A lot of fiduciary duty disputes start before anyone uses that phrase.

A minority owner gets excluded from a deal discussion. A founder approves a transaction with a friendly vendor and doesn’t fully disclose the relationship. A financial advisor recommends a product that benefits the advisor more than the client. The people involved usually think the fight is about money, control, or disclosure. Legally, the fight often turns on a more specific question: what is a breach of fiduciary duty, and can someone prove it?

For Connecticut businesses, investors, officers, directors, and financial professionals in FINRA matters, that question isn’t academic. It affects how deals are documented, how boards make decisions, how conflicts are handled, and how claims get prosecuted or defended when trust breaks down.

Understanding Fiduciary Duty in a Business Context

A fiduciary duty is a legal obligation that arises when one party is trusted to act for the benefit of another. In business settings, that usually means a person with power, access, or discretion has to use that position for the beneficiary’s interests, not their own.

The core concepts are loyalty and care. Loyalty means avoiding self-dealing, hidden conflicts, and misuse of position. Care means making decisions with appropriate diligence, attention, and judgment. In some settings, disclosure and good faith are also central to how courts and arbitration panels evaluate conduct.

That sounds abstract until you place it in a boardroom.

A Connecticut company is evaluating a sale of assets. One director has a personal relationship with the proposed buyer. Another director wants to move fast and skip a fuller review because the business needs cash. A minority owner asks for records and gets brushed off. None of that automatically proves liability. But all of it raises fiduciary questions.

Why this matters in practice

Most business clients don’t need a philosophical definition. They need to know when ordinary decision-making crosses into legal exposure.

The practical questions are usually these:

- Who owes the duty: Is it a director, officer, manager, partner, trustee, broker, or advisor?

- What conduct creates risk: Was there self-dealing, nondisclosure, favoritism, misuse of assets, or weak supervision?

- What proof matters: Are there emails, board minutes, trading records, valuation materials, or client communications?

- What response works: Internal review, demand letter, negotiated fix, court action, or FINRA arbitration?

Good governance reduces a lot of this risk before a dispute starts. If you want a broader operational view of managing fiduciary obligations, that resource is useful because it treats fiduciary responsibility as a day-to-day governance discipline, not just a litigation issue.

For businesses, fiduciary duties also overlap with governance structure. The quality of your minutes, conflict procedures, committee process, and approval record often determines whether a later dispute looks like a hard decision made carefully or a breach dressed up after the fact. That’s part of why corporate governance deserves more attention than many companies give it. A useful starting point is this discussion of corporate governance basics.

Practical rule: Fiduciary duty claims are rarely won or lost on rhetoric. They’re won or lost on who had the obligation, what they knew, what they disclosed, and what the record shows.

