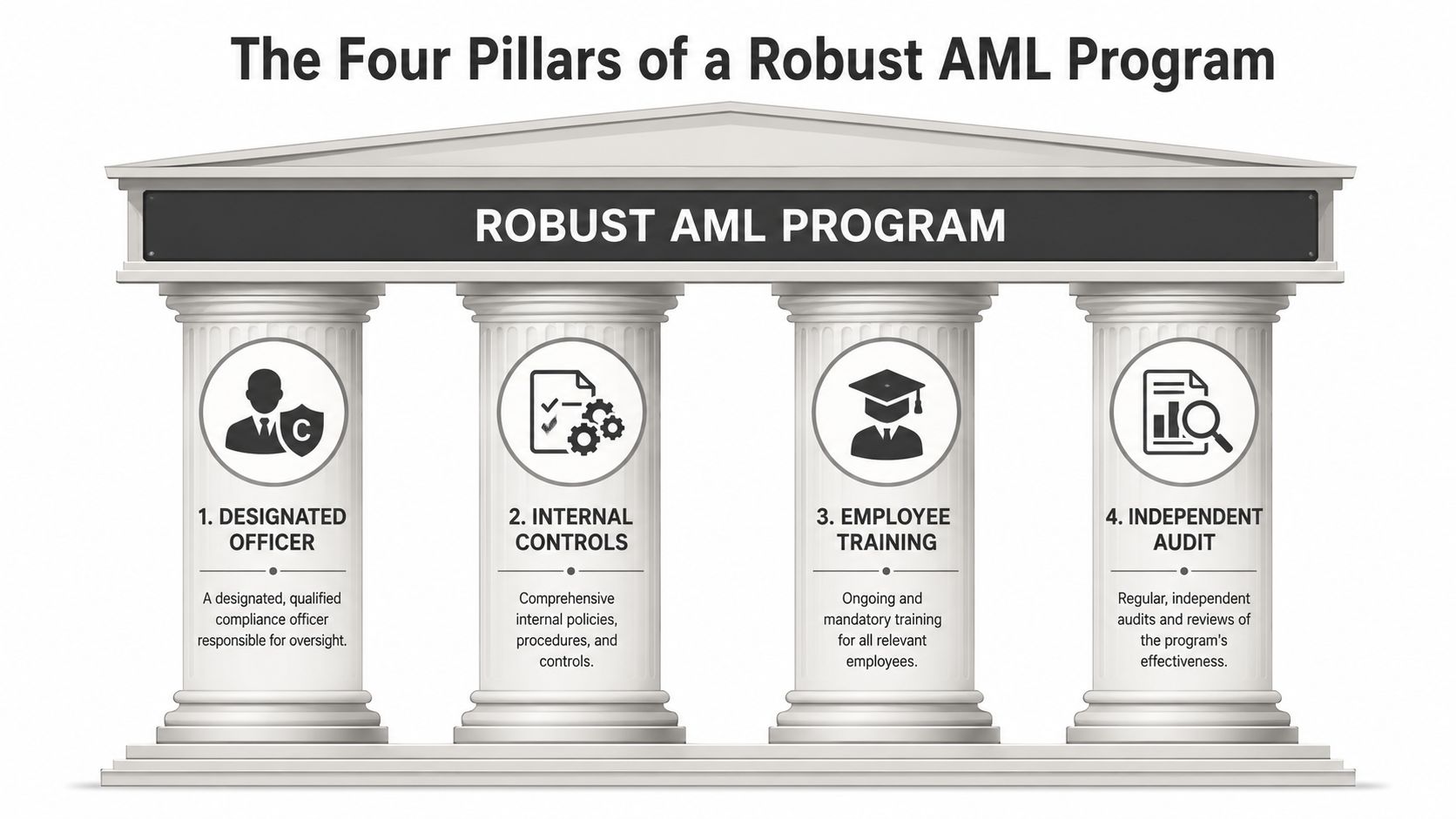

The Four Pillars of a Robust AML Program

A workable AML structure looks less like a binder on a shelf and more like a fortified system. Remove one support and the rest starts to sag. For smaller firms, that usually happens when responsibility is unclear, procedures are copied from a template, training is superficial, or testing is treated as an afterthought.

