You’re close to a deal, but the price still doesn’t work. You believe your company’s next phase justifies a higher valuation. The buyer sees risk, customer concentration, integration costs, or uneven recent performance and wants to pay less at closing. That gap is where many business sales in Connecticut stall.

An earn-out agreement is often the tool that saves the transaction. It lets the parties split the disagreement over value into two parts: what gets paid now, and what gets paid later if the business performs the way the seller says it will. Used well, it can align incentives and preserve upside. Used poorly, it can turn a successful closing into a long fight over accounting, operations, and control.

Business owners should understand that an earn-out is not just a pricing formula. It’s a post-closing relationship document. It affects how the business will be run, what records you can inspect, how performance gets measured, and what happens when the buyer’s strategic priorities change after the deal closes.

If you’re preparing for a sale, two resources matter early. First, a working grasp of understanding the due diligence process helps frame what the buyer is really testing before it agrees to any contingent payment. Second, sellers should know how diligence in a business acquisition unfolds in legal terms, including the practical checkpoints covered in what is due diligence in business.

Bridging the Valuation Gap in Business Sales

A seller usually prices the business based on future opportunity. A buyer usually prices it based on what can be verified today. Both positions can be rational.

That tension is especially common in founder-led businesses, service firms tied to relationships, and companies that recently accelerated but haven’t yet built a long record to prove the new numbers are sustainable. In those deals, a flat compromise on price often leaves both sides unhappy. The seller feels underpaid. The buyer feels exposed.

An earn-out changes the conversation. Instead of arguing only about present value, the parties agree that part of the purchase price will depend on actual post-closing results. If the company performs, the seller receives additional consideration. If it doesn’t, the buyer hasn’t overpaid.

Why this structure shows up so often

The reason earn-outs remain attractive is simple. They give each side a way to preserve its story about value without forcing the other side to accept it blindly. The seller keeps upside. The buyer gets proof.

For Connecticut small and mid-sized business owners, that matters in deals involving:

- Professional services firms: The value often depends on whether clients stay after the owner exits.

- Growth-stage companies: The buyer may believe the growth is real, but still want evidence before paying the full premium.

- Founder-driven operations: A buyer may worry that recent performance reflects the founder’s personal involvement more than a transferable system.

A workable earn-out doesn’t eliminate disagreement. It organizes disagreement into a contract the parties can actually live with.

Why local deal reality matters

Many generic explanations of what is an earn out agreement stop at the definition. That’s not enough. In practice, the questions are harder: What metric should control? Who controls the business after closing? What access does the seller get to books and records? What happens if the buyer folds the target into a larger platform and the standalone numbers disappear?

Those drafting points decide whether the earn-out functions as a fair bridge or a future lawsuit.

