A Connecticut business owner usually meets merchant cash advance regulation at the worst possible moment. Revenue is tight, payroll is close, equipment just failed, or inventory has to be purchased before a busy stretch. A funder offers fast capital, the documents arrive electronically, and the deal language looks nothing like a bank loan. Instead of interest, there's a factor rate. Instead of monthly payments, there's a daily sweep of receivables. Instead of familiar lending disclosures, there's a contract built around the sale of future revenue.

That speed is exactly why MCA products remain attractive. It's also why disputes happen. Merchants often sign before they fully understand the repayment mechanics, and funders sometimes rely on forms or collection tactics that no longer fit the current enforcement climate. If you're trying to understand if merchant cash advances are legal, the short answer is yes in many situations, but legality depends heavily on how the transaction is structured, disclosed, and enforced.

Merchant cash advance regulation is no longer a niche issue. It now sits at the intersection of contract law, commercial law, disclosure rules, licensing rules in some states, federal scrutiny, and state enforcement trends that can turn a profitable transaction into litigation. In Connecticut, that patchwork matters even more because parties often assume they can use forms and remedies developed for New York or other jurisdictions without adjusting for local law.

The Growing Need for MCA Regulatory Clarity

A Hartford restaurant owner with a broken walk-in cooler doesn't have time for a traditional underwriting cycle. The owner needs capital quickly or starts losing product, customers, and staff confidence. An MCA provider may be able to fund fast, sometimes with lighter underwriting than a bank. The problem is that urgency tends to compress legal review.

That's where confusion starts. Many businesses don't realize they are not signing a conventional loan agreement. They are signing a receivables purchase contract that may still carry major legal risk if the drafting, disclosures, or collection provisions are flawed.

Why the old gray area is shrinking

For years, the industry operated with limited oversight because MCA providers argued these transactions were commercial purchases rather than loans. That distinction still matters, but the regulatory environment has tightened. States have imposed disclosure requirements, some have added registration or licensing obligations, and federal agencies have increased scrutiny of fees, practices, and reporting obligations.

The practical takeaway is straightforward. A business can't treat an MCA as “just another contract,” and a funder can't assume older templates are still safe.

Practical rule: Fast funding doesn't reduce legal risk. It often increases it because everyone is moving before the paper has been tested.

Who needs clarity right now

Two groups need a sharper understanding of merchant cash advance regulation.

- Merchants under pressure: They need to know the true repayment burden, what triggers default, whether remittances in fact adjust with sales, and what remedies the funder can use if revenue drops.

- Funders and brokers: They need to know whether the agreement will hold up in court, whether the transaction could be recharacterized as a loan, and whether their disclosures and collection strategy fit the states where they operate.

Connecticut sits in an important middle position. It is not a state where parties can ignore commercial law principles and assume contract language alone will save the deal. Courts and regulators look at substance, not just labels. That makes careful drafting and practical compliance more valuable than aggressive papering.

