If you're thinking about selling your company, you've probably already discovered the first hard truth. A sale doesn't begin when a buyer shows up. It begins months earlier, when you decide who will represent the business, who will protect the deal, and how much risk you're willing to carry while the process unfolds.

Most owners in Connecticut come to this point with a mix of urgency and caution. Retirement is getting real. A partner wants out. A competitor has made an unsolicited approach. Or the company has reached a level where the owner knows the next chapter may require a different operator. In each of those situations, choosing the right connecticut business broker matters, but so does understanding the broker's limits. A broker can create momentum, manage outreach, and keep buyers engaged. Legal counsel makes sure the momentum doesn't carry you into a bad contract, a broken confidentiality process, or a closing structure that exposes you after the money changes hands.

That broker-lawyer relationship is where many sellers either preserve value or lose it. The strongest transactions are coordinated. The broker drives the market process. The attorney structures and documents the risk. The owner stays focused on keeping the business stable while both advisors do their jobs.

Defining the Broker's Role and When to Hire One

A business broker markets a business for sale, helps position it to buyers, screens prospects, coordinates information flow, and pushes the transaction toward a signed deal. That sounds simple until you live through a sale. In practice, the broker becomes the traffic manager for a process that can easily spin out of control if no one is controlling buyer access, timing, and expectations.

Connecticut has a real brokerage market, not a thin bench. Prominent firms include Sunbelt Business Brokers, which has facilitated over $100 million in transactions, while Inbar Group works with companies with revenues from $500,000 to $250 million, and Murphy Business Brokers operates as part of a large North American network. That breadth reflects a mature market for small and mid-sized transactions in Connecticut's $300+ billion GDP economy, according to ClientsIO's overview of Connecticut brokerages.

What a broker does, and what a broker doesn't do

Owners often blur the roles of a broker, M&A advisor, commercial real estate agent, CPA, and attorney. That creates problems early.

A broker is not your lawyer. The broker should not draft your definitive legal documents, advise you on indemnification language, interpret restrictive covenants, or make judgment calls about successor liability, creditor issues, consent requirements, or post-closing exposure. A broker is also not your tax advisor. If your sale structure has different consequences in an asset deal versus an equity deal, that analysis belongs with legal and tax professionals.

A commercial real estate agent handles the property side. If your business sale includes a lease assignment, landlord consent, or a real estate transfer, that piece may overlap with the transaction, but it isn't the same assignment. An M&A advisor may be the better fit for larger or more complex deals, especially where buyer outreach, financial packaging, and negotiation strategy need a deeper investment-banking style process.

Practical rule: If the question is about market positioning, buyer contact, screening, or managing deal flow, the broker usually owns it. If the question affects liability, tax treatment, legal rights, or enforceability, legal counsel needs to be involved.

The right moment to engage a Connecticut business broker

Waiting too long is common. Owners often call a broker after they've already spoken to a buyer, shared sensitive information informally, or formed unrealistic expectations about price.

The better time to hire a connecticut business broker is when one of these conditions is true:

- Retirement planning is becoming concrete. If you know you want out, you need enough runway to clean up records, address contract issues, and prepare for diligence.

- You've received an unsolicited expression of interest. That can be flattering, but one buyer without a market process rarely provides you with maximum bargaining power.

- The business depends too heavily on you. A broker can help you see how buyers will view key-person risk before you go to market.

- Your financial reporting is good enough to support a sale process. Buyers don't need perfection, but they do need a coherent story backed by usable records.

- You operate in a sector where discreet outreach matters. That often includes Connecticut manufacturing, healthcare-related businesses, distribution, and local service businesses where employees and customers may react badly to loose rumors.

Which businesses benefit most

Not every company needs a broker. Some very small deals are handled privately. Some larger deals belong with an M&A advisory firm. But many Connecticut companies sit in the middle. They're too substantial for a casual buyer-to-owner negotiation and too operationally specific for a generic listing approach.