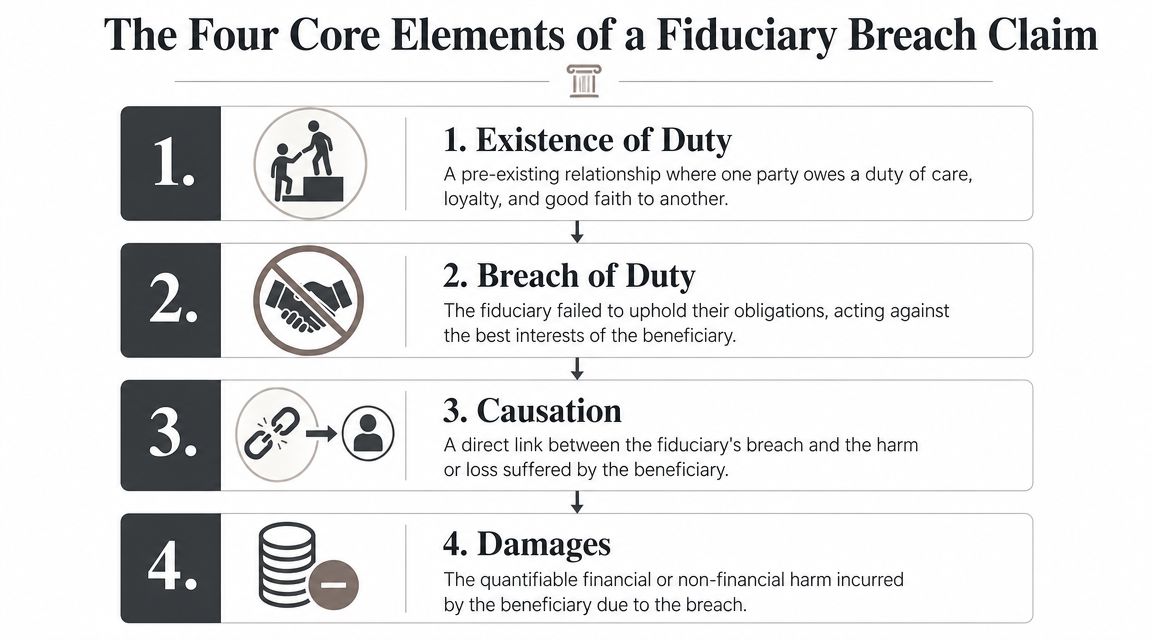

The Four Core Elements of a Fiduciary Breach Claim

A fiduciary duty claim is often described in shorthand, but in real litigation or arbitration, the analysis is more disciplined than that. The plaintiff has to connect several points in a chain. If one link is weak, the claim can fail.

The easiest way to think about it is a ship captain analogy. Passengers entrust the captain with authority, judgment, and safety. If the captain ignores a known hazard, that may be a breach. But the case still requires proof that the captain had the duty, violated it, caused the injury, and caused measurable harm.

Courts often discuss three core elements: existence of duty, breach, and causation with quantifiable damages. In practice, lawyers usually separate damages into their own category because proving harm is often its own battlefield. The underlying framework appears in this explanation of breach of fiduciary duty elements.

Existence of a fiduciary duty

You can’t sue for breach of fiduciary duty unless the relationship imposed fiduciary obligations.

That sounds obvious, but it’s frequently contested. Not every business disagreement involves a fiduciary relationship. A contractual counterparty may owe duties under the agreement without owing fiduciary obligations. An employee may owe duties to an employer, but not every workplace dispute becomes a fiduciary case. A broker’s role may create obligations in one context that look different in another.

Typical fiduciary relationships include:

| Relationship | Why the duty may exist |

|---|---|

| Corporate director to corporation or shareholders | Decision-making power and obligation to act loyally and carefully |

| Officer to company | Control over operations, assets, and disclosures |

| Partner to partner or partnership | Mutual trust and duties tied to shared enterprise |

| Financial advisor or broker in certain contexts | Trusted guidance involving client assets and disclosures |

| Trustee to beneficiary | Formal obligation to manage property for another |

The first defense in many cases is simple. The defendant argues, “I didn’t owe that kind of duty here.”

Breach of that duty

Once duty exists, the next question is whether the fiduciary violated it.

The most common breach patterns are familiar to business people:

- Self-dealing: Using company opportunities or assets for personal benefit

- Undisclosed conflicts: Participating in decisions without full disclosure of personal interests

- Unauthorized activity: Acting beyond authority, including unauthorized trades in investment settings

- Negligent oversight: Failing to supervise when supervision was part of the role

- Material omissions: Withholding information that should have been disclosed

Many clients want a bright line rule, but the law usually doesn’t offer one. The same transaction can look proper or improper depending on process. A related-party deal with full disclosure, independent review, and fair pricing is very different from a rushed insider deal hidden from decision-makers.

Causation

Causation is where a lot of otherwise serious allegations weaken.

A claimant must usually show that the breach proximately caused the harm. That means more than showing bad conduct occurred. The claimant has to connect the misconduct to the loss in a direct, evidentiary way.

For business disputes, that often requires a record like this:

- The fiduciary had control over a transaction or decision.

- The fiduciary failed to disclose, acted in self-interest, or ignored a duty.

