In the world of business and finance, not all creditors are created equal. A secured creditor is a lender who isn't just relying on a borrower's promise to pay—they have a direct legal claim, called a lien, on a specific asset owned by the borrower. This asset is known as collateral.

What is a Secured Creditor?

Think of it this way: when a bank gives you a loan to buy a company vehicle, they almost always take a security interest in that truck. The truck itself is the collateral. While you get to use it for your business, the bank holds a legal claim to it until every last dollar of the loan is paid off.

This simple arrangement transforms the bank into a secured creditor, giving it a powerful advantage. If the borrower stops making payments, the secured creditor has the legal right to take possession of that specific asset and sell it to get their money back.

The Foundation of Financial Security

This special status is the bedrock of commercial lending. By having collateral to back up the loan, the lender's risk drops significantly. Their investment is tied to a tangible piece of property, making them far more willing to extend credit, often with better interest rates and terms. This is what makes it possible for businesses to get the capital they need for equipment, inventory, or real estate.

At its core, being a secured creditor means you have a legally enforceable path to repayment that goes beyond a simple IOU. It puts you in a much stronger position than an unsecured creditor or even a judgment creditor who has obtained a court order.

The real power of this position shines through when a borrower hits tough financial times. In those moments, the secured creditor's right to their collateral almost always jumps to the front of the line, taking priority over most other claims. This hierarchy is well-established in the law, primarily governed by the Uniform Commercial Code (UCC).

A secured creditor's claim is tied directly to an asset, not just a promise. This connection to collateral provides a powerful advantage, ensuring they are first in line for repayment from that asset if the borrower defaults.

Secured vs Unsecured Creditor At a Glance

For business owners, understanding the fundamental differences between secured and unsecured creditors is critical. This table breaks down the key distinctions.

| Attribute | Secured Creditor | Unsecured Creditor |

|---|---|---|

| Basis of Claim | A specific asset (collateral) | The borrower's general promise to pay |

| Risk Level | Lower risk for the lender | Higher risk for the lender |

| Default Remedy | Right to repossess and sell collateral | Must sue, get a judgment, then find assets |

| Bankruptcy Priority | Paid first from collateral proceeds | Paid after secured creditors, often gets less |

| Examples | Mortgages, car loans, equipment financing | Credit card debt, medical bills, trade suppliers |

As you can see, the presence of collateral fundamentally changes the creditor's position, especially when things go wrong.

Why Secured Lending Matters

The economic impact of a strong secured lending system is massive and recognized globally. Legal frameworks that protect secured creditors lead directly to more available credit and healthier economic activity. In fact, research shows that countries with robust secured-transactions laws have much higher levels of private-sector credit compared to those with weak protections.

For businesses and lenders, this translates into much higher recovery rates when a borrower becomes insolvent. Secured claims often recover the full value of the collateral, while others are left with pennies on the dollar, if anything at all. This principle is why structuring loans with clear, perfected security interests is a vital practice for Connecticut businesses looking to lend money or secure financing.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Creating and Perfecting a Security Interest