Understanding the Mechanics of a Merchant Cash Advance

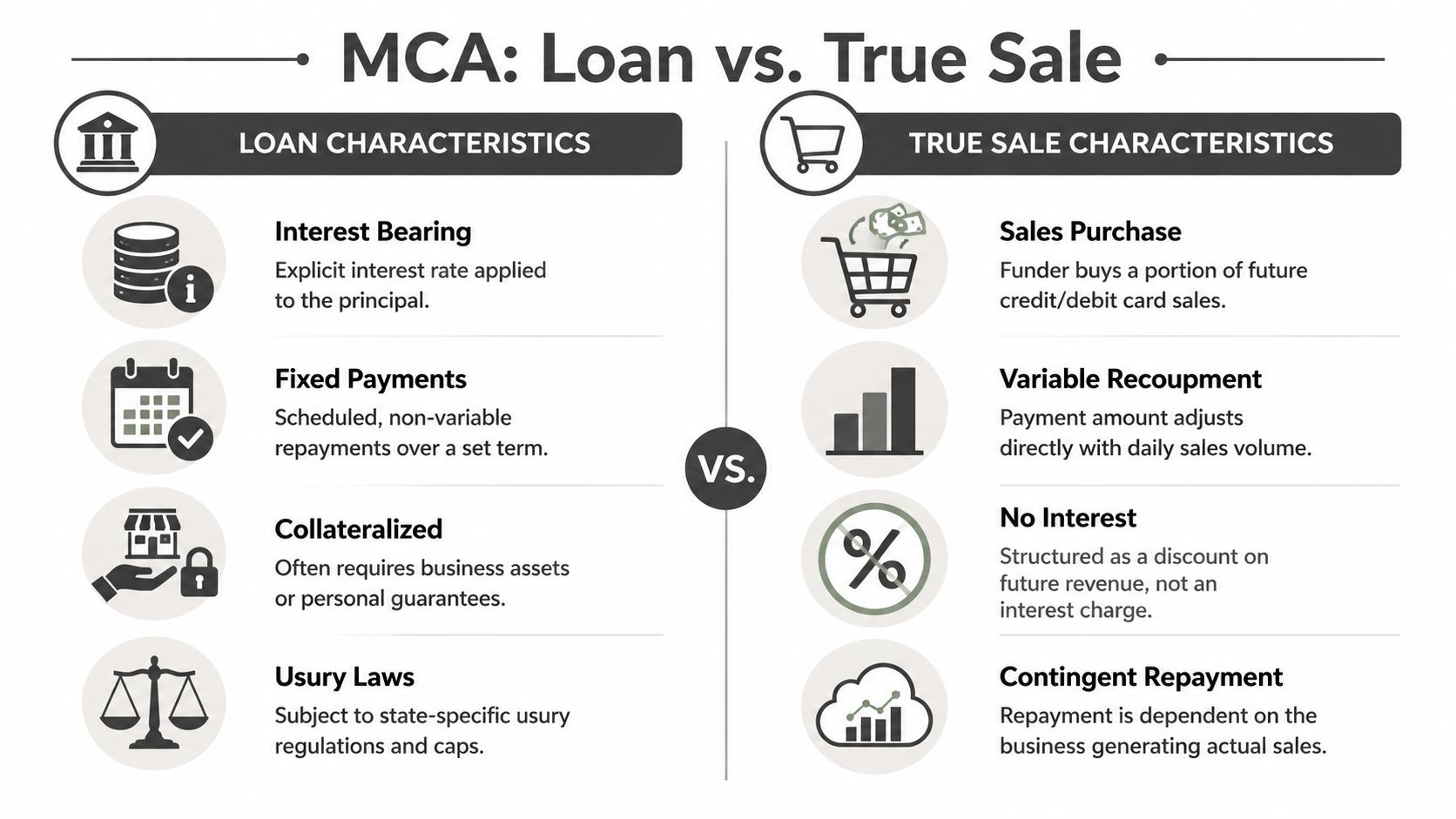

A merchant cash advance is usually framed as a purchase of future receivables. The funder gives a business money now and buys a specified amount of future revenue at a discount. That's why the contract uses terms like advance amount, purchased amount, and holdback, rather than principal and interest.

The product is large and widely used. The U.S. market is valued at approximately $22 billion, yet 46% of merchants cite limited transparency in funding terms and 28% report difficulty managing high daily repayment deductions, according to Ken Research's U.S. merchant cash advance market analysis. Size hasn't solved the core communication problem.

The three numbers that matter most

When I review these agreements, I start with three figures.

| Contract term | What it means | Why it matters |

|---|---|---|

| Advance amount | The money the business receives upfront | This is the cash available to solve the immediate problem |

| Factor rate | The multiplier used to calculate total repayment | It fixes the purchased amount owed regardless of early payoff in many deals |

| Holdback | The share of receivables remitted to the funder | It drives day-to-day cash flow strain |

A simple way to think about it is a crop sale. A farmer sells part of a future harvest at a discount to get cash now. If the harvest comes in slowly, the buyer collects slowly. If the crop performs well, the buyer collects faster. In a true MCA, repayment should rise and fall with actual sales performance.

