When your business needs cash fast, a merchant cash advance (MCA) might seem like the perfect solution. It’s not a loan in the traditional sense. Instead, an MCA provider gives you a lump sum of cash today in exchange for a slice of your business's future sales.

Repayment happens automatically, with the provider taking a small, fixed percentage of your daily credit and debit card sales until the full amount is paid back. The biggest draw? The speed. Funds can often hit your account in as little as 24 to 48 hours.

What Exactly Is a Merchant Cash Advance?

It's easy to think of a merchant cash advance as just another type of business loan, but that's a critical mistake. An MCA operates on a completely different legal and financial foundation, and misunderstanding this can lead to serious trouble down the road.

The concept is straightforward: a finance company is buying a portion of your future revenue, not lending you money. Imagine you own a farm and need cash now to buy seeds for next season. You could sell the rights to 10% of your future harvest to an investor for immediate cash. That's essentially what an MCA is—you're selling a piece of your future sales to get working capital today.

A Sale, Not a Loan

Because this transaction is legally structured as a sale of future receivables, it sidesteps many of the state and federal laws that regulate loans, like usury laws that cap interest rates. This is a key distinction.

Instead of an interest rate, the cost of an MCA is calculated using a "factor rate"—a simple multiplier we'll break down soon. Since it's a sale and not a debt, repayment is flexible; you pay more when sales are strong and less when they're slow.

This structure is what makes MCAs so accessible. Providers care more about your daily sales volume than your FICO score, opening a door for businesses that can't qualify for a traditional bank loan. This has fueled explosive growth in the MCA market, which was valued at around $25.9 billion and is expected to nearly double to $45.0 billion.

Speed Comes at a Price

While getting funded in 24 hours is incredibly tempting, that convenience comes with a hefty price tag. The factor rates on MCAs, when converted into an Annual Percentage Rate (APR), can easily soar into the triple digits. This makes them one of the most expensive financing options on the market.

A merchant cash advance is not a debt instrument but a purchase agreement. The provider is not lending you money; they are purchasing an asset—your future sales—at a discounted price. Understanding this is the first step toward making an informed financing decision.

For business owners weighing their options, it’s vital to grasp this foundational difference. To understand the core concept in more detail, delve into this comprehensive guide explaining what is a merchant cash advance. In the following sections, we will break down exactly how repayment works and how to calculate the true cost, so you can determine if this tool is a strategic opportunity or a potential pitfall for your business.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How You Pay Back a Merchant Cash Advance

The moment that lump sum hits your bank account, the clock starts ticking on repayment. But unlike a traditional loan with a predictable monthly bill, an MCA starts taking its share of your revenue immediately and automatically. It’s relentless, so you need to know exactly how that money is going to come out of your business.

There are two main ways MCA providers get their money back: the holdback method or an Automated Clearing House (ACH) withdrawal. The method your provider uses will directly hit your daily cash flow, and understanding the difference can be the deciding factor in whether the MCA feels manageable or completely suffocating.

The Holdback Percentage Method

By far the most common structure is the holdback, sometimes called a "split." In this setup, the MCA provider links up directly with your credit card processor. Every single day, a pre-set percentage of your credit and debit card sales—usually between 10% and 20%—is automatically diverted to the MCA provider. The rest goes to you.

Think of it as a daily toll on every transaction you run. This model does have a certain built-in flexibility, which is often its biggest selling point.

- On a great day: Sales are high, so you pay back a larger amount. This helps you settle the debt faster.

- On a slow day: Sales are low, so you pay back a smaller amount, which eases the immediate pressure on your cash flow.

Because the payments rise and fall with the rhythm of your business, it can feel less painful. But don't be fooled—even a small percentage, taken every single day, adds up to a massive amount over time.

The Fixed ACH Withdrawal Method

The other route is a fixed withdrawal system using the Automated Clearing House (ACH) network. Instead of taking a percentage from your sales, the provider yanks a fixed daily or weekly amount right out of your business bank account.

While the ACH method is predictable, it completely lacks the flexibility of a holdback. That fixed payment is coming out whether you made a killing or sold absolutely nothing, creating a serious cash flow crisis during slow periods.

Let’s put this in real-world terms. Imagine a local Connecticut coffee shop gets an MCA.

