A common version of this question starts in the middle of a deal.

A Connecticut business owner is buying equipment, expanding a line of credit, or using accounts receivable to support working capital. The lender says approval is ready, but one condition remains. It will file a UCC-1. For many clients, that is the first time they hear the term.

That filing is not clerical noise. It affects who has rights in the collateral, whether another lender can step ahead in line, and whether the business can use the same assets for future financing. If you are borrowing, lending, or reviewing a closing checklist, understanding what is a UCC financing statement is part of protecting the transaction, not just documenting it.

Securing Your Business Future An Introduction to the UCC-1

A growing company often reaches the same moment. Sales are up. A new contract is pending. Production needs equipment, inventory financing, or a larger revolving facility. The lender agrees, but it wants a lien on business assets.

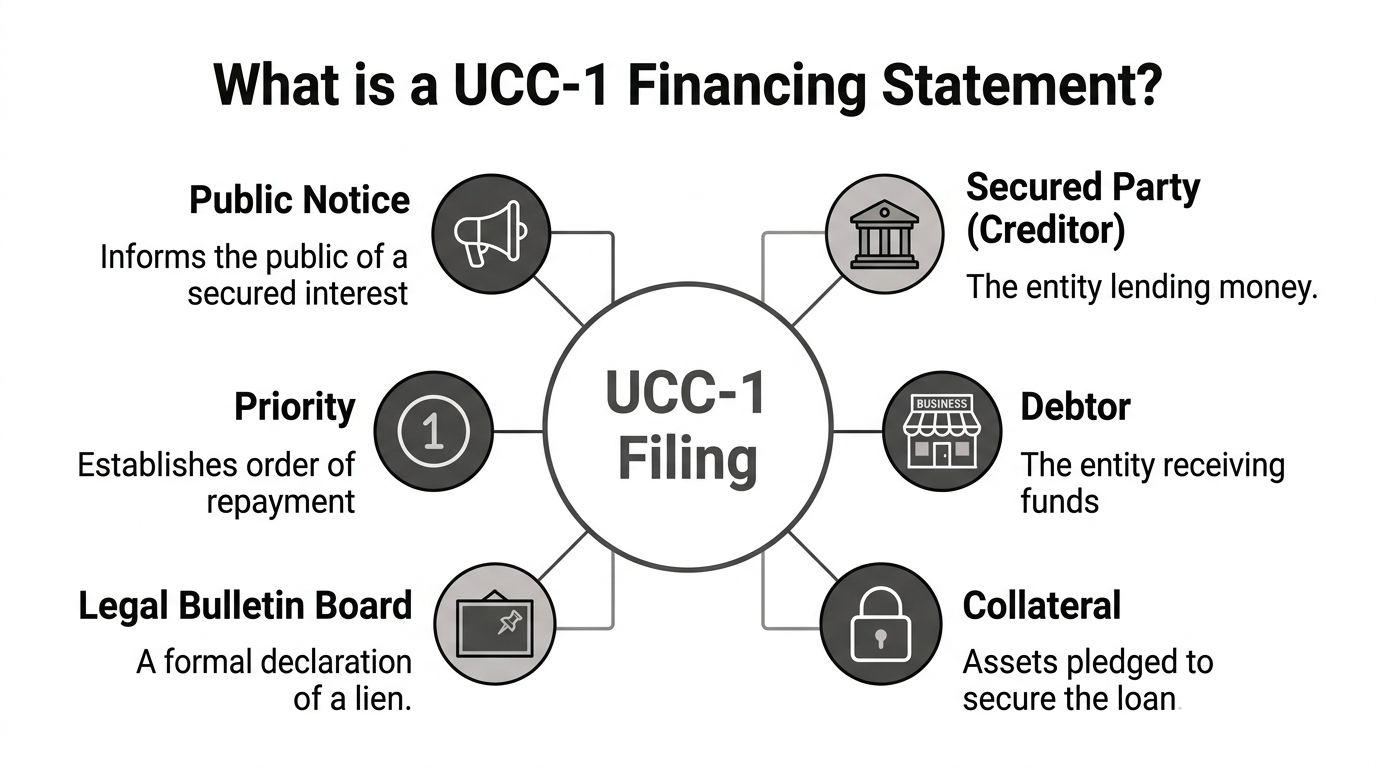

That is where the UCC-1 financing statement enters the picture.

