A client calls after the market opens. The coupon didn't arrive. A notice from the trustee mentions an event of default. The client wants a quick answer to a hard question: is this a temporary disruption, a covenant problem, or the start of a real recovery fight?

That's where many advisors get pulled into unfamiliar terrain. A bond default looks like a portfolio issue at first, but it quickly becomes a legal process governed by the indenture, trustee action, creditor priorities, and, in some cases, bankruptcy procedure. Good advice starts with recognizing that bonds in default are no longer just pricing problems. They are enforcement and recovery problems.

The urgency is real. Over the past decade, global corporate bond default risk has surged by 40%, reflecting a broad deterioration in credit stability and a meaningful migration toward high-yield issuance, according to Credit Benchmark's 10-year default risk analysis. For advisors, that means more clients will face defaults, distressed exchanges, restructurings, and downgrade-driven selling pressure. The old habit of treating a default notice as a back-office event isn't good enough anymore.

When a Client's Bond Enters Default

The first practical problem is that clients usually call after the damage is visible, not when the legal risk begins. They've seen a missed payment, a shocking price move, or a terse brokerage alert. By then, the advisor has to calm the client, preserve optionality, and avoid casual statements that overpromise recovery.

What the client usually hears

Most clients reduce the event to one sentence: “My bond defaulted.” That phrase hides several separate issues:

- Income interruption: The expected stream of interest may stop.

- Valuation shock: The market price may trade at distress levels long before a final outcome is clear.

- Process confusion: Clients often don't know who speaks for bondholders, what rights they have, or whether they need to act.

- Tax and suitability questions: Advisors may have to assess how the position was held, why it was purchased, and what disclosures were made.

In practice, the first call is rarely about legal doctrine. It's about control. The client wants to know whether anyone is protecting bondholders, whether the issuer can fix the problem, and whether selling now locks in the worst result.

Practical rule: The first bad answer in a default situation is usually “let's wait and see” without first reading the indenture and trustee notices.

Why this matters more now

A decade ago, many advisors could treat isolated defaults as niche events affecting small slices of speculative portfolios. That's less workable in a market where credit quality has been under pressure across sectors. The increase in global default risk noted above matters because more clients now hold credits that can deteriorate quickly from “income-producing” to “workout-driven.”

That shift changes the advisor's job. You're not just interpreting bond math. You're identifying what happened, what rights attach to the default, and which path is likely to preserve value. Some defaults resolve through negotiation. Others harden into litigation, acceleration, bankruptcy, or trustee enforcement. The better the early triage, the better the client's position later.