- Scenario 1 (Holdback): They agree to a 15% holdback. On a busy Saturday, they make $3,000 in card sales and repay $450. On a slow Tuesday, they only do $800 in sales, so they repay just $120.

- Scenario 2 (Fixed ACH): The agreement calls for a fixed $300 daily payment. That Saturday, $300 is no problem. But on that slow Tuesday, that same $300 represents a huge chunk of their revenue, potentially leaving them short for payroll or inventory.

This rigid structure is a critical legal and financial distinction. The agreement authorizing these withdrawals is a binding financial instrument, often containing language you might see in other contracts. It's vital to grasp the commitment you're making. For more context on the legal nature of these payment promises, you can read about what is a promissory note and its function.

Before you sign anything, you absolutely must know which repayment method is being used and model out how it will impact your business’s financial health, day in and day out.

The Real Cost of a Merchant Cash Advance

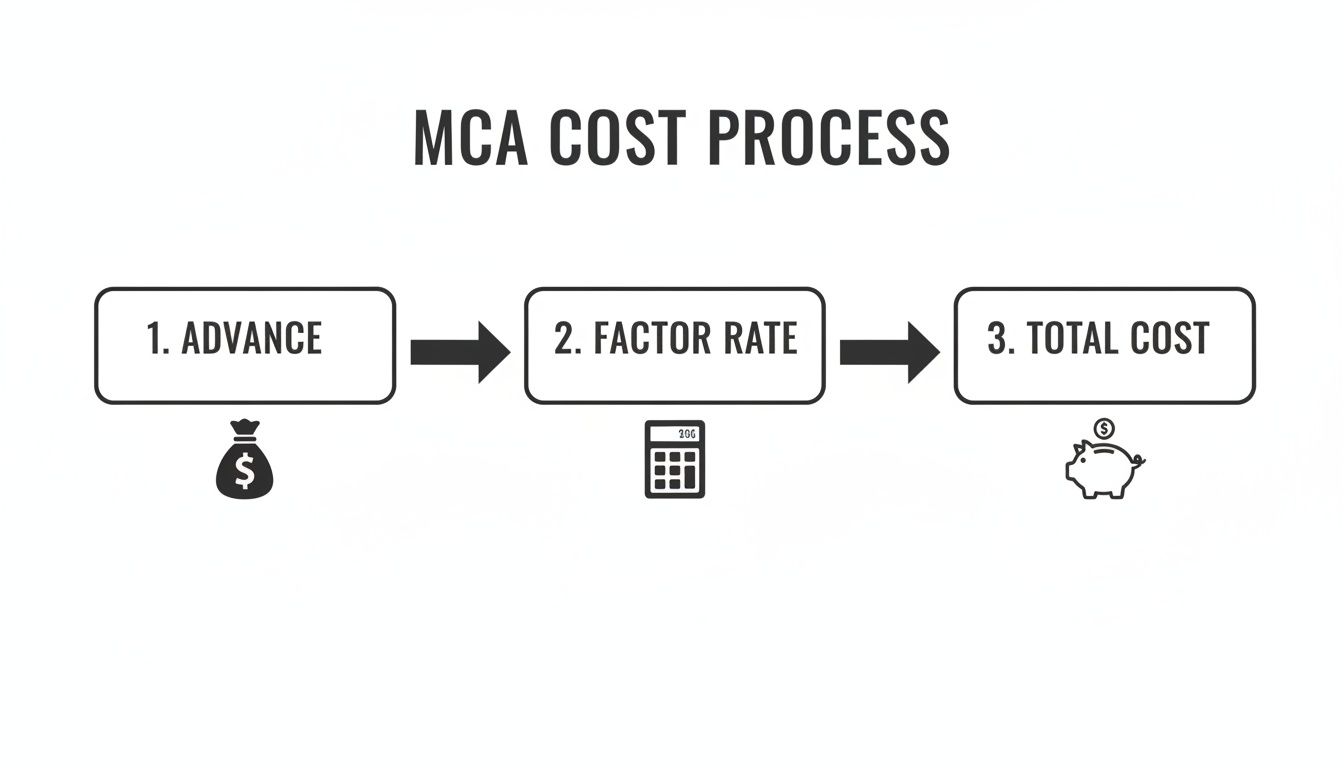

The biggest selling point of a merchant cash advance is speed. But that convenience comes at a price—often a shockingly high one. To really understand what you’re signing up for, you have to look past the upfront cash and calculate the true cost. It all starts with the factor rate.