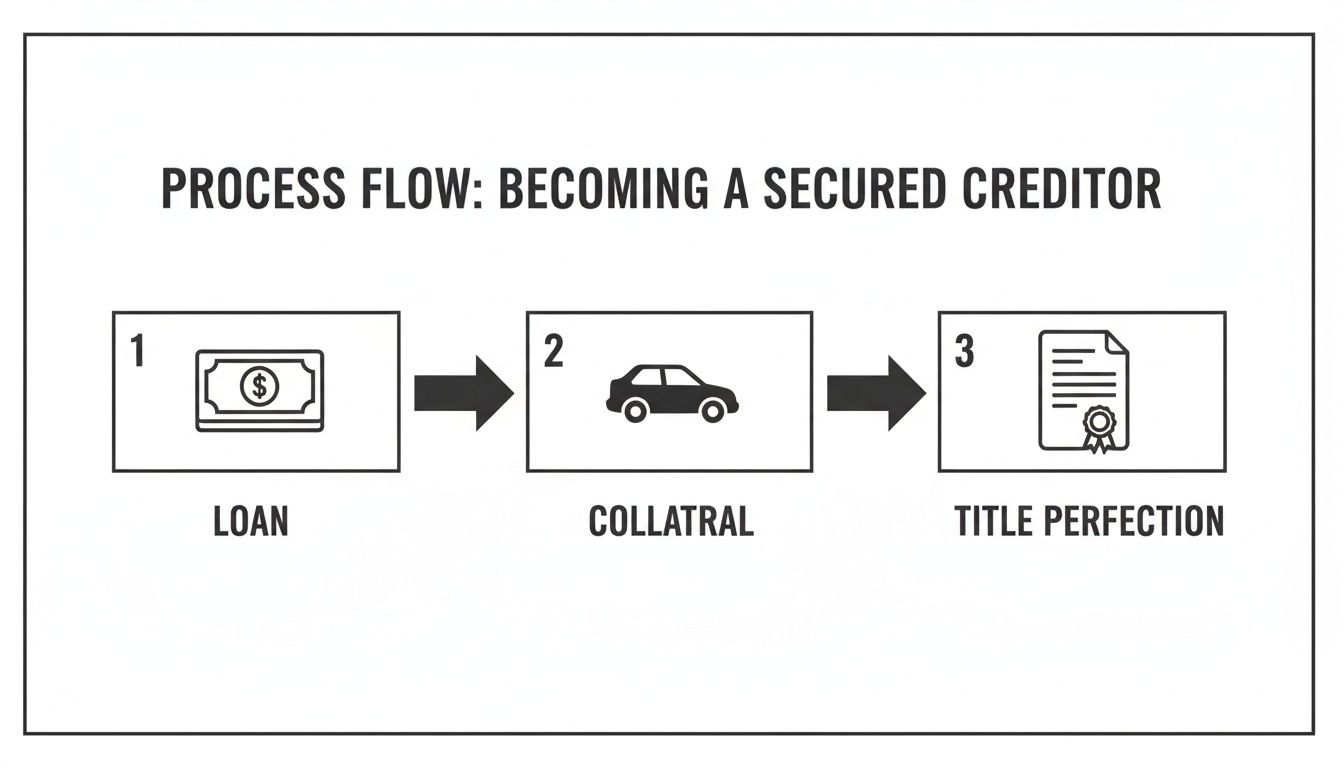

Becoming a secured creditor isn't something that happens by accident. It’s a deliberate, two-step legal process designed to protect your financial interests. The steps are attachment and perfection.

Think of it like building a fortress around your loan. Attachment lays the foundation, making your security interest legally valid between you and the borrower. Perfection builds the walls, making your claim strong enough to stand up against the rest of the world.

If you miss a step, your claim on the collateral could be weak, unenforceable, or pushed to the back of the line behind another creditor.

The First Step: Attachment

Attachment is the moment your security interest becomes legally enforceable against the debtor. It's when your claim officially "attaches" to the collateral. For this to happen under the Uniform Commercial Code (UCC), three things must occur at the same time:

- Value Has Been Given: This one’s pretty straightforward. You, the creditor, have to provide something of value, like a loan, a line of credit, or goods sold on account.

- The Debtor Has Rights in the Collateral: The person or business pledging the asset must actually own it or have the right to pledge it. You can't use your neighbor's delivery truck as collateral for your own business loan.

- A Security Agreement Exists: There has to be an agreement that grants you a security interest. While this can sometimes be verbal if you physically possess the collateral (like a pawn shop holding jewelry), the only safe way is a written document. It must be signed by the debtor and clearly describe the collateral.

A solid, written security agreement is the cornerstone of any secured transaction. Without one that precisely identifies the collateral, your claim is built on sand and likely to crumble when you need it most.

This process is what turns a simple promise to repay into a secured debt, backed by a specific asset.

The diagram above shows this flow—the loan is linked to specific collateral, and a legal agreement locks in your position.

The Second Step: Perfection

Once your interest has attached, the next move is perfection. If attachment is the private handshake between you and the debtor, perfection is shouting your claim from the rooftops. It puts everyone else on notice that you have a legal right to that specific asset.

This public announcement is critical for establishing your priority. What happens if a desperate debtor pledges the same piece of equipment to two different lenders? Generally, the one who perfected their interest first wins. It's the legal equivalent of planting your flag on the asset for all to see.

For most business assets in Connecticut—things like inventory, equipment, or accounts receivable—the standard way to perfect your interest is by filing a UCC-1 financing statement. This is a public document filed with the Connecticut Secretary of State. It contains basic information: the debtor's name, your name as the secured party, and a description of the collateral. Filing it creates a public record and solidifies your place in line.

While other methods exist, like taking physical possession of jewelry or gaining legal control over a bank account, the UCC-1 filing is the go-to for most commercial deals.

