A business owner calls after a closing falls apart for reasons that make no sense. Wiring instructions changed at the last minute. A title search shows a lien no one can explain. A deed appears in the land records that the owner never signed. By the time that call happens, the panic is already real, because property fraud rarely looks dramatic at first. It looks administrative. It looks like paperwork. Then it starts tying up bank relationships, investor confidence, refinancing plans, tenant issues, and sale timelines.

When fraud touches real estate, the damage spreads fast. It can cloud title, freeze deal proceeds, trigger defaults, and force you into litigation on multiple fronts at once. For Connecticut business owners and investors, the right response isn't just to “report it” and hope someone fixes it. You need a strategy that protects the asset, preserves evidence, and puts you in position to recover money or unwind the deal.

The Growing Threat of Real Estate Fraud

A common fact pattern starts with something small. You pull a title update before refinancing or selling, and a document appears that shouldn’t exist. It may be a mortgage payoff issue, a suspicious assignment, a lien filed by someone you’ve never dealt with, or a deed transfer you never authorized. In commercial settings, the first sign is often indirect. A lender refuses to proceed, a buyer’s counsel flags a chain-of-title problem, or a title company raises an exception that wasn’t there before.

That’s why victims often second-guess themselves at first. They assume there must be a clerical issue at the town clerk’s office or a misunderstanding between counterparties. Sometimes that’s true. Fraud cases are different because the paperwork was created or used to deceive someone into transferring money, title, or an advantage.

This image captures the moment many victims recognize something is badly wrong.

The larger trend supports that instinct to take the problem seriously. In 2021, the FBI's Internet Crime Report documented 11,578 complaints of real estate crimes in the United States, with victims suffering total losses exceeding $350 million, a 64% increase from the previous year, according to Andre Clark Law’s discussion of the FBI report. Those figures address internet-enabled crime only, which means many traditional transaction disputes and recording-related frauds don't fit neatly inside that count.

Why business owners face a different kind of risk

A homeowner may be dealing with one parcel and one closing. A business owner or investor may be managing a portfolio, tenant obligations, lender covenants, operating agreements, guaranties, and tax consequences. Fraud in that environment creates layered risk.

- Deal interruption: A title issue can stop a sale, refinance, or loan modification.

- Cash-flow pressure: Frozen proceeds or disputed escrows can affect payroll, vendor payments, and debt service.

- Exposure to other claims: Partners, lenders, or buyers may assert claims even when your business was the victim.

- Reputational impact: Investors and counterparties may question controls, authorization practices, and diligence.

Practical rule: If the problem touches title, loan proceeds, closing instructions, recorded documents, or disclosure failures, treat it as potentially fraudulent until a qualified lawyer proves otherwise.

A real estate fraud attorney doesn’t just “file a lawsuit.” The job is to diagnose what happened, identify the fastest path to stabilizing the asset, and choose the right legal remedy for the business objective. Sometimes that means clearing title. Sometimes it means pursuing money damages. Sometimes it means unwinding the transaction before the fraud spreads into a larger commercial dispute.

What Constitutes Real Estate Fraud in Connecticut

Not every bad deal is fraud. That distinction matters.

A failed renovation, an overoptimistic projection, or a dispute over contract wording may lead to litigation, but fraud requires something more deliberate. In practical terms, real estate fraud involves a knowing misrepresentation, concealment, or deceptive act used to induce someone to part with money, property rights, or legal advantage.

The key issue is intent to deceive

Think about selling a car with a bad engine. If the seller did not know about the defect, you may still have a dispute. If the seller knew the engine was failing, reset warning indicators, and told the buyer the car was in excellent condition, that starts looking like fraud. Real estate cases work much the same way.

The legal system usually separates these categories:

| Situation | What it usually suggests |

|---|---|

| An honest mistake in paperwork | Negligence, mistake, or contract dispute |

| A disagreement over value or interpretation | Commercial dispute, not necessarily fraud |

| A known defect or false statement hidden to get the deal done | Potential fraud |

| A forged signature, fabricated payoff, or fake authority | Strong fraud indicators |

That difference matters because fraud claims can support remedies that ordinary contract claims may not. They also change how a court views credibility, reliance, and damages.

How fraud shows up in real transactions

In Connecticut practice, fraud often appears through conduct, not dramatic admissions. Someone uses false authority to sign. A seller conceals a material condition to avoid losing the deal. A closing participant redirects funds with fake instructions. A business partner records documents designed to alter ownership advantage. A borrower or broker submits knowingly false information to secure financing.

