A Connecticut creditor often reaches the same frustrating point. You did the work, filed the case, obtained the judgment, and still haven't been paid. The debtor may be employed, but voluntary payments never arrive or stop after a few weeks. At that stage, a paper judgment isn't enough. You need an enforcement tool that reaches actual income.

In Connecticut, that tool is usually called a wage execution, even though many business owners search for it as CT wage garnishment. It is one of the most practical post-judgment remedies because it puts collection into a formal payroll process instead of relying on promises. But it only works well when the creditor, the levying officer, and the employer all follow the rules precisely.

What trips people up is that Connecticut doesn't operate on the federal baseline alone. The state uses its own wage-execution formula for many ordinary judgment debts, has a service-and-notice process that matters, and gives debtors a limited window to raise exemptions or hardship issues. Employers also have their own compliance obligations, and those obligations are easy to mishandle if payroll treats the order like a generic deduction.

A good collection strategy doesn't ignore those realities. It accounts for the withholding limits, the order in which executions are paid, the marshal's role, and the possibility that the employee may challenge the amount before money starts moving.

Introduction

If you're holding an unpaid Connecticut judgment right now, you're probably dealing with a practical problem, not a legal theory problem. You already proved the debt. The question is how to convert that judgment into payment without wasting more time and money on collection steps that don't produce results.

For many creditors, CT wage garnishment is the most dependable route when the debtor has regular employment. A bank execution may hit an empty account. A property lien may sit for a long time. A wage execution, by contrast, can create recurring payments through payroll once the process is in place.

That doesn't mean wage collection is automatic. Connecticut uses a formal post-judgment system with service requirements, waiting periods, employer duties, and debtor defenses. If any part is handled loosely, collection slows down or gets challenged. If it's handled correctly, wage execution can become a disciplined recovery method rather than a series of ad hoc collection attempts.

Practical rule: A judgment is leverage. A properly executed wage execution is enforcement.

Business owners and creditors also need a balanced understanding of the process. Many articles focus only on how to start garnishment. In real practice, you also need to understand why withholding may be delayed, reduced, or contested. That matters because collection strategy improves when you anticipate objections instead of reacting to them after payroll has already been served.

The rest of this guide stays focused on what matters in practice. That includes the legal framework, the withholding limits, the enforcement path from judgment to payment, the employer's role, and the debtor's options to seek relief.

Connecticut's Legal Framework for Wage Garnishment

A creditor may have a valid Connecticut judgment and still collect nothing from payroll if the wrong procedure is used. I see that mistake most often when someone assumes the federal cap answers the whole question. It does not. In Connecticut, wage collection is governed by both federal garnishment limits and a separate state wage-execution process, and the state procedure is where many delays, objections, and reductions occur.