What Is an Earn-Out Agreement Fundamentally

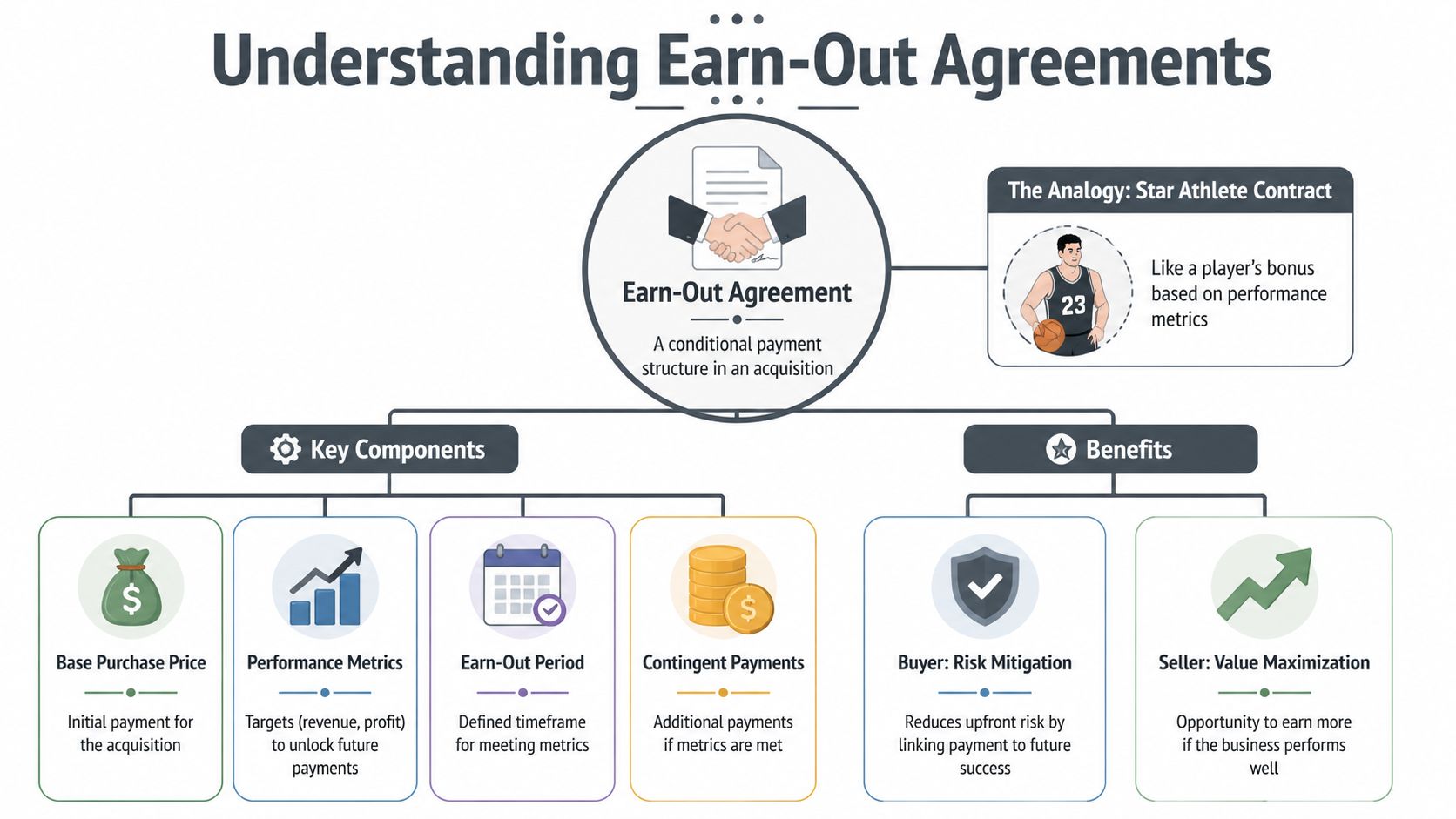

A simple way to understand what is an earn out agreement is to compare it to a performance bonus in a star athlete’s contract. The athlete signs now, gets guaranteed money now, and earns additional compensation later if specific performance targets are achieved. The bonus isn’t charity and it isn’t automatic. It’s a negotiated formula tied to defined outcomes.

That’s the same basic idea in M&A. Part of the purchase price is paid at closing. Another part is deferred and becomes payable only if the acquired business hits agreed targets after closing.

According to the earn-out overview collected at Wikipedia’s earnout entry, an earn-out agreement is a pricing mechanism where 10-50% of the purchase price is deferred and contingent on post-closing performance over a 3-5 year period. The same source notes the Delaware warning that earn-outs often “convert today’s disagreement over price into tomorrow’s litigation,” especially when the contingent portion exceeds 20-30% of total price.

The moving parts that matter

Every earn-out has a few core components:

- Upfront payment: The amount paid at closing, usually the portion the buyer is confident enough to fund immediately.

- Contingent payment: The additional amount the seller may receive later if the business meets the earn-out targets.

- Performance metric: The benchmark that controls payment, such as revenue, EBITDA, gross margin, or a non-financial milestone.

- Measurement period: The period after closing during which performance is tested.

- Payment mechanics: Whether the payout is all-or-nothing, tiered, annual, cumulative, or based on excess performance.

Those elements sound straightforward. They rarely stay straightforward once the buyer owns the company.

Why earn-outs exist at all

At bottom, an earn-out exists because the parties disagree about risk. The seller says, “Pay me for the future I built.” The buyer says, “I’ll pay for the future after I see it happen.” The earn-out is the compromise.

That compromise can be smart, but only if the metric is objective and the parties address post-closing control properly. The seller usually no longer controls daily operations. The buyer does. That means the buyer may control the very decisions that affect whether the seller gets paid.