Why businesses get tripped up

The confusion usually comes from the factor rate. A factor rate tells you the total payback, but it doesn't function like an annual interest rate. That makes side-by-side comparison with bank financing difficult, especially when the remittance is daily or weekly and cash flow is already uneven.

A second issue is operational, not legal. The deduction may be automated, but that doesn't make it painless. A business with volatile revenue can handle a percentage remittance in theory and still struggle in practice when the account is swept during a slow stretch.

For a plain-language primer on deal structure, this explanation of how merchant cash advance work is a useful companion to the legal analysis.

A good MCA contract should let a business answer one basic question without a calculator: what am I receiving, what am I selling, and what happens when sales fall?

What works and what doesn't

Effective transactions track revenue and clearly inform merchants how remittances are calculated and adjusted.

What doesn't work is paperwork that uses the language of a sale while operating like a fixed-payment loan in practice. That gap is where litigation usually starts.

The Critical Legal Test Loan Versus True Sale

The central legal question in many MCA disputes is simple to state and hard to litigate. Is the transaction a true sale of receivables, or is it really a disguised loan?

That distinction decides whether a court treats the deal under general commercial contract principles or subjects it to lending rules and usury analysis. Labels alone won't control the outcome. Courts look at the actual allocation of risk.

What courts tend to examine

The strongest MCA agreements preserve uncertainty. The funder's collection depends on future sales, and the merchant's remittances should move with those sales. If the merchant has a bad month, the remittance should reflect that. If the business fails, the funder bears real transactional risk.

By contrast, a deal starts to look like a loan when repayment is effectively guaranteed no matter what happens to revenue.

According to SoFi's discussion of merchant cash advance regulations, factor rates commonly range from 1.1 to 1.5, and a $10,000 advance with a 1.4 factor rate produces a $4,000 cost that can equate to about a 78% APR over 12 months. That cost level becomes legally dangerous when the deal isn't strictly tied to variable sales.

Red flags that increase recharacterization risk

A contract is more vulnerable when several of these features appear together:

- Fixed remittance behavior: The paper may say remittances are sales-based, but the actual ACH pull looks fixed and doesn't adjust in a meaningful way.

- Weak or unusable reconciliation rights: If the merchant technically has a right to request adjustment but the process is impractical, delayed, or discretionary, the clause may not help much.

- Absolute repayment expectations: Language that strongly implies the purchased amount will be repaid on a set schedule, regardless of sales performance, can undercut the “true sale” position.

- Recourse that wipes out funder risk: Broad personal guarantees or default triggers tied to ordinary business downturns can make the arrangement look less like a purchase and more like debt.

A practical contract review lens

When I assess exposure, I don't ask whether the agreement says “purchase” fifty times. I ask whether the economics and remedies match the label.

| Question | Lower risk answer | Higher risk answer |

|---|---|---|

| Does remittance vary with sales? | Yes, in operation and in drafting | Not really, or only on paper |

| Is reconciliation workable? | Clear, prompt, objective | Burdensome, narrow, discretionary |

| Does the funder bear downside risk? | Yes, if sales decline | Minimal risk because payment is effectively fixed |

| Are remedies consistent with a sale? | Focused on receivables rights | Broad remedies that resemble loan enforcement |

For businesses signing electronically, execution discipline matters too. If the platform workflow, assent language, or record retention is sloppy, enforcement fights become more expensive. This ESIGN Act and UETA compliance guide is helpful for understanding how electronic signatures hold up when deal documents are challenged.

A related mistake is using a loan document as a shortcut. If the transaction is supposed to be a receivables purchase, importing debt-language from a promissory note form can create avoidable inconsistency.

If the funder gets paid the same way in a bad sales month as in a strong sales month, the contract may say “sale,” but a judge may see “loan.”

Mapping The New Federal and State Regulatory Framework

Merchant cash advance regulation now turns on three recurring themes. Disclosure, registration or licensing, and data or enforcement oversight. Once you organize the legal environment that way, the patchwork makes more sense.

