You’re probably here because you’re extending credit, financing equipment, taking a security interest in inventory, or trying to protect repayment on a business deal that already feels riskier than it did when the papers were first signed. In that moment, the question isn’t academic. It’s whether your claim will hold up if the debtor stops paying, another lender appears, or a bankruptcy case gets filed.

That’s where many creditors make a costly mistake. They treat the UCC filing as clerical work. It isn’t. A UCC filing is part legal notice, part priority tool, and part risk control. If it’s done correctly, it can put you in a strong position against competing creditors. If it’s done carelessly, you may discover too late that your “secured” deal wasn’t secured in any meaningful sense.

If you want to understand how to file a UCC lien the right way, start with this principle: the filing only helps if every critical detail is right.

Why a UCC Lien is Your Most Powerful Collection Tool

A customer misses payments, cash gets tight, and another lender suddenly appears claiming the same inventory, receivables, or equipment. At that point, the difference between being owed money and holding an enforceable security interest becomes expensive.

A UCC lien, usually reflected by filing a UCC-1 financing statement, gives a creditor public notice and priority rights that an unsecured claimant does not have. Under Article 9 of the Uniform Commercial Code, which applies across the United States, the filing is generally made in the appropriate filing office for the debtor’s state, often the Secretary of State, as outlined in this UCC filing overview. For Connecticut creditors, that filing decision is often straightforward in a single-state deal, but it gets more technical once the debtor is organized elsewhere, operates in multiple states, or the collateral includes assets tied to special filing rules.

That is the practical value of a UCC lien. It can move you from the general pool of creditors into a defined priority position against identified collateral.

What the filing actually gives you

The UCC-1 does not replace the underlying contract. The promissory note, security agreement, lease, or credit documents still define the deal and the collateral package. The filing matters because it helps make that security interest effective against third parties, including competing creditors, lien claimants, and a bankruptcy trustee.

That point gets missed all the time. A creditor can have signed loan documents, personal assurances, and a payment history that looks fine, then still lose ground because the public filing was never made, was filed in the wrong jurisdiction, or described the debtor incorrectly.

In practice, a properly perfected lien matters when:

- The debtor defaults and collection shifts from negotiation to asset recovery

- A bank or finance company files against the same collateral

- A bankruptcy case freezes the usual collection options

- A buyer, investor, or diligence team searches the public record

- The collateral is mobile, sold, deposited, or turned over in ordinary operations

A strong security agreement without a proper UCC filing often leaves a creditor with far less power than expected.

Why experienced creditors rely on it

Institutional lenders, equipment lessors, factors, and trade creditors use UCC filings because priority usually determines who gets paid first from business assets. This is the actual competition. The issue is not whether a debtor owes money. The issue is whose claim stands up when the assets are not enough to cover everyone.

A filing can cover specific collateral or all present and after-acquired assets, depending on the transaction. It also gives creditors a public record they can search before extending credit. That search can change the economics of a deal quickly. A proposed borrower may already have a blanket lien on all assets. Receivables may already be pledged. Equipment that looks available may already be encumbered.

Credit decisions should reflect that reality. Public filing searches are one piece of the analysis, and some creditors also review broader business intelligence sources such as InvestorPulse Reports when they want more context on ownership patterns, financing activity, and risk indicators surrounding a company.

For a practical primer on where a secured party stands in the collection hierarchy, see this explanation of secured creditor rights.

Why precision matters more than the form itself

Many business owners assume the power comes from having filed something. Legally, that is not enough. A UCC lien is only as good as the details behind it. The debtor name has to be correct. The filing office has to be correct. The collateral description has to match the transaction and the strategy. If the deal crosses state lines, those choices become even more important.

I tell clients the same thing in Connecticut matters. Courts and counterparties do not give partial credit for a filing that was almost right.

A UCC filing also has a limited life and must be maintained before it lapses. If that deadline is missed, priority can disappear at the worst possible moment, after default, during refinancing pressure, or in bankruptcy. That is why a UCC lien is such a powerful collection tool when handled with care, and why it becomes nearly worthless when treated as routine paperwork.

