You're often introduced to a UCC filing at exactly the moment you're trying to get something done. You're closing an equipment loan, opening a working capital line, buying inventory on supplier terms, or cleaning up diligence before a sale. Then someone mentions a UCC-1, a search, or a termination, and what sounded like routine paperwork starts to look like a lien problem.

That reaction is understandable. A UCC filing sits at the intersection of finance, public records, and priority rights. It affects lenders, borrowers, buyers, and investors differently. In Connecticut, it also becomes a practical process issue because getting the filing right is only part of the job. Managing it over time is just as important.

A practical business owner usually doesn't need another abstract definition. What matters is what a UCC filing does, how it affects your financing options, and where businesses get into trouble.

Why UCC Filings Matter for Your Business

A Connecticut business closes on new equipment on Friday. By Monday, the lender expects its lien in place, the borrower wants to draw funds, and a second creditor may already be searching the record. That is where a UCC filing stops being paperwork and starts affecting priority, flexibility, and risk.

For a lender, the filing is how a claimed interest in collateral becomes visible to the market. For a borrower, it becomes part of the company's financing profile. It can affect the next credit facility, a refinancing, investor diligence, or the sale of a business unit. Businesses that treat UCC filings as an administrative detail often discover the problem later, when a deal stalls because an old filing is still of record or a broad lien blocks new money.

In practice, the question is not only what a UCC filing is. The harder question is what it does over time. A properly handled filing can protect repayment rights and support a clean priority position. A poorly handled one can create avoidable disputes over collateral, delay closings, and reduce negotiating room when the business needs additional capital.

That trade-off matters on both sides of the transaction.

Borrowers should review the collateral description with the same care they give the interest rate and repayment terms. A filing against "all assets" may be acceptable in one deal and a serious constraint in the next. If a future lender wants a first-priority lien on receivables, inventory, or specific equipment, an existing UCC record can force an intercreditor negotiation, a payoff, or a lien release before the new financing can close.

Lenders have a different problem. Their documents may give them contractual rights, but a filing error can still weaken priority against other creditors or a bankruptcy estate. That is why secured lending depends on more than loan approval. It depends on correct filing, continued maintenance, and follow-through when amendments, continuations, or terminations are required. For a useful companion on the creditor side, see this explanation of what a secured creditor is.

One practical rule is simple. Treat every UCC filing as a live business issue, not a closing checklist item.

That approach also improves loan administration. Teams that monitor lien position, collateral coverage, and portfolio performance tend to spot problems earlier, and resources such as Visbanking insights for loan profitability can help frame the credit side of that review. In Connecticut, where filing accuracy and follow-up directly affect later transactions, the businesses that do this well are usually the ones that can refinance, expand, or sell with fewer surprises.