Disclosure is no longer optional in key markets

States moved first by requiring providers to tell businesses more about pricing and repayment structure. New York adopted a disclosure law in January 2022 for certain commercial financing transactions under $500,000, according to Credible Law's merchant cash advance industry report. The broader point is that state regulators no longer accept the view that business borrowers need little or no pricing transparency because the product is commercial.

Disclosure rules matter beyond the form itself. Once a provider commits to a description of holdbacks, fees, and estimated cost, that disclosure becomes part of the litigation record if the merchant later claims deception.

Registration and licensing are spreading

Utah and Virginia went further. They require certain providers to disclose terms and also register or obtain state licenses, applying to providers that complete more than five commercial financing transactions annually, as described in the same Credible Law report. That creates a major operational issue for national funders. A provider cannot rely on one compliance approach across every jurisdiction.

Here's the practical split:

- Disclosure-focused states: These states want standardized cost information in front of the merchant before closing.

- Registration-focused states: These states also want to know who is in the market and whether providers meet administrative requirements.

- General enforcement states: Even without a dedicated MCA statute, attorneys general and courts may still police deceptive or abusive conduct through existing laws.

Federal oversight is now part of the risk analysis

At the federal level, the industry no longer sits outside serious agency attention. The CFPB launched investigations in 2024 targeting MCA practices and disclosure of terms and fees, and the FTC pursues legal action against providers engaging in deceptive or predatory practices, according to Credible Law's report. Section 1071 of the Dodd-Frank Act also requires certain covered financial institutions to collect and report small business credit application data.

That changes boardroom conversations. A funder's exposure isn't limited to private lawsuits brought by merchants. It may include agency scrutiny of sales practices, forms, recordkeeping, and reporting procedures.

Operational takeaway: Compliance isn't a single document. It's a system that connects origination, disclosures, underwriting, servicing, complaints, and collections.

For merchants, these developments help, but they don't replace contract review. Better disclosure rules improve visibility. They don't make a bad deal affordable.

Enforcement Trends And Specifics of Connecticut Law

Connecticut businesses often assume MCA risk is mostly about pricing. In practice, the bigger legal problem is often enforcement. A contract can be expensive and still enforceable. A contract can also become difficult to collect if the remedies overreach, the structure is inconsistent, or the chosen enforcement tools are no longer available.

Connecticut changed the collections equation

In 2025, Connecticut adopted UCC-aligned safeguards that prohibit absolute Confessions of Judgment in MCA contracts, according to OnyxIQ's analysis of lending regulation and MCA enforcement. The same source reports that courts invalidated 25% of COJ enforcements between 2024 and 2026. For funders, that means a shortcut many in the industry once relied on is no longer a dependable collection device.

Confessions of judgment provide creditors with an expedited path to legal rulings, often leaving merchants with little chance to mount a defense before aggressive collection actions begin. When this legal tool is restricted, the fundamental economics of debt enforcement shift instantly.

Why proactive compliance costs less than litigation

A funder using outdated forms now faces a stack of avoidable problems:

- The contract may trigger a recharacterization fight if the receivables purchase structure isn't credible.

- The remedy package may be partially unenforceable if it depends on prohibited or heavily disfavored provisions.

- Collections may move into ordinary litigation, which takes more time, more documentation, and more disciplined pleading.

For merchants, Connecticut's approach provides an advantage, but not immunity. A weak MCA agreement can still lead to suit, account restraints through lawful means, and expensive business disruption. The safest approach is still to challenge risky terms before signing, not after default.

A funder that operates in Connecticut should also revisit how it uses UCC tools. Filing on receivables may remain part of a legitimate secured strategy, but the paperwork and enforcement theory must line up with the actual transaction. If counsel is handling post-default recovery, the framework should fit Connecticut's current creditor rights law landscape, not a generic nationwide playbook.