- That failure changed the course of the transaction.

- The company, shareholder, or client suffered a measurable loss because of that change.

Causation is where suspicion has to become proof.

In practice, this often turns on documents, communications, and financial analysis. Forensic accounting can matter a lot in cases involving diverted funds, hidden compensation, inflated pricing, or investment losses.

Damages

A breach without provable harm may still create legal consequences in some circumstances, but most real disputes are about money, control, or both.

Damages can include direct financial loss, lost opportunity, disgorgement of profits, or equitable relief. The exact measure depends on the setting. In a company dispute, the issue may be how much value the business lost or how much the fiduciary wrongfully gained. In a securities case, the question may be what losses flowed from unsuitable recommendations, omissions, or unauthorized trading.

For discerning readers, this is the key strategic point: a strong claim needs more than unfair facts. It needs a clean theory of proof.

That’s true on both sides. Plaintiffs need a disciplined damages model. Defendants need to attack weak links in the chain instead of arguing every issue at once.

Who Owes a Fiduciary Duty Common Real-World Examples

The question 'what is a breach of fiduciary duty' is rarely abstract; it typically arises when an individual is dealing with a specific actor, such as a director, a partner, an advisor, a trustee, or a controlling member. The legal analysis starts with role, but it gets decided by conduct.

Directors and officers

Corporate directors and officers sit closest to classic fiduciary duty law. They make strategic decisions, control information, approve transactions, and influence how the company uses capital.

A common example is a conflicted acquisition. A CEO pushes the company to acquire a struggling business owned by a friend or family connection. The board gets limited information. Independent valuation is weak or absent. The transaction closes anyway. If the process was tainted and the company paid too much, that can become a duty of loyalty case.

Another recurring example involves access to information. Minority owners ask for records that would reveal compensation arrangements, related-party transactions, or dividend decisions. The board stalls or refuses. That doesn’t automatically establish liability, but it can become part of a broader pattern showing unfair dealing and disregard of minority rights.

One cited discussion notes that self-dealing by a CEO can divert 10-20% of corporate assets, that board refusals to disclose records can trigger derivative litigation, and that the entire fairness doctrine is a key defense issue in conflicted transactions, as discussed in this overview of fiduciary breach examples and defenses.

What usually works

Directors and officers reduce risk when they do three things consistently:

- Disclose conflicts early: Before discussion, not after objections arise

- Build a decision record: Minutes, valuations, term sheets, and recusal notes matter

- Use independent process: Outside valuation, disinterested committee review, and separate counsel can change the whole posture of a case

What doesn’t work is relying on informal trust. Closely held companies often believe relationships can substitute for process. They can’t.

Partners and co-owners

Partnership and closely held business disputes are often more personal, and that makes fiduciary issues more volatile.

Consider a two-owner business where one partner starts moving customers, opportunities, or personnel toward a separate side venture. The other partner discovers the conduct only after revenue drops and key relationships shift. In that setting, the core issue is usually loyalty. Did one owner exploit a position of trust for private gain?

Another common pattern involves compensation or distributions. One owner controls the books and changes pay structure to benefit insiders while starving another owner of information or returns. The dispute may look like an accounting problem, but it often includes fiduciary allegations because control was used opportunistically.

A lot of partnership fiduciary cases aren’t about one dramatic act. They’re about a sequence of concealed decisions that only make sense when viewed together.

The practical challenge here is evidence. Closely held companies often operate informally. That creates room for opportunistic conduct, but it also creates proof problems. If the company never documented authority, expense approvals, or ownership expectations, both sides face avoidable uncertainty.

Financial advisors and brokers

Financial professionals face a different version of fiduciary risk because the relationship is heavily shaped by account documentation, disclosures, product selection, and supervision.

One client scenario is unauthorized trading. Another is excessive trading that appears designed to generate commissions rather than serve the customer’s objectives. Another is recommending products or strategies without adequately disclosing risk, liquidity limits, concentration concerns, or conflicts.