In practical terms, the filing tells the public that a creditor claims an interest in identified collateral owned by the debtor. In business lending, that collateral may include equipment, inventory, accounts receivable, or other personal property tied to the transaction. The filing itself does not transfer ownership of the assets to the lender. It puts everyone else on notice that the lender has a claim.

For a borrower, this matters because the filing can affect more than the current loan. It can shape future borrowing options, limit how certain assets are reused as collateral, and create cleanup work at payoff if the filing is not properly terminated. For a lender, it is one of the central tools for preserving rights if the borrower defaults.

Why business owners run into UCC filings so often

Many commercial loans are asset-backed. A bank may lend against machinery. A private lender may take a lien on receivables. A vendor may finance equipment and expect repayment over time. In each of those settings, the creditor wants a documented and enforceable public claim.

Without that filing, the lender may have a contract with the borrower, but a later creditor with a proper filing may gain a stronger position against the same assets. That is why experienced lenders do not treat the UCC process casually.

What business clients should understand early

When clients ask what is a ucc financing statement, the useful answer is not just “a form.” It is a financing tool with consequences.

A borrower should know:

- It affects collateral availability: Assets tied up in an active filing may not be available for a new lender without a release.

- It affects deal timing: Closing can stall when names, collateral language, or filing locations are wrong.

- It affects cleanup after payoff: If the record remains active longer than it should, later financing and asset sales can become harder than they need to be.

A UCC filing is often routine. Its consequences are not. Routine documents cause serious problems when parties assume the details do not matter.

What Is a UCC Financing Statement Legally Speaking

A Connecticut company closes on a line of credit, orders inventory, and assumes the paperwork is done. Two months later, a second lender runs a lien search, sees an active UCC filing against the same assets, and the new financing stalls. That is the practical legal function of a UCC financing statement. It puts the market on notice that a creditor claims a security interest in the debtor’s collateral.

Legally, a UCC financing statement is a public filing made under Article 9 of the Uniform Commercial Code. It does not transfer ownership of the collateral. It does not contain every business term of the deal. It serves a narrower and very important role. It gives notice to other lenders, buyers, and parties reviewing the record that certain assets may already secure an obligation.

The filing’s legal purpose

In secured lending, lawyers usually separate three concepts. The security interest must attach to the collateral. The creditor must perfect that interest by the method the law requires. If multiple creditors claim the same assets, priority rules determine who stands first in line. A UCC-1 filing often handles the perfection and notice side of that framework for personal property collateral.

That point matters in real deals. A lender with signed loan documents but no effective filing may still have rights against the borrower, yet lose ground against another creditor who filed correctly first. For a Connecticut borrower, that can affect whether existing assets remain available for working capital, equipment financing, or refinancing. For a lender, it is a risk-control document, not clerical surplus.

If you want a related primer on creditor status, this discussion of a secured creditor is a useful companion.

Why the public notice system matters in practice

The filing system exists to reduce hidden lien risk. Commercial credit would be far less predictable if lenders had no reliable way to check whether receivables, inventory, equipment, or general business assets were already pledged.

That issue comes up often with growing Connecticut businesses. A manufacturer in Hartford may seek asset-based financing. A contractor in New Haven may need equipment funding to support a public project. A healthcare practice may be trying to qualify for additional credit while participating in a federal reimbursement or grant program with its own documentation standards. In each situation, an existing UCC filing can change the underwriting conversation immediately.

Public notice also affects compliance. Federal funding programs and federally backed lending often require clear disclosure of existing liens, accurate entity information, and documentation that matches the borrower’s legal structure. A sloppy filing record can create extra diligence, delay disbursement, or raise questions that should have been resolved before closing.