Federal baseline and Connecticut procedure

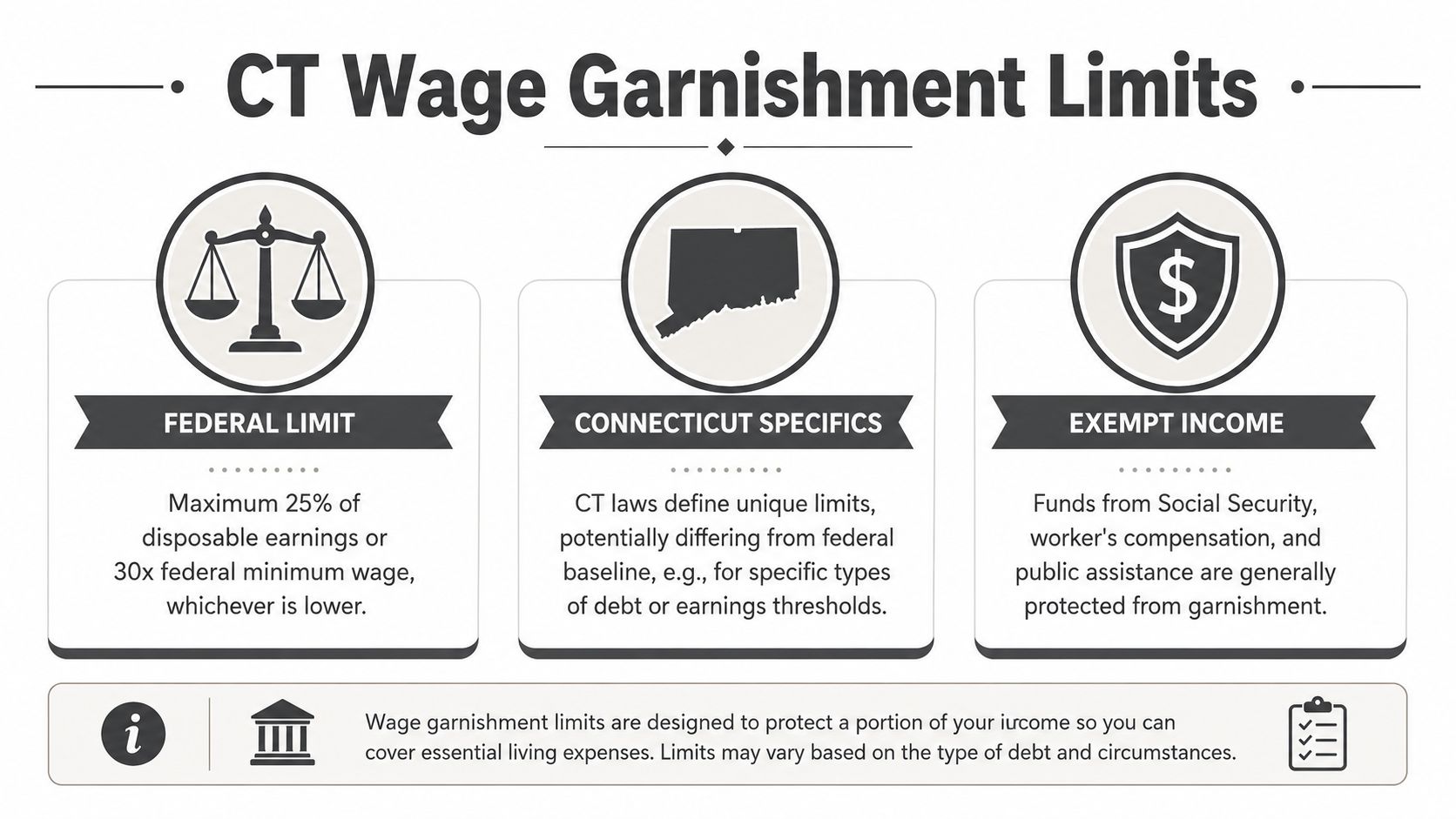

Federal law sets the outer limits for many garnishments. For ordinary judgment debts, the Consumer Credit Protection Act limits withholding to the lesser of 25% of disposable earnings or the amount by which weekly disposable earnings exceed 30 times the federal minimum wage. Using the current federal minimum wage of $7.25, that protected floor equals $217.50 per week, and if disposable earnings are $217.50 or less, nothing can be garnished for an ordinary debt; if earnings are $290 or more, the federal cap reaches 25%, as explained in the U.S. Department of Labor fact sheet on CCPA garnishment limits.

Family support obligations are treated differently under federal law and can reach much higher withholding percentages. For a business creditor enforcing a civil judgment, though, the practical point is narrower. Federal law sets a ceiling, but Connecticut decides how an ordinary judgment creditor gets to payroll, what forms must be served, when withholding starts, and how a debtor can ask the court to reduce or stop the execution.

That state-law layer matters in practice. A debtor who does not file bankruptcy may still slow, limit, or challenge a wage execution through Connecticut's own exemption and modification procedures. Creditors who ignore that part of the process usually misread the likely recovery timeline.

Different debt categories do not follow one rule

Connecticut creditors should sort wage deductions by debt type before doing anything else. The legal authority, the withholding limit, and the available defenses can change depending on what is being collected.

- Ordinary judgment debts, such as unpaid contracts, business accounts, promissory notes, or other civil judgments.

- Family support obligations, which are enforced under a different framework and typically allow more aggressive withholding.

- Government claims, including certain tax and administrative debts that may proceed under separate statutes.

This is more than a labeling issue. Payroll departments routinely ask what type of execution or withholding order they received, and they should. If a creditor treats an ordinary civil judgment like a support order, the numbers will be wrong and the employer may hesitate or reject the papers. If a debtor receives the papers and sees a category mismatch, that error can become the basis for an objection.

A wage execution is a specific post-judgment remedy

A Connecticut wage execution reaches future earnings from employment. It does not reach a bank balance that already exists, and it does not attach real estate equity. That makes it a strong tool when the debtor has steady wages and a weak one when the debtor is self-employed, out of work, paid in cash, or earning irregular commission income.

