A business owner extends terms to a long-time customer. A lender closes a loan secured by equipment, accounts, or membership interests. On paper, both believe they are protected.

Then the borrower defaults, another creditor appears, or a bankruptcy case starts. That is when many people learn a hard lesson. Having a signed loan document is not the same as having an enforceable, priority position in collateral.

If you want to know how to perfect a security interest, the answer is not just “file a UCC.” A complete answer is more disciplined. You need the right grant language, the right collateral description, the right perfection method, the right filing office, and ongoing maintenance after closing. In Connecticut, as elsewhere, most costly mistakes happen in execution, not theory.

The Critical Difference Between Secured and Unsecured Debt

A Connecticut lender closes a loan and leaves the closing table with a signed note, a security agreement, and confidence. Six months later, the borrower misses payments, a tax lien surfaces, or a bankruptcy petition is filed. The first question is no longer whether money is owed. It is whether the creditor holds a claim that reaches identifiable collateral ahead of competing parties.

That is the line between secured and unsecured debt.

Why security documents alone are not enough

A signed promissory note proves the debt. A signed security agreement can make the lien enforceable between debtor and creditor. Neither step, by itself, gives the creditor the protection that matters in a priority fight.

The practical advantage usually comes from perfection. A perfected security interest can preserve a creditor’s place against other creditors, a bankruptcy trustee, and later lien claimants, depending on the collateral and the facts. An unperfected creditor may still have a breach-of-contract claim, but that is a very different position when the debtor has limited assets and several parties are chasing the same pool of value.

For a basic primer on that legal status, see what a secured creditor is.

What this looks like in practice

Take two creditors extending comparable value to the same business.

The first sells goods on credit and relies on invoice terms and a personal assurance from the owner. The second documents a security interest in inventory and accounts, then completes the required perfection step. If the business fails, those creditors do not enter the workout, collection case, or bankruptcy from equal positions.

The unsecured creditor may sue, obtain a judgment, and try to collect like any other general claimant. The perfected secured creditor may have rights in specific collateral and identifiable proceeds, subject to senior liens and Article 9 priority rules. That changes settlement pressure, available remedies, and often whether there is meaningful recovery at all.

In my experience, business owners and private lenders often miss this point when the deal is between familiar parties. They assume trust reduces legal risk. It does not. Informal deals are often the ones that collapse into expensive disputes because nobody checked whether the collateral was described correctly, whether the debtor owned it, or whether a filing was ever made.

Why this matters for Connecticut businesses

This issue reaches far beyond banks.

Connecticut companies run into it in seller financing, owner buyouts, equipment loans, affiliate transactions, and ordinary trade credit. The risk is not only failing to file at closing. It is also filing once and forgetting about continuation deadlines, or treating collateral as simple when its classification can shift. LLC interests are a common example. Depending on how the interest is structured and whether it is a security under Article 8, the path to perfection may change.

Those are execution problems, and execution problems are what cost creditors priority.

The Foundation Attaching Your Security Interest

A Connecticut lender can leave a closing with a signed note, wired funds, and what looks like a secured deal, then learn during a default that no enforceable lien ever attached. That usually happens because the wrong entity signed, the borrower did not have rights in the collateral, or the security agreement described the assets too loosely to hold up in a dispute.

Before perfection matters, attachment has to exist.

The three requirements for attachment

Under Article 9, attachment generally depends on three basics.

Value must be given

That usually means loan proceeds, credit extended on a sale, or a forbearance agreement. If nothing of legal value changed hands, there is no secured transaction to enforce.The debtor must have rights in the collateral

Many privately documented deals break down when this requirement is not met. A borrower cannot grant a lien on assets owned by an affiliate, held by a spouse, titled in another entity, or subject to restrictions the lender never checked. In Connecticut closely held businesses, I often see this issue with family entities, operating companies using equipment owned by a related LLC, and membership interests that were assumed to be personally owned without reviewing the governing documents.There must be an authenticated security agreement with an adequate collateral description

The debtor must sign or otherwise authenticate a record that creates the security interest, and the description has to identify the collateral in a legally sufficient way. If the grant language is thin, copied from the wrong form, or detached from the assets being pledged, attachment becomes harder to prove when it matters.