What changes in practice

I'd summarize the Connecticut position this way.

| Issue | Older industry instinct | Better Connecticut approach |

|---|---|---|

| Collection leverage | Use aggressive judgment shortcuts | Prepare for ordinary litigation and defensible commercial remedies |

| Contract drafting | Import broad national templates | Tailor forms to Connecticut law and the actual revenue model |

| Risk management | Focus on closing speed | Focus on enforceability and records |

A contract that looks tough on paper may be worth less than a narrower agreement that a Connecticut court will actually enforce.

That's the key lesson. In a tighter regulatory market, aggressive drafting often creates less advantage, not more.

Compliance Best Practices For Funders and Merchants

The most useful compliance advice is usually boring. Clear drafting. Clean disclosures. Consistent servicing. Good records. Merchant cash advance regulation punishes shortcuts more than complexity.

If you want a broader business-side frame for how companies handle industry regulations, this overview of how companies handle industry regulations is a practical reminder that compliance succeeds when it becomes an operating process rather than a one-time legal memo.

Checklist for funders

Funders should pressure-test the agreement before it ever reaches a merchant.

- Draft for actual variable remittance: If remittances are supposed to track sales, make sure the servicing process can do that. Don't rely on a theoretical reconciliation clause that operations can't administer.

- Use plain disclosure language: Even where a statute doesn't mandate a particular form, explain the purchased amount, remittance method, default triggers, and any fees in direct terms.

- Audit state-by-state obligations: A national product needs a jurisdiction matrix. Registration, licensing, disclosure format, and collection restrictions differ across states.

- Keep complete servicing records: Save remittance histories, reconciliation requests, notices, and underwriting materials. If litigation starts, missing records weaken both enforcement and defense.

- Review broker practices: A compliant contract can still lead to trouble if a broker overpromises, misstates terms, or markets the product like a low-cost loan.

Checklist for merchants

Merchants should review an MCA agreement as a cash-flow instrument first and a legal document second. Both matter, but cash pressure is what usually causes default.

- Pin down total repayment. Ask what amount has been sold and how the remittance is collected.

- Ask how adjustments work. If sales decline, what is the process for reducing the remittance, who decides, and how quickly?

- Read every default trigger. Some agreements define default far beyond missed remittances.

- Review guarantee language carefully. Personal exposure can expand the practical risk far beyond the business itself.

- Confirm provider compliance where required. In states with registration or licensing rules, don't skip that step.

What strong compliance looks like

A good MCA file should show coherence. The marketing should match the contract. The contract should match the servicing reality. The servicing reality should match the collection theory.

For both sides, this is easier when someone is responsible for compliance as a function, not as an afterthought. Businesses dealing with sales-based financing issues often benefit from reviewing their broader regulatory compliance obligations at the same time, especially if financing intersects with ongoing commercial operations, vendor contracts, or collections activity.

Strong compliance doesn't make every dispute disappear. It gives you better facts, better documents, and better options when one arrives.

Mitigating Risk And Moving Forward In A Regulated Market

The MCA market is still active, still useful, and still capable of solving urgent business cash needs. It is not a legal free-for-all anymore. That's the most important shift.

For merchants, the lesson is to stop treating speed as the only metric. Quick funding can be worth the cost in the right situation, but only if the remittance structure is understood, the reconciliation rights are real, and the enforcement provisions are tolerable under the law that will apply. A business under pressure needs clarity more than optimism.

For funders, the message is even sharper. Old assumptions about minimal oversight, aggressive forms, and one-size-fits-all collections are no longer safe. The better approach is disciplined product design, state-specific review, documented servicing practices, and a litigation strategy built around enforceability rather than intimidation.

Connecticut adds a distinctive wrinkle because it illustrates how local law can change the value of remedies overnight. If a collection tool is prohibited or disfavored, it doesn't matter how often it worked in another jurisdiction. The paper has to fit the forum. The same is true of disclosures, signature process, UCC strategy, and default administration.

Good MCA practice now comes down to alignment. The structure must match the business reality. The contract must match the structure. The disclosures must match the contract. The enforcement plan must match the governing law.

That isn't just a compliance preference. It's what keeps a financing transaction from turning into a lawsuit that costs more than the advance solved.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.