Designated officer

Someone has to own the program. Not ceremonially. In practice.

Your AML officer should understand your account-opening flow, your products, the kinds of clients you serve, and the points where suspicious activity could surface. In a smaller firm, this person often wears multiple hats. That isn't automatically a problem. The problem starts when the title exists but the authority, time, and access to information do not.

An effective officer usually has three things: authority to halt questionable onboarding, direct access to senior leadership, and enough familiarity with the business to know when a transaction pattern doesn't fit.

Internal controls

Many firms lose credibility here. They adopt polished written procedures that describe an idealized process instead of the actual one. Examiners notice that quickly.

Your internal controls should address:

- Client intake: What documents are required before an account can be approved.

- Risk classification: Which client traits trigger enhanced review.

- Escalation paths: Who decides whether an issue is cleared, monitored, or reported.

- Documentation standards: What the file must show if a decision is later questioned.

For legal entity ownership issues, beneficial ownership diligence is often the part firms handle too casually. A helpful outside reference on transparency trends is the RegisterCompany.ie beneficial ownership brief, which underscores why ownership information deserves close attention even when a structure initially appears routine.

Employee training

Training has to be relevant to the job. Front-office staff should know what facts require escalation during onboarding and relationship management. Operations personnel should know what activity patterns deserve a second look. Supervisors should know when an explanation is incomplete even if it sounds elaborate.

Practical rule: If training only tells employees what the law says, but not what they should do with a problematic account file on a busy Tuesday afternoon, it isn't enough.

Independent audit

Independent testing is the pillar smaller firms neglect most often because it doesn't produce revenue and can feel duplicative. That's a mistake. It's the mechanism that tells you whether the rest of the program works as intended.

Think of the four pillars this way:

- The officer gives the program accountability.

- The controls give it structure.

- The training gives it reach.

- The testing gives it credibility.

If your firm is strong in only two of those areas, you don't have a robust anti-money laundering compliance program. You have partial coverage and a false sense of security.