Collateral descriptions deserve more attention than they usually get

Creditors often focus on the UCC-1 and treat the security agreement as paperwork. That is backward. The financing statement helps with perfection. The security agreement is what gives the lien its footing against the debtor.

The description should fit the deal and the asset class. Inventory, equipment, accounts, instruments, deposit accounts, and LLC interests do not all present the same drafting issues. A generic form may work for one transaction and fail badly in another.

Blanket language also needs care. Broad collateral grants can be appropriate, but the security agreement still has to identify collateral with enough precision to support attachment. A lender who wants a lien on all business assets should make sure the grant language reaches the assets the debtor owns and uses, rather than relying on shorthand that may invite a later challenge.

Practice tip: If the collateral includes LLC interests, do not stop at the phrase "membership interest." Review the operating agreement and related records to determine how Article 9 classifies that interest. The correct path can shift depending on whether the interest is treated as a general intangible or as an investment property security.

Attachment is separate from the debt instrument

A promissory note proves the debt. It does not, by itself, create an enforceable lien on collateral.

That distinction gets missed in owner-financed transactions and private loans. Parties sign a note, assume they are secured, and only later realize nobody signed a true security agreement. If you want a refresher on that distinction, see this explanation of what a promissory note is.

In litigation, that gap is expensive. A creditor may be able to prove the borrower owes money and still lose the fight over collateral because the lien was never properly granted.

A practical attachment checklist

Before treating the deal as secured, confirm these points:

- Correct debtor: Is the grant coming from the legal owner of the collateral?

- Value given: Was money advanced, credit extended, or forbearance properly documented?

- Rights in collateral: Did someone verify ownership, title, account rights, or governing documents instead of assuming?

- Signed security agreement: Is there a grant of collateral, not just a note, invoice, or term sheet?

- Workable collateral description: Does the language fit the assets involved and hold up if challenged?

Attachment can occur once the required elements are in place, even if they do not happen in a perfect sequence. Good practice is still to close the transaction in a way that leaves no doubt about who granted the lien, what assets are covered, and whether the file will stand up six months later if the borrower defaults.

Choosing Your Method of Perfection

A Connecticut lender can close what looks like a well-documented secured loan and still lose the collateral fight by choosing the wrong perfection method.

That problem shows up most often when parties assume filing is always enough. It usually is for ordinary business assets. It is not for every asset class, and the mistakes tend to surface only after default, a competing lien search, or a bankruptcy filing.

