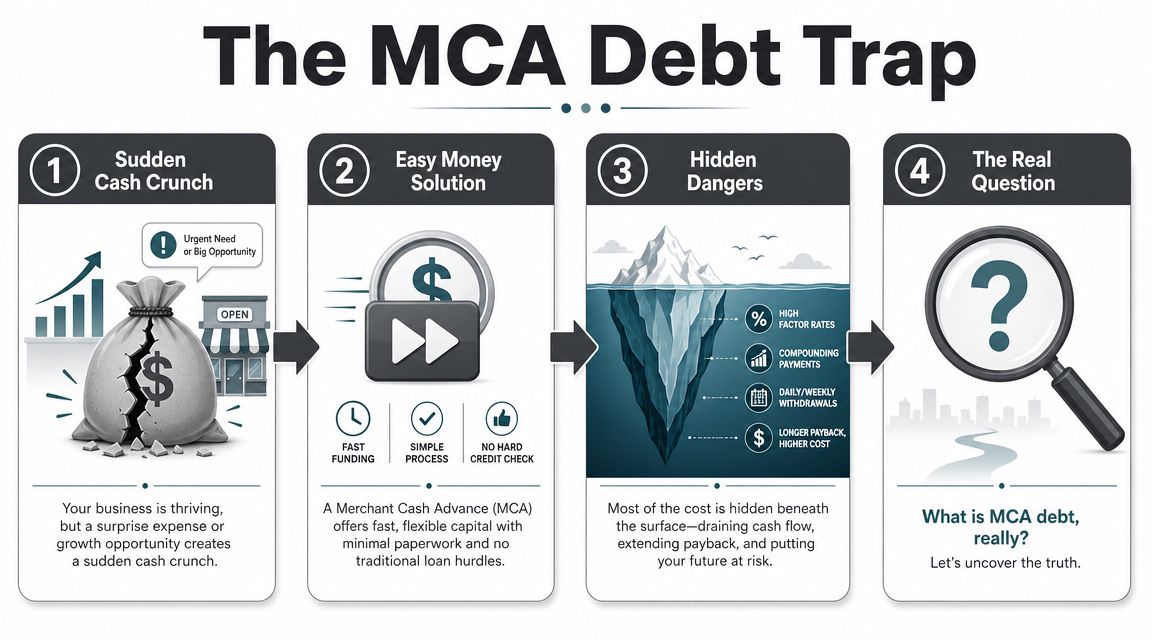

A lot of business owners ask about MCA debt only after the withdrawals have already started. Payroll is due. Inventory has to move. A tax bill lands at the wrong time. A customer pays late, or a seasonal slowdown drags on longer than expected. Then a funding company offers fast money with less friction than a bank, and the deal looks like a practical bridge.

That's usually the moment when the wrong question gets asked.

The question isn't only whether the business can get the money. The better question is what legal and financial obligations come attached to that speed, and what happens if revenue doesn't cooperate. If you're trying to understand what MCA debt is, you need more than the marketing version. You need to understand how these agreements work in real operations, how defaults happen, and what defenses may exist if enforcement begins.

The Allure of Fast Cash and the Rise of MCA Debt

A business can look healthy on paper and still hit a cash crisis. That happens all the time. A contractor lands a promising job but needs materials up front. A retailer has to buy inventory before a busy period. A restaurant replaces equipment after an unexpected breakdown. In each of those situations, waiting on a conventional underwriting process can feel impossible.

That's where merchant cash advances gain traction. The pitch is simple. Fast review, fast funding, and repayment tied to future receivables rather than a standard loan payment. For businesses that have been turned down by banks, or don't have time for a long approval cycle, that offer can sound less like a luxury and more like a lifeline.

Why the product keeps spreading

This isn't a niche corner of business finance. The U.S. MCA market has become a major small-business funding channel, with annual originations estimated at $15 billion to $20 billion, and effective APR-equivalent costs frequently cited in the 40% to 350%+ range, according to this discussion of outstanding MCA balances and market size. That combination explains why MCA debt shows up so often in business distress matters. The capital arrives quickly, but the repayment burden can tighten just as quickly.

Some industries are especially exposed because they already operate in volatile or restricted payment environments. If your revenue profile puts you in a riskier merchant category, it helps to understand the broader processing environment before taking on fast capital. This overview of understanding high-risk business classification is useful context because funding pressure and payment-processing pressure often travel together.

Many MCA problems don't begin with fraud or mismanagement. They begin with urgency.

What owners usually miss at signing

Owners often focus on the advance amount and how quickly funds can hit the account. They spend less time on the contract language that controls collection rights, default provisions, and whether the agreement will behave like a true sale of receivables or like something much closer to a loan.

That distinction matters more than most owners realize. It also sits at the center of many disputes involving enforcement and regulation. If you want more background on that legal environment, this discussion of merchant cash advance regulation is a good starting point.

How a Merchant Cash Advance Really Works

A merchant cash advance is usually framed as a purchase of future receivables, not a loan. In plain English, the funder gives the business money now and claims the right to collect an agreed amount from future sales or deposits. That legal framing is one reason MCA contracts look different from ordinary commercial loans.