It also means timing matters. The court judgment alone does not put money in the creditor's hands. The execution has to be issued, served correctly, and allowed to run through the statutory process before payroll begins withholding. During that window, debtors sometimes file exemption claims or ask the court for relief based on earnings, support obligations, or other protected circumstances under Connecticut law.

For creditors, the practical lesson is straightforward. Use wage execution when the debtor has real payroll to reach, but expect Connecticut procedure to matter as much as the judgment itself. For debtors, the same framework means bankruptcy is not the only possible response. State-law objections, exemption claims, and modification requests can change the result if they are raised correctly and on time.

Garnishment Limits and Exemption Rules

The most important practical question in CT wage garnishment is usually this one: How much can be withheld? Creditors want a realistic estimate. Employers want a compliant calculation. Debtors want to know whether payroll has taken too much.

Connecticut is especially important here because, for most ordinary judgment creditors, the state rule is more protective than the federal baseline.

The Connecticut formula creditors usually face

For most Connecticut judgment creditors, the controlling formula is the lesser of 25% of disposable earnings or the amount by which weekly disposable earnings exceed 40 times the federal minimum wage, which is stricter than the federal baseline of 30 times the federal minimum wage, as summarized by the Connecticut garnishment overview from Payroll Training Center.

Using the current federal minimum wage of $7.25, the Connecticut protected floor under that formula is $290 per week because 40 × $7.25 = $290. That means the lower-income range is where Connecticut law most often changes the outcome for ordinary debts.

Why the math matters in real cases

Many creditors hold unrealistic expectations. They assume a quarter of pay will be available because they know the federal 25% figure. In many Connecticut cases, that won't be true, because the "amount over $290" test produces a smaller collectible amount.

Here is a simple way to think about the calculation:

| Weekly Disposable Earnings | Garnishable Amount (A): Income - $290 | Garnishable Amount (B): 25% of Income | Amount Actually Garnished (Lesser of A or B) |

|---|---|---|---|

| $250 | $0 | $62.50 | $0 |

| $290 | $0 | $72.50 | $0 |

| $320 | $30 | $80 | $30 |

| $400 | $110 | $100 | $100 |

| $600 | $310 | $150 | $150 |

That table shows why CT wage garnishment often feels slower than creditors expect. At lower disposable earnings, the amount over the protected floor can be very small or zero. Once earnings rise enough, the 25% cap becomes the limiting number.

Working rule for creditors: Don't value a wage execution by the debtor's gross pay. Value it by weekly disposable earnings and the Connecticut formula.

Exemptions and the waiting period matter

Payroll also can't just start deducting the moment papers arrive. Connecticut procedure includes notice to the employee and an exemption process. The employee receives notice and an exemption form, and withholding generally doesn't begin until the waiting period has run unless no exemption claim is filed, as noted in the earlier Connecticut-specific framework.

That has two practical consequences:

- For creditors: early service doesn't guarantee immediate money flow.

- For employers: rushing the first deduction can create compliance trouble.

- For debtors: silence can waive bargaining power they might otherwise have used to reduce or delay withholding.

A lot of disputes come from sloppy assumptions. One side assumes the federal cap controls. Another assumes garnishment starts at once. Connecticut practice is narrower and more procedural than that.

The Enforcement Process from Judgment to Collection

The enforcement path matters because CT wage garnishment is a court-backed process, not a collection letter with payroll attached. If the paperwork, service, or timing is off, the file slows down quickly.