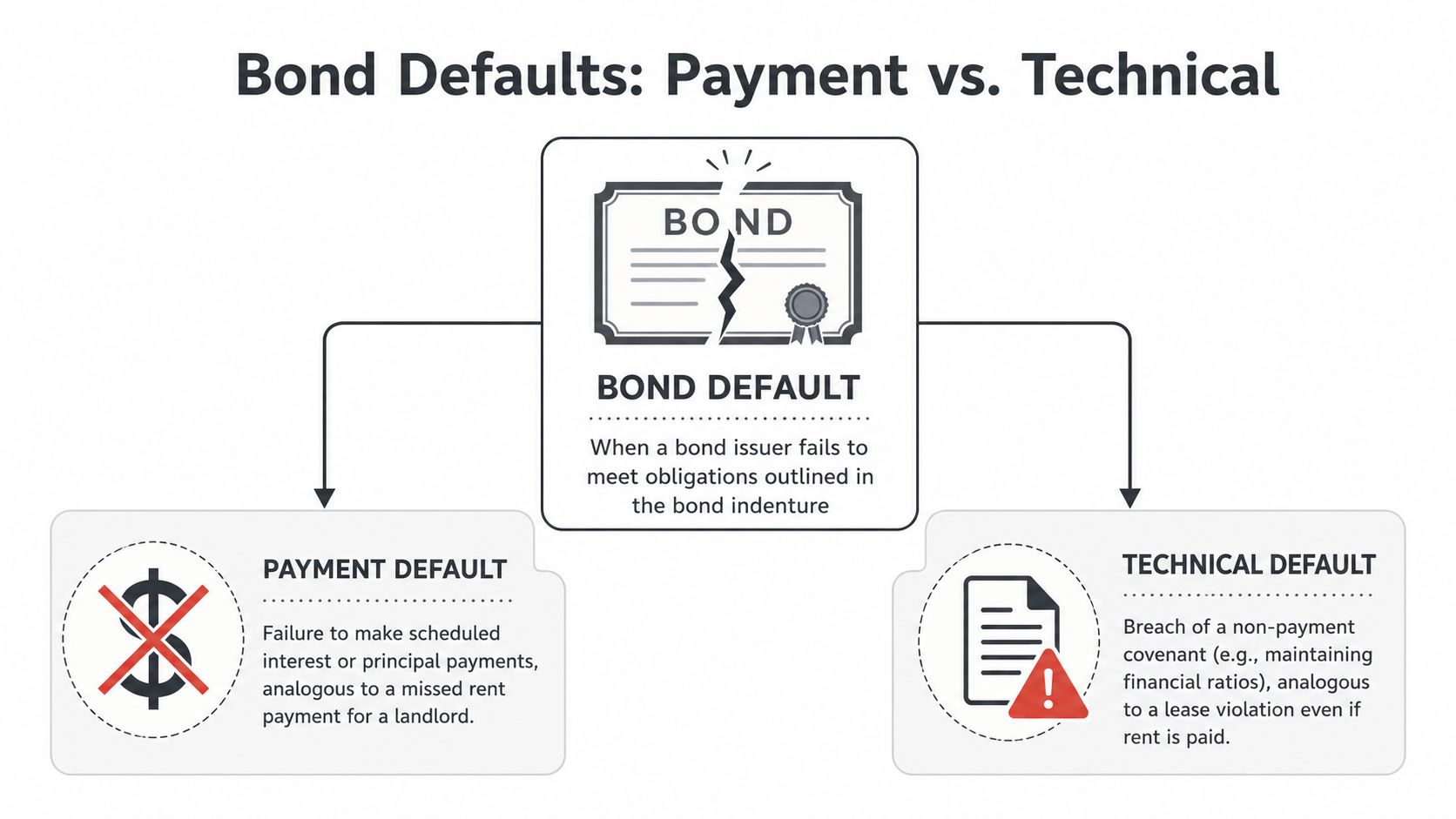

Understanding the Types of Bond Default

Not every default starts with a missed payment. That distinction matters because advisors often focus on cash flow failure and miss the earlier legal trigger.

A payment default is the straightforward case. The issuer fails to pay principal, interest, or a redemption price when due. A technical default happens when the issuer breaches a non-payment covenant in the bond documents. The National Association of Bond Lawyers explains that distinction, and it also notes that high-yield bonds showed a default rate of 4.4% in May 2025, up from 3.7% in April, while high-debt loan default rates increased to 1.7% from 1.5%.

Payment default

Think of this as the missed mortgage payment version of default. Money was due. Money wasn't paid. That usually gets immediate attention because it is easy to spot and easy to explain to clients.

Common consequences include:

- Stopped income: The bond no longer performs its basic investment function.

- Faster price deterioration: Buyers price in uncertainty about recovery and timing.

- Escalating remedies: The trustee may gain grounds to declare an event of default and pursue indenture remedies.

Technical default

Technical default is more subtle and often more important than advisors expect. The issuer may still be making scheduled payments while violating a covenant, such as a requirement to maintain insurance, comply with reporting duties, or preserve agreed financial conditions.

That makes technical default an early legal warning, not a harmless paperwork issue.

A bond can be current on payments and still be in serious trouble under the indenture.

For advisors, document review is crucial. The covenant package determines whether the breach is curable, whether notice is required, and whether the breach matures into a formal event of default after a cure period expires. That's also why it helps to understand the difference between secured and unsecured positions when assessing financial risk and remedies. A basic primer on what makes a creditor secured provides useful context when a distressed bond sits alongside pledged collateral or competing claims.

Why the distinction changes strategy

A payment default often triggers immediate recovery planning. A technical default may create bargaining power before cash stops flowing. If a client waits until the issuer misses interest, the best negotiating window may already have closed.

Advisors who understand this difference can ask better questions early:

| Issue | Payment default | Technical default |

|---|---|---|

| Immediate cash impact | Usually yes | Not always |

| Easier for clients to recognize | Yes | No |

| Can trigger enforcement rights | Yes | Yes |

| Best use | Damage assessment | Early intervention |

Legal and Financial Consequences of a Default

Once default is on the table, two tracks begin at the same time. The issuer deals with market exclusion and negotiating pressure. The bondholder deals with lost income, impaired liquidity, and an uncertain recovery path.