The easiest analogy is this. A farmer sells part of a future harvest today for immediate cash. The buyer pays less now than the future crop may ultimately be worth. MCA providers use a similar concept with future business receipts.

The core terms that matter

The numbers that matter most are the factor rate, the holdback, and the repayment window. MCA debt is commonly repaid through a percentage of future sales over 3 to 18 months, holdback rates are often 5% to 20%, and factor rates typically fall in the 1.1 to 1.5 range, meaning a $100,000 advance can require $110,000 to $150,000 in total repayment, as described in this breakdown of MCA debt mechanics.

That structure is very different from a bank loan with a stated interest rate and amortization schedule.

Here's how those terms function in practice:

- Factor rate means the provider fixes the payback amount upfront. If the factor rate is higher, total repayment rises regardless of whether the business uses the money for one month or the full expected term.

- Holdback means the funder takes an agreed share of incoming sales or deposits. That's the part many owners feel first because it affects operating cash every day or every week.

- Repayment period tells you how compressed the obligation really is. A short repayment period increases pressure on cash flow even if the original advance seemed manageable.

How the money is collected

Repayment usually happens through one of two methods.

First, the provider may use ACH withdrawals from the business bank account. That means automatic daily or weekly pulls. In many real disputes, this is the flashpoint. The business expected payments to move with revenue, but the withdrawal pattern behaves more rigidly than expected.

Second, some arrangements use split funding or a lockbox approach. The processor or payment stream diverts a portion of receipts directly to the funder before the business receives the balance.

Practical rule: If you can't explain exactly how the withdrawals are calculated and triggered, you're not ready to sign.

Many owners also assume the “sale of receivables” label answers every legal question. It doesn't. Courts often look beyond the label and examine the actual terms, especially when the risk allocation doesn't match a genuine receivables purchase. For a more general primer on the mechanics, see how a merchant cash advance works.

The True Cost of MCA Debt Compared to Traditional Loans

The cheapest part of an MCA is often the pitch. The expensive part is the structure.

A traditional business loan usually tells you the interest rate, the payment schedule, and the maturity date in a form most owners already understand. An MCA uses different language. Instead of a familiar annual rate, you often see a factor rate and a short repayment cycle. That makes comparison harder, which is one reason owners underestimate cost.

Why the comparison gets distorted

With a bank term loan, the borrower usually sees a monthly payment spread over a longer horizon. The borrower may also have clearer disclosure around principal, interest, and maturity. An MCA compresses the repayment burden into far more frequent withdrawals and often a shorter period, so the effective cost can feel much heavier inside day-to-day operations.

The problem isn't only that MCA financing is expensive. It's that the expense interacts with business volatility. If receivables fluctuate, payroll and rent don't.

MCA vs Traditional Loan Cost Comparison

| Metric | Merchant Cash Advance (MCA) | Traditional Bank Loan |

|---|---|---|

| Legal structure | Often framed as a purchase of future receivables | Loan |

| Pricing language | Usually factor rate | Usually interest rate |

| Repayment rhythm | Often daily or weekly withdrawals | Commonly scheduled installment payments |

| Cash flow impact | Can put immediate pressure on operating cash | Usually more predictable for budgeting |

| Adjustment to sales changes | Depends heavily on contract language and actual reconciliation practices | Not tied to daily receivables in the same way |

| Litigation risk profile | Often includes aggressive enforcement clauses | Usually follows more familiar lending enforcement patterns |

What works and what doesn't

What works is comparing the obligation based on total dollars repaid, repayment frequency, and what happens in a slow month. What doesn't work is focusing only on the amount funded.

A useful internal test is simple:

- Look at timing: Faster repayment means higher pressure.

- Look at control: Automatic withdrawals reduce your room to manage a temporary dip.

- Look at contract remedies: Default terms often matter more than the sales pitch.

If a business owner tells me the advance “only costs a factor rate,” that usually means they haven't translated the deal into operational reality yet. By the time they do, the withdrawals are already affecting vendor payments, payroll timing, and tax compliance.

Hidden Dangers MCA Stacking and Aggressive Collections

The legal trouble usually starts after the second or third bad week, not on the day of funding. A business takes one advance to solve a short-term gap. The withdrawals tighten liquidity. Then another lender offers fresh money to “consolidate,” “bridge,” or “stabilize” the account. In reality, the business may just be layering new obligations on top of an already strained cash stream.

That's MCA stacking, and it's one of the clearest signs that the financing has shifted from support to distress.

Why stacking becomes dangerous fast

According to this discussion of MCA pitfalls, MCA agreements often carry short payback windows of 90 to 180 days, holdback rates of 5% to 20%, and can push businesses into stacking when revenue can't support the withdrawal pace. The same source notes that many contracts also include personal guarantees, which can shift collection exposure from the company to the owner's personal assets.

That combination changes the problem completely. The issue is no longer just expensive financing. It becomes a rolling collections problem attached to your operating account and possibly your personal balance sheet.

Operational warning signs

The businesses in the most danger usually show the same pattern:

- Payroll gets timed around withdrawals instead of ordinary revenue cycles.