These businesses often benefit most from broker involvement:

| Business type | Why broker involvement helps |

|---|---|

| Owner-operated service companies | Buyers need help understanding recurring revenue, staffing, and owner transition risk |

| Manufacturing businesses | Marketing, buyer screening, and confidentiality become more delicate |

| Healthcare-adjacent companies | Regulatory and operational questions make coordinated communication important |

| Retail and wholesale businesses | Buyer qualification matters because interest can be broad but uneven |

| Multi-location businesses | Process management gets harder as diligence expands |

A broker earns value when they create a controlled process. They lose value when they post a listing and wait.

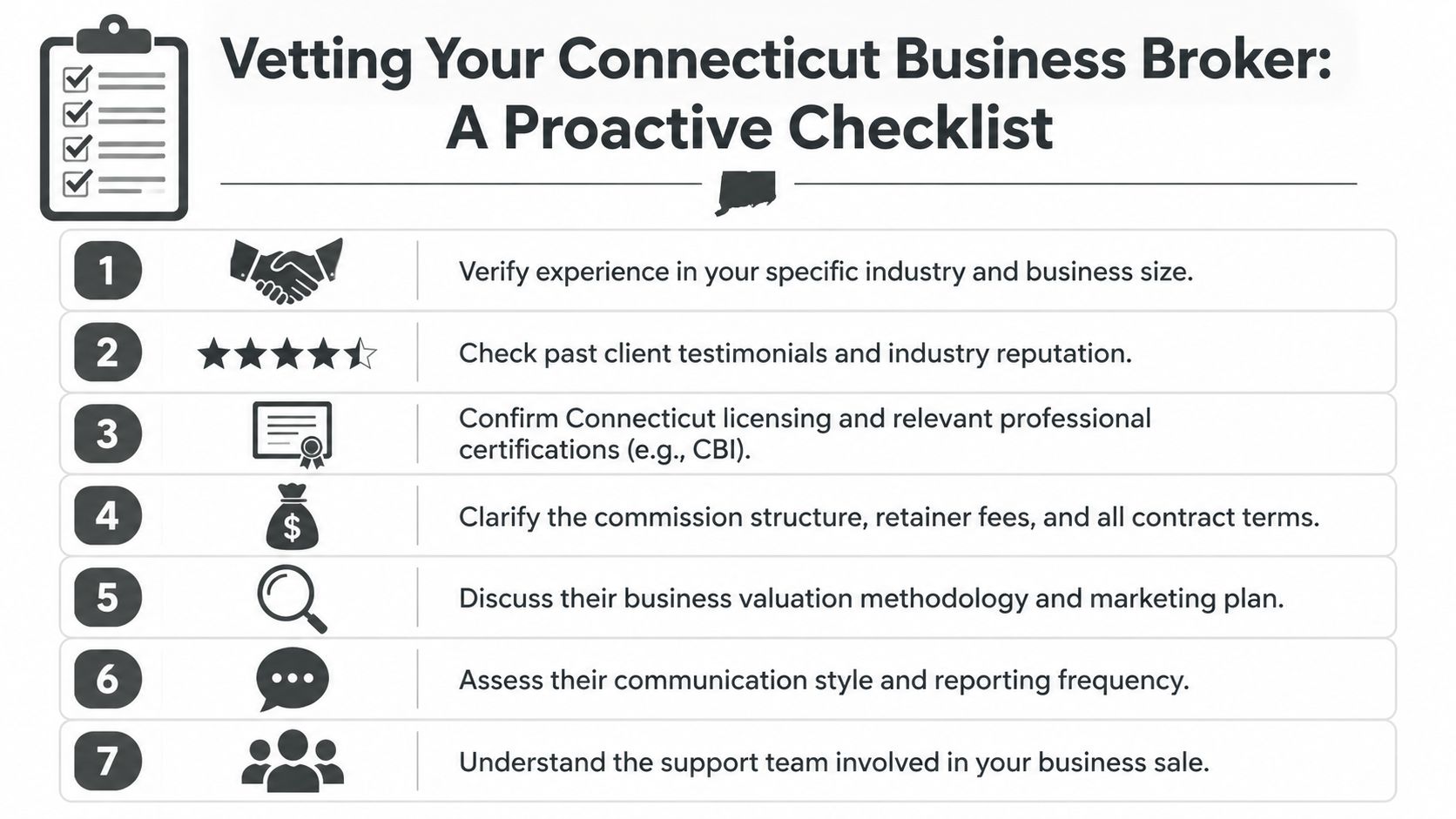

How to Vet a Connecticut Business Broker

Choosing a broker shouldn't feel like hiring a salesperson after one good meeting. You need evidence. A connecticut business broker may present polished materials, confident pricing, and a reassuring timeline. None of that tells you whether the broker can manage confidentiality, qualify buyers, survive a hard diligence phase, or close a deal that gets rough.

Start with skepticism. Healthy skepticism is not mistrust. It's due diligence.

Start with fit, not personality

A broker can be impressive and still be wrong for your business. The first question isn't whether you like them. It's whether they routinely handle businesses with your profile.

Look at three points together:

- Industry familiarity. A broker who understands manufacturing backlog, healthcare referral flow, route density, or customer concentration will ask better questions.

- Deal size alignment. If your company is small, a firm built only for larger transactions may under-serve it. If your business is more complex, a high-volume small-deal broker may not have the right process.

- Geographic reach. Connecticut is local in some respects and regional in others. A broker needs enough local awareness to market intelligently and enough reach to find serious buyers.

For niche sectors, it can also help to compare how specialized brokers position deals in adjacent markets. For example, owners in route-based businesses can learn a lot from resources discussing the best firms for selling routes, especially around buyer qualification and territory-specific valuation issues.

Ask for proof behind the pitch

The most abused phrase in the brokerage world is "success rate." It sounds objective, but it often isn't. A credible broker should be able to explain when they started tracking results, how they define success, and what happened to listings that never reached closing.