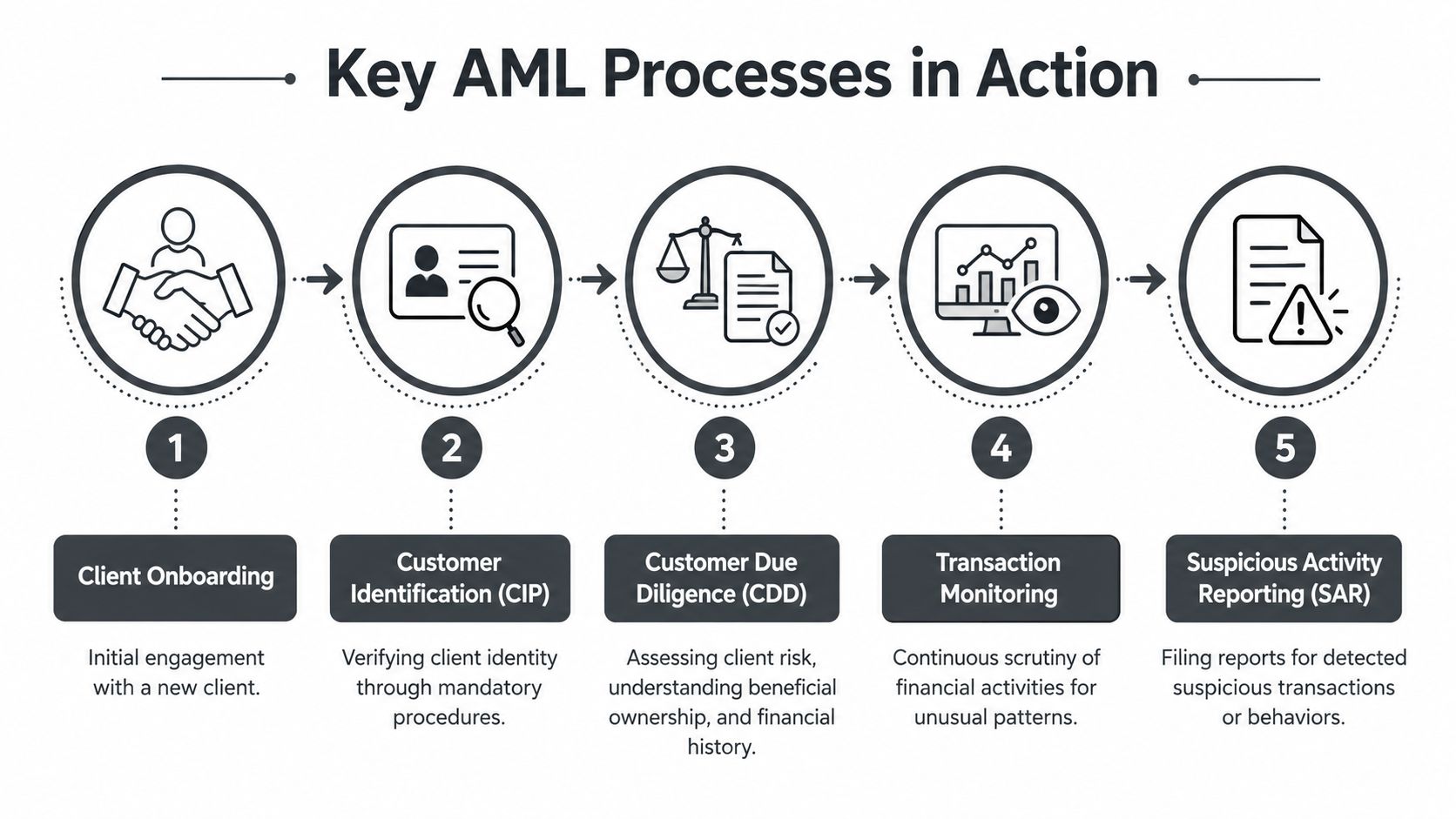

Key AML Processes in Action

A new advisory client wants the account opened before the market closes. The paperwork looks clean, the referral source is known, and the revenue is attractive. Then operations notices that the funding account sits in a different entity's name and the ownership chart in the file does not match the client's explanation. That is how AML issues usually arrive at smaller firms. Not as obvious fraud, but as pressure to explain away details that do not fit.

Onboarding and identification

Customer Identification Program procedures belong inside the account-opening workflow. At an independent firm, that usually means the same few people are collecting documents, speaking with the client, and clearing exceptions. The advantage is speed. The risk is that staff start treating identification as an administrative task instead of a judgment call about whether the relationship makes sense.

For legal entity customers, the file should support a coherent picture of who owns the business, who controls it, and why the account is being opened at your firm. Formation documents, governing agreements, tax identification information, and address records should line up with the client's explanation. If they do not, the issue is not minor because the documents are technically complete. It is an unresolved onboarding problem.

Smaller broker-dealers also miss a basic point here. If one person reviews CIP and another handles account approval, someone has to reconcile inconsistencies before the account goes live.

Due diligence and risk classification

Customer due diligence should produce an answer to a practical question. What activity would make sense for this client in this account?

That matters more at smaller firms than many principals realize. A thin risk-rating method creates trouble later because monitoring staff cannot tell the difference between expected activity and activity that deserves escalation. I often see files with good documents and weak judgment. The account is labeled low or medium risk, but no one documented why, what products the client will use, whether third-party transfers are expected, or whether entity complexity creates a higher risk of concealed control.

That analysis often overlaps with customer-profile obligations. Firms should make sure the AML file and the customer file are not telling two different stories about the same relationship. The expectations behind risk classification often depend on the same facts required under FINRA Rule 2090 and the know-your-customer framework.