Step one through service on the employer

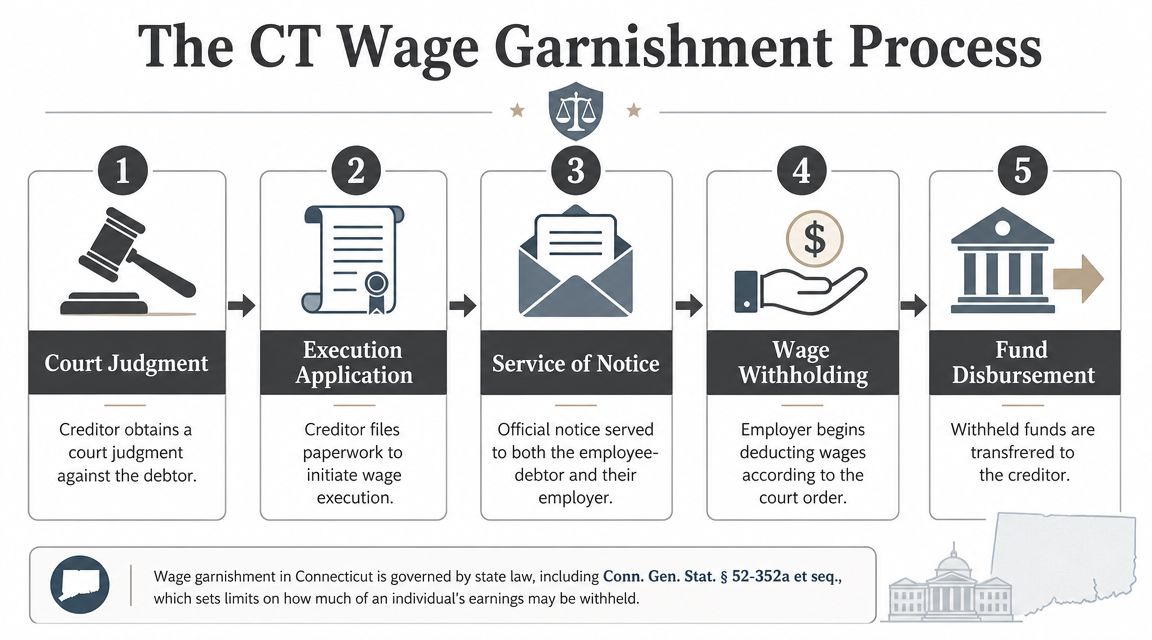

The process starts after the creditor has already obtained a judgment. At that point, the creditor seeks the wage execution and moves into enforcement rather than liability litigation. At this stage, details matter. Incorrect party names, outdated employer information, or poor document handling can delay service and give the debtor extra time.

For businesses that don't routinely handle post-judgment filings, practical resources on procedure can help. If you're organizing and submitting supporting documents electronically, expert advice on court filings can help tighten the filing process and reduce preventable administrative mistakes.

Once the paperwork is in order, Connecticut uses a state marshal or constable to carry the process forward. A wage execution allows a judgment creditor, through a state marshal or constable, to collect directly from a debtor's wages after court action, and the marshal's fee is 15% of the execution amount. After the marshal collects funds from the employer, the marshal must distribute them to the judgment creditor no later than 30 calendar days from collection or upon reaching $1,000 collected, whichever comes first, according to Connecticut wage execution guidance discussing the marshal process.

What actually happens after service

Once the employer is served, the matter turns into an ongoing payroll compliance issue. The employee receives notice and has an opportunity to assert exemptions or seek relief before money is taken. Creditors who expect immediate remittance often underestimate how much of the timeline is built around notice and due process.

A disciplined file usually includes:

- Verified employment information before service.

- Clean judgment records with no unresolved clerical issues.

- Follow-up with the levying officer so service status is confirmed.

- A realistic collection forecast based on payroll frequency and expected withholding limits.

If you want a broader overview of post-judgment collection strategy, this guide on how to enforce a judgment in Connecticut is a useful companion because wage execution is only one part of the enforcement toolbox.

Creditors lose time when they treat wage execution like a one-step remedy. It works better when managed as a file that needs active follow-up.

Why timing and cost affect results

The marshal's 15% fee matters strategically. It affects the economics of smaller files and should be factored into your recovery planning from the start. In some matters, wage execution is still the right move because recurring payroll deductions are more reliable than chasing sporadic voluntary payments. In others, a different enforcement route may produce a better net result.

The remittance timeline matters too. Even after withholding begins, funds don't move instantly from employer to creditor. Collection has a rhythm shaped by payroll dates, employer processing, marshal handling, and statutory disbursement requirements.

The practical point is straightforward. A creditor gets the best result when the file is prepared carefully, the employer information is accurate, and someone is monitoring the process instead of assuming the first service will carry the matter through to payment.

Employer Duties and Potential Liabilities

Employers are often the least prepared party in a Connecticut wage execution. They didn't create the debt, but once they are served, they become responsible for carrying out a court-directed payroll process. If they mishandle it, the problem can become theirs.