That pressure is not confined to isolated names. In the U.S., the trailing 12-month speculative-grade bond default rate was 4.8% as of August 2025, and it had remained above 4% for two consecutive years, according to Charles Schwab's discussion of Standard & Poor's data. For advisors, sustained distress in the high-yield market means defaults can't be treated as rare accidents. They need a repeatable response framework.

What happens to the issuer

An issuer in default doesn't just face a missed obligation. It faces a credibility crisis.

Three effects show up quickly:

- Capital markets access narrows: New borrowing becomes harder, costlier, or unavailable.

- Bargaining power shifts: Creditors, trustees, and restructuring professionals begin dictating terms.

- Reputation suffers: Vendors, counterparties, and existing lenders may tighten their positions.

Even before a formal filing, the issuer may have to choose between concessionary exchanges, covenant resets, asset sales, or a court-supervised reorganization. Advisors should assume management is acting under pressure, not from a position of strategic calm.

What happens to the bondholder

The holder's problem is immediate and practical. Expected income may stop. Mark-to-market value may collapse. Liquidity often becomes thin right when clients most want flexibility.

A default also changes the nature of the investment. The bond is no longer just a fixed-income product. It becomes a claim that must be analyzed like a distressed legal asset. That means the relevant questions are no longer only yield, duration, and rating. They are seniority, collateral, covenant package, trustee posture, and venue.

The fallen angel problem

Advisors also need to separate true default from the fallen angel scenario, where an investment-grade bond is downgraded into junk territory. A fallen angel isn't automatically in default, but the downgrade can trigger forced selling, mandate violations, and severe price pressure.

That distinction matters because clients often react to downgrade-driven price damage as if recovery is already gone. Sometimes that assumption is wrong. A downgraded issuer may still have room to restructure, refinance, or stabilize operations. The legal question is whether the downgrade is a market reclassification or the start of covenant breaches and payment failure.

A downgrade hurts. A default activates rights.

For portfolio management and client communication, those are very different events. Treating them as the same can lead to premature sales or delayed enforcement.