According to Morgan & Westfield's discussion of measuring broker success rates, you should demand year-by-year data and a clear definition of success. That source notes that a claimed 96% success rate is more credible if it is supported by over 25 annual listings, that reputable brokers may maintain 80-90% closure rates on listed deals, and that up to 70% of listings can fail because of overvaluation or due diligence issues.

That tells you what to ask. It also tells you what not to accept.

If a broker gives you one global percentage without the raw story behind it, treat that figure as marketing, not diligence.

Questions that reveal competence fast

Use questions that force specifics. A weak broker answers with broad confidence. A strong one answers with process.

- How do you define a successful listing? Count only closed deals, not signed letters of intent or listings that disappear.

- What happened to the last several listings that didn't close? This reveals honesty and pattern recognition.

- How do you screen buyers before releasing sensitive information? You want a disciplined confidentiality process, not curiosity-driven traffic.

- Who prepares the marketing package and who fields buyer questions? Some firms delegate heavily. That isn't always bad, but you should know who is doing the work.

- How often will I hear from you, and in what format? Sparse communication leads owners to interfere with the process or lose trust in it.

Verify the infrastructure around the broker

A business sale is rarely handled by one person alone, even if one broker is your lead contact. Ask who else touches the file. That includes analysts, buyer-screening staff, listing coordinators, and anyone drafting the confidential information package.

Then review the legal side of your own preparation. A seller who wants an advantage should have contracts, leases, corporate records, and employment documents organized before serious buyer diligence begins. If your due diligence foundation isn't ready, this due diligence overview for buying a business is also useful from the seller's side because it shows what a disciplined buyer will demand once they engage.

Watch for these warning signs

Some red flags aren't dramatic. They're subtle and common.

| Warning sign | Why it matters |

|---|---|

| The broker promises a price quickly | Fast valuation talk often means shallow analysis |

| They avoid discussing failed listings | That usually means weak tracking or selective disclosure |

| Their NDA process sounds casual | Confidentiality failures can damage operations |

| They speak as if legal issues are minor | That usually means they don't recognize where deals actually break |

| They overemphasize volume | High listing count doesn't prove high-quality representation |

The right broker won't promise certainty. They'll show discipline.

