You left your firm on Friday. By Monday, a recruiter is asking whether your registration transfer will be clean, a branch manager wants an explanation for the separation, and someone mentions the Form U5 as if it were routine paperwork.

It isn't.

For a financial advisor, a Form U5 can become the official version of why your employment ended. Future firms review it. Regulators review it. In the wrong case, clients and counterparties may start asking questions that you weren't prepared to answer. A vague line, an overbroad disclosure, or a loaded termination reason can create problems long after the employment relationship is over.

Most articles stop at the definition. That doesn't help much when you're the person trying to preserve licenses, move a book, answer recruiters, and decide whether the language on the filing is merely unfavorable or something you need to fight immediately.

Your Employment Ended Now What About the Form U5

A common version of this problem looks like this. An advisor resigns after months of friction with a manager. The firm says the departure is being “reviewed.” The advisor expects a standard offboarding process, then learns a Form U5 will be filed and starts hearing terms like “discharged,” “permitted to resign,” or “under internal review.”

That is usually the moment the issue becomes real.

If you're in that position, your first instinct may be to treat the U5 like an HR exit form. That's a mistake. In practice, it is a regulatory filing with career consequences. It can influence how a new firm evaluates your hire, how quickly you can move through registration, and the bargaining power each side holds in any post-separation dispute. Advisors who have restrictive covenants or compensation issues should be just as careful about the surrounding documents, including an employment agreement review, because the U5 rarely exists in isolation.

What advisors get wrong in the first week

The biggest early mistake is waiting to “see what happens.” By the time an inaccurate narrative starts circulating, you may already be answering for language you didn't write and didn't approve.

Another mistake is focusing only on whether the departure was fair. Fairness matters, but U5 disputes usually turn on wording, classification, timing, and proof. You need documents, dates, names, and a coherent explanation of what happened.

Practical rule: The first days after separation are for record preservation, not venting. Save emails, messages, notes from meetings, compensation records, compliance communications, and any draft separation terms.

A third mistake is assuming a clean conscience automatically leads to a clean filing. It doesn't. Firms file the form, not the individual. If the wording is sloppy, aggressive, or unsupported, you may need to challenge it quickly.

What Is the FINRA Form U5 and Why Does It Matter

FINRA Form U5 is the Uniform Termination Notice for Securities Industry Registration. FINRA states that it must be filed when an individual leaves a firm for any reason, and the submission is required within 30 days of the person's employment end date, generally through Web CRD, according to FINRA's Form U5 instructions.

That filing requirement is only the start. FINRA also requires firms to provide timely, complete, and accurate information, and Regulatory Notice 10-39 reiterates that the disclosure must contain enough detail for a reasonable person to understand the circumstances behind an affirmative response. If the language is too thin, too broad, or plainly wrong, the filing can still create immediate damage while everyone argues later about what it meant.

For advisors trying to understand the practical side of Form U5 FINRA issues, think of the document as a regulatory narrative. It records the fact of your departure, but it also frames the reason. That framing matters because it can affect future registrations, background checks, and disputes over the reason for termination. Advisors dealing with these issues often also need counsel on the underlying securities regulation matters that can grow out of the filing itself.

Why firms and future employers scrutinize it

A receiving firm doesn't read a U5 casually. It reads it as a risk document. Compliance staff want to know whether the departure signals a paperwork problem, a business dispute, a supervision concern, or a potential misconduct issue.

A recruiter may ask softer questions. A compliance department usually won't.

What the form does in practice

A U5 often becomes the anchor document for several decisions at once:

- Registration review: A new firm may delay onboarding until it understands the filing.

- Internal compliance escalation: Certain disclosures trigger more detailed questioning.

- Reputation management: The advisor has to explain the departure consistently to firms, clients, and counsel.

- Dispute posture: The wording can affect whether the matter stays informal or turns into arbitration.

A U5 isn't just about why you left. It's about what the record says happened when you left.