Instead of a traditional interest rate, MCA providers use a factor rate, which is just a simple multiplier. You’ll usually see it expressed as a decimal, like 1.2, 1.35, or even 1.5. To figure out what you owe, you just multiply the advance amount by that number.

Let’s say you get a $20,000 advance with a factor rate of 1.3. The math is simple:

- Advance Amount: $20,000

- Factor Rate: 1.3

- Total Repayment: $20,000 x 1.3 = $26,000

Here, the cost of the financing is $6,000. That seems straightforward, but the factor rate is designed to be misleading. It cleverly hides the one number that actually matters for comparing financing options: the Annual Percentage Rate (APR).

The Deceptive Simplicity of the Factor Rate

A factor rate tells you what you'll repay, but it conveniently leaves out how fast. The speed of repayment is the hidden key that unlocks the true cost of an MCA. Since these advances are typically paid back over just a few months, that seemingly innocent factor rate balloons into a dangerously high APR.

This is a huge deal for small businesses, which make up an estimated 94% of the entire merchant cash advance market in the United States. That number alone shows just how many businesses are turning to MCAs because traditional banks won't fill the funding gap. If you want to dig deeper into this trend, you can explore the full market research.

From Factor Rate to Triple-Digit APR

Let's unpack how that $6,000 cost on a $20,000 advance gets so out of control. We’ll assume you have six months (180 days) to repay it.

- Total Cost: $6,000

- Repayment Period: 6 months

At a glance, a 30% cost over six months might seem steep but maybe manageable. The problem is, that's not the whole story. When you annualize it, the picture gets ugly fast. Because you paid that 30% fee in just half a year, the effective APR is roughly double, or 60%. If the repayment term was only three months, that APR would launch well into triple-digit territory.

The real danger of an MCA is the disconnect between the simple factor rate on the contract and the brutal reality of its APR. A short repayment window acts like a powerful amplifier, turning what looks like a reasonable fee into a rate that can suffocate a business's cash flow.

To see this clearly, you have to get your hands dirty with your own financial data. The best way to calculate the true cost is to map out your daily payments and see the impact for yourself. Learning how to convert bank statements into Excel for detailed analysis is a practical skill that gives you the power to model these scenarios before you sign anything. It’s the single most important step in figuring out if an MCA is a helpful tool or a devastating financial trap.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

The Legal Landmines Buried in MCA Agreements

Beyond the sky-high costs, a merchant cash advance agreement is a serious contract. It's loaded with clauses that can have devastating consequences for both your business and your personal finances. These aren't your standard loan documents; they are highly specialized commercial contracts drafted to give the funding company all the power.

It's a classic mistake: a business owner, desperate for quick cash, skims the fine print and signs on the dotted line. This can be a catastrophe. Clauses buried deep in the agreement can waive your legal rights, put your family's assets on the line, and block you from getting other financing down the road. You have to approach any MCA contract with extreme caution and professional scrutiny.

This visual shows the simple but often painful math behind an MCA's true price tag.

As the infographic shows, the advance you receive is multiplied by a factor rate to determine your total repayment. It's a formula that masterfully conceals the astronomical effective APR.

The Confession of Judgment: A Dangerous Shortcut

One of the most treacherous clauses you might find in an MCA agreement is the Confession of Judgment (COJ). In simple terms, this is a pre-signed confession that you've defaulted—before any default has even happened. If the MCA provider merely claims you've breached the contract, they can file this COJ in court and get a legal judgment against you instantly. No trial, no hearing, not even a notification.

This legal weapon allows the funder to skip the entire court process. Once they have that judgment, they can immediately start aggressive collection actions like freezing your bank accounts, seizing business assets, and putting liens on your property.

A Confession of Judgment is a complete surrender of your right to defend yourself in court. It hands the MCA company the power of judge and jury, letting them declare a default and begin collections without due process.

For any business owner in Connecticut, it's vital to understand what this clause really means. To learn more about the specifics of how this works, it’s critical to understand what is a Confession of Judgment and its legal implications.

Your Personal Assets Are on the Line

Another standard feature of MCA agreements is a personal guarantee. When you sign it, you are personally promising to repay every last cent if your business can't. This clause pierces the "corporate veil" that normally shields your personal assets from business debts.