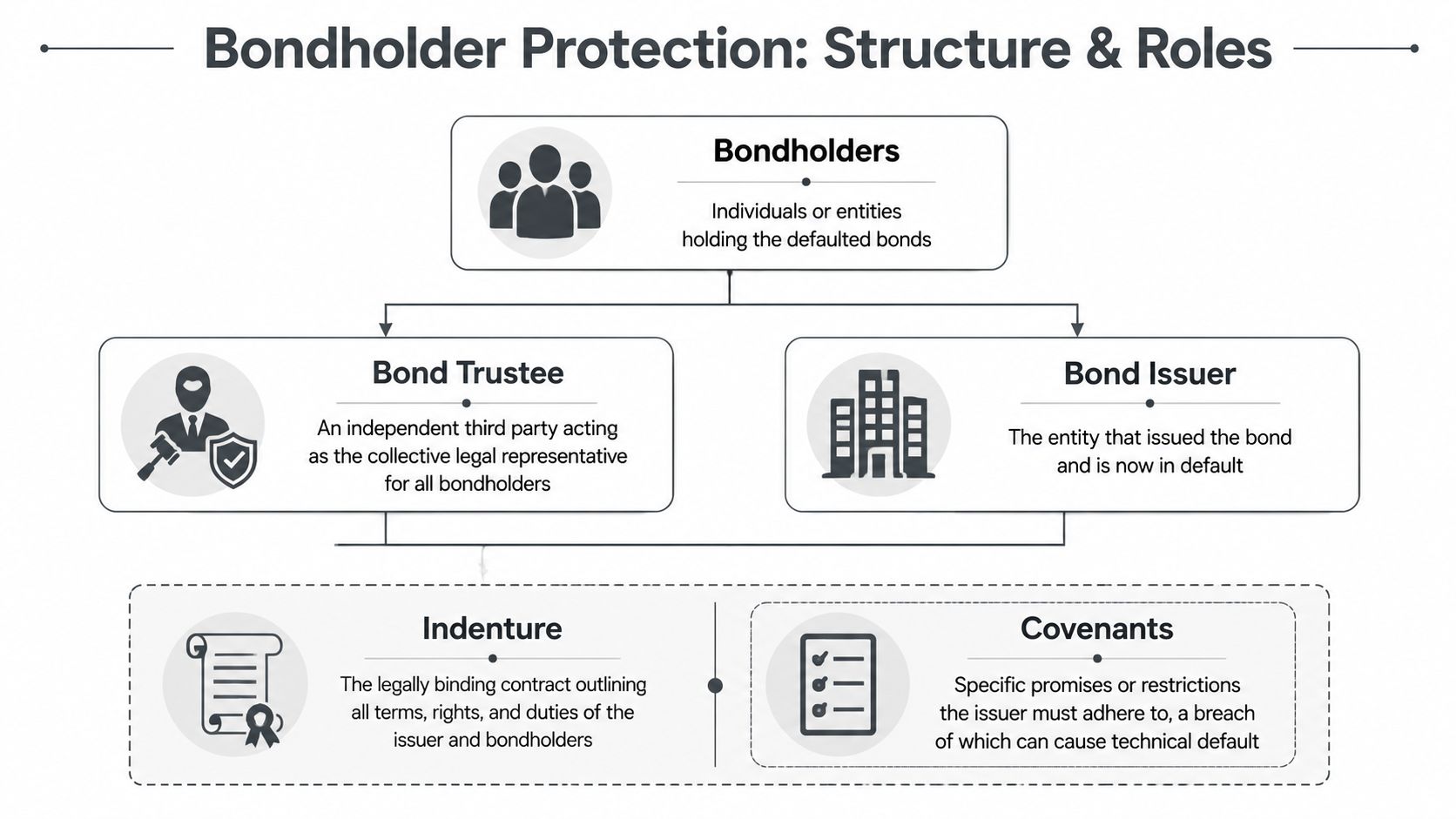

Navigating Bondholder Rights and Trustee Roles

Bondholders are rarely meant to act one by one. In most bond deals, the trustee stands at the center of enforcement. When a default occurs, the trustee becomes the collective representative for bondholders under the indenture.

That role is widely misunderstood. Clients often assume their custodian, brokerage firm, or advisor will drive the process. Usually they won't. The trustee holds the contractual authority to issue notices, evaluate defaults, accelerate debt in the right circumstances, and pursue remedies on behalf of the bondholder group.

What the trustee actually does

The trustee's authority comes from the indenture, not from generalized notions of fairness. That means advisors should expect the trustee to act within the four corners of the contract.

Typical trustee functions include:

- Receiving and circulating notices

- Determining whether an event of default has been triggered under the indenture

- Collecting direction or indemnity from bondholders when required

- Starting enforcement steps, including acceleration or litigation, if authorized

The trustee is not a volunteer rescue service. If the indenture requires thresholds, notices, or bondholder instructions, those conditions matter.

Why acceleration matters

Acceleration is one of the strongest tools in a default scenario. Instead of waiting for each future payment to come due, acceleration makes the full outstanding principal immediately due and payable, subject to the terms of the indenture.

That changes the negotiation dynamic. It tells the issuer that bondholders are no longer discussing a temporary delinquency. They are asserting the entire debt claim now.

In practice, acceleration can:

| Effect | Why it matters |

|---|---|

| Increase pressure on issuer | Management loses time and flexibility |

| Clarify damages | The full debt is put in issue |

| Strengthen settlement talks | Restructuring discussions occur under sharper legal risk |

How advisors should work with the trustee structure

Advisors don't need to litigate the case, but they do need to know where authority sits. That means identifying the trustee, obtaining current notices, and checking whether bondholders must act collectively to direct next steps.

Some clients also hold interests through entities, family offices, or layered structures. In those cases, related collection remedies can matter if disputes spill beyond the bond itself. For example, charging orders in business ownership disputes are a separate remedy, but understanding them helps advisors spot where creditor rights intersect with entity interests and judgment enforcement.

The practical mistake is passivity. If a trustee is moving, monitor it. If a trustee is waiting for direction, know that waiting has a cost.