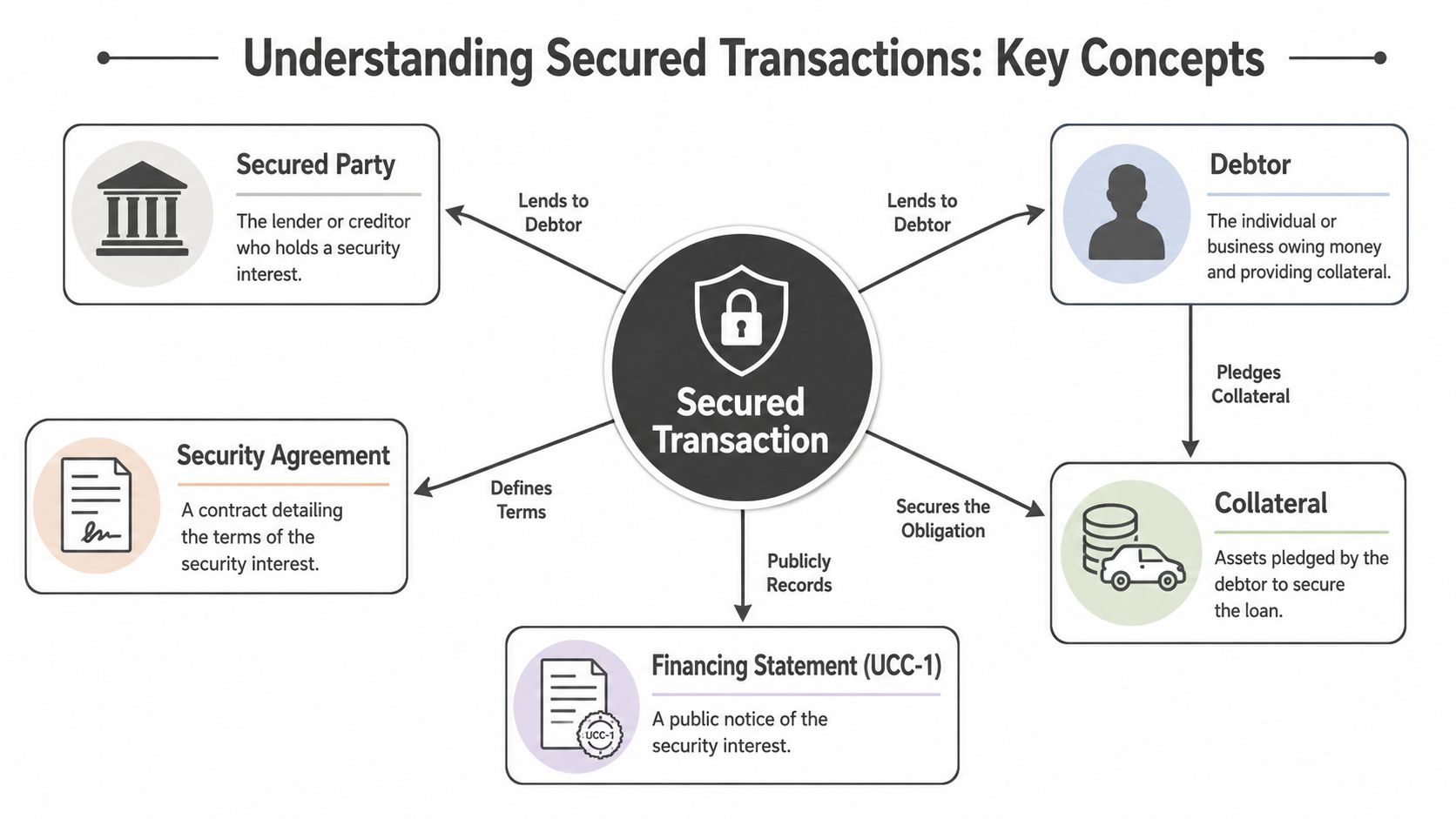

The Building Blocks of a Secured Transaction

Most confusion around UCC filings comes from mixing up the private loan documents with the public filing. They're related, but they're not the same thing.

At the core, a secured transaction has four moving parts:

- Secured party. The lender, creditor, or financing source claiming rights in collateral.

- Debtor. The business or individual granting those rights.

- Collateral. The personal property that supports repayment.

- Security agreement. The contract that creates the security interest between the parties.

A useful analogy is a home mortgage. The loan documents set the deal between borrower and lender. The recorded mortgage tells the world the lender has rights in the property. In commercial finance, the UCC system plays a similar notice function for many categories of personal property.

Attachment and perfection

The security interest first has to become enforceable between the parties. Lawyers call that attachment. In practical terms, the debtor grants the interest, value is given, and the collateral is identified with enough clarity to make the deal enforceable.

Then comes perfection. That's the step that usually matters against third parties. In many business transactions, perfection happens by filing a UCC-1 financing statement in the proper jurisdiction. If you want a focused discussion on that process, this article on how to perfect a security interest breaks it down well.

A lender can have a signed security agreement and still have a problem if it doesn't perfect correctly. That's why commercial lenders, counsel, and credit teams build filing review into closings.