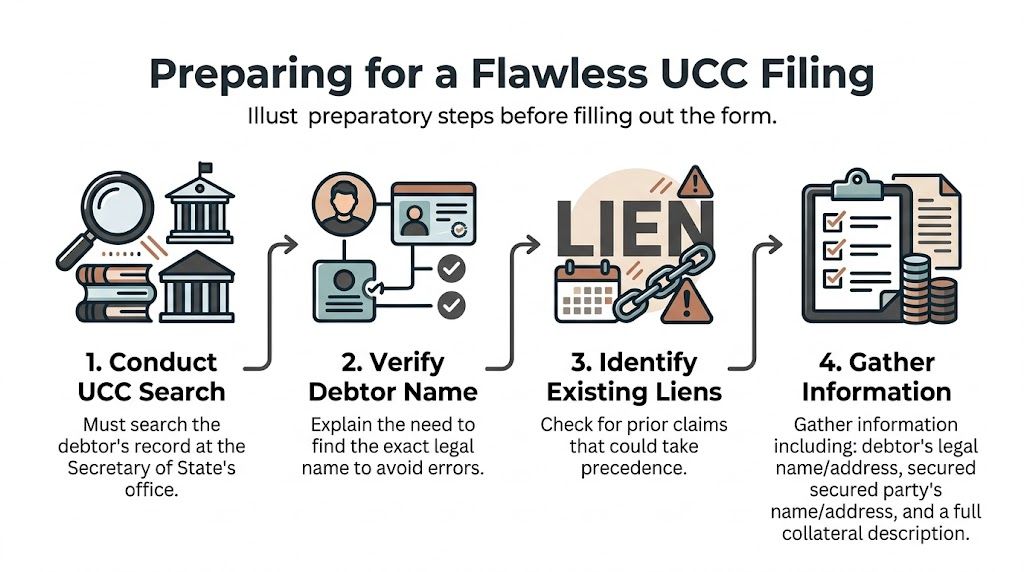

Preparing for a Flawless UCC Filing

Most UCC filing problems begin before anyone touches the form. The failure usually happens in the prep work. Someone copies a name from an invoice instead of formation documents, assumes the debtor’s home state is the right filing state for an entity, or describes collateral in a way that doesn’t match the underlying deal.

Preparation is where you protect yourself.

Start with the debtor record, not the deal summary

Before filing, pull the debtor’s exact legal information from the right source. For a company, that means the formal entity record and organizational documents, not marketing materials, email signatures, or the name printed on a truck. For an individual, it means using the legally correct identifying name rather than a nickname or trade style.

Then run a UCC search in the relevant filing office. You’re looking for two things at once:

- The exact debtor name used in public records

- Existing liens that may already have priority

This step often changes the deal conversation. A lender may discover a blanket lien already covers all present and after-acquired assets. A trade creditor may learn the borrower’s receivables are already encumbered. A purchaser may find that equipment being sold is subject to a prior filing.

Gather the information that actually belongs on the filing

Before you file, assemble the data set you’ll need to verify line by line:

- Debtor legal name and address

- Secured party legal name and address

- Collateral description tied to the security agreement

- The debtor’s jurisdictional facts

- Any fixture-related facts if the collateral is connected to real property

A lot of online content makes this process sound simple. Some practical industry explainers, including MCA UCC Filing Explained, help readers understand how these filings function in financing transactions. But what those summaries often miss is that the filing only works if the legal inputs are exact.

Search first. Draft second. Filing a UCC-1 before checking the debtor record is one of the fastest ways to create a false sense of security.

Review priority before you advance funds

A creditor who files perfectly but ignores existing liens can still end up disappointed. The filing protects your place in line only relative to what is already there and how your transaction is structured.

That means your due diligence should answer practical questions such as:

| Question | Why it matters |

||---|

| Is there an existing blanket lien? | It may already cover the same collateral you expect to claim. |

| Is the debtor using multiple entity names? | You need the correct legal debtor, not an affiliate or trade name. |

| Does the deal involve equipment, inventory, or receivables? | Different collateral categories create different drafting and priority issues. |

| Is any collateral attached to real property? | That may trigger an additional fixture filing requirement. |

For a more detailed discussion of the legal concept behind perfection, this article on how to perfect a security interest is a helpful reference.

