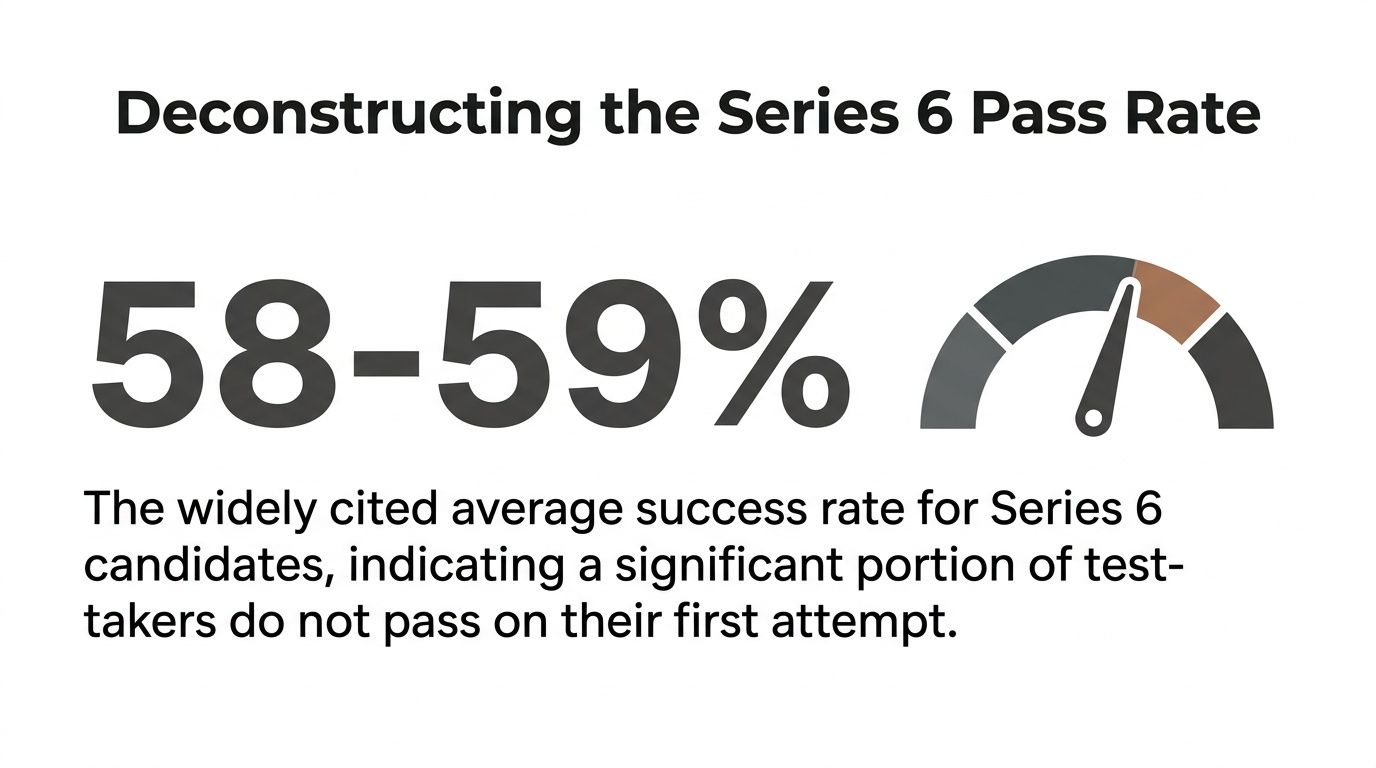

The official first-time Series 6 pass rate is 59%, and industry sources often cite 58%. That means more than 40% of first-time takers fail, which makes this exam a real career gate, not a formality.

For advisors, the pass rate for Series 6 matters for more than bragging rights. A failed attempt can delay onboarding, interrupt production plans, strain sponsor relationships, and in some firms create employment consequences that reach far beyond exam prep. The smart way to look at this exam is through two lenses at once: how to pass it, and how to avoid turning a licensing setback into a regulatory or career problem.

Your Guide to the Series 6 Exam

The pass rate for Series 6 often prompts a deeper question. You want to know whether this is an exam you can manage on the first try, or whether you're walking into a preventable setback.