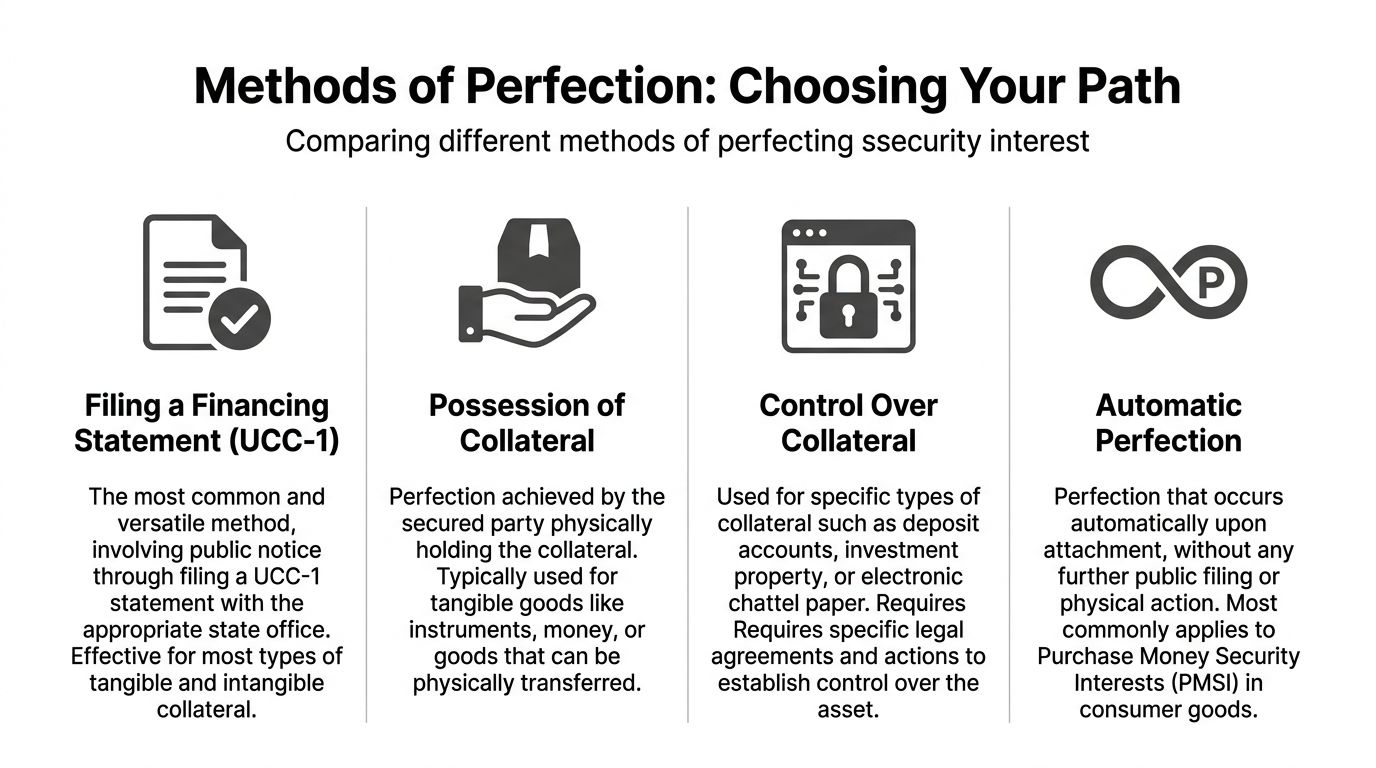

Filing is the default, not the universal answer

For inventory, equipment, accounts, and many categories of general intangibles, a UCC-1 financing statement is usually the practical first choice. It lets the borrower keep using the assets while the secured party puts the world on notice of its claim.

That matters in real operating businesses. A manufacturer cannot hand over its equipment. A distributor cannot stop selling inventory. A company that lives on receivables cannot function if the lender insists on controlling every customer payment from day one.

Filing fits those deals because it is efficient and scalable.

Some collateral needs possession, control, or title notation

Method follows collateral type. The right question is not what the parties call the asset in conversation. The right question is how Article 9 classifies it and whether another statute controls perfection.

Deposit accounts are a common example. A filed UCC-1 may help with notice in a broader loan file, but control is generally what matters for perfection and priority. The same issue comes up with investment property, letter-of-credit rights, and certain uncertificated interests.

Possession can also matter. If the collateral is an instrument, negotiable document, money, or tangible chattel paper, physical possession may be available and may put the secured party in a better position than filing alone.

Title law creates a separate trap. If the collateral is covered by a certificate of title statute, such as many motor vehicles, the lien often must be noted through the title system rather than perfected through an ordinary UCC filing.