Getting this right is a technical process where every detail matters. A simple typo in the debtor’s legal name or a vague description of the collateral can render your entire filing useless. The need for precision is similar to what contractors face when they learn how to file a mechanic's lien to get paid for work on real estate. In both cases, you have to follow the legal playbook exactly for your claim to be effective.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Understanding the Priority Ladder of Creditors

When a business hits a rough patch and can't pay its bills, one question trumps all others: who gets paid first? It’s not a free-for-all. The law establishes a clear hierarchy for who gets paid and in what order—a system we call the priority ladder.

At its core, the priority ladder operates on a simple but powerful principle: "first in time, first in right." This means creditors who locked in their legal claims earlier generally get paid before those who came later. Knowing exactly where you stand on this ladder can be the difference between getting paid in full and walking away with nothing.

The Rungs of the Ladder

Picture a small manufacturing company in Connecticut that’s juggling several loans and supplier debts. When it finally defaults, its creditors all show up, but their claims aren't equal.

The ladder has very distinct levels, and a creditor's spot is decided by whether their loan is secured and, just as importantly, if that security interest has been "perfected."

-

Top Rung - Perfected Secured Creditors: These are the creditors in the strongest position. They not only have a signed security agreement (attachment) but have also put the world on notice by filing a public record, usually a UCC-1 financing statement (perfection). They get first claim on the specific collateral that backs their loan.

-

Middle Rung - Unperfected Secured Creditors: This group did part of the work. They have a valid security agreement with the debtor, but they never took the final step to perfect it. Their claim is good against the debtor, but they can easily lose their spot in line to another creditor who did perfect their claim or to a bankruptcy trustee.

-

Bottom Rung - Unsecured Creditors: At the very bottom are creditors who extended credit on nothing more than a promise. Think of suppliers who sold goods on credit or a standard credit card company. They only see a dime if there’s any cash left after every single secured creditor has been paid in full.

In our manufacturer's case, the bank that perfected its security interest in the factory's equipment gets paid first from the sale of those machines. The supplier who has an unperfected interest might get nothing, and the office supply company with no security at all will almost certainly be left empty-handed. This strict hierarchy is fundamental when dealing with complex situations like liens on foreclosures and other default scenarios.

A Special Exception: The Purchase Money Security Interest

While "first in time" is the general rule, there’s a major exception that can completely rearrange the priority ladder: the Purchase Money Security Interest (PMSI).

A PMSI gives a creditor what’s known as "super-priority," letting them jump to the very front of the line, even ahead of creditors who perfected their claims years earlier. This special status is reserved for a lender who provides the specific funds a debtor needs to buy a new asset.

For example, let’s say a bank already has a blanket security interest covering all of the manufacturer’s "current and after-acquired equipment." Later, a specialty finance company lends the manufacturer money to buy a brand-new, high-tech cutting machine. If that finance company follows the specific UCC rules for perfecting its PMSI, it gets first priority only on that new machine. The rule exists to encourage lenders to finance new equipment, knowing their investment won't automatically fall behind older, broader claims.

The existence of a strong, predictable priority system for secured creditors is not just a legal detail; it's a fundamental driver of economic activity. It gives lenders the confidence to extend credit, knowing their rights are protected.

This confidence has a real-world, measurable impact. Research from the World Bank shows that countries with robust secured-lending laws and public collateral registries see major increases in private credit and lower interest rates for borrowers. In fact, jurisdictions with high scores for creditor protection reported private credit-to-GDP ratios near 60%, compared to just 30% in countries with weaker legal systems. You can discover more about these global lending trends and see the data for yourself. It’s a powerful reminder of why meticulous documentation and timely perfection are so critical for Connecticut lenders.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How Secured Creditors Enforce Their Rights

When a borrower defaults on a secured loan, the whole game changes. That security agreement, once just a piece of paper in a file, suddenly becomes your most powerful tool. As a secured creditor, you have several legal remedies to get back what you're owed—and many don't even require you to step foot in a courtroom.

These enforcement rights are what give a security interest its teeth.

The goal is simple: take control of the collateral and turn it into cash to pay off the outstanding debt. While the exact steps depend on the collateral and the agreement, the process is governed by strict rules designed to protect both you and the debtor. Getting this right is critical for enforcing your rights legally and effectively here in Connecticut.

Self-Help Repossession: The First Line of Action

One of the most potent and immediate tools you have is self-help repossession. This right, granted under the Uniform Commercial Code (UCC), allows you to take possession of tangible collateral—think company cars, construction equipment, or inventory—without needing a court order first.