That concern is justified. A sub-60% first-time pass rate tells you the test punishes loose preparation, weak reading discipline, and overconfidence. It also tells you something else that many prep discussions miss. In a brokerage or insurance-affiliated setting, the exam isn't just academic. It's tied to timing, supervision, compensation, and your standing with the firm sponsoring you.

Why advisors should treat this as a business risk

The Series 6 sits at the intersection of sales authority and regulatory competence. If you need it to sell packaged securities products, delays in licensure can affect your role, your transition plan, and your near-term income expectations.

That's why it helps to think like a regulated professional, not like a student cramming for a quiz.

- Licensing affects employability: Firms hire against production needs and licensing windows.

- Failure affects credibility: Managers may forgive one miss. They often become less flexible when preparation looked casual.

- The record around separation matters: If employment ends because required licensing wasn't obtained, how that event is characterized can matter later.

Professionals looking at the broader licensing path can also compare roles and registration tracks through this overview of how to become a stock broker.

Practical rule: Treat your Series 6 study plan the same way you'd treat a suitability file. Build it early, document it, and don't assume you can fix weaknesses at the last minute.

What actually works

The candidates who usually put themselves in the best position do three things well. They respect the exam blueprint, they practice under time pressure, and they stop relying on recognition alone.

What doesn't work is equally clear. Reading a manual once, memorizing isolated definitions, and postponing full-length timed practice until the final days is a poor trade. The exam rewards application, not familiarity.

What Is the Series 6 Exam and Who Needs It

The Series 6 exam is the qualification exam for representatives who want authority to sell a limited menu of securities products rather than the broader universe covered by Series 7. It exists for a specific role: the professional who works with packaged investment products and variable contracts, often in insurance, retirement, or bank-based settings.

The exam is administered by FINRA and sits inside a broader registration path. It isn't a standalone credential you casually pick up. It is part of a regulated sequence tied to sponsorship, role definition, and product scope.

What the license covers

According to Ironclad Law's summary of the Series 6 exam format and product scope, the exam includes 50 scored multiple-choice questions plus 5 unscored pretest questions mixed into a total of 55, and candidates can't tell which items are scored. That same source explains that FINRA and the SEC require this license for representatives who want to sell specific products including mutual funds, UITs, and municipal fund securities such as 529 college savings plans.

This is why the Series 6 appeals to advisors whose practices center on packaged products instead of individual stock or broader securities activity.

How the exam is built

The exam is tightly structured. It has a fixed time limit, a fixed scoring threshold, and a content focus that has shifted toward customer-facing conduct and practical interactions.

A few points matter on day one of preparation:

- You won't know the unscored questions: So every item deserves full attention.

- The test is multiple choice, but not simple: Distractors are designed to punish shallow reading.

- Customer interaction matters: The exam's orientation isn't just product trivia. It reflects how representatives communicate and operate.

For advisors weighing narrower versus broader registrations, this comparison of Series 63 vs. Series 7 helps frame where Series 6 fits in an actual career path.

The most costly mistake is choosing a licensing track without understanding what products and client activity your role will actually require.

Why the SIE relationship matters

The Securities Industry Essentials exam is a required corequisite before taking Series 6. That matters because the Series 6 candidate pool has already cleared an earlier barrier. If you're evaluating the pass rate for Series 6 in isolation, you're missing the fact that entrants have already been screened for baseline industry knowledge before this exam even begins.

Deconstructing the Series 6 Pass Rate

Roughly 4 in 10 first-time Series 6 candidates do not pass. For advisors, that number matters. It affects licensing timelines, onboarding expectations, manager confidence, and, in some firms, your margin for error before employment questions start.

The official and industry figures

FINRA's Series 6 qualification page sets out the exam itself and the SIE co-requisite. Industry providers that track exam prep outcomes, including Achievable's Series 6 overview and Ironclad Law's discussion of the Series 6 pass rate, commonly cite a first-time pass rate in the high-50% range.

The exact figure matters less than the operating reality. A large minority of first-time test takers fail.

For a licensing exam tied to a limited representative role, that is a serious attrition rate.

The filter most candidates miss

The pass rate gets misunderstood because many people read it as if it describes true beginners. It does not. The Series 6 pool has already been narrowed by the mandatory SIE requirement.

That changes the meaning of the statistic.