In this space, fiduciary language often overlaps with suitability, disclosure, supervisory failures, and best interest obligations. The legal framing may differ depending on the forum and claims asserted, but the factual core is familiar. The client trusted the professional to act with honesty, care, and loyalty. The client says that trust was abused.

If you want more concrete illustrations across business and financial settings, this collection of breach of fiduciary duty examples is a useful companion.

Trustees and other control roles

Trustees, executors, and similar fiduciaries manage money or property that belongs beneficially to someone else. The duty here is often easier for non-lawyers to understand because the trust relationship is explicit.

Problems usually arise through misuse of funds, selective disclosure, favoritism among beneficiaries, or failure to account. In these cases, the paper trail matters enormously. Courts expect accurate records, not reconstructed explanations.

Across all of these roles, one point stays constant. Power plus trust plus discretion creates risk. The more one person controls assets, information, or decision-making for another, the more likely fiduciary standards will govern the relationship.

Special Considerations for Connecticut and FINRA

Connecticut business disputes and FINRA arbitration matters often involve the same core fiduciary principles, but they don’t play out the same way. The procedural environment, the governing documents, and the available remedies can shift the entire strategy.

Connecticut business disputes

In Connecticut, fiduciary duty issues commonly arise in closely held corporations, LLCs, partnerships, shareholder disputes, and officer misconduct claims. The most important practical point is that your governing documents matter. Bylaws, operating agreements, shareholder agreements, buy-sell terms, and consent requirements shape both the duty analysis and the remedy analysis.

For example, a manager’s authority under an LLC operating agreement may affect whether disputed conduct looks like authorized discretion or concealed overreach. A shareholder agreement may define approval rights, transfer restrictions, or information access in ways that sharpen a fiduciary dispute. In litigation, the contract and the fiduciary theory usually interact. They don’t live in separate boxes.

That has two consequences for Connecticut companies.

First, sloppily drafted internal documents make fiduciary disputes harder and more expensive. Second, good governance records often carry more weight than after-the-fact narratives from participants who now disagree about what was “understood.”

FINRA has its own rhythm

FINRA cases are different. They’re driven by account history, product suitability, disclosure, communications, supervision, and the procedural realities of arbitration.

The numbers show these claims are not niche issues. FINRA arbitration statistics show breach of fiduciary duty filings peaked at 1,518 in 2023 and average over 1,300 annually, with 214 such cases served through March 2026. In the same period, failure to supervise accounted for 302 cases, according to FINRA’s dispute resolution services statistics.

For advisors and firms, that data matters because many cases don’t turn on dramatic fraud allegations. They turn on supervisory structure, suitability review, concentration issues, disclosure quality, and whether the file shows that the recommendation fit the customer’s objectives and risk tolerance.

Common FINRA pressure points

- Failure to supervise: Firms need systems that identify and escalate red flags. A policy manual that nobody enforces won’t help much.

- Unsuitable recommendations: Product complexity, concentration, time horizon, and liquidity all matter.

- Disclosure gaps: If the file doesn’t show meaningful disclosure, the defense gets harder.

- Form U5 fallout: Language used at separation can trigger separate disputes and reputational damage.

In FINRA arbitration, the paper file is often the first witness. If the notes, emails, and approvals are weak, the defense starts behind.

For business owners and financial professionals who haven’t been through the forum before, the mechanics also matter. Pleadings, discovery limits, hearing prep, and panel presentation are different from court practice. This overview of the FINRA arbitration process is a practical reference if you’re trying to evaluate exposure or plan a response.

One issue, two very different forums

A fiduciary case in Connecticut Superior Court and a fiduciary-related claim in FINRA may involve similar accusations, but they reward different habits.

In court, governance structure, entity documents, witness credibility, and equitable remedies may take center stage. In FINRA, account documentation, supervisory evidence, and hearing presentation often dominate. The underlying duty matters in both places. The proof architecture is different.

That’s why business people get into trouble when they assume a single generic “fiduciary” answer will cover every setting. It won’t.