Comparing methods of perfection

| Method | Applicable Collateral | How It Works | Best For |

|---|---|---|---|

| Filing a financing statement | Most common business collateral, including many tangible and intangible assets | Public notice filing in the appropriate filing office | General commercial lending and trade credit |

| Possession | Collateral that can be physically held, such as instruments, money, goods, negotiable documents, and tangible chattel paper | Secured party or qualified agent physically possesses the collateral | Assets where custody is realistic and legally effective |

| Control | Deposit accounts, investment property, letter-of-credit rights, and certain LLC interests or uncertificated interests depending on structure | Secured party obtains legal control through account arrangements, agreements, or issuer recognition | Financial assets and collateral where control gives stronger priority |

| Automatic perfection | Limited specialized collateral types, including some purchase-money situations and proceeds | Perfection occurs upon attachment without separate filing | Narrow situations where Article 9 provides it |

| Certificate-of-title notation | Titled assets when governed by title law | Lien is noted through the relevant title system rather than ordinary UCC filing | Vehicles and other title-governed collateral |

What usually works in practice

Filing for operating assets

For most Connecticut commercial loans, filing remains the workhorse method. It covers the collateral package lenders see every day and does not interfere with operations.

The risk is overconfidence. A filing strategy still fails if the debtor name is wrong, the filing is made in the wrong state, or the collateral description in the loan documents does not match the assets the lender expects to reach.

Control where priority is the objective

If a lender is underwriting to cash in bank accounts, securities, or similar financial assets, control deserves attention at the start of the deal, not after documents are signed. Priority disputes are often decided there.

This is especially important for non-bank lenders in Connecticut. The legal path may be clear, but execution usually depends on account control agreements, cooperation from the depositary bank or intermediary, and realistic timing. If those pieces are not lined up before closing, the lender may end up with paper rights and weak practical protection.

Possession where the asset can be held

Possession works best for discrete collateral that can be segregated and delivered. It is often a poor fit for assets the borrower needs to use every day.

That trade-off is easy to miss. A method can be legally available and still be commercially inefficient.

Connecticut issues that generic guides often miss

Collateral classification can shift over the life of the loan. LLC interests are a good example. The governing documents and the way the interest is structured can affect whether the collateral is treated more like a general intangible or investment property, which can change whether filing is enough or control is the better approach.

Lapsed filings create another avoidable problem. A lender may choose the right method at closing and still lose its position later by failing to continue perfection on time or by missing a change in debtor name, location, or structure that requires follow-up action.

Before choosing the method, ask a few practical questions:

- What asset will repay the debt if the borrower defaults?

- Is filing sufficient for that asset class, or does priority depend on control or possession?

- Will the borrower need uninterrupted use of the collateral?

- Could the collateral’s legal classification change during the term of the loan?

- Is there an existing senior lender whose documents or collateral package limit what this lender can really obtain?

The right perfection method is the one that holds up after closing, during distress, and in a priority fight. That is a narrower question than many loan files assume.