What payroll has to do first

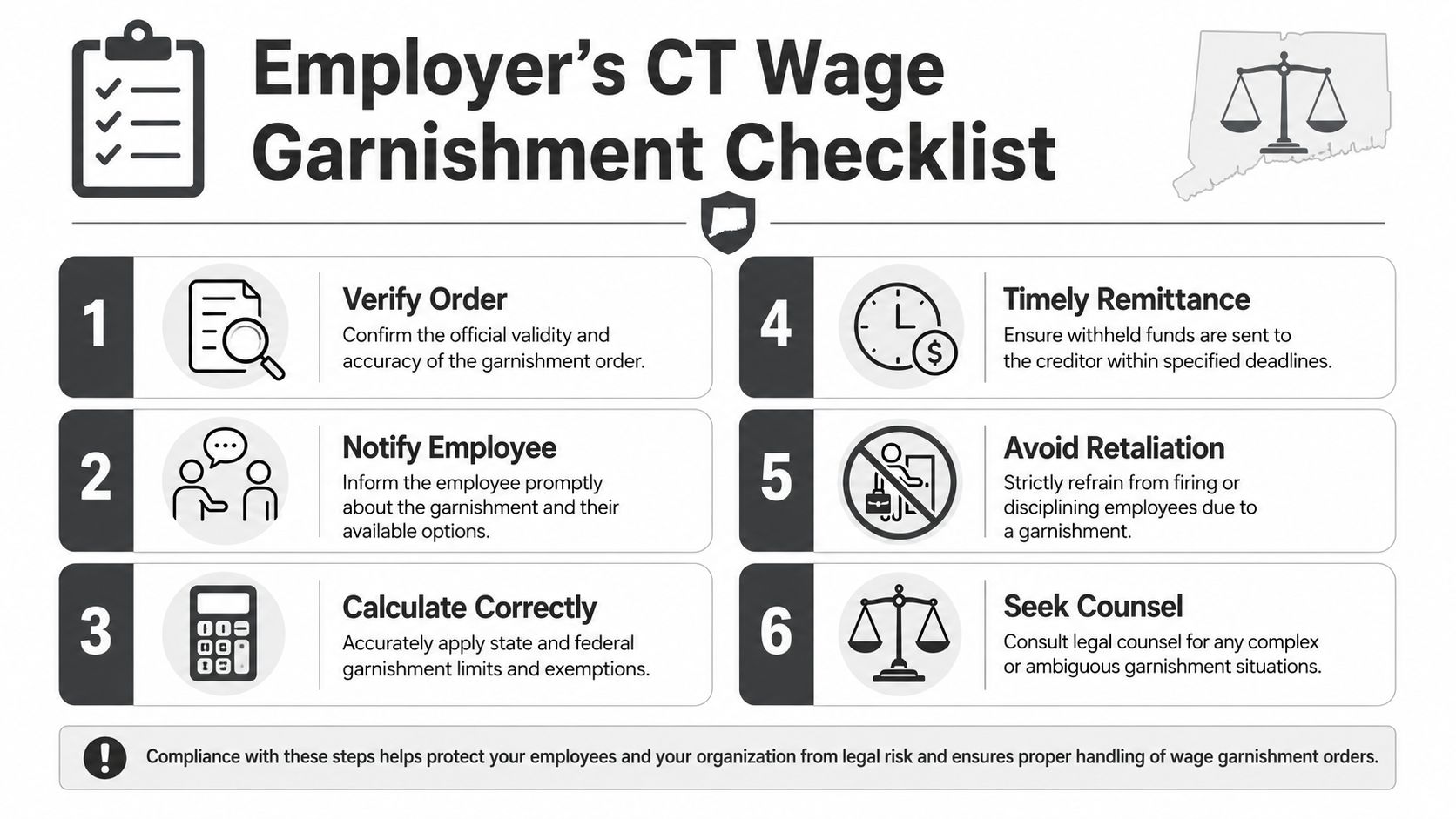

When an employer receives a wage execution, the first job is verification. Payroll should confirm that the order is authentic, identify the employee correctly, and review whether another execution is already in place. Employers should not treat wage execution as a casual accounts-payable item. It belongs in a controlled legal-payroll workflow.

A useful internal checklist looks like this:

- Confirm the order: Match the employee name and identifying information to your records before setting anything up.

- Route it properly: Legal, HR, and payroll should know who owns implementation and who answers employee questions.

- Calculate with care: Use the applicable formula and withholding timing required for Connecticut wage execution.

- Track priority: Earlier executions may need to be satisfied before later ones begin collecting.

- Remit on payroll cadence: Once withholding properly starts, payment follows the employer's payroll frequency.