Fraud can also overlap with contract law. A transaction may involve both. One party lies to induce the contract, then later claims the dispute is “just breach of contract.” That framing often benefits the wrongdoer. Victims need to examine whether the misconduct started before the ink was dry.

For a useful discussion of how false statements affect contractual rights, see this article on misrepresentation in a contract.

The fastest way to weaken a fraud case is to treat it like an ordinary deal dispute. The fastest way to strengthen one is to identify who said what, when they said it, what documents supported it, and how your business relied on it.

What Connecticut victims should focus on first

When clients describe suspected fraud, the useful questions are straightforward:

- Who made the statement or filed the document

- What exactly was false or hidden

- Why it mattered to the decision

- How the victim relied on it

- What money, title rights, or power changed hands because of it

That framework helps separate actionable fraud from ordinary transaction friction. It also gives your lawyer the building blocks for emergency relief, damages claims, quiet title work, and negotiations with insurers, lenders, or adverse parties.

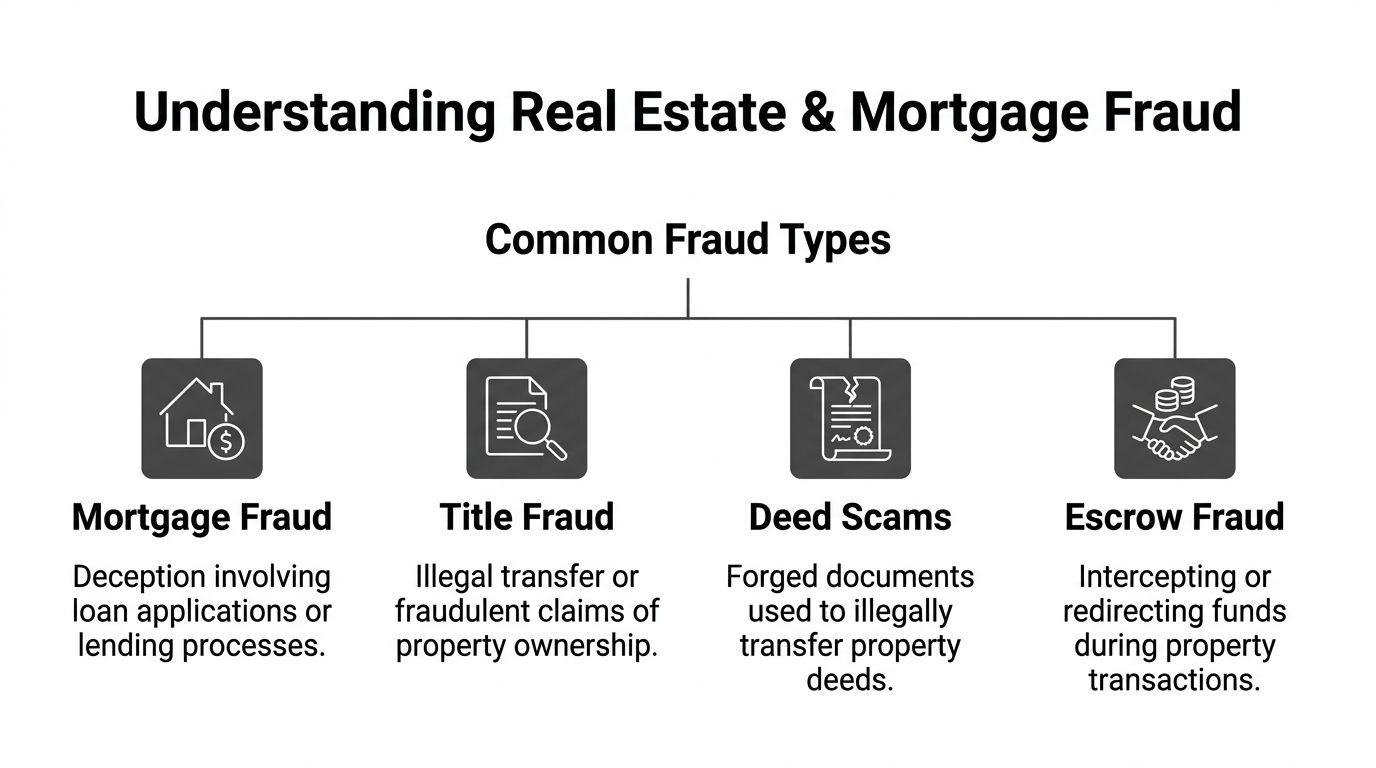

Common Types of Real Estate and Mortgage Fraud

Fraud schemes rarely arrive labeled. They usually show up as “closing confusion,” “title issues,” or “a disagreement over authority.” Once you pull the thread, the pattern becomes clearer.