Practical rule: If the earn-out formula looks clean on paper but ignores who controls pricing, staffing, overhead allocation, and integration decisions after closing, it isn’t finished.

The hidden tension in the structure

The seller wants a metric that can’t be easily manipulated. The buyer wants flexibility to run the business after closing. Those goals naturally collide.

A seller may push for top-line metrics because they’re easier to verify. A buyer may prefer profitability-based metrics because they better reflect value. Neither side is wrong. But if the parties don’t define terms with precision, they leave room for the worst kind of post-closing dispute: one where both sides can read the same contract and still believe they’re clearly right.

Common Earn-Out Structures and Performance Metrics

Most earn-out negotiations come down to two design questions. First, how will the payout work? Second, what exactly must the business achieve to trigger it?

The market data helps frame that discussion. According to Kroll’s analysis of earn-outs in M&A, approximately 50%–80% of earn-outs use EBITDA or revenue as the primary performance metric. The same source reports a 24-month median earn-out period and says the median earn-out potential represents 32% of the closing payment.

How payout structures usually work

Not every earn-out is built the same way. The structure changes the incentives.

Some agreements use a single payment at the end of the measurement period. That can simplify administration, but it also delays the dispute if the parties disagree.

Others use annual or multi-period payments. That gives the seller earlier visibility and may make it easier to identify a problem before it compounds.

Common approaches include:

- Cliff structure: The seller gets paid only if the target is fully met. Miss the threshold and there’s no payout.

- Tiered structure: The payout increases as performance rises through defined bands.

- Formula-based variable payout: The seller receives a percentage or multiple tied to results above a baseline.

- Fixed contingent payment: A pre-set amount becomes due if a specific milestone occurs.

A buyer may prefer a cliff because it’s easier to budget and easier to administer. A seller often prefers a tiered structure because it better rewards partial success and reduces the chance that a small shortfall wipes out the entire earn-out.

The metric often matters more than the formula

Revenue and EBITDA dominate because they answer different concerns. Revenue is usually easier for the seller to track and harder for the buyer to depress through internal accounting choices. EBITDA gives the buyer a closer view of operating performance, but it invites more arguments about expenses, allocations, and adjustments.

Non-financial milestones also appear in the right deal. A service business may tie payments to client retention. A regulated business may use approvals or licenses. A product company may focus on a launch milestone if launch timing is central to value.

For context on how the transaction structure itself affects these issues, sellers should also understand the mechanics discussed in what is an asset purchase agreement. The form of the deal can influence what’s being measured and how cleanly the acquired business can be tracked after closing.

Comparison of Common Earn-Out Metrics

| Metric | Seller's Perspective (Pros/Cons) | Buyer's Perspective (Pros/Cons) |

|---|---|---|

| Revenue | Pros: Easier to verify, less exposed to expense allocation. Cons: May reward sales that don’t produce healthy margins. | Pros: Objective and easy to monitor. Cons: Can require payment even when profitability is weak. |

| Gross Profit | Pros: Better than revenue alone when margin discipline matters. Cons: Can still trigger disputes over cost classification. | Pros: Links payment more closely to economic quality of sales. Cons: Requires careful definitions of included and excluded costs. |

| EBITDA | Pros: Can capture real operating performance if clearly defined. Cons: Vulnerable to disputes over overhead, add-backs, and accounting treatment. | Pros: Closely tied to operating value. Cons: Drafting has to be very precise to avoid fights over calculation. |

| Net Income | Pros: Familiar concept. Cons: Often the least seller-friendly because many post-closing decisions can affect it. | Pros: Measures bottom-line performance. Cons: Highly sensitive to accounting policies, financing, and tax treatment. |

Revenue is often cleaner. EBITDA is often more economically precise. “Better” depends on who controls the levers after closing.

What works and what usually doesn’t

A metric works when the parties can test it without re-litigating the buyer’s management decisions every quarter. It fails when ordinary business judgment and earn-out math become inseparable.

For example, a revenue metric may work well in a stable recurring-revenue business with consistent pricing. EBITDA may work if the business remains operationally separate and the agreement tightly defines expense allocation. Non-financial milestones can be effective when the milestone is objectively verifiable. They become dangerous when the buyer can delay or redefine the milestone without consequence.