Monitoring and escalation

Monitoring at a small firm does not need bank-level software to satisfy regulators. It does need a defined process that matches the firm's business. If your practice handles retail advisory accounts with limited cash movement, your review should focus on the patterns that create risk in that setting, such as third-party wires, unexplained journal activity, sudden liquidations followed by outgoing transfers, or account activity that does not fit the client profile established at onboarding.

A process that usually holds up in examination has four parts:

- Set an activity baseline: Record expected funding sources, transaction types, and account purpose at opening.

- Review exceptions against that baseline: Flag activity that is inconsistent with the customer profile, not just activity above a dollar threshold.

- Escalate to someone with authority: The reviewer needs access to a supervisor or AML officer who can ask hard questions and delay action if needed.

- Document the decision: State what was reviewed, what explanation was received, and why the activity was cleared or escalated further.

Documentation is where many smaller firms lose credibility. A note that says “reviewed, no issue” does not help if FINRA later asks why an unusual transfer pattern was accepted.

Reporting obligations

Once suspicious activity cannot be reasonably explained, the firm needs a prompt internal path to a reporting decision. Delay is a common small-firm failure point. The branch assumes home office is reviewing it. Home office assumes the producing representative has more context. Meanwhile, the clock keeps running.

Some reporting decisions require judgment, especially where the facts develop over several interactions. Others are rule-based and should be handled mechanically once the trigger is met. Firms need written procedures that distinguish those two categories and assign responsibility clearly. If that responsibility sits with one AML officer, the backup person should be identified in advance. Vacations and year-end workloads are not good excuses in an exam file.

For independent advisors and smaller broker-dealers, the practical test is simple. Can the firm show who saw the issue, when it was escalated, what facts were gathered, who made the reporting decision, and where that record is kept. If the answer is unclear, the process is too loose.