Decoding the Brokerage Agreement and Commission Structures

Once you've chosen a broker, the next risk point is the engagement agreement. Sellers often sign this document too quickly because it feels preliminary. It isn't. The brokerage agreement controls who has the right to market the business, when a fee is earned, how long the relationship lasts, and whether a commission may still be owed after the formal term ends.

That contract deserves the same care you would give a major customer agreement. If anything, it deserves more.

Exclusive versus open engagement

Most broker agreements are drafted as some form of exclusive right to sell. That usually means the broker is entitled to compensation if the business is sold during the engagement period, even if the owner located the buyer through some other channel. The broker wants that protection because they are investing time and market exposure into the process.

An open arrangement gives the seller more flexibility, but it often produces less broker commitment. When nobody has clear control over the sale process, buyer messaging gets messy, confidentiality becomes harder to protect, and disputes over who "procured" the buyer become more likely.

A practical review should cover:

- Scope of authority. Can the broker advertise broadly, contact named parties, or circulate information only under NDA?

- Owner restrictions. Are you free to pursue inbound interest independently, or must everything route through the broker?

- Trigger for commission. Is the fee earned only at closing, or can it be triggered earlier by a signed LOI or some other event?

Term, tail, and post-engagement risk

The term tells you how long the broker controls the assignment. The tail period is what catches sellers by surprise. A tail provision usually says that if a party introduced during the engagement later acquires the business after the agreement expires, the broker may still be entitled to compensation.

That concept is legitimate in principle. The negotiation issue is scope. The buyer list should be clear, the time period should be reasonable, and the trigger language should not be vague enough to cover remote or casual contacts.

Sellers should ask for a written, specific protected-buyer list at the end of the engagement, not a fuzzy claim that the broker "had discussions in the market."

The broker agreement also needs to define the broker's duties with enough precision to avoid misunderstandings. Marketing effort, confidentiality handling, reporting cadence, and seller cooperation obligations should be reasonably clear. Loose drafting creates avoidable conflict.

For owners who haven't recently reviewed commercial agreements, it can help to refresh the basic contract framework before negotiation. A practical starting point is this overview of a small business contract template, especially for understanding how defined obligations and termination language work in practice.

Commission structure and what to negotiate

Commission terms vary. Smaller business sales often use a percentage-based success fee. Some brokers also require a retainer, a minimum fee, reimbursement of marketing expenses, or a hybrid arrangement. For larger transactions, fee structures can become more layered.

What matters most isn't finding one "standard" number. It's understanding the economic incentives in your specific contract.

Review these points carefully:

- Success fee definition. Is the percentage applied to total consideration, cash at closing, assumed liabilities, earnout value, or seller note value?

- Minimum fee. This can matter if the deal size changes during negotiations.

- Retainer credit. If you pay an upfront amount, does it offset the final commission?

- Expense reimbursement. Marketing costs, travel, or document preparation charges should be spelled out.

- Transaction structure neutrality. The agreement should avoid rewarding the broker for deal structures that may be worse for you legally or economically.

A seller should never evaluate the commission in isolation. A lower fee paired with weak buyer screening, poor confidentiality controls, or sloppy process management can cost far more than the fee difference.

Navigating the Deal Workflow From Listing to Closing

A business sale usually feels orderly from the outside and turbulent from the inside. To the owner, the process often starts subtly. A few calls. A request for documents. A draft summary of the business. Then the tempo changes. Buyers begin asking sharper questions, the broker starts qualifying interest, and legal issues that seemed minor suddenly affect timing, price, or structure.

The first phase is preparation, not selling

Before a broker markets anything, the business has to be packaged coherently. That usually means financial normalization, a defensible narrative about operations, and a confidential information memorandum that presents the opportunity without casually exposing sensitive details.

Owners who haven't looked critically at their own reporting should do that early. Buyers will. A useful refresher is this practical guide to financial statements, especially for understanding how outsiders read balance sheets, profit-and-loss statements, and supporting schedules.

The broker's role here is to shape the market presentation. Legal counsel's role is different. Counsel should identify issues that can weaken the story later, such as unsigned contracts, assignability problems, old ownership irregularities, or compliance gaps buried in the records.