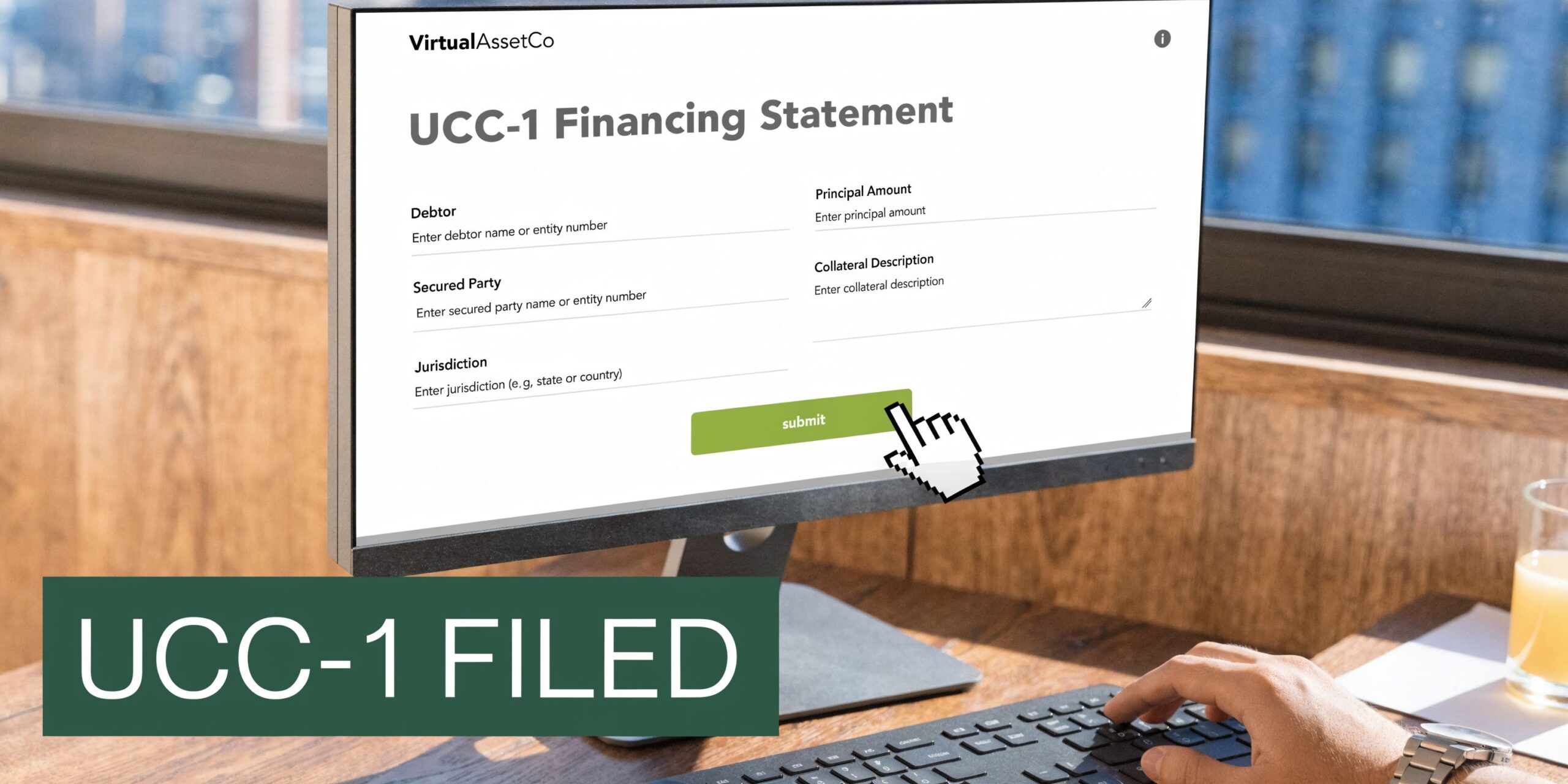

The UCC-1 Filing Process in Connecticut

A lender closes on Friday, funds the loan, and files a UCC-1 on Monday. Six months later, the borrower defaults. Then someone discovers the filing used the borrower’s trade name instead of its exact legal name, or covered the wrong debtor in a multi-entity structure. That is how a secured deal starts to look unsecured.

For many Connecticut transactions, the UCC-1 financing statement is the filing that puts the market on notice. The form is short. The risk sits in the details.

Start with the debtor’s correct legal identity

The debtor name has to match the legal name of the person or entity that owns the collateral and grants the security interest. For a registered organization, that usually means checking the formation records, not relying on invoices, signatures, email footers, or a “doing business as” name.

This point matters even more in Connecticut middle-market deals involving affiliated entities. Business owners often refer to a group of companies as if it were one borrower. Article 9 does not. If the operating company owns the equipment but the parent signs the wrong documents, the filing problem is not clerical. It goes to whether the secured party perfected against the right debtor at all.

File in the correct jurisdiction

For most Article 9 collateral, the filing location follows the debtor’s location, not the physical location of the collateral. That catches lenders who focus on where the inventory, equipment, or records sit rather than where the debtor is legally located.

For a Connecticut entity, that often means filing through the Connecticut UCC system. But "often" is doing work here. Some collateral falls outside ordinary UCC-1 practice or raises parallel filing questions. Fixtures, titled vehicles, and certain collateral tied to real estate need separate attention. A lender that expects to enforce its rights after default should line up the filing strategy with the remedy strategy, including whether it may later need to foreclose a lien on collateral tied to the dispute.