Priority is where the real fight happens

Priority decides who stands ahead of whom when collateral value isn't enough for everyone. That issue becomes critical in workouts, insolvency, distressed sales, and refinancing.

Here's the practical version:

- One lender files early and files correctly.

- Another lender comes in later and wants the same collateral.

- The earlier filing often controls the outcome.

That's why due diligence teams run searches before closing. It's also why finance teams track filed liens over time rather than assuming an old record no longer matters. On the analytics side, lenders often pair legal lien review with portfolio performance work. Resources like Visbanking insights for loan profitability can be useful for understanding how underwriting and collateral strategy fit into broader credit performance decisions.

A strong security agreement without proper perfection is incomplete. A filed UCC without a sound collateral package is also incomplete.

The UCC-1 Financing Statement Unpacked

A Connecticut company closes a new credit facility on Friday, then learns on Monday that the lender filed against broader collateral than the owners expected. Nothing about the filing changes the loan economics overnight, but it can change the company's flexibility. That is why experienced borrowers and lenders treat the UCC-1 as more than clerical paper.

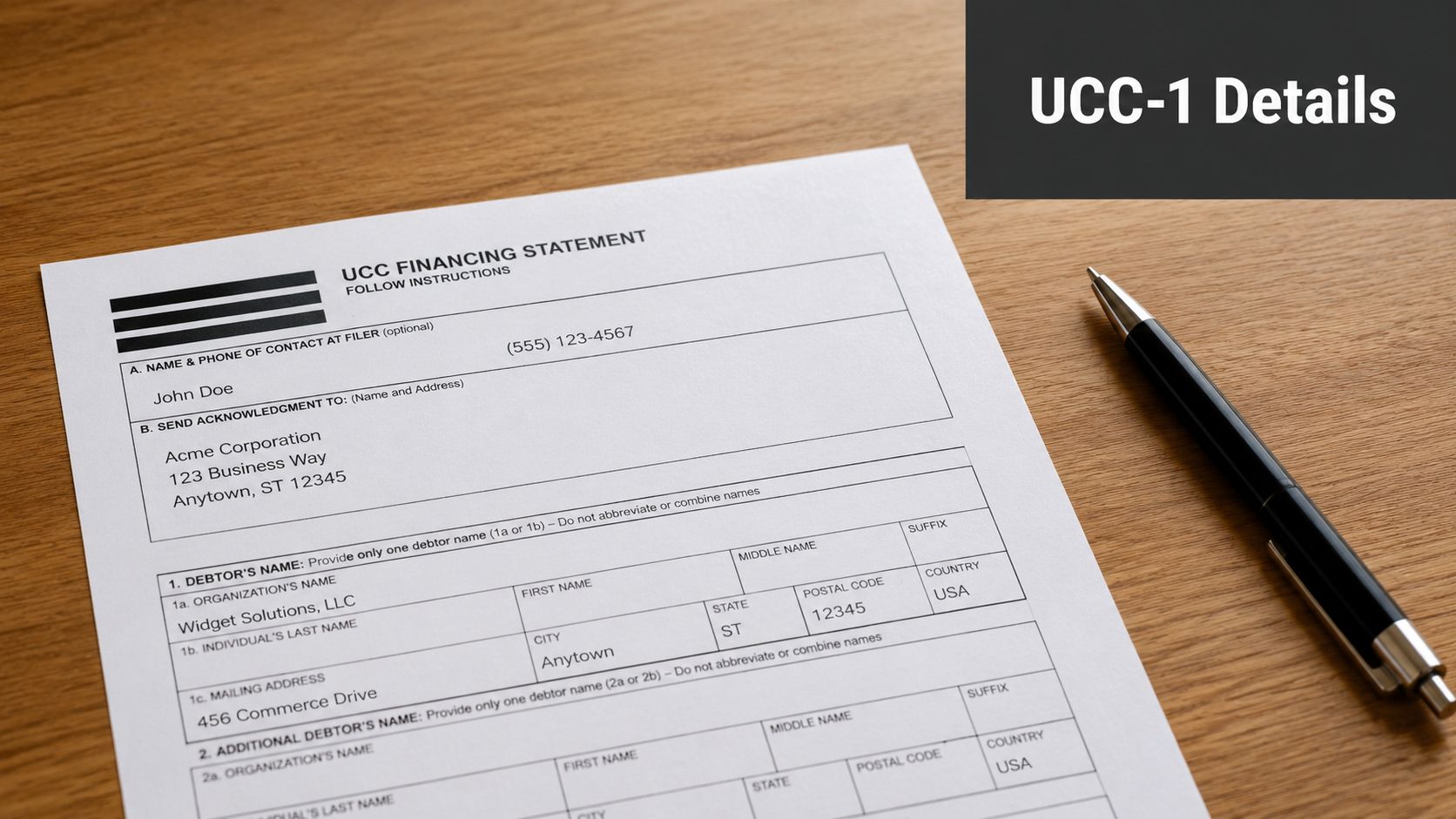

A UCC-1 is the public notice document in a secured transaction. It tells the market that a creditor claims an interest in identified collateral. The filing does not replace the security agreement, and it does not spell out the full bargain between the parties. Its value is practical. It puts other lenders, buyers, and diligence teams on notice that they need to ask harder questions.

What the filing usually includes

A standard UCC-1 generally identifies:

- The debtor's exact legal name

- The debtor's mailing address

- The secured party's name and address