What does this mean in the real world? If your business revenue slows down and you fall behind on payments, the MCA provider won't just go after your business. They'll come after you.

- Your Home: A lien could be placed on your house, putting it at risk.

- Your Savings: Your personal and family bank accounts can be frozen and garnished.

- Your Car: Your vehicle and other personal property could be seized to cover the debt.

The personal guarantee turns what seems like a business transaction into a huge personal risk. MCA funders almost always demand it because it shifts all the risk onto you, making your personal wealth their ultimate collateral.

The Impact of UCC-1 Liens

When you sign an MCA contract, you are almost certainly giving the funder permission to file a UCC-1 financing statement. This is a public legal notice that puts a lien on your business assets, giving the funder a security interest in your company.

This UCC-1 lien establishes the MCA provider's priority as a creditor. If your business were to fail or file for bankruptcy, they get paid first from the sale of your assets—your accounts receivable, inventory, and equipment.

Even more damaging, a UCC-1 lien can choke off your access to other funding. Banks and traditional lenders will see this lien during their background checks and will almost certainly deny you a loan, as they don't want to be second in line behind an MCA company. This can trap your business in a cycle, forcing you to rely on more expensive MCAs because healthier options are no longer on the table.

Navigating the complex legal language of these agreements requires expertise. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Spotting Predatory MCA Lenders and Red Flags

An MCA can feel like a lifeline, offering a quick injection of cash when you need it most. But this corner of the lending world isn’t uniformly regulated, meaning the space is crowded with both reputable funders and outright predators. Knowing how to tell them apart is absolutely essential to protecting your business.

A predatory agreement isn’t just expensive—it’s a trap. These contracts are often designed to lock you into a cycle of debt that becomes nearly impossible to escape. The only way to stay safe is to do your homework. Predatory lenders thrive on panic and confusion, banking on the idea that a business owner’s desperation for capital will make them overlook the fine print. Spotting the red flags is your best line of defense.

Transparency Is Non-Negotiable

A good MCA provider will be completely upfront about their terms and costs. A predatory one will hide behind jargon, high-pressure tactics, and a frustrating refusal to answer straight questions. If a funder can’t give you a clear, simple answer, it’s time to walk away.

Here are a few tell-tale signs of a transparency problem:

- Dodging the APR Question: They’ll talk all day about the factor rate but clam up when you ask about the Annual Percentage Rate (APR). If you ask for the effective APR and they can't—or won't—provide it, that’s a massive red flag.

- Confusing Contract Language: The agreement is a maze of dense legal terminology, vague definitions, and clauses that make your head spin. This is almost always intentional, designed to hide nasty surprises like a Confession of Judgment or an iron-clad personal guarantee.

- High-Pressure Sales Tactics: You’re being rushed to sign right now with talk of a "limited-time offer" that’s about to disappear. Legitimate funders will always give you the time you need to have your lawyer review the contract.

Do Your Homework on the Provider's Reputation

The contract itself is only half the story; the provider's reputation speaks volumes. A few minutes of online research can save you from months or even years of financial misery. This is especially true in industries like retail and e-commerce, where MCAs are common for managing fluctuating cash flow for inventory and marketing. You can explore the market research on Allied Market Research to learn more about this trend.

Before you sign anything, run these simple checks:

- Check Online Reviews: Look them up on the Better Business Bureau (BBB), Trustpilot, and other independent review sites. Pay close attention to complaints about hidden fees, aggressive collection tactics, or radio silence after the contract is signed.

- Ask for References: A reputable provider should be happy to connect you with other business owners they’ve worked with. If they refuse, that’s a bad sign.

A personal guarantee is a standard part of most MCA agreements, but the terms can be wildly different. You need to understand exactly what you're on the hook for. To get a better handle on the legal side, read our guide on what is a guaranty agreement to protect your personal assets. These agreements are complicated; if you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Smarter Alternatives to Merchant Cash Advances

When cash is tight and you need it yesterday, a merchant cash advance can feel like the only game in town. The reality, though, is that their eye-watering costs and relentless repayment schedules often dig a deeper hole than the one you were trying to fill.

The good news? There are much healthier, more sustainable ways to finance your business. It's all about knowing your options and choosing a path that supports long-term growth, not just a short-term fix.

Business Line of Credit

Think of a business line of credit as a financial safety net. It’s a fantastic tool for handling the unpredictable ups and downs of business. Instead of getting a lump sum of cash you have to start repaying immediately, you get access to a pool of funds you can draw from whenever you need it.