Candidates sitting for Series 6 have already cleared an earlier screen for baseline securities knowledge. So a sub-60% first-time pass rate does not suggest candidates have never seen the material before. It suggests many are still unable to apply rules, product limits, and client-facing obligations with enough precision to pass a timed regulatory exam.

From a compliance perspective, that distinction matters. The exam is not just measuring familiarity with terms. It is measuring whether a candidate can function within a narrower registration without creating avoidable risk.

What the pass rate actually signals

A filtered candidate pool with a pass rate in the high 50s usually points to specific weaknesses, not bad luck.

| Signal | What it usually means |

|---|---|

| “Limited” gets misread as “easier” | Candidates underprepare because the license sounds narrower than Series 7 |

| SIE success creates false confidence | Foundational knowledge gets mistaken for exam readiness |

| Product knowledge outruns rule application | Candidates know what a mutual fund is, but miss suitability, communication, or sales-practice details |

| Timed reading breaks discipline | They change right answers, miss qualifiers, or answer from memory instead of from the fact pattern |

The career point is easy to miss. Failing once is usually a study problem. Failing repeatedly can become an employment problem, especially in firms that track licensing deadlines closely and document performance concerns. That is why the pass rate should be read as more than an exam statistic. It is an early warning about preparation quality and, for some advisors, about downstream legal and Form U5 risk if exam trouble starts affecting the job itself.

Why So Many Candidates Fail the Series 6

A large share of first-time candidates do not pass this exam, and the reasons are usually visible well before test day. By the time a candidate walks out surprised by a failing score, the problem has often been building for weeks in the way they studied, practiced, and judged their own readiness.

Candidates misread what the exam rewards

Series 6 is narrow in product scope, but it is not forgiving. Candidates who come in after the SIE often make a predictable mistake. They treat this exam as a shorter version of basic securities study, when the actual task is applying rules to client-facing situations with precision.

That distinction matters.

A candidate may know what a mutual fund, variable annuity, or 529 plan is and still miss the question because the tested issue is suitability, prohibited conduct, communications standards, or the representative's permitted role. In practice, I see the same pattern supervisors see in new hires. Recognition gets mistaken for mastery.

Weak preparation patterns

Several study habits lead to avoidable failures:

- Treating a limited registration like a light exam: A narrower license creates false comfort. The questions still test judgment under FINRA rules.

- Reading without retrieval practice: Candidates highlight manuals and watch videos, but they do not force themselves to recall rules from memory and apply them under pressure.

- Studying topics evenly instead of by exam weight: Time gets wasted on low-value review while heavily tested functions stay shallow.

- Delaying full timed exams: Pacing problems usually appear late because candidates postpone realistic practice until the final few days.

The candidate who says, “I knew the material,” often means, “I recognized the chapter headings.” That is not enough to pass a timed regulatory exam.

Function 3 gives candidates trouble for a predictable reason

This part of the exam exposes weak judgment fast. It tests communication with customers, recommendations, disclosures, and the handling of investment information inside a regulated sales process. Those are the same areas that create real supervisory risk inside a firm.

Candidates miss these questions because they answer from product familiarity instead of from the rule set that governs the interaction. They pick the answer that sounds commercially reasonable, not the one that is compliant. On Series 6, that mistake is costly. On the job, it can become a documentation issue, a supervisory issue, or both.

That is the point many prep guides miss. Failure is not only an academic problem. Repeated exam trouble can start to affect how a firm views reliability, coachability, and licensing risk.

Test-day errors still sink prepared candidates

Some candidates know enough to pass and still lose points through poor execution. They rush through qualifiers such as best, first, or most appropriate. They change correct answers after second-guessing themselves. They spend too long fighting through one difficult question and create a pacing problem for the rest of the exam.

Those are not minor mistakes. On an exam with a tight margin for passing, a handful of discipline errors can separate a clean first-time pass from a retake and the employment pressure that can follow.