Describe the collateral with enough precision to hold up

A financing statement is a notice filing, but that does not excuse lazy drafting.

The collateral description should be broad enough to match the deal and specific enough to avoid an avoidable fight. Overly narrow language leaves value uncovered. Vague language invites a challenge. Boilerplate copied from an old file often misses assets that matter in the current loan, especially deposit accounts, payment rights, proceeds, or LLC interests that may need more than a standard filing approach depending on how they are structured.

In practice, I want the UCC-1 description to track the security agreement closely enough that a third party can see what is being claimed without guessing.

Build a filing routine that catches Connecticut deal-file mistakes

The filing step works best when someone confirms a short list before submission:

- The exact debtor name from current organizational records

- The debtor entity that owns the collateral

- The secured party name and capacity shown in the loan documents

- The collateral categories covered by the signed security agreement

- Whether any asset requires possession, control, or a separate recording method

- Who will review the filed record after acceptance

That last item gets skipped too often.

A filing acknowledgment only confirms that something was accepted for filing. It does not confirm that the indexing is useful, the debtor was named correctly, or the collateral description matches the closing package. Review the filed record while the deal is still fresh and the documents are still in front of the team.

What works in practice

Good filings usually come from disciplined intake and document matching. Counsel or the lender checks the charter documents, confirms the borrower structure, compares the UCC-1 against the signed security agreement, and resolves odd collateral questions before submission.

Bad filings usually come from speed, assumptions, and recycled forms. That is where Connecticut lenders get surprised by name changes, merged entities, stale organizational documents, and collateral that looked ordinary at closing but is harder to categorize once enforcement starts.

Maintaining Perfection and Winning Priority Disputes

Many creditors treat perfection as a closing task.

That is a mistake. Perfection has a life cycle, and priority can be lost after a deal is fully documented if no one maintains the public record.

The five-year clock matters

Under UCC Article 9, a financing statement lapses exactly five years from the date of filing, and a creditor must file a UCC-3 continuation statement within the six-month window before the lapse date to keep perfection in place, as explained in this discussion of protecting a security interest and continuation timing.

That timing is strict.

A continuation filed too late does not rescue the filing. A missed continuation can reduce a once-protected creditor to a much weaker position, especially if another creditor filed during the gap or if bankruptcy intervenes.

Priority usually follows filing order

For many disputes, the rule is simple enough to remember and serious enough to respect. First to file holds priority.

That means a creditor who files early and maintains perfection usually preserves a stronger claim than a later filer. It also means administrative sloppiness can undo a carefully negotiated credit position. If the senior creditor lets its filing lapse, another creditor may move ahead.

This is one reason workouts should begin with lien review, not just payment history review.

A practical example of how creditors lose ground

Consider a longer-term commercial loan.

The creditor closes properly and files a UCC-1. Years pass. The relationship seems stable. Staff changes. The continuation deadline is missed. Another lender later extends credit and files.

At that point, the original lender may still have contractual rights against the borrower, but its perfected status may be gone. In an insolvency case, that shift can change recovery, negotiating power, and settlement pressure dramatically.

Maintenance is an enforcement tool

Perfection is not just about future litigation. It affects day-to-day bargaining power.

A lender with a current, defensible filing can demand different concessions in a restructuring. A creditor with a lapsed filing may find that negotiations now resemble ordinary collection work rather than collateral enforcement. If enforcement becomes necessary, the analysis may overlap with remedies discussed in foreclosing a lien.

Key takeaway: Filing is step one. Calendar control is step two. If no one owns the continuation process, the original filing can become a false sense of security.

How to manage the life cycle

A reliable approach usually includes:

- Central tracking: One person or team should own continuation dates.

- Portfolio review: Check secured files periodically, especially before renewals, restructurings, or assignments.

- Change monitoring: Watch for debtor name changes, mergers, conversions, and collateral shifts.