You only pay interest on the money you actually use, which makes it perfect for covering payroll during a slow patch or grabbing a great deal on inventory. It gives you incredible flexibility without locking you into the kind of aggressive, daily repayment plan that comes with an MCA.

A business line of credit is all about control. It’s revolving capital that’s there when you need it, offering far more breathing room and lower costs than the daily drain of a merchant cash advance.

Traditional Term Loans

For big, planned investments—think new equipment, a major renovation, or expanding to a second location—a traditional term loan from a bank or reputable online lender is almost always your best bet. Yes, the application process is more involved than getting an MCA, but the payoff is huge.

Term loans offer predictable, fixed monthly payments and much, much lower interest rates, all laid out in a clear APR. This stability makes budgeting a breeze and protects your daily cash flow from being siphoned away. While you’ll need a solid credit history, the favorable terms make it the smartest move for established businesses planning for the future.

Invoice Factoring

Is your biggest headache waiting for customers to pay their invoices? If slow-paying clients are strangling your cash flow, invoice factoring can be a game-changer. Instead of selling a piece of your future sales, you’re selling your existing unpaid invoices to a factoring company at a small discount.

Here's how it works: the factor gives you a big chunk of the invoice value—often 80% to 90%—right away. They then take over collecting the full payment from your customer. Once your customer pays up, the factor sends you the rest of the money, minus their fee. It's a brilliant way to unlock the cash you've already earned without taking on new debt. For many businesses, it's a vital tool, and you can learn more by reading our guide on how to collect unpaid invoices.

Choosing the right financing is one of the most important decisions you'll make. Before you get pulled in by the promise of fast cash from an MCA, take a hard look at these smarter alternatives. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Clearing Up the Confusion: Your MCA Questions Answered

When you're looking into a merchant cash advance, it's natural to have questions. The way these agreements are structured is unconventional, and the financial and legal details can get complicated quickly. Let's tackle some of the most common questions business owners ask when they're trying to figure out if an MCA is the right move.

So, is an MCA Just a Fancy Name for a Loan?

Not at all, and this is probably the single most important thing to understand. An MCA is legally defined as the sale of future receivables. Think of it this way: the funding company isn't lending you money; they are buying a piece of your future revenue, right now, at a discount.

This distinction is what allows MCAs to exist outside of traditional lending laws. Because they aren’t classified as loans, they don't have to follow state usury laws that put a cap on interest rates. It’s the reason an MCA’s effective APR can skyrocket into the triple digits without breaking the law. Getting your head around this legal setup is the first step to truly understanding the risks you’re taking on.

What Happens if Business Dries Up and My Sales Tank?

This is where the fine print of your agreement really matters. Your contract will specify one of two repayment methods:

- Percentage Holdback: If your MCA is set up this way, a fixed percentage of your daily credit card sales is automatically sent to the funder. When sales are down, your payment is smaller. If you have a great day, the payment is larger. This structure has a built-in flexibility that can help you weather a slow spell.

- Fixed ACH Withdrawal: The alternative is a fixed daily or weekly payment pulled directly from your bank account via ACH. This amount stays the same no matter what. If your sales suddenly drop, that payment is still coming out, which can drain your bank account and push your business into a serious cash-flow crisis.

Be absolutely certain you know which repayment method is in your contract before you sign. A fixed withdrawal structure puts all the risk of a sales slump squarely on your shoulders.

I Already Have an MCA. Can I Get Another One?

You can, but it’s a practice called “stacking,” and it's one of the fastest ways to put your business in jeopardy. Juggling two MCA payments at once can create a devastating financial vortex. The combined daily withdrawals can eat up so much of your revenue that you're left without enough cash to cover basic operational costs like rent or payroll.

On top of that, almost every MCA agreement includes a clause that forbids you from taking on additional advances. If you violate that term, you’ll likely trigger an immediate default on your first MCA, opening the door to aggressive collection tactics and serious legal trouble. Stacking is a high-risk gamble that often leads businesses to failure. It’s a path you want to avoid.

The aggressive terms and complex nature of MCA contracts mean you shouldn't navigate them alone. If you're facing issues with an MCA or need advice on your business's legal options, contact Kons Law at (860) 920-5181 to discuss your situation.