Treat diligence like loss prevention

Creditors often focus on getting money out the door. Counsel focuses on whether the documents will survive a dispute. Both perspectives matter, but the second one is what keeps a collection problem from turning into a write-off.

A clean filing starts with disciplined intake:

- Verify the debtor from official records

- Check existing liens before relying on collateral

- Match the collateral language to the actual transaction

- Confirm where the filing belongs before submission

Those steps aren’t administrative padding. They are the difference between a perfected lien and an avoidable fight.

Completing the UCC-1 Form with Precision

The UCC-1 is a short form, but it’s unforgiving. Creditors sometimes assume that because the document is brief, the legal risk is low. The opposite is true. Short forms leave very little room for error because every field carries weight.

The debtor name field is the danger zone

The most important entry on the form is the debtor’s legal name. Under UCC Article 9, the debtor’s exact legal name is the critical element, and for registered organizations the filing should use the name from the most recent public organic record under UCC § 9-503(a)(1). Even small mismatches, including something like “Inc.” versus “Incorporated,” can make the filing “seriously misleading” and ineffective against third parties, as described in this guide to filing a UCC lien.

That rule catches well-established businesses more often than it should. People use a trade name, copy a billing profile, or shorten the entity name to what everyone in the industry calls the borrower. None of that controls. The filing has to identify the legal debtor correctly.

If the debtor is a Connecticut entity, use the exact name reflected in the Connecticut business record. Not the common name. Not the invoice footer. Not the “close enough” version.

Fill the form as if a hostile lawyer will read it later

That’s because one probably will.

At a minimum, the UCC-1 should accurately state:

- Debtor name and address

- Secured party name and address

- Collateral description

- Any applicable fixture or related indication, if relevant

The form is not where you improvise. If the deal documents say the collateral is specific equipment, don’t casually broaden the filing unless the security agreement supports that scope. If the agreement grants a blanket lien, make sure the filing reflects that approach clearly.

For a plain-language explanation of the filing instrument itself, see this overview of what a UCC financing statement is.

Broad collateral versus specific collateral

One of the recurring practical choices is whether to file broadly or narrowly. That depends on the transaction.

Blanket lien approach

A blanket lien is common in commercial lending and asset-based transactions. It usually covers substantially all business assets, often framed in broad terms such as all assets or all personal property, subject to the actual security documents.

This approach is useful when the lender wants a broad claim across inventory, equipment, accounts, and proceeds.

Specific collateral approach

A narrower description often makes sense when the creditor financed a particular asset or class of assets, such as leased equipment or identified receivables. Precision matters even more in that setting because the collateral description is doing more of the work.

A purchase money structure, for example, often demands tighter drafting than a general working capital line.

Bad drafting habits to avoid

Some errors are common:

- Using collateral language that doesn’t match the signed security agreement

- Listing internal account labels that don’t identify collateral meaningfully

- Assuming a trade description is legally sufficient

- Being so vague that a later reader can’t tell what was claimed

A filing is public notice. It should give a reader a workable understanding of what collateral is covered.

Think in terms of searchability and enforceability

A UCC-1 has to work in the filing system and later in a dispute. Those are different tests, and both matter. The filing office may accept something that still creates litigation risk later. A court may ask whether the record was seriously misleading, whether the collateral was adequately identified, and whether the filing corresponds to a valid security interest.

That’s why precision beats speed here. The best filers build a review process before submission:

- Pull the debtor name from the official record

- Compare the filing draft to the signed security documents

- Confirm party names and addresses

- Recheck collateral wording

- Submit only after a final legal review

Connecticut-specific practical point

In Connecticut matters, the most common filing errors are rarely exotic. They are usually ordinary data mistakes with expensive consequences. The filer uses the wrong entity name, files against the wrong debtor variant, or assumes the state filing alone covers collateral that intersects with real property issues.

That is why creditors should treat form completion as legal work, not just data entry. The UCC-1 may be short, but its effect on priority can be decisive.