What the filing does not do

Clients often overestimate what the financing statement accomplishes by itself. The UCC-1 serves as the notice piece of the secured transaction. It works only when the underlying documents were prepared and signed correctly.

A financing statement does not replace the loan agreement, which sets the payment terms and default rights. It does not replace the security agreement, which gives the creditor the security interest in the first place. It also does not replace diligence on existing liens, entity status, authority, or collateral-specific filing rules.

For businesses preparing documents internally, good forms can help organize the transaction, but forms are not a substitute for legal judgment. If you are reviewing base language before counsel finalizes the deal, structured Contract Templates can be useful as a starting point for commercial paperwork.

In practice, the legal meaning of a UCC financing statement is simple. It is a public notice filing with serious business consequences. Used correctly, it supports credit access and protects lien rights. Used carelessly, it can interfere with borrowing, refinancing, asset sales, and compliance review at exactly the wrong time.

The Anatomy of a UCC-1 Filing Getting the Details Right

A Connecticut lender closes a deal on Friday, funds on Monday, and assumes the collateral package is protected because the UCC-1 was accepted for filing. Months later, a refinance, workout, or asset sale puts that record under real scrutiny. That is when small drafting errors stop looking small.

A UCC-1 is a short form with outsized consequences. Filing offices accept records based on format and basic submission rules. They do not verify that the debtor name is legally sufficient, that the collateral description fits the deal, or that the public record will hold up against another creditor, a trustee, or a buyer doing diligence.

The fields that carry the risk

Three parts of the form usually decide whether the filing does its job:

| Element | Why it matters | Common problem |

|---|---|---|

| Debtor name | Determines whether the record is discoverable and legally effective | Trade name, shorthand, or an outdated entity name |

| Secured party information | Identifies the party of record and affects later amendments, assignments, and terminations | Incorrect legal name, old address, affiliate confusion |

| Collateral description | Defines the property covered by the notice filing | Boilerplate that is either too generic or mismatched to the transaction |

The debtor name causes the most avoidable failures.

Debtor name means the exact legal name on the right public record

For an LLC or corporation, the safest practice is to pull the entity record and copy the name exactly as it appears with the Secretary of State. In my practice, I see businesses lose time and negotiating position over missing commas, old suffixes, merged entity names, and informal trade styles that everyone in the deal used except the filing system.

For Connecticut businesses, this point affects more than litigation risk. Banks, private lenders, and federal funding reviewers often run lien and entity searches early in underwriting. If the filing record does not line up with the borrower’s legal identity, the borrower may face extra diligence requests, delayed draws, or questions about internal controls that should have been avoided before closing.

A filing against “Hartford Industrial Solutions” may not protect a lender if the legal entity is “Hartford Industrial Solutions, LLC.” That is not a clerical irritation. It is a priority problem waiting for the wrong moment.

The secured party field matters for administration, not just formality

The secured party’s information should be current and consistent with the closing documents. That becomes important when loans are assigned, serviced by another entity, or held through an affiliate structure.

A clean public record makes later amendments easier. A messy one creates friction during portfolio sales, payoff negotiations, and terminations. It also creates avoidable confusion if enforcement becomes necessary, including questions that can surface in a dispute over remedies or the process of foreclosing a lien against collateral.

Collateral description requires judgment

The collateral description must reasonably identify what the creditor claims. That standard sounds simple until parties try to apply it to inventory, equipment, deposit accounts, contract rights, intellectual property, or a mixed collateral package tied to a growth facility.

Breadth is not always better. Precision is not always safer. The right description depends on the transaction documents, the asset class, and the lender’s risk tolerance.

For example, an equipment lender often benefits from language tied closely to the financed assets, serial-numbered schedules, proceeds, and related records. A working capital lender may need category-based language broad enough to cover shifting collateral pools. Copying language from a different deal is how gaps get created.

Filing office acceptance proves very little

Clients are often surprised by this. Acceptance confirms that the office took the record. It does not confirm legal sufficiency.