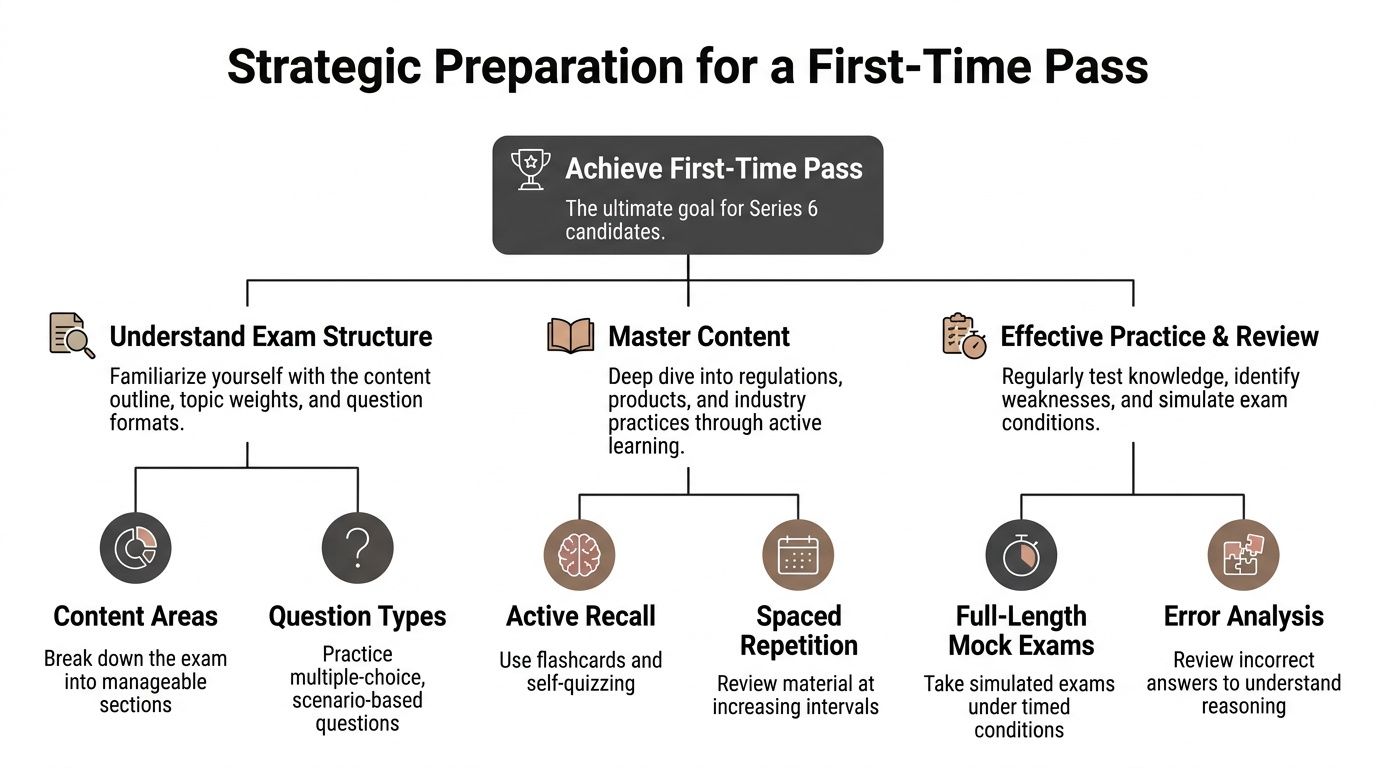

Strategic Preparation for a First-Time Pass

A first-time pass usually comes from structure, not motivation. Candidates who perform well tend to narrow the task into a controlled system: content review, recall testing, error analysis, and timed simulation.

That matters because the Series 6 is scored precisely. According to Achievable's FINRA exam guide, candidates must answer 35 out of 50 scored questions correctly to earn a 70% passing score within 90 minutes, and recommended preparation is 40 to 50 hours with heavy attention to Function 3.

Build a study plan around the scoring reality

You don't need to master every sentence in every manual equally. You do need a study plan that reflects how the exam behaves.

A practical approach looks like this:

Start with the outline, not the textbook

Know what is tested before you decide how to study it. Candidates who begin with raw reading often spend too much time on material that feels difficult rather than material most likely to drive the score.

Give Function 3 extra weight

This is the section many candidates feel they “sort of know.” That's dangerous. If your grasp of product communication, recommendation logic, and related rules is soft, your practice scores may look acceptable until harder question sets expose the weakness.

Use active recall every week

Flashcards, self-quizzing, and verbal explanation force retrieval. Passive highlighting doesn't.