That is why careful advisors don't ask only, “Was the form filed?” They ask, “How was it classified, what language was used, and what support exists for each statement?”

Decoding Your Form U5 Termination Reason

Most advisors focus on one line first, the termination reason. That's sensible. It is often the first thing a reviewer notices and the first thing you will be asked to explain.

The labels carry different signals

The common labels are familiar, but their practical impact differs sharply.

| Termination Reason | What It Means | Potential Impact |

|---|---|---|

| Voluntary | The firm reports that you left by choice | Usually the easiest category to explain, though surrounding disclosures still matter |

| Permitted to Resign | The firm allowed a resignation instead of stating a discharge | Often signals an underlying dispute or review and invites follow-up questions |

| Discharged | The firm states it terminated you | Commonly treated as a significant red flag and usually requires a detailed explanation to future firms |

The label alone doesn't decide your future, but it shapes the conversation. “Voluntary” may still sit next to damaging disclosure language. “Discharged” may be explainable if the underlying issue was administrative or disputed. The point is not to panic at the category. The point is to read it with the rest of the filing.

Full termination, partial termination, and amendments

A lot of advisors miss another critical distinction. A U5 can be filed as a full termination, a partial termination, or later amended.

As explained in this discussion of FINRA U5 classifications, a full U5 terminates all registrations, a partial U5 removes only selected jurisdictions, SROs, or roles, and an amendment updates prior information such as the termination reason, disclosure responses, or residential data. Those differences matter because amendments can retroactively change how a departure is interpreted by regulators and future firms.

How to read between the lines

When I review a U5 dispute, I don't look only at the headline category. I compare the category to the surrounding facts.

Ask these questions:

Does the category match the separation documents?

If you resigned with written notice, “discharged” needs scrutiny.Do the disclosures track actual events?

A reference to an internal review should be supported by real facts, not post hoc framing.Is the language factual or conclusory?

“Violated firm policy by failing to submit X” is different from “acted with deceit.”Was the form later amended?

A later change may help you, hurt you, or reveal that the original filing was rushed.

Advisors facing this issue sometimes also need to understand whether the firm's wording hints at broader allegations, including matters commonly grouped under securities fraud concepts, even where no such finding has been made. That distinction is important because imprecise language can create a much harsher impression than the facts support.

Watch for this mismatch: a mild employment dispute paired with severe regulatory wording. That often signals a challenge worth examining.

The Career Impact of a Negative Form U5 Disclosure

A negative U5 doesn't stay in the past. It follows you into interviews, transfer discussions, and internal reviews at the next firm.

The damage usually begins with delay. A firm that was ready to hire you may pause and ask for documents, explanations, and supporting correspondence. During that pause, the recruiting narrative can shift from production, clients, and fit to whether your record presents avoidable compliance risk.

Why the issue can't be brushed aside

Form U5 disputes are not rare. Littler reported that FINRA dispute-resolution data showed a 24% increase in Form U5 defamation claims over the referenced period, and ThinkAdvisor reported that FINRA's disciplinary system typically brings about 700–800 disciplinary actions per year after reviewing more than 25,000 cases, as summarized in Littler's discussion of rising Form U5 defamation claims.

Those figures matter because they show how seriously the industry treats this document. Firms don't view U5 language as a clerical detail. They treat it as a risk signal.

How a negative disclosure affects an advisor in the real world

The consequences are often practical before they become legal:

- Hiring friction: A new firm may hesitate to extend or finalize an offer.

- Registration pressure: Extra review can slow your transition.

- Client questions: If your move becomes visible, clients may wonder whether there is more to the story.

- Bargaining power: A former firm may gain bargaining power if the filing creates urgency on your side.

A particularly harmful feature of U5 disputes is that broad or accusatory wording can outlast the employment dispute that caused it. Even if you later reach a compensation settlement, the filing may remain a separate problem unless it is corrected.