Strategic Reasons to Use an Earn-Out Agreement

Some deals need an earn-out. Others are better off without one. That’s the first strategic judgment.

An earn-out makes sense when the parties agree on the business but disagree on timing, certainty, or proof. It’s often useful where there’s genuine upside, but the buyer can’t responsibly pay for that upside on day one.

When buyers benefit

From the buyer’s side, the strategic value is risk control. If management projections are aggressive or the business depends heavily on the founder, the buyer may want to tie part of the price to actual transition success.

That can be especially sensible when:

- Recent growth is real but unproven: The buyer wants evidence that the trend survives post-closing.

- Customer relationships are personal: The buyer doesn’t know whether key accounts will stay.

- The business will need a transition period: The buyer wants the seller invested in continuity.

- The industry is volatile: The buyer wants to reduce the risk of paying for projections that don’t materialize.

When sellers benefit

Sellers often resist earn-outs, and for good reason. They shift part of the price into a period the seller may no longer control. But in the right deal, an earn-out can be a powerful tool for the seller.

It may be worth using when the seller believes the buyer’s current valuation misses the company’s trajectory. Rather than accepting a lower fixed price, the seller can preserve upside if post-closing performance confirms the seller’s view of value.

That’s often true in businesses with strong pipelines, recurring relationships, or pending commercial developments that haven’t yet converted into fully recognized results by signing.

The best fit and the worst fit

An earn-out is usually a better fit for businesses that can be measured cleanly after closing. It’s a worse fit when the buyer will immediately absorb the target into a larger operation and the standalone economics will become impossible to isolate.

Good candidates often include:

- founder-led service businesses where retention and transition support matter

- companies with clear and trackable revenue lines

- high-growth businesses where current earnings don’t fully capture future value

- deals where both parties expect the seller to stay involved for a transition period

Poor candidates usually include:

- transactions where the seller wants a full and immediate exit

- deals where the buyer plans rapid integration across finance, HR, pricing, and sales

- situations where the metric can’t be measured without subjective judgments every month

- relationships already strained before signing

If the parties don’t trust each other enough to define post-closing conduct with precision, an earn-out often magnifies that distrust rather than solving it.

A practical Connecticut lens

In the Connecticut lower middle market, many companies are still relationship-driven. That makes earn-outs attractive, but also fragile. If the founder’s departure changes client behavior, employee morale, or referral flow, the earn-out may become a proxy fight over transition quality. The cleaner the business systems and reporting before the sale, the better the odds the earn-out can function the way both sides intended.

Drafting Critical Clauses to Prevent Disputes

The legal drafting decides whether the earn-out is a business solution or a litigation file. Most disputes don’t arise because earn-outs are inherently flawed. They arise because the contract leaves too much room for post-closing reinterpretation.

The Delaware observation is famous because it’s accurate. As summarized by Harvard Law School Forum on Corporate Governance, Vice Chancellor J. Travis Laster noted that an “earn-out often converts today’s disagreement over price into tomorrow’s litigation.” The same discussion notes that many agreements now use carry-forward and carry-backward provisions in multi-year earn-outs so overperformance in one year can offset underperformance in another.

Define the metric with surgical precision

If the earn-out turns on EBITDA, don’t stop at the acronym. Define it. Spell out the accounting principles. Identify permitted and prohibited adjustments. Address how shared costs will be allocated. State whether the buyer can change accounting policies during the earn-out period and, if so, under what limits.

Bad drafting uses broad financial labels and assumes everyone shares the same understanding. Good drafting uses detailed definitions, examples, and schedules where necessary.

A seller should ask questions like these:

- What expenses can the buyer allocate to the business?

- Will corporate overhead be charged?

- How are one-time integration costs treated?

- Can the buyer reclassify revenue or defer recognition?

- Does the agreement use consistent accounting methods throughout the period?

If those answers aren’t in the contract, they’ll be argued later.

Address post-closing operations directly

Sellers often focus on the formula and miss the operations covenant. That’s a mistake. The formula matters less if the buyer has unrestricted power to alter the business in ways that make the target impossible to hit.

The contract should address whether the buyer must operate the business consistently with past practice, maintain separate books, preserve a defined level of autonomy, or avoid taking actions primarily intended to impair the earn-out. Not every buyer will accept extensive restrictions. But if the seller gives up control, the seller should demand clarity about what replaces it.