- A description of the collateral

The debtor name deserves more attention than any other line item. For a registered organization, the name should match the public formation record exactly. Small errors matter. An omitted word, the wrong entity suffix, or use of a trade name can create a filing problem that shows up later in diligence, enforcement, or a refinancing.

The filing also needs to match the deal structure. If counsel drafts a careful security agreement but the financing statement describes the wrong debtor or collateral category, the public record may fail to give the notice the lender expected. For a more form-specific explanation, see this overview of what a UCC financing statement is.

Collateral language drives business consequences

The collateral description is where strategy becomes visible. A lender financing one machine may file against that machine alone. A working capital lender may cover inventory, accounts, deposit accounts, and proceeds. A blanket lien may reach nearly all personal property of the business.

Each approach has trade-offs.

- Specific collateral filings fit limited-purpose loans and reduce spillover into unrelated assets.

- Category-based filings are common where the borrowing base changes over time, especially with receivables or inventory.

- Blanket filings give the secured party broad protection, but they often create the most resistance in future financings, intercreditor discussions, and exit transactions.

Borrowers should read the collateral description as carefully as the interest rate section. "All assets" may be acceptable in one deal and too restrictive in another. Lenders should be equally disciplined. Overbroad language can be commercially efficient, but it also increases the chance of later disputes over lien scope, required releases, and whether a termination must be partial or complete.

If the lender calls the filing standard, ask which assets it reaches, what exclusions apply, and what must happen at payoff to clear the record.