The hidden business cost

Advisors often think first about pride and reputation. Those matter. But the immediate business problem is continuity. If the U5 complicates your move, every delayed client transfer and every uncertain recruiter conversation creates pressure.

A bad U5 can change the question from “Where are you going next?” to “Will another firm take the risk?”

That is why timing matters. The longer damaging language sits unchallenged, the more likely it becomes the default version of events.

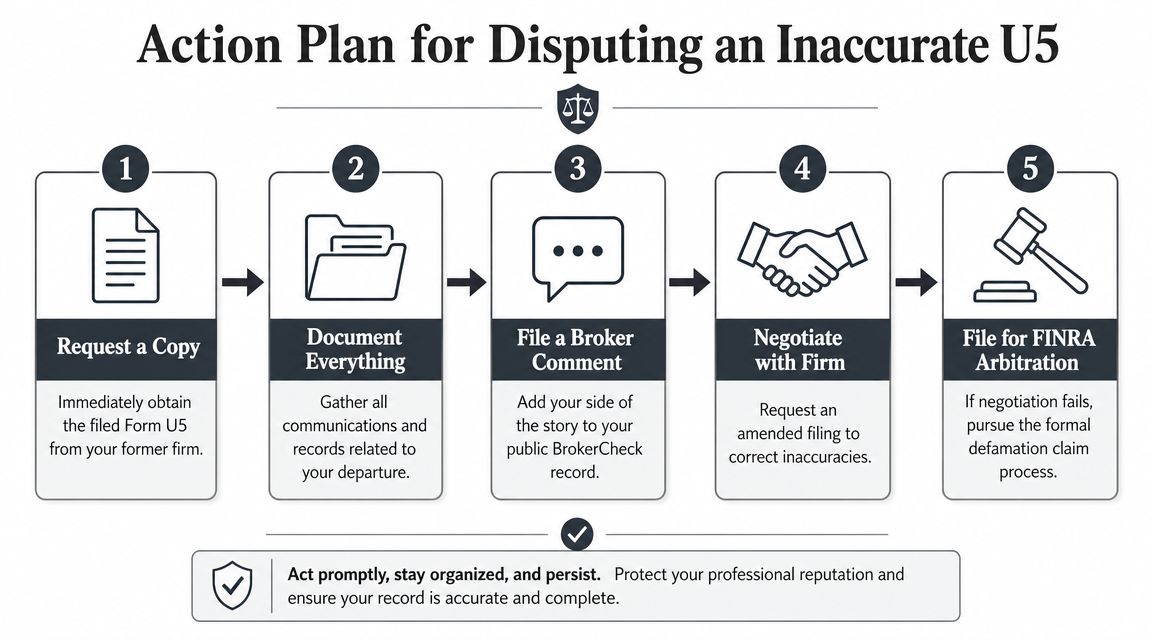

Your Action Plan for Disputing an Inaccurate U5

Your employment ends on Friday. By Monday, a recruiter asks about language on your U5 that you have not even seen yet. That is how these disputes often begin. If the filing overstates what happened, uses loaded wording, or suggests misconduct the facts do not support, the first few days matter.

Treat this as a record-correction problem and a career-protection problem at the same time. A scattered response usually makes both worse. A disciplined response gives you the best chance to limit damage, preserve options, and put pressure on the firm to justify what it filed.

Step one is to get the actual filing

Do not work from memory or secondhand descriptions. Get the filed U5 and read it line by line.

Focus on four things first: the termination category, any disclosure yes-or-no responses, the narrative language, and the dates. I often see advisors react to the headline term, such as "permitted to resign," while missing the narrative text that creates the larger problem.

If you are already interviewing, compare the filing to what you have been telling prospective employers. Any gap needs a plan immediately.

Step two is to freeze the facts before they drift

U5 disputes are won with documents, chronology, and discipline. They are rarely won with outrage.