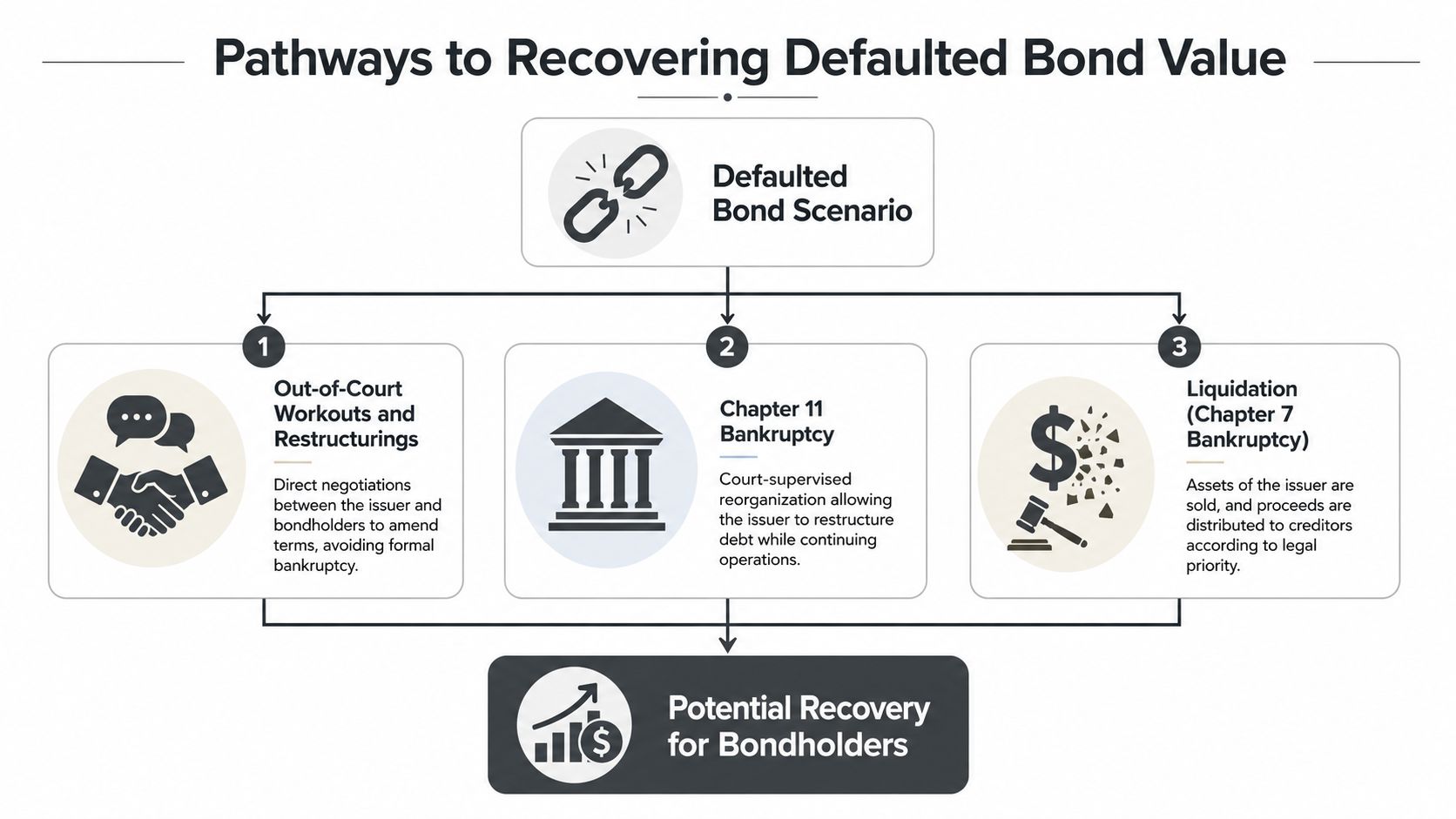

Key Recovery Pathways for Defaulted Bonds

Default doesn't always end in a wipeout. Recovery depends on structure, debt burden, collateral, sector, timing, and the quality of the creditor response. Historical outcomes support that more measured view. The weighted average recovery rate on defaulted high-yield bonds in 2010 was 56.7% of par, according to the NAIC corporate bond default study. That same study noted that broadcasting and media led defaults at 5.5% during 2010, while the auto industry led defaults through April 2011.

Those figures don't promise any future result. They do support one important point for advisors: a default is a recovery analysis, not an automatic total loss.

Out-of-court workouts

This is usually the fastest path when the issuer still has a viable business and creditors believe a consensual fix preserves more value than immediate litigation. Terms may be amended, maturities extended, covenants reset, or debt exchanged for new securities.