- Vendor relationships fray because payment dates keep slipping.

- Taxes and rent compete with funder debits for the same dollars.

- A new advance is used to pay the last one, which rarely fixes the underlying cash issue.

If your business also struggles with payment disputes or excessive chargebacks, those problems can magnify MCA pressure because they interfere with the receivables stream the advance depends on. This resource from Disputely on chargeback issues can help owners understand that side of the problem.

Once stacked withdrawals start controlling the account, management stops making business decisions and starts making triage decisions.

What collection pressure can look like

Collection pressure varies by contract, but the practical effect is often immediate. Daily or weekly ACH pulls may continue even while the business is trying to stabilize. If there's a personal guarantee, the owner may discover that the dispute is no longer confined to the company.

You also need to think beyond the funder's own conduct. Debt enforcement is shaped by contract rights, court process, and state law. For Connecticut businesses, this overview of Connecticut debt collection laws helps frame the enforcement environment.

Your Legal Defenses Against MCA Enforcement

This is the part most general explainers leave out. When an MCA dispute reaches litigation, the central fight often isn't just whether money is owed. The core fight is what the agreement is.

If the contract is a genuine sale of future receivables, it may be treated one way. If a court decides the terms function like a loan, the analysis can change sharply. That can affect enforceability, available defenses, and whether usury arguments come into play.

Recharacterization matters

Neutral legal commentary has noted that courts can reclassify an MCA as a loan based on the agreement's actual terms, and that this can affect enforceability while opening the door to usury defenses. The same discussion explains that many owners underestimate the significance of personal guarantees and confession-of-judgment clauses in litigation, as described in this legal overview of merchant cash advance debt.

That means labels alone won't save a contract. Courts look at substance. They may ask whether the funder truly assumed risk tied to future receivables, or whether the contract instead guarantees repayment in a manner more consistent with a loan.

Clauses that deserve immediate attention

When reviewing an MCA agreement in a dispute, I'd focus early on several provisions:

- Personal guarantee language because it can expand the case from a business dispute into a personal exposure problem.

- Default triggers because some contracts define default broadly enough to accelerate the dispute before the business sees it coming.

- Forum selection terms because they can force the business to defend itself in a distant court.

- Confession-of-judgment provisions where permitted, because they can hand the funder a procedural advantage before the owner has a real chance to contest liability.

A confession of judgment deserves special attention because many owners don't understand it until enforcement begins. This explanation of what a confession of judgment is is worth reviewing if that language appears anywhere in your documents.

The strongest MCA defense often begins with contract analysis, not with an emotional argument about hardship.

Defenses aren't one size fits all

Some owners assume the only options are pay, default, or close the business. That's too narrow. In the right case, potential defenses may involve contract construction, enforceability, reconciliation language, recharacterization, notice failures, or challenges to specific collection actions.

What doesn't work is waiting until a judgment, freeze, or sweeping demand arrives and only then pulling the paperwork together. MCA litigation moves fast. If the agreement has procedural weapons built into it, delay helps the other side.

Navigating MCA Debt How Kons Law Can Help

Once a business is under MCA pressure, the objective isn't to find a magic phrase that erases the obligation. The objective is to regain control before withdrawals, defaults, and collection tactics destroy the company's operating capacity.

That usually requires a decision among several imperfect options.

The realistic paths forward

One option is negotiation. In some cases, a funder will discuss modified payment terms, especially if the alternative is a collapsing business with no practical path to full recovery. Negotiation can work when the business still has revenue, records are organized, and the owner moves early.

Another option is consolidation. As this discussion of merchant cash advance consolidation notes, stacking is a common distress signal, and owners often look to combine multiple advances into one loan with longer terms. But consolidation only helps when it improves the structure in a real way. If it merely adds another expensive layer, it can delay default rather than prevent it.

A third path is litigation defense or proactive legal intervention. That may involve reviewing whether the agreement can be challenged, assessing collection exposure, responding to aggressive demands, and negotiating from a position informed by the contract's vulnerabilities. That's where a business law firm such as Kons Law can be one practical option for contract review, dispute strategy, negotiation, and litigation defense in commercial matters.

What businesses should do first

When an owner calls about MCA trouble, the most useful first steps are usually simple:

- Gather the full contract set including guarantees, amendments, and payment authorizations.

- Map the withdrawals so you know which funder is taking what and when.

- Separate business distress from legal posture because a bad cash position doesn't automatically mean the funder's contract is airtight.

- Avoid casual admissions in panicked emails or calls. Those statements can matter later.

Owners also benefit from tightening the broader financial picture while the legal issues are being assessed. For a practical planning resource, these finance tips from ReceiptsAI can help organize the operational side of the response.

Good MCA strategy starts with triage. Stop guessing, preserve cash where you legally can, and review the papers before making the next move.

The common mistake is passivity. Owners hope revenue will improve, hope the withdrawals will become manageable, or hope the funder will be reasonable if they just explain the situation. Sometimes revenue does improve. Often it doesn't. And once enforcement rights are triggered, hope isn't a strategy.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.