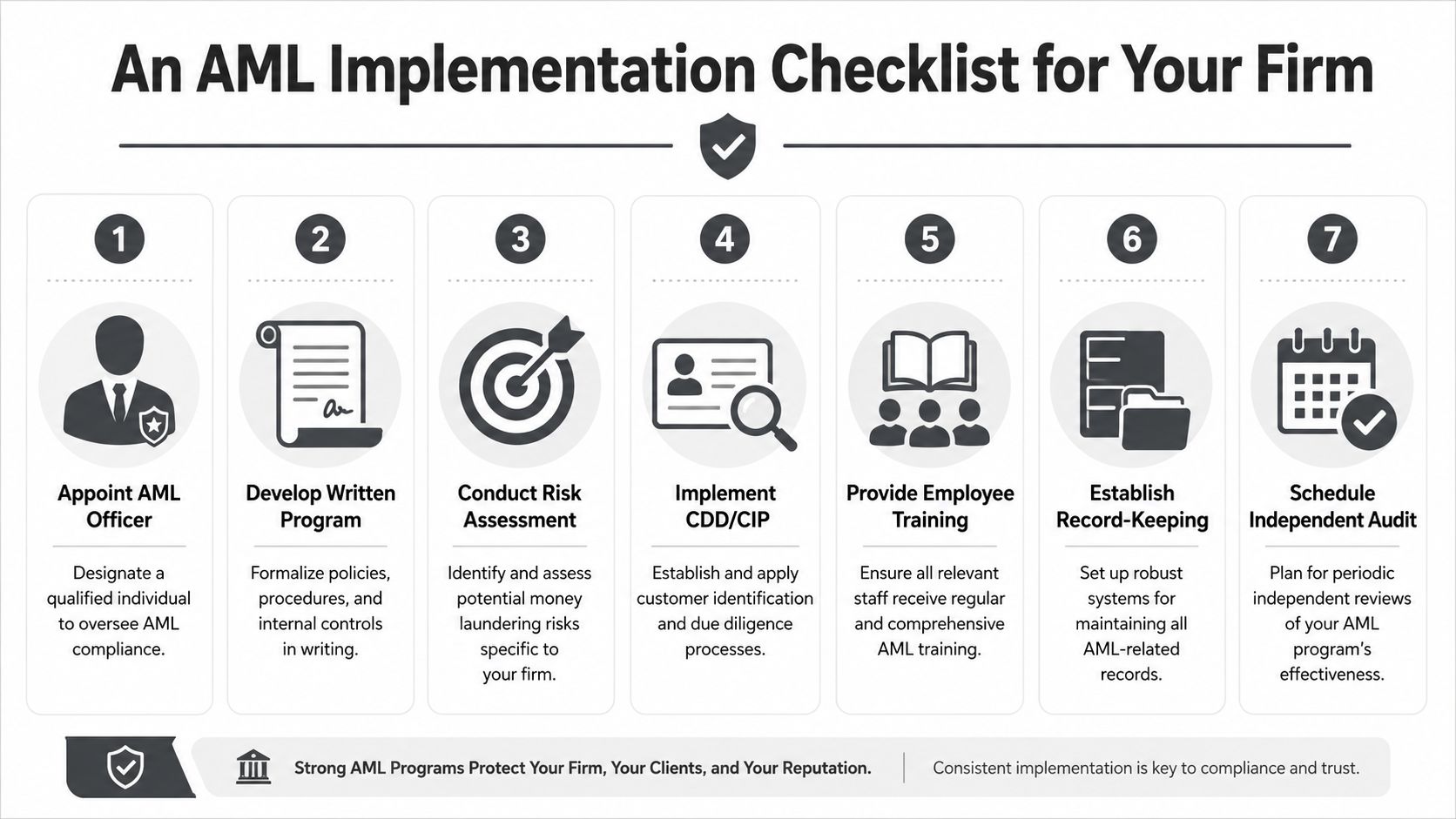

An AML Implementation Checklist for Your Firm

Building an AML program at a small firm doesn't require the infrastructure of a national institution. It does require discipline. The right approach is to build a system proportionate to your business, then document why it fits. That's more defensible than adopting enterprise-grade language your staff can't execute.

A practical checklist

Map your business model

List your account types, client categories, funding methods, affiliated entities, and product lines. A small introducing broker has different risks than a firm with complex entity clients or frequent third-party money movement.Appoint the right AML owner

Pick someone who can make uncomfortable decisions and isn't afraid to slow down a lucrative account opening. If that person lacks operational visibility, the designation won't help.Draft procedures from the ground up

Start with your actual workflow. Who receives documents, who reviews them, who clears exceptions, and where those decisions are recorded. A generic manual often fails because it assumes departments and approval layers your firm doesn't have.Create a client-risk method your staff can use

Risk-rating systems fail when they are too abstract. Keep the categories understandable. Staff should know why a legal entity with layered ownership is different from a straightforward retail account, and what that difference requires.

Where smaller firms can save money without cutting corners

Independent testing is one area where nuance matters. While FINRA Rule 3310 mandates annual independent testing, it explicitly exempts members that engage solely in proprietary trading or conduct business only with other broker-dealers, allowing testing every two years instead under FINRA Rule 3310. Smaller firms often overpay because they assume annual outside testing is always required.

That doesn't mean firms should automatically minimize review frequency. It means they should understand whether the exception applies and whether qualified internal personnel can perform the work without compromising independence. Cost control is legitimate. Guessing is not.

Implementation choices that usually work

A lean but credible implementation plan often includes:

- Written exception logs: Record onboarding issues, follow-up requests, and clearance decisions.

- Role-based training: Give advisors, operations staff, and supervisors different examples and escalation instructions.

- Periodic file reviews: Sample completed account files to see whether staff followed procedure.

- Simple monitoring criteria: Focus on patterns your firm can realistically review and explain.

For firms that want a structured planning aid, Visbanking's data-driven framework offers a useful way to think about implementation categories, even though each firm still needs to tailor the details to its own risk profile.