What works:

- Early organization among holders

- Clear financial disclosure from the issuer

- Credible deadlines and negotiation advantage

What usually doesn't work:

- Open-ended forbearance with no milestones

- Informal promises outside written amendments

- Assuming management's optimism substitutes for legal protections

Bankruptcy proceedings

When a consensual fix fails, a court-supervised case may become unavoidable. In a reorganization, bondholders typically need to file claims, monitor debtor filings, evaluate proposed treatment, and track plan terms carefully.

Here the legal priorities matter more than the headline narrative. Senior secured debt, unsecured notes, subordinated claims, and equity don't stand on equal footing. Advisors should be careful not to tell clients that “everyone will get something.” Sometimes value exists. Sometimes the fulcrum security is above or below the client's position.

The client's recovery doesn't depend on how angry the default feels. It depends on where the claim sits and how the case is structured.

Liquidation presents a different reality. If operations can't be preserved, assets may be sold and proceeds distributed by priority. That can be clean in theory and disappointing in practice.

Litigation and arbitration

Litigation is appropriate when the issuer, guarantor, or another obligated party can be sued to enforce payment or related contractual rights. Arbitration may matter if a separate dispute exists with an intermediary, advisor, or brokerage firm concerning how the bond was sold, supervised, or handled after distress emerged.

This path can be effective when there is a solvent target, a guaranty worth enforcing, or a clear covenant breach that confers an advantage. It is less effective when the defendant has no collectible assets or when a bankruptcy filing is imminent and will stay the case.

For advisors assessing post-judgment realities, it helps to understand the mechanics of enforcing a civil judgment. A paper victory without a realistic collection path is not a strategy.

Side-by-side recovery view

| Path | Main advantage | Main risk | Best fit |

|---|---|---|---|

| Out-of-court workout | Speed and flexibility | Delay without accountability | Viable issuer, cooperative creditors |

| Bankruptcy | Structured process and court oversight | Cost and time | Complex capital stack, broad creditor conflict |

| Litigation or arbitration | Direct enforcement pressure | Collection risk or stay risk | Solvent obligor, strong contract claim |

Special Focus The Nuances of Municipal Bonds

Many advisors still speak about municipal bonds as if they share one risk profile. They don't. That assumption creates trouble when clients own project-backed debt issued through municipal structures that look safer than they are.

A critical distinction is between general obligation bonds and conduit bonds. According to VanEck's discussion of municipal bond stress, 90% of municipal defaults occur in conduit issues, such as senior living and charter school financings. That is materially different from general obligation bonds, which have near-zero default rates.

Why conduit bonds behave differently

Conduit bonds are often tied to a specific project, borrower, revenue stream, or operating enterprise. If the project underperforms, bondholders are not relying on the full taxing power of the municipality in the way they would with a true GO bond.

That changes the recovery analysis:

- Trustee enforcement may be central

- Special backstops may matter

- Project documents can be as important as the bond form itself

In some cases, recovery can compare favorably with corporate bonds because of those trustee-driven mechanisms and structural supports. But that doesn't make them simple. It makes them document-intensive.

Why advisors should treat sovereign and municipal stress separately

Municipal distress also gets confused with broader public debt crises. Those are not the same legal animals. If you want a useful contrast in how public-sector debt problems can unfold at the national level, Exploring the Greek economic crisis offers helpful background on sovereign debt dynamics that are very different from a conduit bond default tied to a single operating project.

The practical takeaway is straightforward. Don't let the word “municipal” substitute for due diligence. In bonds in default, structure controls outcome.