- Action before deadlines: Do not wait for the edge of the continuation window.

The verified source frames this well in practical terms. A loan lasting beyond the original filing period requires active monitoring and timely continuation to preserve the creditor’s priority rights.

Avoiding Common Pitfalls and Complex Collateral

Many problems in secured transactions are not caused by unusual law. They are caused by ordinary carelessness applied to unforgiving rules.

A filing can be accepted and still fail to do what the creditor thinks it does. A security agreement can be signed and still leave gaps. A lender can perfect correctly on day one and lose position later because the collateral changed shape.

The errors that show up most often

The recurring mistakes are familiar.

- Wrong debtor name: Using a trade name, shorthand name, or the wrong affiliate.

- Weak collateral drafting: Descriptions that do not match the transaction or fail to cover what the creditor relies on.

- No follow-up after organizational changes: A debtor changes its name, structure, or governing documents, and the secured party does nothing.

- Assuming filing solves every problem: It does not.

These are execution failures, not exotic disputes. They often begin with rushed closings and end with expensive litigation.

LLC membership interests require extra attention

One of the more overlooked risk areas involves LLC membership interests.

A lender may initially treat the interest as collateral perfected by standard filing. But the LLC can later amend its organizational documents to opt in to UCC Article 8, which can cause the interest to be treated as a security. According to this practitioner discussion of four paths to perfection, that change can invalidate a prior perfection based on ordinary UCC-1 filing if the secured party does not monitor the governance documents and re-perfect through control when needed.

That risk is easy to miss because many generic guides stop at the initial filing analysis.

Why this matters in Connecticut deals

Connecticut businesses often use LLCs for operating companies, holdings, and joint ventures. That makes membership interests common collateral in closely held business transactions.

The practical problem is not theoretical. A lender can document the original deal carefully and still lose position if nobody monitors amendments to the operating agreement or related organizational records. For that kind of collateral, legal diligence should continue after closing.

Practice tip: If LLC interests matter to the credit decision, build governance monitoring into the deal. A covenant requiring notice of amendments is far better than discovering the issue after default.

Challenge the assumption that “one filing covers it”

That assumption causes trouble in complex collateral files.

Collateral can move between entities. Business structures can change. LLC interests can shift classification. Deposit accounts may require control rather than reliance on a general filing strategy. The right answer is often a combination of good drafting, pre-closing diligence, and post-closing monitoring.

A strong secured transaction file is built for change, not just for closing day.

Frequently Asked Questions and Next Steps

Business owners and lenders often ask the same practical questions once they understand the basics.

What if the debtor moves or reorganizes

Do not assume the original filing remains sufficient forever.

A move, merger, conversion, or name change can affect where perfection should be maintained and whether additional action is required. Those events should trigger legal review, not just an update in the borrower’s contact information.

Does every secured transaction require a UCC-1

No.

Filing is the most common method, but not the only one. Some collateral is better perfected by possession or control. Some transactions involve other perfection regimes. The right method depends on the collateral type and the priority position the creditor needs.

Can a creditor rely on broad forms from a prior deal

That is risky.

Forms are useful starting points, but secured transactions are detail-sensitive. The debtor identity, collateral class, ownership chain, and intended remedy should drive the drafting. Reused forms often carry old assumptions into new files.

What should a lender or trade creditor do before extending credit

At a minimum:

- Confirm the correct debtor

- Identify the collateral clearly

- Use a signed security agreement

- Choose the right perfection method

- Track post-closing maintenance

That sequence is what turns a promise to pay into a more durable credit position.

Where can creditors learn more about enforcement rights

If your concern is not just perfection but what happens after default, review creditors’ rights lawyers for a broader look at the remedies side of the equation.

The practical lesson is straightforward. Learning how to perfect a security interest is not about memorizing one filing form. It is about doing the deal correctly at the start and managing it correctly afterward. Attachment, perfection, and maintenance each matter. If any one of them is mishandled, the creditor may discover the problem at the worst possible time.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.