What works better than rereading

Rereading is comfortable. Comfort is not the goal.

Use a mixed method instead:

- Question banks: Answer questions in small sets, then review every wrong answer for the rule behind it.

- Handwritten rule sheets: Summarize recurring distinctions you keep missing.

- Timed mini-blocks: Train pace before you attempt full mock exams.

- Error logs: Track patterns. If you repeatedly miss suitability-style items or product distinctions, that's the issue to solve.

Exam discipline: Don't just ask whether an answer is wrong. Ask why the wrong option looked tempting. That's where most preventable errors live.

Handle test day like a controlled process

The best preparation loses value if test-day execution is sloppy. Candidates should arrive with routines already practiced. Read stems carefully. Mark difficult items mentally, keep moving, and resist the urge to litigate each answer in real time.

A clean test-day plan should cover:

| Priority | What to do |

|---|---|

| Pacing | Keep a steady rhythm from the first question |

| Stamina | Practice enough timed sets that 90 minutes feels familiar |

| Decision-making | Eliminate bad answers first, then choose among plausible ones |

| Review | If time remains, revisit flagged items without changing answers impulsively |

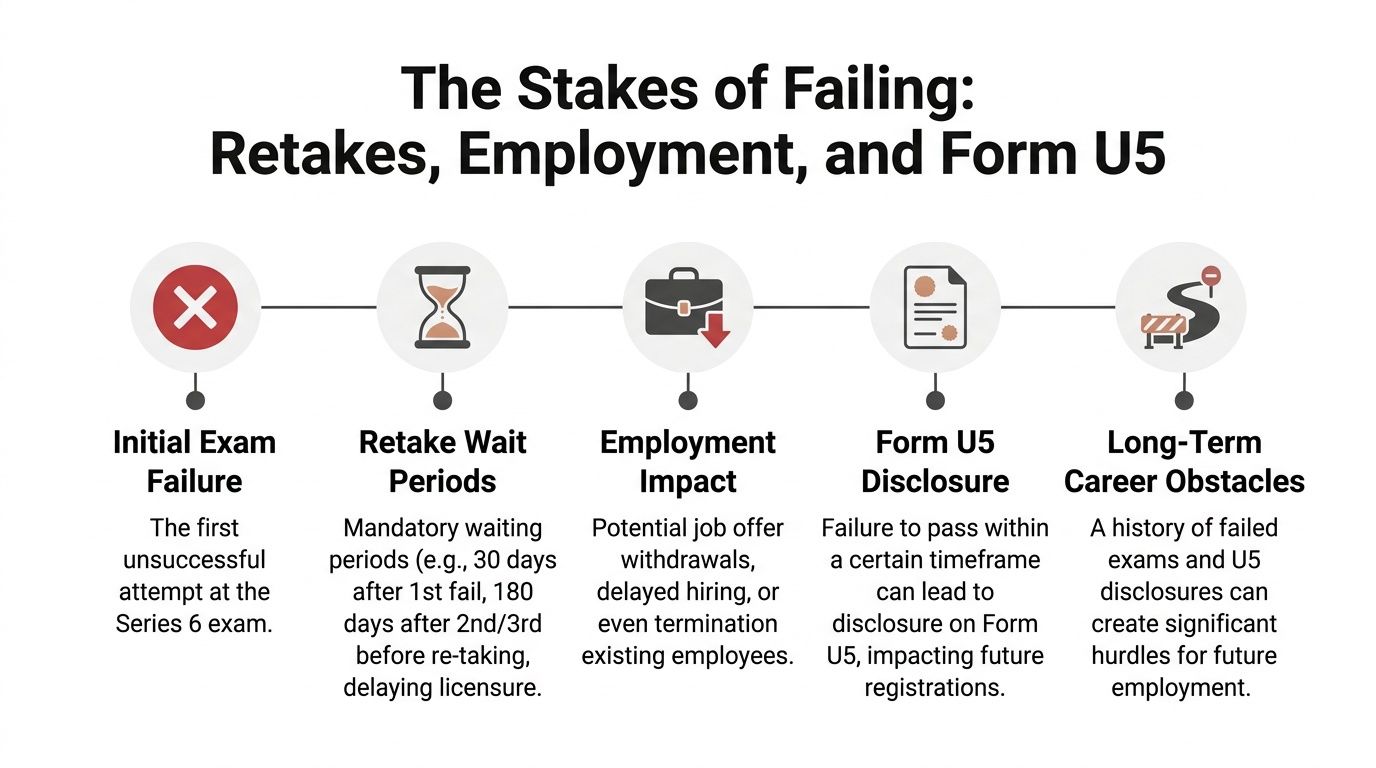

The Stakes of Failing Retakes Employment and Form U5

Failing the Series 6 is not automatically catastrophic. But it can become costly if you ignore the employment and disclosure issues that often ride behind licensing problems.