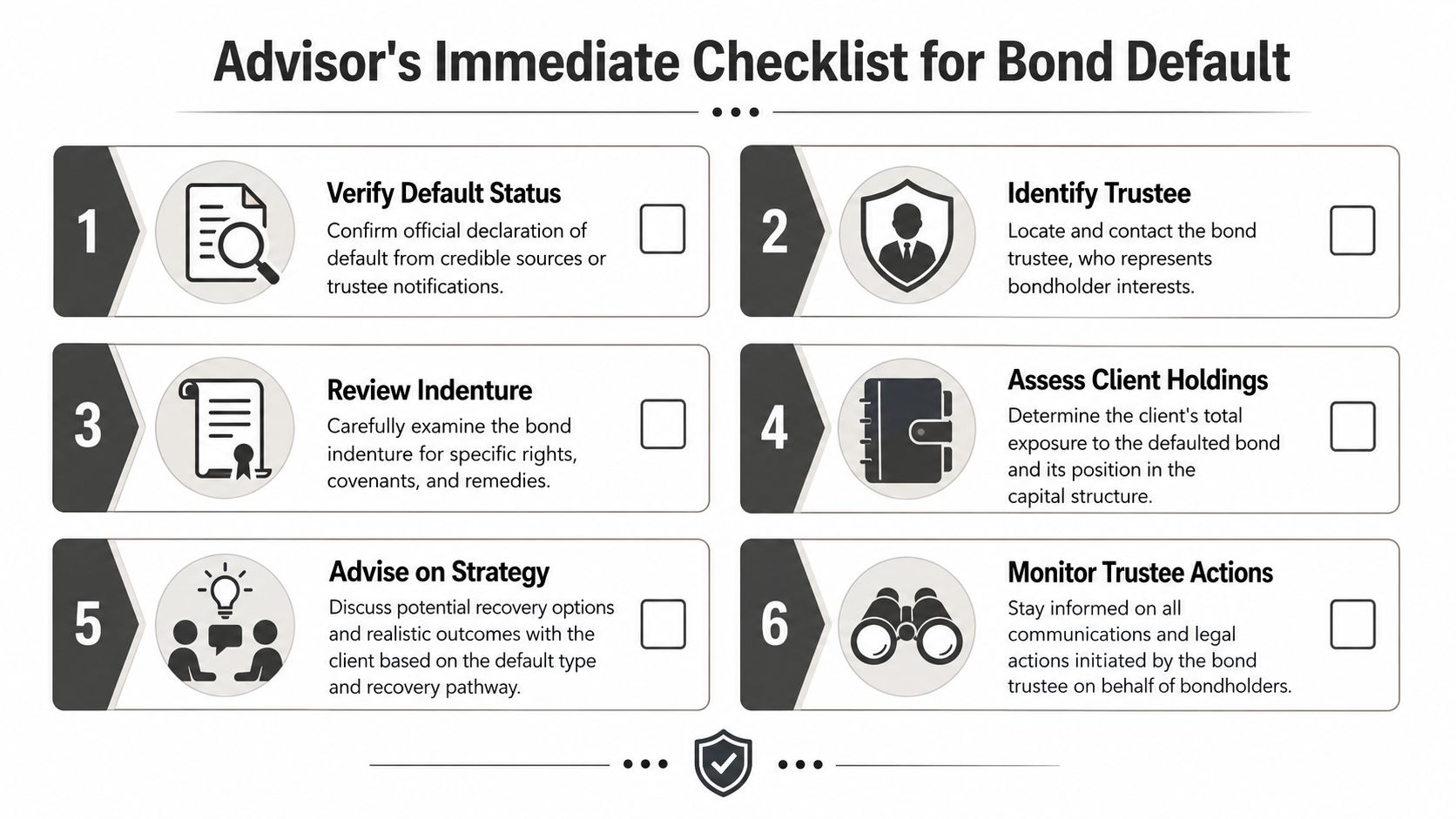

Advisor Checklist and Navigating Next Steps

When a client's bond goes into distress, the advisor's value is in disciplined sequencing. Fast reactions help only if they are the right reactions.

Start with the documents and the parties. Then identify the remedy path. Don't jump from a brokerage alert to a recommendation without confirming what default occurred and who controls enforcement.

Immediate action list

- Verify the default status. Confirm whether the issue is a missed payment, a covenant breach, a grace-period notice, or only a downgrade.

- Locate the trustee. Get the current contact information and every notice already issued to holders.

- Read the indenture. Focus on events of default, cure periods, acceleration rights, collateral, and bondholder voting thresholds.

- Map the client's position. Determine size, account type, purchase history, and where the bond sits in the capital structure.

- Evaluate the likely path. Decide whether the facts point toward workout, bankruptcy, sale, or active enforcement.

- Track all follow-up communications. Trustee letters, exchange offers, and court notices often contain deadlines that matter.

Questions worth asking before giving advice

- Was this position sold as income, principal preservation, or opportunistic yield?

- Did the client understand downgrade and default risk at purchase?

- Is the bond secured, guaranteed, subordinated, or project-backed?

- Would selling now preserve value, or only crystallize panic?

For advisors facing a complicated creditor issue, regulatory concern, or client dispute arising from a defaulted position, it also helps to understand when outside counsel should step in. A practical overview of a creditors' rights lawyer's role is a good starting point.

The best next step is rarely the loudest one. It's the one grounded in the indenture, the trustee's posture, and the client's actual recovery options.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.