Selecting the Correct Filing Jurisdiction and Method

A creditor closes a deal with a borrower operating out of Hartford, files in Connecticut, and assumes the lien is handled. Then the borrower defaults, another secured party appears, and the first question is not whether the debt is real. It is whether the filing was made in the right place. If the debtor is organized in Delaware, a Connecticut-only filing may do very little.

That is the point many creditors miss. The filing office is not chosen by where the trucks are parked or where the inventory happens to sit this month. In most transactions, the starting rule is the debtor’s location under Article 9. If that choice is wrong, the rest of the filing can be perfectly prepared and still fail where it matters most: priority and enforceability.

Start with debtor location, then test for exceptions

For most collateral, jurisdiction follows the debtor:

| Debtor type or collateral | Primary filing focus |

|---|---|

| Registered organization | State of organization |

| Individual debtor | State of residence |

| Fixtures tied to real property | Real estate records where the property is located, plus any required state-level filing |

| Timber or similar real-property-related collateral | Review local real estate filing requirements carefully |

For a Connecticut creditor, that means a Connecticut filing is correct only when Connecticut is the right jurisdiction under the debtor-location rules or when the collateral type creates a Connecticut filing requirement. If the borrower is a Delaware corporation doing business in Connecticut, filing only with Connecticut can leave a serious gap.

I see this mistake in multi-state transactions more often than creditors expect. Operations, assets, guarantors, and payment addresses pull attention away from the legal question that controls the filing.

Connecticut procedure matters, but only after jurisdiction is right

Once Connecticut is the proper place to file, mechanics matter. The filing process runs through the Connecticut Secretary of the State, and electronic submission is often the cleaner option for commercial creditors because it produces faster confirmation and a better record trail. That does not make e-filing safer by itself. A wrong jurisdiction submitted online is still a wrong jurisdiction.

Paper filing can still have a place in some situations, but it creates more opportunities for delay, intake error, and weak internal tracking. For a lender or trade creditor managing multiple accounts, that administrative friction turns into real risk when a continuation deadline is missed or a rejection notice sits unnoticed.

Method is an operations decision, not just a convenience choice

Online filing usually works better when timing matters, when several related debtors must be filed consistently, or when the business needs a clear acknowledgment for its lien file. Portal-based filing also forces the filer to enter information into defined fields, which can expose formatting problems before submission.

Paper filing gives less control once the document leaves your hands. It may also make later proof issues harder if the file does not include a clean timestamp, receipt trail, and reviewed copy of what was submitted.

A filing method should match the creditor’s internal controls. If there is no docketing system, no saved acknowledgment, and no review protocol after acceptance, the problem is not only legal. It is operational.

The hardest cases are the ones that look ordinary

Jurisdiction analysis needs closer attention in deals involving:

- A debtor that recently converted, merged, or changed its state of organization

- Collateral that includes fixtures or other real-property-related interests

- Multiple affiliated borrowers in different states

- A lender relying on asset location instead of debtor location

- A transaction closing fast enough that no one stops to confirm where each debtor is legally located

Those are the filings that become expensive later.

The practical rule is simple. Identify each debtor’s legal location first. Then check whether the collateral type adds another filing requirement, especially in Connecticut matters involving fixtures or property connected to real estate. That extra review takes less time than litigating over a lien that was recorded, accepted, and still ineffective.

Critical Mistakes That Can Invalidate Your UCC Lien

Most failed UCC filings do not fail because the law is mysterious. They fail because someone assumed accuracy was optional. It isn’t.

The most damaging mistake is usually the simplest one. The debtor’s name is wrong.

Name errors are not clerical defects

According to CSC Global’s UCC filing guide, incorrect debtor name accuracy is the top filing error, with state rejection rates of up to 20% in 2025 filings based on their analysis of 500,000+ records. The same source notes that DIY filings fail at rates of 15-25%, based on 2024 UCC service provider statistics discussed there.

That should change how creditors think about “minor” mistakes. Using a trade name, dropping part of the legal entity name, relying on an assumed name, or shortening a suffix can turn a secured position into a contested one.