This overview helps victims match what happened to a recognizable scheme.

For related disputes involving improper transfers designed to put assets beyond reach, this discussion of fraudulent conveyance is also useful.

Mortgage fraud

A borrower, broker, or intermediary submits false information to obtain financing that wouldn’t otherwise be approved. In residential matters that may involve fabricated income, fake occupancy plans, or undisclosed liabilities. In commercial settings, it can involve doctored rent rolls, false borrower authority, concealed side agreements, or manipulated financial disclosures.

One common version looks routine on paper. The file contains complete application materials, polished statements, and supporting documents that appear consistent. Only later does the lender or investor discover that key facts were invented or concealed to move the loan through underwriting.

Red flags often include:

- Documents that appear overly uniform: Pay records, leases, or financial statements that look generated for the file rather than kept in the ordinary course

- Last-minute changes in borrower structure: New entities, guarantors, or managers inserted without a clear business reason

- Occupancy or use representations that don't match reality: Especially when financing terms depended on that distinction

Title fraud

Title fraud targets ownership itself. A bad actor records documents that create the appearance of legal rights they don’t hold. That may be a forged deed, a fraudulent mortgage, an unauthorized release, or a fabricated assignment.

For an investor, the first signal may be a title company exception or a lender refusal. For an absentee owner, it may be much later. A property can sit unnoticed until a refinance, sale, or enforcement effort exposes the defect.

If a recorded document changes who controls the property, who gets paid, or what encumbers title, don’t assume the land records speak for themselves. Recorded doesn't always mean legitimate.

Deed scams and deed forgery

These schemes are direct. Someone signs another person’s name, uses a fake notarial process, or creates a deed that appears valid enough to enter the public record. The fraud may transfer title outright or position the fraudster to borrow against the property.

This often affects vacant property, inherited property, investment property, or any parcel where the true owner isn’t physically present. In business settings, it may involve forged corporate authority, fabricated resolutions, or someone acting as if they have signing power they do not possess.

A typical pattern:

- The fraudster identifies a property that appears easier to exploit.

- They prepare a deed or supporting transfer document.

- The document gets signed or notarized through deceptive means.

- The instrument is recorded.

- The fraudster tries to sell, finance, or monetize the asset before the owner reacts.

Escrow and closing fraud

This category often involves diverted funds. The fraudster intercepts email traffic, spoofs instructions, or manipulates communications so money goes to the wrong account. It can also involve someone inside the transaction misusing escrowed money or disbursing contrary to closing instructions.

The reason these cases are dangerous is speed. Once money leaves the intended channel, recovery becomes harder. Delay helps the wrong person. Businesses should treat any unexplained change in payment instructions as a legal problem, not just an accounting problem.

Look closely at:

- Unexpected wiring changes

- Requests to bypass established verification procedures

- Instructions that arrive with urgency but little context

- Pressure to close before inconsistencies are resolved

Disclosure fraud and concealment

Some fraud cases don't involve forged documents at all. They involve what someone chose not to say. A seller may hide structural issues, environmental conditions, occupancy problems, or defects that materially affect value or use. In investment deals, a sponsor or manager may withhold lease problems, litigation exposure, or income instability while soliciting capital or negotiating a sale.

This type of case often turns on documents created before the sale. Internal emails, inspection records, contractor communications, prior tenant complaints, and insurance claims can matter far more than the closing file itself.

Fraud in commercial real estate relationships

Commercial fraud often grows out of a relationship that once looked legitimate. A partner self-deals. A manager records unauthorized interests. A borrower misstates collateral status. A seller conceals facts that would have changed pricing or lender approval. A distressed asset workout becomes an opportunity for someone to exploit confusion over authority, defaults, or document control.

These are rarely simple cases. They often involve overlapping claims for fraud, breach of fiduciary duty, conversion, unjust enrichment, and contract breaches. They may also affect collections strategy if the wrongdoer moved assets after the dispute surfaced.

Connecticut Legal Remedies and Statutes of Limitation

Once fraud is identified, the next question is practical. What can a Connecticut victim do about it?

The answer depends on the business goal. Some clients want the property back. Some want title cleared so a transaction can close. Some want money damages. Some need all of the above, plus injunctive relief to stop additional transfers or encumbrances.