The legal concepts behind these negotiations often overlap with the allocation of risk elsewhere in the purchase agreement, including the topics discussed in what is a representation and warranty. Earn-outs don’t stand alone. They sit inside a broader set of negotiated protections.

Buyers want freedom. Sellers want protection. Strong drafting accepts that tension and resolves it in express language instead of leaving it to implied duties.

Give the seller real access to information

A seller can’t enforce an earn-out it can’t verify. The agreement should provide regular reporting, define what the buyer must deliver, and state when the seller may inspect supporting records.

That usually includes:

- Periodic statements: Monthly, quarterly, or other scheduled earn-out reports.

- Supporting detail: Enough backup to test the calculation, not just a one-line conclusion.

- Access rights: The ability to review books and records relevant to the calculation.

- Audit procedure: A process for raising objections and submitting unresolved accounting items to an independent expert if needed.

A common drafting error is giving the seller a right to receive the final number but not the underlying material needed to assess it.

Separate accounting disputes from broader legal disputes

One of the most important clauses is the dispute resolution clause. It should say who decides what.

An independent accountant may be the right decision-maker for narrow calculation disputes. That same accountant is usually not the right person to decide whether the buyer acted in bad faith, breached an operating covenant, or improperly integrated the business. Those broader issues may belong in arbitration or court, depending on the agreement.

The clause should clearly distinguish:

| Issue | Better fit |

|---|---|

| Mathematical or accounting calculation dispute | Expert determination by an accounting firm |

| Dispute over buyer conduct, covenant compliance, or bad faith | Arbitration or litigation, depending on the agreement |

| Mixed dispute involving both calculations and operational conduct | A clause that allocates issues carefully rather than sending everything to one forum |

Use smoothing tools when the business is uneven

Multi-year earn-outs can be distorted by timing. A delayed contract, a seasonal cycle, or a one-period disruption can make a single-year test unfairly harsh. That’s where carry-forward and carry-backward concepts can help.

Those provisions let one period’s outperformance help cure another period’s shortfall, reducing the chance that a timing anomaly defeats the intended economics. They don’t solve every problem, but they can make a multi-period earn-out more faithful to the parties’ real bargain.

Navigating Earn-Out Tax and Accounting Implications

The purchase price isn’t the same thing as the after-tax result. Sellers often focus on the headline number and pay too little attention to how the contingent portion may be taxed.

According to AdvisorLegacy’s discussion of earn-out agreements, earn-out payments in the United States are often taxed differently from the upfront purchase price. The source states that sellers frequently face ordinary income tax rates up to 37% federal plus state on earn-out proceeds, compared with capital gains rates of 15-20% on the initial payment.

Why tax treatment changes the real economics

That difference matters because two deals with the same nominal value can produce very different net proceeds. A seller who accepts a large contingent component without modeling tax treatment may discover that the apparent upside is less attractive than it looked during negotiations.

This issue becomes even more important where the seller is deciding between:

- a lower but more certain upfront payment

- a higher headline purchase price with a significant earn-out

- cash versus equity in contingent consideration

- compensation-like payments tied to continued services versus true purchase price treatment

Those distinctions can affect not just taxes, but incentives and influence during the earn-out period.

Accounting treatment affects behavior too

Buyers also need to think about accounting consequences. Contingent consideration may have to be tracked and valued on the buyer’s books, which can influence how finance teams monitor the acquisition and how management views the earn-out internally.

That doesn’t mean accounting should drive the legal structure. It does mean legal drafting, tax advice, and accounting analysis should happen together, not in separate silos.

A seller shouldn’t evaluate an earn-out only by asking, “What’s the maximum payout?” The better question is, “What will I actually keep, and what control do I have over earning it?”

Practical takeaways for sellers

Tax treatment depends on deal-specific facts and structure, so general rules only go so far. But the practical point is clear. Don’t negotiate the earn-out formula first and ask tax questions later. By then, you may be defending a structure that already bakes in an unfavorable outcome.

For Connecticut business owners, the right move is to have transaction counsel and tax advisors review the earn-out together while the letter of intent and definitive documents are still negotiable.