That distinction matters in contested files. Another lender, a bankruptcy trustee, an investor, or an agency reviewer will not care that the filing was accepted if the debtor name was wrong or the collateral description does not match the deal. In secured lending, clerical success and legal success are not the same thing.

A practical filing review before submission

Before a UCC-1 goes out the door, review the file with the same discipline used for the note and security agreement:

- Confirm the debtor’s exact legal name against current formation or registration records

- Check entity status and recent changes such as mergers, conversions, or amendments

- Match the debtor and grantor roles to the signed transaction documents

- Draft collateral language for this deal rather than reusing old boilerplate

- Review secured party details carefully if affiliates, servicers, or assignees are involved

- Ask how the record will read to a third party doing diligence under time pressure

That last question is practical and often overlooked. If a future lender, buyer, or agency examiner searches the record, the filing should make sense without explanation from the original deal team.

The UCC-1 is not difficult because it is long. It is difficult because a short filing has to be right in exactly the places that affect credit access, lien priority, refinance options, and compliance review. For Connecticut businesses using secured debt to grow, those details are business terms, not paperwork.

The Lifecycle of a UCC Filing From Creation to Termination

A UCC filing has a lifespan. Treating it as a one-time closing task is a common mistake.

From the first filing through continuation or termination, someone needs to monitor the record. That is true for lenders protecting collateral and for borrowers trying to keep their asset base clean for future transactions.

Filing is the beginning, not the end

The UCC-1 is usually filed with the Secretary of State in the appropriate jurisdiction for the debtor. The filing gives public notice of the secured party’s claim, but good practice does not stop at submission.

Parties should confirm acceptance, confirm indexing, and keep the acknowledgment with the deal file. If the filing information does not match the closing documents, the right time to catch that problem is immediately, not during a default workout.

The five-year clock matters

A UCC-1 financing statement typically lasts for five years from the filing date (InCorp). That timeline is one of the most important practical facts in secured lending.

If the filing is not continued on time, the public notice can lapse. A lender that assumes the lien “stays in place because the loan is still unpaid” can discover too late that the record no longer protects priority the way it once did.

The basic lifecycle in practice

A standard file usually moves through these stages:

- Initial filing

The lender files the UCC-1 after the security interest is granted. - Monitoring period

During the life of the loan, parties track the filing and any changes affecting debtor information or collateral. - Continuation or amendment if needed

If the loan remains outstanding and the filing is nearing expiration, a UCC-3 continuation may be necessary. Other UCC-3 filings can amend or update the record. - Termination after payoff

Once the secured obligation is fully satisfied, the filing should be cleaned up through a termination when appropriate.

If a dispute later turns toward enforcement, lien rights become part of the broader remedies picture. This overview of foreclosing a lien gives useful context on what happens after default.

Why continuation discipline matters

The five-year period creates a calendar problem, not just a legal one. Many portfolio issues arise because someone assumed another person was tracking deadlines.

For lenders, missed continuation windows can weaken their position. For borrowers, old filings that should have been addressed can continue to interfere with refinancing, asset sales, and diligence reviews.

A disciplined process usually includes:

- Tickler systems: Calendar the lapse date early.

- Portfolio review: Check active filings against live obligations.

- Name-change monitoring: If an entity changes its legal name, counsel should assess whether additional action is needed.

- Payoff closeout: Do not let terminated debt linger in the public record longer than necessary.

Termination is not housekeeping

Businesses often discover old UCC filings when a new lender runs a search and asks why prior liens are still active. At that point, what should have been a simple payoff cleanup becomes a closing condition.

Borrowers should confirm that payoff packages address lien release and UCC termination. Lenders should avoid filing termination documents prematurely, but once the debt is satisfied and the record should be released, delay creates avoidable friction.

A paid-off loan should not keep blocking future financing because no one closed the loop on the UCC record.

The business lesson

The lifecycle of a UCC filing is an operational issue as much as a legal one. The legal rule is stable. The execution is where parties slip.

Strong file management means the original filing is accurate, the deadline is tracked, needed changes are handled correctly, and the record is cleared when the deal is done. Businesses that borrow regularly should build this into their standard finance administration, not treat it as occasional cleanup.