The main civil remedies in Connecticut

A real estate fraud attorney usually evaluates several remedies at once, because one claim rarely solves the entire problem.

| Remedy | When it fits | Primary objective |

|---|---|---|

| Damages claim | You suffered financial loss from deception | Recover money |

| Rescission | The transaction was induced by fraud | Undo the deal |

| Quiet title action | The land records are clouded or ownership is disputed | Clear title |

| Injunctive relief | Immediate action is needed to stop transfers or preserve rights | Stabilize the asset |

| Related business tort claims | The fraud overlaps with fiduciary or asset diversion issues | Expand recovery options |

Rescission can be powerful when the transaction itself was tainted from the start. Quiet title is often essential when a forged deed, false lien, or unauthorized instrument sits in the land records. Damages become critical where fraud caused lost proceeds, financing harm, litigation costs, or business disruption.

Why local law matters

Real estate fraud isn’t governed by one national playbook. State law changes both the available remedies and the pressure points in negotiation.

For example, California Civil Code Section 2945.4 establishes criminal liability for foreclosure fraud, defining prohibited acts like charging excessive fees or taking power of attorney through deception, as discussed by Los Angeles Criminal Lawyer. That’s a useful reminder for Connecticut businesses with out-of-state assets or counterparties. Multi-state deals require jurisdiction-specific analysis. The same conduct may create very different legal advantages depending on where the property sits and where the parties acted.

A victim’s biggest early mistake is assuming “fraud is fraud everywhere.” It isn’t. The facts may be similar, but remedies, deadlines, and procedural tools change from state to state.

Connecticut statutes of limitation

Deadlines can decide the case before the merits are ever reached. The exact limitation period depends on the claim asserted and the facts supporting it. Because fraud cases often involve overlapping theories, lawyers typically analyze several deadlines, not just one.

Here is a practical planning table.

| Claim Type | Statute of Limitation | Governing Statute (Example) |

|---|---|---|

| Fraud or intentional misrepresentation | Fact-specific and should be analyzed promptly | Connecticut statute and case-law analysis required |

| Breach of written contract tied to the transaction | Fact-specific and should be analyzed promptly | Connecticut statute and contract terms required |

| Negligence connected to closing or professional conduct | Fact-specific and should be analyzed promptly | Connecticut statute and role of the defendant required |

| Quiet title or ownership-related relief | Timing can depend on possession, recording, and claim posture | Connecticut property statutes and equitable principles required |

| CUTPA or related business claims | Fact-specific and should be analyzed promptly | Connecticut statute and transaction context required |

Because deadlines are claim-specific, the safest move is immediate legal review. For a broader starting point on deadline analysis, see this overview of Connecticut statutes of limitations.

Choosing the right mix of claims

What works in practice is claim selection tied to business objectives.

If title is clouded, don’t lead with a damages-only mindset. You may need court orders that directly address the land records. If the fraudster is moving assets, don’t wait to see whether a demand letter changes behavior. If insurers, lenders, or investors are involved, build the record in a way that supports both litigation and parallel claim handling.

What usually doesn’t work is filing a broad complaint without a clear asset-protection plan. Fraud cases often require sequencing. Preserve evidence first. Stabilize title or proceeds second. Then pursue full recovery with the strongest factual record available.

Immediate Steps for Victims of Property Fraud

The first few days matter. The goal is to stop additional damage and avoid mistakes that make recovery harder later.

Preserve every document and communication

Don’t edit anything. Don’t forward chains with commentary added into the body. Save emails, PDFs, wiring instructions, title commitments, closing statements, corporate resolutions, signature pages, text messages, and voicemail records in their original form if possible.

Create a clean chronology that includes dates, names, entities, and what each person did. In business disputes, internal approvals and authority records often matter as much as the fraudulent document itself.

- Keep originals intact: Metadata and file history can matter.

- Separate fact from assumption: Record what happened, not what you think happened.

- Centralize the file: One organized evidence set beats five inconsistent inbox exports.

Notify the right institutions fast

If money was diverted, notify the sending bank, receiving institution if known, title company, escrow participant, and lender immediately. If the problem involves a recorded document, alert the title insurer and gather certified land records.

If the fraud touches a Connecticut property, reporting may also involve local law enforcement and state agencies, depending on the facts. A lawyer can help determine the right sequence so you don’t create inconsistent statements across forums.

Don't start with a broad email blast to everyone involved. Start with targeted notices that preserve rights, request holds where appropriate, and avoid unnecessary admissions or speculation.

Stop direct engagement with the suspected fraudster

Victims often want answers. That impulse is understandable and sometimes expensive.

The wrongdoer may use the conversation to test your evidence, shape a defense, shift blame, or lure you into a side agreement that complicates later claims. If communication is necessary, it should be planned. In many cases, counsel should handle it from the start.