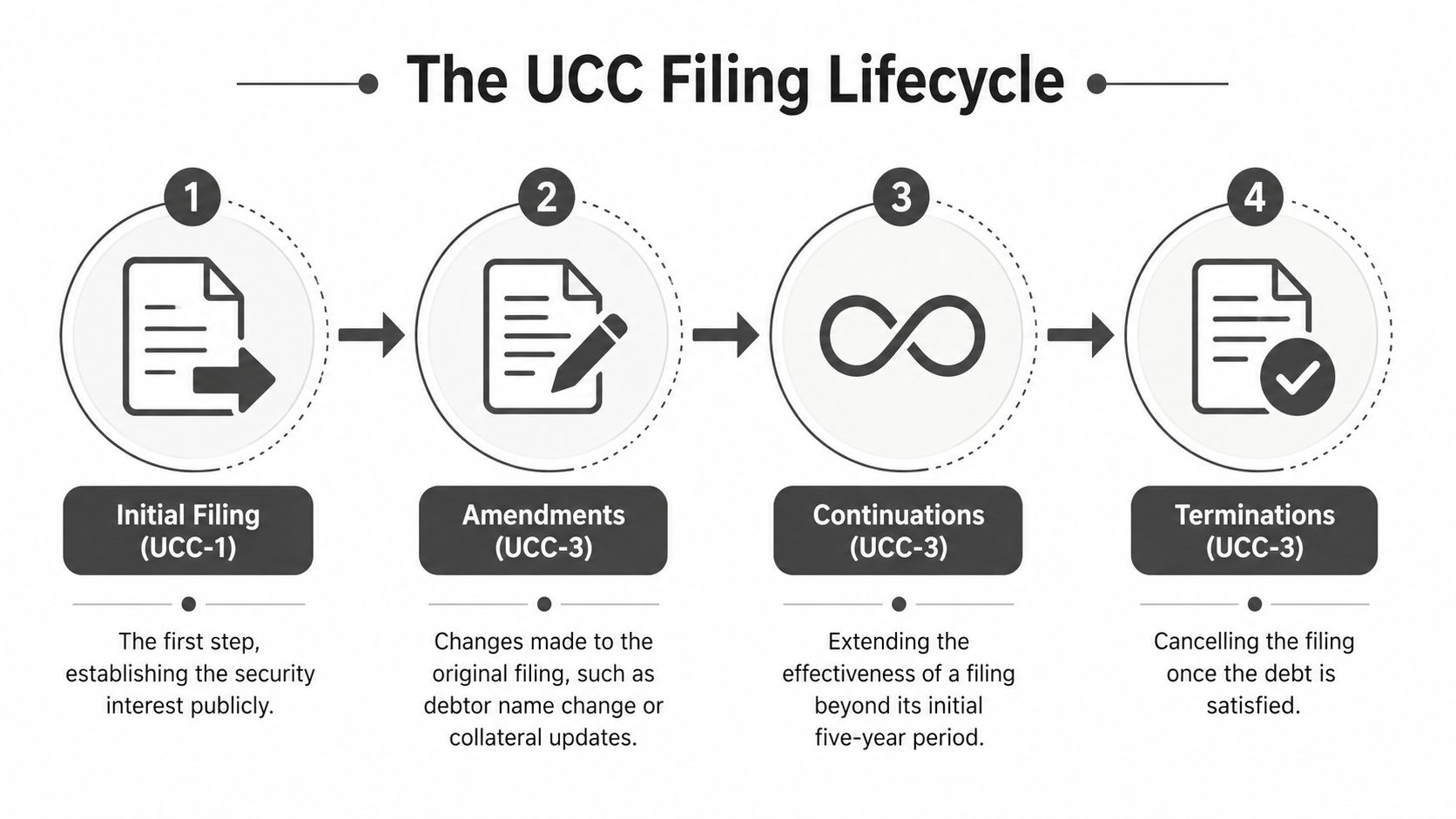

In practice, the UCC-1 is the start of a filing lifecycle, not the end of the analysis. The initial filing has to be accurate on day one, but it also needs to hold up through amendments, continuations, payoffs, and future deal activity.