Build a proof file that includes:

- Separation documents: resignation notice, termination notice, severance or exit communications

- Compliance records: approvals, exception requests, supervisory emails, internal review notices

- Business records: production reports, client communications, calendar entries, call notes

- Compensation materials: promissory note demands, deferred compensation notices, forfeiture claims

- Witness list: supervisors, HR personnel, branch staff, or others present for key conversations

Create a timeline while events are still fresh. Include dates, who said what, what documents exist, and what happened next. That timeline will shape every later decision, whether you ask for a correction, add a broker comment, or file a claim.

Step three is to choose the right lane

Not every bad U5 calls for the same response. Advisors get into trouble when they either underreact to a serious accusation or overreact to a fixable drafting problem.

Use this decision tree:

Clerical or objective error

Ask for a written correction at once. Quote the exact language, identify the mistake, and attach the supporting document.Ambiguous or slanted wording

Request an amendment with proposed replacement language. Give the firm wording that is accurate, narrower, and easier to defend.Disclosure that implies misconduct or creates hiring risk

Preserve all evidence and prepare for a formal dispute if the firm does not correct it promptly. At that point, the issue is no longer just wording. It is employability.Retaliatory, false, or defamatory statement

Handle it as a litigation matter from the start. Do not send a rushed, emotional email that gives the firm your arguments before you have organized the record.

The trade-off is straightforward. An early amendment request can solve the problem faster and at lower cost, but only if the firm is willing to fix the filing. If the language was chosen to create pressure, you need to plan for resistance.

Step four is to make a targeted written demand

A good challenge letter does three jobs. It identifies the exact U5 language at issue, shows why it is inaccurate or misleading, and states the remedy sought.

Keep the tone controlled. State facts, not conclusions. Attach the documents that matter most. If there is substitute language that would fairly describe the separation, propose it. Firms are more likely to amend a filing when they can see a defensible path to doing so.

Bad demand letters usually have three flaws. They are too emotional, too vague, or too broad. If every sentence accuses the firm of bad faith, the letter stops being a correction request and starts reading like posturing.

Do not overlook the broker comment

A broker comment does not remove the disclosure, but it can help if hiring conversations are happening now and a formal challenge will take time.

Use it carefully. The best broker comments are short, factual, and drafted with the expectation that a recruiter, compliance officer, arbitrator, and future employer may all read the same text. Angry commentary usually hurts credibility. A concise statement of dispute often helps.

Know when informal efforts have run their course

Some firms will correct a U5 when shown clear proof. Others will not move without a filed case. You need to recognize the difference early.

Warning signs include refusal to explain the language used, shifting justifications, demands tied to unrelated compensation issues, or silence after you provide documents. In those cases, counsel should evaluate whether the next step is amendment negotiations, a broker comment, or a claim through the FINRA arbitration process for U5-related disputes.

Where counsel adds value

An experienced securities employment attorney does more than draft a threat letter. Counsel can separate a fixable filing error from a defamation case, preserve evidence in a way that supports later testimony, and keep the U5 dispute aligned with promissory note, compensation, non-solicit, or separation issues.

That coordination matters. Advisors sometimes solve one problem and worsen another. A quick statement to challenge the U5 can complicate a compensation claim. An aggressive settlement demand can harden the firm's position on amendment language. The right strategy accounts for all of it before the record gets harder to change.

Act quickly, but not carelessly. The goal is not to respond first. The goal is to challenge the filing with a clear record, a defensible remedy, and a plan that protects your next move.

Navigating the Path to Form U5 Expungement

An amendment changes the filing. A broker comment adds your position. Expungement is different. It is the effort to remove damaging information from the record entirely.

That is why advisors often see it as the strongest remedy. But it is also the most demanding one.

What expungement is and is not

Expungement is not a customer-service request. It is not something you obtain by sending a frustrated letter or pointing out that the language feels unfair.

It is a formal remedy pursued through the FINRA dispute process and related court procedures where required. The evidentiary burden is meaningful. You need a record that supports the relief sought.