Understanding Perfection and Priority Rules in Secured Lending

Many clients ask what the UCC-1 buys the lender. The short answer is position.

A secured transaction is not only about whether the lender has a claim. It is also about where that claim stands compared with everyone else. In a distressed situation, order matters.

Perfection turns a private deal into an externally effective claim

The borrower and lender may sign a security agreement, but other creditors are not bound to treat that private contract as senior just because it exists. Perfection is the step that strengthens the claim against third parties.

In most ordinary business lending transactions, filing the UCC-1 is the public act that gives the lender that protected posture. Without it, a creditor may find itself arguing from a weaker position than expected.

If you want a more focused discussion of the mechanics, this article on how to perfect a security interest is worth reviewing.

Priority is the line at the window

Priority decides who gets paid first from collateral when claims compete. The everyday analogy is a line at a ticket counter. The person who got in line first is usually served first.

That is why experienced lenders search before filing and file promptly after closing. Delay creates exposure. If another creditor beats you to the public record on the same collateral, the priority analysis can change fast.

Why active filings affect future credit

This area matters to borrowers even when they are not in distress. Active UCC filings can shape how future lenders view the business.

Crestmont Capital notes that multiple active UCC filings can signal excessive debt or financial risk, which may lead lenders to impose higher rates, tighter conditions, or deny financing altogether (Crestmont Capital).

That does not mean every filing is bad. Many healthy companies operate with secured debt. The issue is what the filing record communicates to the next lender reviewing your balance sheet, collateral package, and existing encumbrances.

How this plays out in real business decisions

A borrower may want to:

- refinance an equipment loan,

- open a new line secured by receivables,

- sell part of its business, or

- pledge the same asset base to support expansion.

If old liens remain active, or if collateral is already heavily encumbered, the next lender may narrow the deal, demand additional collateral, or walk away.

Businesses using receivables finance see this often. If your company is evaluating that structure, a practical explanation of a factoring contract agreement helps show how collateral and payment rights can overlap in commercial finance.

A borrower’s view and a lender’s view differ

Here is the same UCC record from two perspectives:

| Party | Main concern | Typical reaction |

|---|---|---|

| Borrower | Access to future capital | Wants old liens terminated quickly |

| Existing lender | Preservation of collateral position | Wants filing accuracy and continuity |

| New lender | Hidden risk and lien competition | Searches records and underwrites cautiously |

The legal concepts of perfection and priority are not abstract. They drive underwriting decisions, closing conditions, intercreditor disputes, and influence negotiations in workout scenarios.

If your business expects to borrow again, your UCC record is part of your financing profile. Treat it the way you treat your contracts, tax filings, and corporate records.

Common UCC Filing Mistakes That Can Invalidate Your Claim

The most expensive UCC problems usually do not begin with fraud or a complex legal theory. They begin with ordinary sloppiness.

A team copies the wrong debtor name from an invoice. Someone files in the wrong state. A collateral description is written so vaguely that it does not do the job. Later, everyone is surprised that the record does not protect the deal.

Mistake one is usually name error

Using a trade name instead of the legal entity name is still one of the most damaging errors. Businesses market themselves under brand names all the time. Lenders and vendors start using those names in emails, proposals, and invoices.

The UCC record is not the place for that shortcut.

For registered entities, the filing needs to line up with the official legal name, not the name people casually use in commerce. A filing under the wrong name may sit in the record without giving effective notice to other creditors.

Vague collateral language creates a different problem

The collateral field is not where parties should get lazy. Litera notes that UCC-1 filings must reasonably identify the collateral, and generic descriptions such as “all of the debtor’s personal property” are generally insufficient to perfect a lien. The same source notes that filing fees typically range from $10 to $25 per filing, with additional per-debtor fees in some jurisdictions (Litera).

That fee is modest. The cost of a defective filing is not.

Other recurring errors

These issues appear often in practice:

- Wrong jurisdiction: The lender files where the business operates instead of where the entity is organized.