Priority and stacking are where mistakes happen

Connecticut wage execution is not a one-time attachment. It is an ongoing post-judgment enforcement tool that can stack behind earlier executions and is administered through a levying officer. The state marshal's fee is 15% of the amounts collected, and prior wage executions must be satisfied first, while employers remit on the same frequency as payroll, as described in Connecticut wage garnishment guidance on execution priority and remittance.

That priority rule is one of the most common operational problems. Payroll departments sometimes receive a new execution and assume they should begin withholding immediately, without determining whether an earlier execution already occupies the available deduction slot. That can create errors in both amount and sequence.

Employer-side warning: The hard part usually isn't receiving the order. It's applying the order correctly when the employee already has another withholding in place.

Liability grows from process failures

Employers also need to think beyond math. They need a repeatable internal process that protects the company from avoidable disputes. That includes preserving documents, recording service dates, and making sure staff understand that the employee may have exemption rights and may ask questions that payroll alone can't answer.

When the situation becomes messy, counsel should review it early rather than after an error compounds through multiple pay periods. Businesses already reviewing workplace documents and payroll-related risk issues often benefit from broader legal housekeeping, including employment agreement review and related compliance planning, because wage withholding problems rarely stay isolated from other HR process weaknesses.

What works is consistency. What doesn't work is improvising each garnishment order from scratch.

Debtor Defenses and Strategic Relief Options

Most articles about CT wage garnishment tell debtors one thing: file bankruptcy. That advice is incomplete. In many Connecticut cases, the immediate question isn't whether the debt disappears. Instead, the question is whether the withholding amount can be challenged, reduced, delayed, or redirected under the existing process.

The short window that matters

Public guidance notes that money cannot be taken until 20 days after service of the wage execution, which creates a short period to file an exemption claim. That same guidance also notes that the outcome is not always all-or-nothing because garnishment may be reduced, delayed, or redirected depending on the debt type and the debtor's disposable earnings, as discussed in Nolo's overview of Connecticut wage garnishment law.

That waiting period matters for both sides. A debtor who acts promptly may preserve meaningful arguments. A creditor who ignores the possibility of an exemption or hardship claim may overestimate near-term recovery.

What tends to work and what usually doesn't

From a practical standpoint, courts respond better to concrete hardship showings than to general statements that the deduction is difficult. The employee usually needs to engage the process directly and provide organized support for the claimed exemption or inability to afford the statutory amount.

What tends to help:

- Specific financial proof: pay records, recurring expense documentation, and anything that shows the actual effect of withholding.

- Prompt filing: waiting until deductions have already begun usually weakens your position.

- Debt-type clarity: support obligations, ordinary judgments, and other categories don't all leave the same room for relief.

What tends not to help:

- General unfairness arguments with no supporting documents.

- Informal side deals that assume payroll will stop because the debtor offered a payment plan.

- Silence during the notice window followed by objections after withholding is underway.

Some debtors don't need a complete stop. They need a modification. Creditors who understand that are usually better prepared for the hearing.

For creditors, this isn't just background information. It is part of risk assessment. If you know the employee may raise exemptions or hardship, you can prepare a more realistic collection timeline and avoid treating a temporary delay as a failed enforcement effort. For a broader look at the legal environment surrounding collection practice, this overview of Connecticut debt collection laws provides additional context.

Protecting Your Rights as a Creditor

A creditor often feels the pressure here after judgment enters. The balance is valid, the court process is complete, and yet collection still slows down because payroll paperwork was incomplete, service was mishandled, or a debtor raised an exemption claim that could have been anticipated.

Protecting your position in a Connecticut wage garnishment matter means more than getting the execution issued. It means treating the file like an enforcement project with deadlines, employer follow-up, and a realistic plan for objections based on hardship or exempt income. Creditors who understand those state-law challenge procedures usually make better decisions about timing, settlement, and whether to press forward or adjust expectations.

Accuracy matters at every step. A miscalculated amount, a priority mistake, or a delay in responding to an employer question can hold up deductions and create avoidable disputes. A debtor's request to reduce or stop withholding does not always mean the collection effort is failing. In many cases, it means the matter is moving into a hearing where preparation will determine the result.

For a practical explanation of the procedure itself, review this guide on how to garnish wages in Connecticut.

For creditors handling collection issues that affect cash flow, vendor relationships, or broader business operations, experienced counsel can help keep the process on track and reduce enforcement mistakes. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.