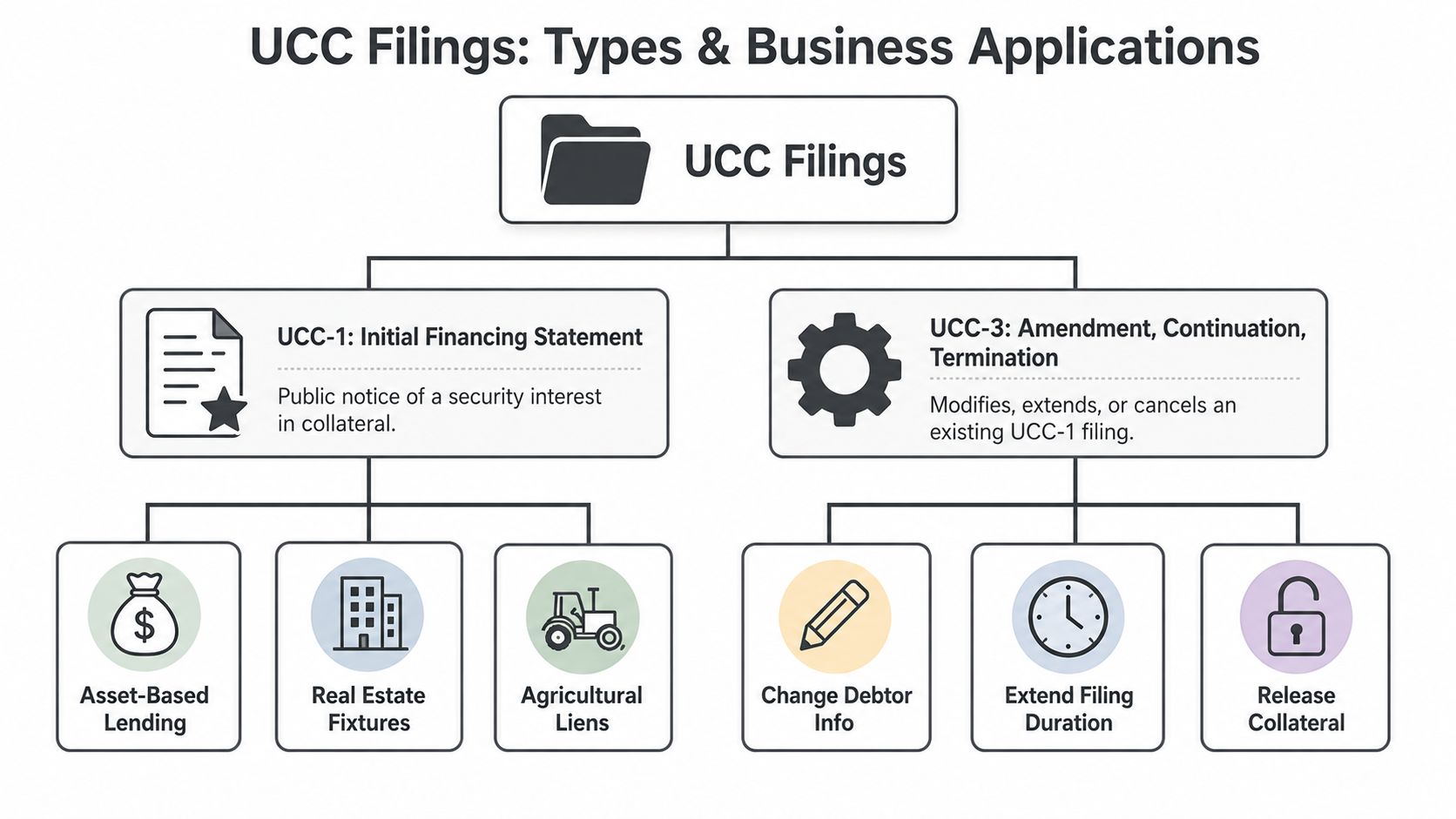

Common Types of UCC Filings and Their Business Uses

Most business people hear “UCC filing” and think only of the initial filing. In practice, the system includes several filing types, and each serves a different purpose in the life of the deal.

The initial filing

The UCC-1 financing statement starts the public record. A bank may file it in connection with an equipment loan. A factor or asset-based lender may file against receivables. A supplier that sells goods on credit may also use a filing structure to protect itself in appropriate circumstances.

In M&A diligence, buyers and investors routinely search these records because they want to know whether business assets are already encumbered. In distressed situations, those searches become even more important because lien position shapes influence.

The follow-up filings

Once a UCC-1 exists, later actions are typically handled through a UCC-3. That form can be used for several very different functions:

- Amendment. Change information in the record, such as debtor details or collateral language.

- Continuation. Extend the effectiveness of the original filing before it lapses.

- Assignment. Transfer the secured party's rights to another creditor.

- Termination. End the public notice after payoff or release.

These aren't technical afterthoughts. They're operational necessities. A secured creditor that ignores post-closing maintenance can lose the value of its filing position, and a borrower who ignores old records may find them resurfacing in a later financing or sale.