A decision table for common small-firm questions

| Question | Weak answer | Better answer |

|---|---|---|

| Who can serve as AML officer? | Whoever has room in the org chart | Someone with authority, access, and enough time |

| Can we use templates? | Yes, with minor edits | Only as a starting point, then rewritten to fit workflow |

| Do we need expensive technology? | Always | Only if your activity and scale justify it |

| Should testing be outsourced? | Always | Sometimes, but first assess independence and firm structure |

The most effective small-firm AML programs are not the most elaborate. They are the ones employees can follow under pressure, supervisors can defend, and examiners can trace from policy to file to decision.

Common Enforcement Pitfalls and Best Practices

A small broker-dealer passes its exam on paper, then gets pulled into a tougher review because the files tell a different story. The AML manual assigns steps no one performs. The designated AML officer has two other jobs and little time to review exceptions. A representative noticed unusual funding activity, but no one documented the escalation. That is how many enforcement problems start in smaller firms. Not with an exotic scheme, but with ordinary gaps that regulators can trace from policy to practice.

Pitfall one is a generic program

Independent advisors and smaller broker-dealers are especially exposed here because many start with a vendor template and never fully rewrite it. The problem is not using a template. The problem is leaving in procedures that do not match your account opening process, product mix, staffing, or actual supervisory chain. FINRA examiners regularly compare the written program to what employees do in live files. If your manual says one person reviews alerts, another approves escalations, and no one in the firm performs those roles, the AML issue quickly becomes a books, records, and supervision issue too.

The better approach is narrower and more disciplined. Draft procedures around the business you operate. Name the key decision-makers. State how exceptions are logged, who can clear them, and what happens when the assigned reviewer is unavailable. For small firms, specificity beats breadth.

Pitfall two is weak or delayed independent testing

Smaller firms often postpone testing because nothing appears wrong. That is usually a mistake.

Independent testing is required, and it needs to happen on a regular schedule that fits the firm's risk and activity. A review that occurs only after an exam notice, an internal problem, or a suspicious account is already too late. The practical question is not whether the firm can afford testing. It is whether the firm can afford to defend an outdated program without it.

There is also a real trade-off here. Outsourcing testing can improve independence, but outside reviewers often miss workflow workarounds that employees use every day unless the scope is well defined. Internal testing may be cheaper, but it can fail the independence test if the reviewer helped build or operate the controls being tested. As noted in the CFTC's discussion of AML program expectations under the BSA framework, firms need testing that evaluates whether the program is operating as intended, not just whether a policy exists.

A useful test report does more than list deficiencies. It ties findings to specific accounts, approvals, and exception handling so the firm can fix the process, assign responsibility, and show follow-through at the next exam.

Pitfall three is poor escalation culture

In many small firms, the biggest AML weakness is not software or staffing. It is hesitation.

Registered representatives, operations staff, and branch supervisors often see facts that do not fit before anyone labels them a red flag. The failure happens when employees assume they need certainty before escalating, or when production pressure makes them treat delay as a business problem instead of a control step. Regulators look closely at those judgment calls, especially where AML concerns overlap with suitability, supervision, or a broader SEC investigation into securities-related misconduct.

Best practice is practical. Give staff a clear escalation standard. Document the question, the handoff, the reviewer, and the outcome. Make it clear that pausing a transaction or account for legitimate review is part of the job. In small firms, that culture matters because one missed escalation can sit unnoticed across multiple functions before anyone revisits the file.

Strengthen Your AML Program with Expert Counsel

A strong anti-money laundering compliance program is not a one-time drafting project. It's an operating system for how your firm accepts clients, evaluates risk, documents decisions, and responds when facts don't fit. Smaller advisory firms and broker-dealers can absolutely build effective programs, but they need to be realistic about staffing, workflow, and the specific regulatory expectations that apply to their business model.

Good AML practice is usually not flashy. It's consistent. The right documents are collected. The right questions are asked. The right people make the hard calls. And the file shows what happened.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you need guidance on building, reviewing, or defending an AML framework that fits your advisory or brokerage business, contact Kons Law.