Your Connecticut Earn-Out Agreement Checklist

A strong earn-out isn’t just negotiated. It’s tested. Before signing, a seller should pressure-test the clause as if a dispute were already underway. If the contract leaves obvious questions unanswered now, those questions won’t get easier after closing.

For broader transaction preparation, business owners should also review a practical mergers and acquisitions due diligence checklist so the earn-out isn’t negotiated in isolation from the rest of the deal.

Pre-signing checklist for sellers

Use this list before you agree to principal terms.

- Test the metric for manipulation: Ask whether the buyer can affect the metric by reallocating costs, changing pricing, delaying revenue recognition, or shifting personnel.

- Confirm the business can still be measured post-closing: If the buyer plans immediate integration, require a clear method for tracking the acquired business or rethink the earn-out.

- Match the metric to the business reality: A relationship-heavy service firm may need a retention-based or revenue-based measure. A standalone operating business may support EBITDA if the definitions are tight.

- Review seller involvement expectations: If your earn-out assumes you’ll stay active after closing, define your role separately and carefully. Don’t leave that to assumption.

- Check the payout timing: A payment formula is only part of the story. The agreement should say when calculations are delivered, when objections are due, and when payment must be made.

Drafting checklist for the purchase agreement

Many deals falter at this stage. The parties agree on economics and treat the text as cleanup. It isn’t cleanup.

Make sure the agreement covers:

Exact definitions of financial terms

If EBITDA is the metric, define every key component, including exclusions, add-backs, and treatment of extraordinary items.Accounting methodology

State the governing accounting principles and whether consistency with past practice controls.Operational covenants

Decide whether the buyer must maintain separate books, preserve a business line, refrain from certain reallocations, or avoid conduct designed to impair the earn-out.Reporting rights

The seller should receive periodic reports with enough detail to verify the calculation.Inspection and challenge process

Set deadlines and procedures for objections. Ambiguity here creates procedural fights before the substantive dispute even starts.Dispute forum

Distinguish narrow accounting issues from broader contract disputes.

A sample covenant concept

Exact language depends on the deal, but sellers often need an operating covenant with real content. A simple concept might read like this:

During the earn-out period, Buyer shall operate the acquired business in material accordance with the accounting and operational practices used immediately prior to closing, shall maintain books and records reasonably sufficient to calculate the earn-out, and shall not take actions in bad faith primarily intended to reduce or avoid earn-out payments.

That clause still needs refinement. “Material accordance,” “operational practices,” and “bad faith” should be shaped to the business. But it’s stronger than a vague expectation that the buyer will “act reasonably.”

Connecticut-specific practical concerns

In closely held Connecticut businesses, earn-outs often run into the same real-world problem. The seller assumed the buyer would preserve continuity. The buyer assumed it bought full discretion to optimize the business. Both assumptions can’t govern at the same time.

That’s why local owners should focus on concrete business behavior, not just legal labels. Ask:

- Will the buyer keep key employees in place?

- Will pricing authority change?

- Will overhead be centralized?

- Will customer relationships move to a new brand immediately?

- Will the business remain a separate reporting unit?

Those aren’t academic questions. They affect whether the earn-out remains measurable and fair.

The final review before signing

Before closing, read the earn-out with one harsh assumption: the relationship may deteriorate. Then ask whether the clause still works.

If the answer depends on cooperation, goodwill, or “they’d never do that,” the agreement needs more work. A durable earn-out is built for imperfect conditions. It assumes incentives may diverge and drafts for that reality.

Conclusion Securing Your Deal's Future Value

An earn-out can be one of the most useful tools in a business sale. It can preserve deal momentum, bridge real valuation disagreements, and let a seller share in future performance. But it only works when the contract matches the business reality after closing.

The practical lesson is straightforward. Clear metrics matter. Operational covenants matter. Access to information matters. Dispute procedures matter. So do tax consequences and the simple question of whether the buyer’s post-closing plan will make the earn-out measurable at all.

For Connecticut owners and investors, what is an earn out agreement isn’t just a definition issue. It’s a deal-structure issue, a control issue, and often a risk-allocation issue. The better the drafting, the better the odds that the earn-out functions as intended. The looser the drafting, the more likely it becomes a delayed fight over price.

An earn-out should be treated like a high-stakes operating agreement for the period after closing. If that period isn’t planned carefully, the sale price on paper may never become the sale price in reality.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.