Specialized business settings

UCC filings also show up outside ordinary bank lending. Government-related and regulated finance transactions use them as well. For example, HUD guidance cited by Incorp states that entities with interests in Section 202 and 811 properties must file a UCC at closing and then every five years thereafter, which shows how embedded UCC practice is in specialized finance programs. See Incorp's discussion of UCC searches and filings.

That's a useful reminder. UCC practice isn't just for banks making middle-market loans. It appears in supplier credit, real estate-adjacent transactions, structured finance, and diligence across industries.

A Practical Guide to UCC Filings in Connecticut

In Connecticut, the legal analysis and the filing mechanics need to line up. Businesses often know they need “a UCC filing,” but the primary questions are where to file, how to search, what to submit, and what to track after acceptance.

The state-level filing office for most UCC records is the Connecticut Secretary of the State, and electronic filings are commonly handled through the CONCORD system. Before filing anything, a business or lender should usually search existing records under the correct legal debtor name. That search tells you whether another creditor is already in line, whether an old filing is still active, and whether payoff or subordination discussions need to happen before closing.

How Connecticut businesses usually approach the process

A practical workflow often looks like this:

- Confirm the debtor name from the formation record or other controlling legal document.

- Run a UCC search before closing to identify competing claims.

- Prepare the filing with a collateral description that matches the deal.

- Submit through CONCORD if filing electronically.

- Review the acceptance record and calendar the next lifecycle date immediately.

For owners doing broader branding or transaction cleanup work before financing, it's common to coordinate legal housekeeping with marketing and operations updates too. If that overlap exists, a local resource like this list of best graphic design companies in CT can be useful on the branding side while counsel handles the lien and entity record issues.

Connecticut UCC Filing Quick Reference 2026

| Action | Form | Filing Fee (Online) | Effective Period |

|---|---|---|---|

| Initial financing statement | UCC-1 | Qualitatively, fees vary by state and filing method | Generally five years |

| Amendment | UCC-3 | Qualitatively, fees vary by state and filing method | Tied to original record |

| Continuation | UCC-3 | Qualitatively, fees vary by state and filing method | Extends existing filing |

| Termination | UCC-3 | Qualitatively, fees vary by state and filing method | Ends public notice |

Because state procedures differ, the operational point is more important than any one form entry. Filing rules aim for uniformity, but state filing fees and methods differ materially, and the key takeaway is that a UCC filing is not a one-time form because its lifecycle and state-specific procedures matter just as much as the initial filing, as explained by CSC's UCC filing services overview.

What usually works and what doesn't

What works in Connecticut is disciplined name review, pre-closing search work, and deadline tracking. What doesn't work is assuming a filing clerk, lender portal, or standard template will catch legal errors for you.

Businesses that file regularly also benefit from having a repeatable internal checklist. If you need a practical filing-oriented companion, this article on how to file a UCC lien is a useful operational reference.

In Connecticut practice, the filing itself is rarely the hard part. The hard part is making sure the filing reflects the right debtor, the right collateral, and the right strategy.

After the Filing Amendments Continuations and Terminations

A lender closes on inventory collateral in January. By October, the borrower has changed its legal name, absorbed an affiliate, and paid off one facility while drawing on another. If the public record is not updated to match those changes, the filing can stop doing the job everyone expected it to do.

The practical point is simple. A UCC filing has a lifecycle, and that lifecycle needs active management. In Connecticut practice, problems often arise after closing, when the parties assume the original filing can sit untouched until the debt is paid.

Amendments when facts change

An amendment is not a housekeeping form. It is the public record catching up to the transaction as it exists.

Common triggers include a debtor name change, a merger or conversion, an assignment by the secured party, or a negotiated change to the collateral package. Some changes can be handled with a UCC-3 amendment. Some require more than that, including a fresh look at whether a new filing is needed to preserve perfection and priority. The answer depends on the type of debtor, the nature of the change, and the timing.