Often, exam articles fall short. They discuss retakes as if the only consequence is inconvenience. Beyond inconvenience, failed attempts can affect training programs, branch staffing decisions, compensation timing, and whether a firm keeps investing in you.

Why exam failure can become an employment problem

A sponsored candidate is rarely studying in a vacuum. The firm often has a licensing window, a training budget, and a staffing expectation. If the candidate misses the exam more than once, management may decide the issue is not bad luck but execution risk.

In some programs, repeated failure can result in delayed start dates, reassignment, or termination. Even when the separation itself is straightforward, the wording around it matters.

That's where advisors need to think ahead. A neutral statement tied to failure to obtain required licensing is very different in practical effect from language that suggests poor judgment, compliance weakness, or broader performance concerns.

Form U5 risk is often mishandled

If employment ends, the reporting implications can follow the advisor long after the exam issue itself is over. Anyone in that position should pay close attention to how the termination is characterized and whether the language used is accurate, narrow, and supportable.

For advisors dealing with separation language or disclosure concerns, this discussion of Form U5 FINRA issues is directly relevant.

A licensing failure should stay a licensing failure. Trouble starts when firms or managers use loose language that creates a different story in the record.

Internalization matters more than people think

There's also a practical point about exam readiness itself. According to Investopedia's explanation of Series 6 test-day conditions, the testing center provides scratch paper, pencils, and a calculator, but no external notes or devices are permitted. Candidates have to internalize the concepts well enough to work without outside prompts.

That test-day rule has a broader lesson. If your study system depends on constantly checking notes, your preparation probably isn't deep enough yet.

Career protection after a setback

If you fail, respond with discipline.

- Document the timeline: Keep records of study efforts, communications, and retest planning.

- Control the narrative with the firm: Be direct about remediation and scheduling.

- Review separation documents carefully: If employment is ending, language matters.

- Don't treat a U5 issue casually: Small wording choices can create large future headaches.

In practice, the best risk mitigation starts before any dispute exists. Candidates who prepare seriously reduce not only the chance of failure, but also the chance that a temporary licensing issue snowballs into an employment or registration problem.

Navigating Your Next Steps with Confidence

The pass rate for Series 6 deserves respect, but it shouldn't intimidate you into paralysis. What it should do is force a realistic approach. This is a regulated exam tied to real client activity and real professional consequences.

The number that matters most isn't just the high-50s pass rate. It's the fact that the exam sits after an SIE filter and still eliminates a large share of first-time takers. That tells you preparation has to be deliberate, practical, and aligned with how the test works.

A sound next-step checklist

If you're getting ready for the exam, focus on decisions that reduce both testing risk and career risk:

- Match your study plan to the exam structure: Don't rely on reading alone.

- Practice under timed conditions: You need pacing, not just knowledge.

- Give applied material the attention it deserves: Especially customer-facing and recommendation-driven content.

- Think ahead about employment context: If your role depends on prompt licensure, treat the exam as a business deadline.

Advisors also benefit from keeping the broader compliance picture in view. This overview of compliance for RIA is useful if your path includes advisory or supervisory obligations beyond the exam itself.

Career readiness is bigger than one test

Candidates who are changing firms or preparing for client-facing interviews should also sharpen how they present experience, judgment, and regulatory awareness. A practical resource on top account management interview questions can help professionals prepare for the kinds of conversations that often follow licensing, transition, or role expansion.

A final point matters. Passing the Series 6 is not just about obtaining authority to sell certain products. It is about showing that you can operate under rules, absorb process, and perform under pressure without creating avoidable risk for yourself or the firm.

| Service | Contact Information |

|---|---|

| Business law matter | Kons Law at (860) 920-5181 |

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.