But this power comes with a major catch: the repossession must happen without a "breach of the peace."

What exactly is a breach of the peace? The law doesn't give a neat definition, leaving it up to the courts. Generally, it means you cannot:

- Use force or make threats. Any physical confrontation or intimidation is out of bounds.

- Enter a private home without permission. You can't break into a debtor's house or garage to get the collateral.

- Deceive or trick the debtor. Posing as a police officer or using other tricks is illegal.

- Continue if the debtor objects. If the debtor clearly tells you to stop or physically blocks you, you have to back off and go through the courts.

Basically, if you can't repossess the property peacefully, you have to pivot to a court-ordered process.

The UCC Foreclosure Sale

Once you have the collateral, the next step is to sell it. This isn't just a simple private sale; it's a formal process called a UCC foreclosure sale. The single most important rule is that every part of the sale must be "commercially reasonable."

This standard covers everything—the advertising, the timing, the location, and the method of the sale. The idea is to get a fair market price for the asset, which helps you recover as much as possible and reduces the debtor's remaining liability.

The standard of commercial reasonableness is the bedrock of a UCC foreclosure sale. If you get this wrong, a court can penalize you significantly, potentially even wiping out your right to collect any money still owed after the sale.

To meet this standard, you must give the debtor reasonable notice before the sale. This notice gives them one last chance to redeem the collateral by paying off the entire debt. The sale can be a public auction or a private sale, but the method has to be right for the type of asset to attract real buyers and get a fair price. You can learn more about the complexities of these actions in our detailed guide on foreclosing a lien in Connecticut.

If the sale doesn't bring in enough cash to cover the full debt, you can often sue the debtor for the rest—this is called a deficiency judgment. On the other hand, if there’s a surplus, you have to give it back to the debtor. The whole process shows why being a secured creditor gives you a direct path to recovery, but it’s a path you have to walk with legal precision.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Navigating Your Rights in a Bankruptcy Case

When a borrower files for bankruptcy, the court immediately issues an automatic stay. Think of it as a legal time-out. This order instantly freezes all collection activities, lawsuits, and repossessions, giving the debtor some breathing room. For a secured creditor, however, this isn't a dead end—it's simply a change in venue and strategy.

Even with the automatic stay in place, your security interest in the collateral doesn't just disappear. The bankruptcy court now supervises the process, but your status as a secured creditor still gives you a major advantage over anyone holding unsecured debt. You have specific legal tools available to protect your claim to that collateral.

Seeking Relief from the Automatic Stay

One of the first and most important moves a secured creditor can make is filing a motion for relief from the automatic stay. This is a formal request asking the bankruptcy court for permission to move forward with your enforcement rights—like repossession or foreclosure—despite the bankruptcy filing.

A court is likely to grant your motion for a few key reasons:

- There’s a Lack of Equity: If the borrower owes you more on the collateral than it's worth, they have no equity in it. In these situations, the court often agrees that the asset isn't critical to a successful reorganization.

- The Asset Isn’t Necessary for Reorganization: You can argue that the debtor's business can continue to operate and restructure its finances without that specific piece of collateral.

- You Haven’t Received Adequate Protection: If the collateral is losing value (think of a depreciating truck) and the debtor isn't making payments to offset that loss, the court may agree you need to take possession to protect your interest.

If your motion is successful, you can step outside the main bankruptcy proceeding and enforce your rights directly against the collateral, just as you would have before the bankruptcy was ever filed.

The Bifurcation of Your Claim

Bankruptcy fundamentally changes how your claim is valued, especially when the collateral is worth less than what's owed. This is precisely where being a secured creditor makes all the difference. Under the U.S. Bankruptcy Code §506(a), your claim is often split into two parts.

A bankruptcy filing doesn't erase your security interest; it redefines it. The court will value your collateral, and that value determines the size of your secured claim, which is the portion most likely to be paid in full.

Let's say you financed a piece of equipment for $100,000. Due to depreciation and market changes, it’s now only worth $70,000. The court will "bifurcate," or split, your claim like this:

- A Secured Claim: This part is equal to the collateral's current value—in this case, $70,000. This portion of your debt is protected and has top priority for repayment from that asset.

- An Unsecured Claim: The remaining $30,000 shortfall is reclassified as an unsecured claim. It gets lumped in with all the other general unsecured debts, like credit card bills and unpaid vendor invoices.