What creditors get wrong in practice

The recurring errors tend to look ordinary:

- Using a DBA instead of the legal entity name

- Misspelling the debtor name

- Choosing the wrong jurisdiction

- Describing collateral in a way the security agreement doesn’t support

- Filing against an affiliate instead of the actual borrower

- Ignoring fixture filing issues

The trap is that many of these filings will still feel complete to the person who prepared them. The form is filed. The fee is paid. The acknowledgment arrives. None of that answers the legal question that matters later, which is whether the lien was properly perfected.

Courts and bankruptcy professionals do not grade on effort. They look at whether the filing identifies the correct debtor and whether the secured party followed Article 9 correctly.

Connecticut creditors should watch entity naming closely

For Connecticut businesses, the best practice is straightforward. Pull the exact entity name from the Connecticut Secretary of the State record and use that form of the name consistently in the filing package.

Do not substitute:

- the sales name

- the shortened version used by employees

- the name on signage

- the name from a stale contract if the entity later changed it

That discipline prevents expensive litigation over whether the filing was seriously misleading.

A quick failure checklist

Use this before you submit any UCC-1:

| Red flag | Why it can be fatal |

||---|

| Name came from invoice or website | Public-facing materials often don’t match the legal debtor record |

| Filing office chosen by collateral location alone | The correct jurisdiction often depends on debtor location |

| Collateral copied loosely from deal summary | The filing should align with the actual security documents |

| Multiple affiliated entities in the deal | You may be filing against the wrong debtor |

| Real estate connection ignored | Fixtures can require additional local filing |

The lesson is simple. Most UCC disasters begin as preventable intake errors. The cure is disciplined verification before submission.

Maintaining and Enforcing Your Perfected Lien

A filed UCC-1 is not a permanent asset. It is a time-sensitive public record that has to be maintained. Creditors who understand the front end of the process but ignore the back end often lose rights they worked hard to secure.

The basic life cycle matters just as much as the initial filing.

Continuations, amendments, and terminations

A standard UCC filing remains effective for five years. To keep the lien alive, the secured party must file a UCC-3 continuation statement before lapse. That continuation requirement is part of the ordinary life cycle of a perfected lien, as discussed earlier from the Article 9 filing framework.

UCC-3 filings also handle other changes:

- Continuation when you need to preserve the filing

- Amendment when information in the record must be updated

- Termination when the obligation has been satisfied and the lien should be released

A creditor who doesn’t docket continuation deadlines is taking unnecessary risk. A creditor who files a termination too early can create a different kind of problem.

Monitoring the lien after filing

Good lien practice includes post-filing review. Confirm the filing was accepted, confirm it was indexed under the correct debtor, and keep the acknowledgment in an accessible file. If the debtor changes name, changes structure, or the transaction evolves, review whether an amendment or new filing is needed.

Here, internal discipline matters more than legal theory. Calendar systems, portfolio reviews, and periodic lien checks prevent a lot of avoidable losses.

A perfected lien is not self-maintaining. Someone has to track it, update it, and confirm it still matches the deal on the ground.

What enforcement looks like after default

When a debtor defaults, the UCC filing becomes part of a much larger enforcement picture. It supports your position, but it doesn’t replace the need for a coherent recovery strategy.

That strategy may include:

- Reviewing the loan and security documents

- Confirming that the filing remains effective

- Identifying the collateral and any competing claims

- Assessing whether litigation, repossession, negotiation, or turnover demands make sense

- Coordinating with insolvency counsel if bankruptcy is involved

A filed UCC-1 gives you security. Enforcement is how that security becomes recovery.

For creditors dealing with the next stage of a secured claim, this discussion of foreclosing a lien helps frame the enforcement side.

The practical takeaway

If you’re learning how to file a UCC lien, the core lesson is that no single step stands alone. Accuracy at filing, correct jurisdiction, disciplined maintenance, and a workable enforcement plan all matter. Miss one of them and the value of the others drops fast.

Complex collateral, multiple debtors, Connecticut-specific real property issues, and multi-state transactions are all situations where careful legal review pays for itself. The cost of fixing a filing problem after default is usually far higher than the cost of getting it right at the start.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.