Common Defenses Against a Breach of Fiduciary Duty Claim

An accusation isn’t a judgment. Fiduciary claims can be serious, but they’re often over-pled, emotionally charged, and strategically used to gain an advantage in a business breakup, shareholder fight, or securities dispute.

The defense starts by forcing precision. Who owed what duty, to whom, under what source of law or agreement, tied to what conduct, causing what specific harm?

The business judgment rule

For directors, this is often the first major defense. The basic idea is that courts don’t second-guess honest business decisions even if they turned out badly.

That protection matters because business decisions are often made under uncertainty. Markets shift. Acquisitions fail. Financing gets tighter. Customers leave. A bad result doesn’t automatically mean the board breached a duty.

The defense is strongest when the record shows:

- Good faith: The decision was made with integrity, not for hidden self-interest

- Reasonable information: Directors reviewed enough material to make an informed choice

- No disabling conflict: Interested parties were identified and handled appropriately

If those conditions break down, the protection weakens.

Consent, ratification, and disclosure

Some fiduciary claims fail because the allegedly harmed party knew about the issue and approved the conduct.

That doesn’t excuse every conflict. But informed consent can change the case substantially. If a board fully discloses a related-party transaction and disinterested decision-makers approve it, the plaintiff’s argument usually becomes more difficult. The same principle applies in investment settings where disclosures were clear and the client knowingly accepted the recommendation or strategy.

This is why documentation beats memory. If disclosure happened, prove it with minutes, acknowledgments, emails, and approval records.

No causation and no real damages

This defense gets less attention from clients than it deserves.

Even if the plaintiff can show sloppy process or suspicious conduct, the case still needs proof that the breach caused a concrete loss. Sometimes the transaction was fair despite a bad process. Sometimes market conditions caused the loss. Sometimes the company would have made the same decision anyway. Sometimes the alleged conflict didn’t change the economic result.

A disciplined defense often narrows the dispute to this question: “Show the loss, and show how this act caused it.”

The most effective defense is often subtraction. Strip away indignation, keep the timeline, and test whether the economics actually support the claim.

Timing and contractual limits

Other defenses can be highly technical but very effective.

A defendant may argue the claim is untimely. The defendant may rely on exculpatory language in governing documents. The defendant may challenge standing, especially where an individual owner tries to pursue what is really a company claim. The defendant may also argue that the dispute is contractual, not fiduciary, and shouldn’t be recast to seek broader remedies.

That last point comes up often in business litigation. Plaintiffs sometimes add fiduciary counts because the label sounds stronger than breach of contract. Courts and arbitration panels still require the legal basis to fit the facts.

Remedies and Consequences of a Proven Breach

When a breach is proven, the consequences can be much broader than a damages check.

Some remedies are financial. Others change who controls the business, unwind transactions, or impose restrictions designed to stop ongoing harm. In serious cases, the legal result can alter ownership relationships, governance structure, and regulatory posture all at once.

Financial remedies

The most familiar remedy is compensatory damages. That’s the amount intended to address the actual loss caused by the breach. In a business case, that may involve diverted funds, overpayment in a conflicted transaction, lost enterprise value, or losses tied to misuse of assets or opportunities.

Another major remedy is disgorgement. That focuses less on the victim’s loss and more on the fiduciary’s gain. If a fiduciary profited through wrongful conduct, a court or panel may require that gain to be turned over.

Prejudgment interest can also matter. So can fee-shifting in settings where a statute, agreement, or other legal basis supports it.

Equitable remedies

Money doesn’t always solve the actual problem.

A company may need an injunction to stop a fiduciary from transferring assets, using confidential information, or continuing conflicted conduct. A shareholder or member may seek access to records. A board may seek removal of an officer or manager. A court may rescind a transaction that should never have been approved in the first place.

These remedies often matter most when the misconduct is ongoing. If the fiduciary still controls accounts, books, customer relationships, or internal systems, waiting for a final damages award may be strategically inadequate.