That timing matters. If a borrower changes its legal name and no one follows through promptly, later search results may no longer tell the full story. In a refinance, acquisition, or audit, that gap creates immediate friction. The lender may face a priority fight. The borrower may face closing delays while counsel reconstructs what should have been updated months earlier.

Continuations before lapse

Financing statements do not stay effective indefinitely. They generally remain effective for a set period and then lapse unless a continuation is filed within the permitted window.

For secured parties, continuation tracking should be treated like any other maturity or covenant deadline. Missing it can mean losing perfected status as to collateral that still secures real debt. At that point, the filing problem becomes a business problem. A lender may lose priority against a later creditor or a bankruptcy trustee, and fixing the record after lapse does not always restore the original position.

For borrowers, continuations matter too. An old filing that should have lapsed may still appear in a search until diligence counsel sorts out the record. A filing that was properly continued may also signal that a lender still claims rights in assets the borrower expected to finance elsewhere. Either way, the search result affects deal timing and bargaining power.

Terminations after payoff

Termination is where many file management issues become visible.

The debt is paid. The relationship may be over. Yet the filing remains in the public record, and the next lender, buyer, or investor sees an active lien notice tied to the borrower's assets. In Connecticut deals, that is a common source of avoidable cleanup work.

The sound approach is operational, not theoretical:

- After payoff, confirm whether the secured obligation has in fact been satisfied in full and whether any collateral remains tied to another facility or guaranty.

- Before authorizing a termination, check the loan documents and any cross-collateralization language so a release does not go out too broadly.

- Before a new financing or sale process, run updated searches and match each active filing to a live obligation, not to memory or email traffic.

- During diligence, ask for filed terminations or other record evidence. Verbal confirmation from a former lender is not enough.

Borrowers often assume payoff automatically clears the filing. It does not. Someone still has to prepare, authorize, and file the termination, and someone should confirm that it appears in the record.

A paid loan and a cleared UCC record are related events, but they are not the same event.

The broader strategy is straightforward. Treat amendments, continuations, and terminations as part of the secured transaction from day one, not as clerical cleanup after the fact. That approach protects lender priority, reduces borrower friction in later financings, and keeps Connecticut diligence from turning into a file reconstruction exercise.

UCC Filing Risks and When to Consult an Attorney

A Connecticut borrower pays off a credit line, assumes the lien problem is over, and starts negotiating a new facility. During diligence, the new lender finds an old UCC filing that still appears to cover inventory, accounts, and proceeds. The closing slows down while everyone tries to determine whether the prior lender still has a live claim or whether the record was never cleaned up.

That is how UCC problems usually surface. Not as abstract filing issues, but as delays, reduced negotiating power, added legal spend, and pressure at the worst point in a transaction.

Priority disputes are where the most serious conflicts arise. A small error in the debtor name can undermine a filing. A collateral description that was drafted too broadly can restrict later borrowing more than either side expected. A missed continuation can leave a lender exposed. An old filing that should have been terminated can interfere with new equipment financing, asset-based lending, investor diligence, or a sale process even if the original debt is no longer a real business issue.

The trade-offs are practical. Lenders often want collateral descriptions broad enough to cover future risk and avoid gaps in perfection. Borrowers usually want enough room to add a working capital line, finance new equipment, or close an acquisition without returning to the same lien cleanup problem. Those goals can coexist, but only if the documents, filing strategy, and post-closing follow-through are aligned from the start.

When legal review is worth it

Attorney involvement makes sense when:

- The collateral package is broad and management wants to preserve flexibility for future financing.

- The borrower operates in multiple states and the correct filing jurisdiction or debtor identification needs closer analysis.

- There is a payoff, refinance, or lender change and releases, assignments, or amendments have to be timed correctly.

- A transaction is under diligence pressure from a buyer, investor, or senior lender and any filing defect could delay closing.

Forms do not solve those problems. The filing itself is short, but the legal and business consequences reach into priority, remedies, disclosure, and deal timing.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.