Protect the business around the asset

Fraud involving one property can affect broader operations. Review pending closings, covenant obligations, investor notices, tenant-facing issues, and insurance requirements. If the property supports financing, operations, or collateral packages, contain the spillover early.

Act on these questions right away:

- Is there a transaction scheduled that must be paused

- Do lenders or investors require notice

- Has title insurance been triggered

- Is there any risk of another transfer, encumbrance, or disbursement

- Are internal authorization controls part of the problem

That triage helps your lawyer decide whether the next move is negotiation, emergency court relief, insurer engagement, or a full civil action.

Working With a Real Estate Fraud Attorney What to Expect

Clients usually want two things at the first meeting. They want a clear read on whether this is really fraud, and they want to know how recovery happens.

A real estate fraud attorney should give you both. Not guarantees. A plan.

The first phase is diagnosis and stabilization

Early work is less glamorous than people expect. Counsel gathers the key documents, maps the transaction, identifies who had authority, and tests the facts against possible causes of action. In many matters, this phase also includes notices to insurers, communication with lenders or title parties, and evaluating whether emergency relief is needed.

You should expect detailed questions about:

- Entity structure and authority

- Who negotiated the transaction

- How funds moved

- What title work existed before the problem surfaced

- Whether related disputes exist with partners, brokers, investors, or servicers

If the matter involves investment real estate or pooled capital, the case may overlap with broader investor or securities issues. That’s one reason commercial counsel sometimes coordinate with professionals who handle adjacent disputes, including forms of expert legal support where occupancy or landlord-tenant issues intersect with the underlying property conflict.

The second phase is pressure with purpose

Once the facts are clearer, your attorney chooses how to apply pressure. That might include a demand letter, a quiet title filing, claims for fraud and related business torts, discovery aimed at tracing money, or negotiations with a title carrier or adverse party. The best approach depends on the strategic advantages.

Some cases should be filed quickly because delay benefits the wrongdoer. Others benefit from focused pre-suit work that locks in documents and narrows the dispute. What doesn’t work is aggressive posturing without a recovery theory. Litigation has to be tied to the asset, the money trail, and the practical endgame.

For disputes centered on ownership boundaries, title rights, or competing claims to property interests, this overview of land dispute attorneys gives useful context.

Good fraud litigation isn't just about proving dishonesty. It's about turning proof into a remedy that matters to the client.

What outcomes are realistic

Real outcomes vary. Some matters settle after the other side sees the documentary record. Others require prolonged civil litigation, parallel insurer involvement, or coordination with law enforcement. In fraud matters, the structure of the claims can materially affect the strength of one's position.

A concrete example comes from Ringler Law Corporation, which recovered $5.5 million for 19 homeowners by prosecuting a construction defect case under fraud and non-disclosure theories, a strategy that, in the firm’s words, could “considerably raise the stakes” beyond a simple contract theory. The important lesson for Connecticut victims isn’t the jurisdiction. It’s the litigation design. When facts support fraud, pleading and proving fraud can change settlement posture and damages analysis.

What clients can do to help their own case

The strongest clients are disciplined. They gather records, stop improvising communications, and align internal decision-makers early.

Useful habits include:

- Designate one business contact: Mixed messages create avoidable problems.

- Preserve calendars and internal approvals: Authority disputes often turn on these records.

- Avoid “fixing” documents: Even innocent changes can create authenticity fights.

- Think commercially: The best outcome may be title clearance, a structured settlement, or targeted asset recovery rather than scorched-earth litigation.

The attorney-client relationship in these cases should feel candid and strategic. You should understand the risks, the likely pressure points, and the cost-benefit tradeoffs of each major decision.

Protect Your Investment and Fight Back Against Fraud

Real estate fraud can leave a business owner feeling ambushed by paper. A forged deed, a diverted wire, a hidden defect, or a false filing can derail a transaction and create exposure far beyond the property itself. But victims aren't powerless. The law provides tools to clear title, unwind tainted deals, pursue damages, and stop additional misconduct.

What matters most is speed and precision. Preserve the record. Stop unnecessary communication. Identify the true business objective. Then match that objective to the right legal remedy. In Connecticut, that usually means looking beyond one label and analyzing the full problem. Title issues, fraud claims, contract rights, lender concerns, insurance questions, and partner disputes often arrive together.

The practical difference between a manageable fraud case and a significantly expensive one is often what happens in the first days after discovery. Businesses that act quickly usually preserve more options. Businesses that treat fraud like routine closing noise often lose their advantage before the fight really starts.

If you believe you’ve been victimized, get the facts organized and get legal advice before the situation hardens. A strong response isn’t emotional. It’s structured, documented, and aimed at recovery.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.