The practical difference from other remedies

Use this comparison to keep the paths straight:

| Remedy | What it does | Best use case |

|---|---|---|

| Amendment | Changes the filed language or classification | The firm is willing to correct or narrow the record |

| Broker Comment | Adds your side to the public-facing record | You need a prompt factual response while the dispute continues |

| Expungement | Seeks removal of the challenged information | The disclosure is false, clearly erroneous, or should not remain on the record |

What makes expungement hard

The challenge is proof. Advisors often know the filing is unfair, but unfairness alone doesn't carry the case. You need a precise theory, clean documentary support, and a presentation that shows why the record should be changed at its foundation rather than merely explained.

That usually means sorting through several questions at once:

- Is the issue a false factual assertion?

- Did the firm overstate what an internal review found?

- Is there a mismatch between the alleged conduct and the wording used?

- Can the challenged language be tied to admissible proof showing it should not remain?

When expungement becomes the right target

In practice, expungement is most worth pursuing when the disclosure is likely to keep resurfacing and no negotiated fix is coming. If the problem is severe enough to undermine future hiring or permanently distort the reason for departure, a temporary explanation may not be enough.

Advisors considering that route should understand the procedure before they start. A useful overview of the forum and mechanics appears in this explanation of the FINRA arbitration process.

Clearing the record and explaining the record are not the same thing. If the filing will keep blocking opportunities, explanation may not be enough.

When to Engage a Securities Employment Attorney

A common mistake happens in the first few days after termination. An advisor sees troubling language on the Form U5, assumes the firm will fix it if asked, and sends a quick email trying to clear things up. Sometimes that works. In the cases that matter most, it often makes the record worse, locks in a bad fact pattern, or gives the firm a statement it can use later.

The practical question is not whether you are upset by the filing. The question is whether the wording creates a real career risk that calls for a controlled response.

Legal review usually makes sense early if the U5 says "discharged," suggests misconduct, refers to dishonesty, implies a compliance or supervisory failure, or appears tied to a compensation dispute, team move, or other contested exit. The same is true if the stated reason does not match resignation emails, review notes, separation paperwork, or what you were told at the time.

Signs you should get counsel involved now

- The language attacks integrity or judgment. Accusations touching fraud, truthfulness, books and records, customer harm, or policy violations can follow you into every hiring conversation.

- The timeline looks retaliatory. If the wording changed after you resigned, raised concerns, joined a competitor, or pushed back on money issues, treat that as a warning sign.

- The paper trail does not fit the story. A mismatch between the U5 and your documents usually needs a disciplined record review before anyone contacts the firm.

- Other disputes are running alongside the U5 issue. Promissory notes, deferred compensation, forfeiture claims, non-solicit allegations, or an internal investigation can affect both timing and strategy.

There is also a decision-tree problem here. Some cases call for a narrowly drafted amendment request. Some are better handled through negotiated separation terms. Others need a broker comment right away while counsel prepares for arbitration or expungement. Choosing the wrong first step can cost time, credibility, and settlement advantage.

An experienced securities employment attorney helps you decide three things quickly. First, whether the disclosure is merely unfavorable or inaccurate, misleading, or defamatory. Second, whether the better target is the language itself, the surrounding paper trail, or both. Third, whether speed matters more than completeness because you are already interviewing or trying to register elsewhere.

That early judgment matters. A rushed response can create admissions, trigger a hardened position from the firm, or turn a fixable wording dispute into a broader credibility fight.

Counsel also helps control the record. That includes reviewing draft communications, preserving key documents, identifying what should and should not be said to the firm, and aligning your U5 strategy with any compensation, transition, or regulatory issues already in play. From a career-protection standpoint, that is often more valuable than filing an aggressive demand on day one.

If you are a financial professional dealing with a complex Form U5 issue and want to discuss your business law matter, contact Kons Law at (860) 920-5181.