- Expired filing: No one tracks the continuation deadline and the record lapses.

- Unterminated lien: The debt is paid, but the filing remains and clouds later transactions.

- Bad internal assumptions: A team assumes the filing service or loan processor verified legal sufficiency when they only handled submission.

Why meticulousness is worth the effort

The argument for care is simple. UCC work looks administrative, but the consequences are strategic.

A defective filing can:

- weaken a lender’s priority,

- invite disputes with later creditors,

- interfere with refinancing,

- create friction in a sale transaction, and

- force emergency cleanup under deadline pressure.

The practical fix

The best prevention is not complicated. It is disciplined.

- Verify names against official records

- Draft collateral language to fit the actual deal

- Confirm filing location before submission

- Track deadlines in a system, not in memory

- Clear paid-off liens promptly

A small error in a short form can have effects that last much longer than the original transaction.

Special Considerations for Connecticut Filings and Federal Funding

Connecticut businesses often assume UCC practice is entirely uniform because the Uniform Commercial Code applies across states. The framework is consistent, but filing execution still depends on local systems, entity records, and transaction details.

For Connecticut companies, that means paying attention to filing mechanics through the Secretary of the State’s system and making sure the legal entity information used in the filing matches the state record exactly. A good filing can still become vulnerable if the debtor information is pulled from contracts, invoices, or branding material instead of formation documents.

Connecticut practice requires disciplined record matching

In ordinary commercial lending, the practical issues are familiar. Confirm the exact entity name. Match the transaction documents. Check whether the filing belongs at the state level, and whether any related real-property issue requires separate treatment.

For businesses already dealing with construction, equipment, or real-property-adjacent claims, this broader primer on how to file a mechanics lien is useful because it highlights a related lesson. Different lien systems serve different functions, and parties should not assume one filing method covers another legal problem.

Federal funding changes the analysis

One area businesses routinely overlook involves federally funded equipment purchases. The usual private-lender mindset does not always fit these transactions.

The Department of Energy guidance identifies a specific compliance issue that many standard UCC discussions miss. For certain federal assistance arrangements, equipment purchases of $5,000 or more per unit under awards exceeding $1 million require UCC-1 filings that include serial numbers and disclose the government’s “undivided reversionary interest” (DOE guidance).

That requirement changes how counsel and finance teams should think about the filing.

Why federal interest creates practical friction

A business may view the equipment as another asset on the balance sheet. A private lender may expect to take a standard security interest. Federal program rules may say the government retains a reversionary interest that must appear in the UCC record.

That can affect:

- Asset sales: The business may not have the flexibility it assumed.

- Refinancing: A new lender may hesitate when federal restrictions appear in the lien profile.

- Collateral planning: The equipment may not be freely available for later secured borrowing.

- Reimbursement timing: If the required filing language is missing, funding administration can become more difficult.

The right way to approach these deals

A transaction involving federal money should not be documented as if it were a standard private equipment loan. Counsel should review the award terms, the filing requirements, the collateral description, and the interaction between the government’s stated interest and any private secured party.

Federal funding can turn a familiar UCC filing into a compliance-sensitive document. Businesses should not assume their ordinary lending forms solve that problem.

For Connecticut companies in energy, housing, or other grant-supported sectors, this issue deserves attention early. It is much easier to structure around competing restrictions at the front end than to repair the record after a lender, auditor, or agency flags the conflict.

Navigating UCC Filings with Confidence

A UCC financing statement is one of the most important routine documents in commercial finance. It affects collateral rights, lender priority, future borrowing capacity, and post-payoff cleanup. The form is short. The consequences are not.

Businesses should not treat a UCC filing as background paperwork. Lenders should not treat filing accuracy as a clerical task. The details decide whether the filing performs when pressure arrives. That means the legal name must be exact, the collateral description must be carefully drafted, the filing lifecycle must be monitored, and any unusual funding source must be reviewed for added compliance obligations.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you need guidance on secured transactions, lien rights, commercial lending documents, or a broader business law issue, contact Kons Law.