Regulatory and reputational consequences

The consequences become even more severe when regulators are involved.

A January 2025 SEC settlement involving BMO Capital Markets is a strong example. According to this account of the BMO fiduciary duty settlement, BMO agreed to pay $40.7 million to resolve charges tied to misleading investors about mortgage-backed bonds. The settlement included a $19 million civil fine, $19.42 million in disgorgement, and $2.24 million in prejudgment interest.

That matters for two reasons.

First, fiduciary failures can lead to large financial consequences even without an admission of wrongdoing. Second, the enforcement theory often focuses on supervision and disclosure, not just intentional theft or classic fraud.

What businesses often underestimate

Business leaders usually focus on whether they can “win the case.” They should also focus on what the case does while it’s pending.

A fiduciary claim can freeze a deal, complicate financing, impair investor confidence, trigger insurer involvement, strain internal relationships, and create disclosure obligations. For advisors and brokerage professionals, it can also affect licensing, employment transitions, and Form U5 disputes.

The legal remedy is only part of the exposure. The operational disruption is often what clients feel first.

How to Prevent Claims and When to Call an Attorney

The best way to handle fiduciary duty disputes is to create records and decision processes that make bad claims hard to bring and good claims easier to prove. Most prevention is not complicated. It’s disciplined.

For Connecticut businesses

The companies that avoid the worst fiduciary disputes usually do ordinary things consistently.

- Use written conflict procedures: Require disclosure before discussion and voting. Related-party deals should never rely on casual hallway disclosures.

- Keep meaningful minutes: Minutes don’t need to be transcripts, but they should reflect who attended, what materials were reviewed, whether conflicts were disclosed, and how the decision was approved.

- Match authority to documents: Make sure bylaws, operating agreements, and shareholder agreements accurately reflect how the business operates.

- Use independent review when needed: For insider transactions, get outside valuation, independent committee review, or separate counsel where appropriate.

- Preserve records early: Once a dispute is brewing, don’t allow emails, texts, or accounting records to disappear through routine neglect.

Good contract administration also helps because a lot of fiduciary disputes are mixed with approval-rights fights, disclosure obligations, and consent disputes. Teams that want to tighten internal process often benefit from tools and systems that streamline contract workflows, especially where multiple decision-makers need a clear approval trail.

For financial advisors and firms

The most effective risk control in the FINRA setting is disciplined documentation tied to the client’s profile and the recommendation itself.

Consider this checklist:

Update client information regularly

If objectives, liquidity needs, time horizon, or risk tolerance changed, the file should show it.Document the why

Don’t just record what product was recommended. Record why it fit that particular client.Escalate red flags

Concentration, product complexity, complaints, unusual trading activity, and account inconsistencies should trigger review.Train supervisors to supervise

“Failure to supervise” claims usually expose a practical gap between policy and execution.Review separation language carefully

If employment is ending, Form U5 language can create a second dispute on top of the first.

What not to do after an allegation surfaces

Clients often make the same mistakes at the start of a fiduciary dispute.

- Don’t rewrite the record: Backfilling minutes or creating convenient explanations late usually creates more risk.

- Don’t contact everyone impulsively: Internal messaging after an accusation should be controlled and purposeful.

- Don’t assume it will blow over: Silence rarely improves a fiduciary problem once documents and money are involved.

- Don’t reduce it to a personal argument: These cases turn on duties, authority, disclosure, and proof.

One practical option when a matter is serious is to involve counsel who handles both business disputes and arbitration-driven fiduciary issues. Kons Law’s fiduciary duty attorneys work in that space, including business litigation and securities-related disputes.

Get legal advice early if the dispute involves insider transactions, books-and-records demands, threatened injunctions, FINRA claims, account supervision issues, or a separation likely to lead to a contested Form U5.

The right time to call an attorney is usually earlier than clients think. If you’re still deciding how to respond to a conflict, document a board process, preserve evidence, answer a demand letter, or frame claims for arbitration, legal strategy can materially affect the outcome.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.