This split has a massive impact on what you ultimately recover. Your secured claim will often be paid in full through the bankruptcy plan or by the debtor surrendering the collateral. The unsecured portion, on the other hand, might only get pennies on the dollar—if anything at all. You can explore detailed federal guidance on this process to see why this numeric split is central to every bankruptcy case. It's the single most important reason why having a perfected security interest is critical before a borrower runs into financial trouble.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Protecting Your Financial Interests in Connecticut

Knowing the rules of secured transactions is one thing; putting them into practice effectively is what truly protects a Connecticut business. The lesson here is simple: becoming a secured creditor gives you a powerful advantage, but only if you follow the process to the letter. This means having a rock-solid security agreement, perfecting your interest correctly and on time, and keeping a close watch on your collateral.

The Uniform Commercial Code is a technical roadmap, and one wrong turn can have serious consequences. I've seen even savvy businesses make simple, costly mistakes that weaken or even void their security interests, leaving them just as vulnerable as an unsecured creditor when a debtor defaults.

Common and Costly Mistakes to Avoid

Creditors often fall into the same predictable traps that put their claims at risk. Being aware of these common missteps is the best way to sidestep them:

- Vague Collateral Descriptions: Simply stating "all assets" in a security agreement often isn't enough to hold up in court. The description needs to be specific enough for a third party to reasonably identify what property is being used as collateral.

- Failing to Perfect Properly: It sounds minor, but a single typo in the debtor's legal name on a UCC-1 financing statement can make your filing completely ineffective. An error like that can send you right to the back of the line behind other creditors.

- Missing Continuation Deadlines: A UCC-1 filing is only good for five years. If you forget to file a continuation statement before that deadline, your perfected status disappears. It’s a silent but devastating mistake.

Understanding the legal concepts behind secured transactions is a powerful start, but expert execution is what truly protects your assets. The complexities of attachment, perfection, and enforcement demand professional guidance to ensure you are fully and legally protected.

Don't leave your financial security to chance. Navigating the nuances of secured transactions requires a deep and practical understanding of Connecticut business law. While this guide gives you a solid foundation, applying these principles correctly to your unique situation is where professional legal counsel becomes indispensable.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Secured Creditor FAQs: Answering Your Pressing Questions

When you're dealing with secured transactions, a lot of "what if" scenarios can come to mind. It’s only natural. Here are some clear answers to the questions we hear most often from business owners, breaking down how these concepts play out in the real world.

What Happens If the Collateral Is Destroyed?

This is a scenario every secured creditor dreads, but it's exactly why the security agreement is so important. A properly drafted agreement will always require the debtor to keep the collateral insured. More importantly, it will name you, the creditor, as the "loss payee" on that insurance policy.

Think of it this way: if that piece of heavy machinery you financed goes up in flames, the insurance check is cut directly to you, not the debtor. This allows you to satisfy the outstanding loan balance immediately. Without that loss payee clause, you’d be left with an unsecured claim against a debtor who just lost a critical asset—a much weaker position to be in.

Can a Business Just Sell an Asset I Have a Lien On?

In short, no—at least not without your permission. That UCC-1 financing statement you filed does more than just perfect your interest; it puts the entire world on notice. Any diligent buyer will run a UCC search and see your lien plain as day.

If a debtor does go rogue and sells the asset anyway, your security interest generally follows the collateral right into the new owner's hands. That means you could still have the right to repossess it. On top of that, your interest can also attach to whatever cash or property the debtor received in the sale. Most commercial loan agreements have a "due on sale" clause to stop this from happening in the first place, making the entire loan balance due if the collateral is sold without consent.

How Is a Security Interest in Real Estate Different?

This is a crucial distinction. While the idea is the same—using property to back a loan—the legal rulebook for real estate is completely different from the one for business assets. For real estate, you don't use a security agreement and a UCC-1. Instead, you use a mortgage or a deed of trust.

These documents get recorded in the town's land records where the property sits, not filed with the Secretary of State. The enforcement process is also a world apart. You can't just repossess a building; you have to go through a formal court process called a judicial foreclosure.

While both create a lien on property to secure a debt, the legal framework for real estate (mortgages) is entirely separate from the Uniform Commercial Code (UCC) that governs personal property like equipment, inventory, and receivables.

The core principles of getting a lien (attachment), making it public (perfection), and figuring out who gets paid first (priority) are still there. But the specific steps, documents, and laws are completely distinct. Knowing which path to follow is absolutely critical to protecting your investment.

Navigating the complexities of secured transactions requires careful planning and precise execution. To ensure your financial interests are fully protected, professional legal guidance is essential. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.