Marketing, NDAs, and buyer screening

Once the package is ready, the connecticut business broker begins outreach. Good brokers don't just chase volume. They qualify prospects before sensitive information moves. That means using NDAs consistently, controlling disclosures, and screening for financial capacity and seriousness.

The seller needs discipline too. Off-the-record disclosures create risk. So do side conversations with buyers that bypass the process. Every unscripted communication increases the chance of inconsistency, leaked information, or accidental commitments.

A controlled process usually looks like this:

- Blind outreach begins. Buyers see enough to identify the opportunity type, but not enough to identify the company.

- NDA execution follows. Access expands only after confidentiality obligations are in place.

- The broker manages early Q&A. Initial questions should be filtered and organized.

- Management contact is delayed. Direct access should come after buyer credibility is established.

A buyer who resists a disciplined information process during the first phase usually becomes harder, not easier, during diligence.

LOI stage and the shift in leverage

The first real turning point is the letter of intent. At that moment, broad market interest narrows into one proposed structure. That's also where many sellers make their first expensive mistake. They treat the LOI as a handshake document with minor significance.

It isn't minor. Even if much of it is nonbinding, the LOI frames price, structure, exclusivity, diligence access, timing, employment expectations, and post-closing obligations. Sellers should understand the commercial effect of every business term before they sign. This explainer on what a letter of intent means in a business transaction is a good primer for owners who want to see how an LOI can shape the rest of the deal.

Diligence and closing pressure

Once the LOI is signed, the buyer examines the business in detail. From the buyer's perspective, that means reviewing 3-5 years of financials, testing add-backs that may increase EBITDA by 10-30%, looking for customer concentration over 20%, and structuring financed offers with 10-20% down payments while negotiating items such as working capital adjustments, as described in Synergy Business Brokers' buyer-process overview.

For the seller, those figures translate into practical pressure points. Every add-back needs support. Every major customer relationship needs context. Every operational weakness that was easy to explain verbally now has to survive document review and buyer skepticism.

Here, the broker and attorney work best as complements:

| Stage | Broker's main job | Attorney's main job |

|---|---|---|

| Early buyer interest | Build momentum and qualify prospects | Protect confidentiality and prepare for diligence |

| LOI negotiation | Compare offers and manage buyer dynamics | Review exclusivity, structure, and legal exposure |

| Diligence | Keep requests organized and moving | Analyze contracts, consents, liabilities, and disclosure risk |

| Purchase agreement | Preserve deal momentum | Negotiate representations, indemnity, restrictive covenants, and closing mechanics |

Closings stall when owners try to improvise. They move when the process is coordinated.

Common Pitfalls and the Role of Legal Counsel

Most failed sales don't collapse because nobody wanted the business. They collapse because the seller, broker, and legal team were not aligned on who was handling risk, who was communicating with the buyer, and which issues needed to be fixed before they became points of contention.

Mistaking the broker for legal protection

A broker can be experienced, careful, and commercially sharp. That still doesn't make the broker your legal shield. Sellers get into trouble when they rely on brokerage advice for issues that belong in legal review.

Common examples include:

- Contract assignability. A buyer assumes key contracts transfer smoothly. They may not.

- Employment and restrictive covenant issues. Key staff may have no enforceable restrictions, or existing agreements may be outdated.

- Entity and ownership problems. Historic equity transfers, missing approvals, or poor recordkeeping can complicate closing.

- Post-closing liability. The purchase agreement may leave the seller exposed through broad indemnity or weak limitation language.

In each of those areas, delay diminishes negotiating power. If counsel gets involved only after the LOI is signed and diligence is underway, the seller may already be negotiating from a defensive position.

Letting confidentiality erode in practice

Owners usually understand confidentiality in theory. The problem is execution. A rumor about a sale can unsettle employees, trigger customer concern, and create openings for competitors. The broker helps control the outward process, but legal counsel helps build the underlying guardrails.

That includes reviewing NDA terms, controlling who gets access to what information, and establishing internal rules for document sharing and management presentations. Confidentiality isn't just about the buyer's promise not to talk. It's about limiting unnecessary exposure inside and outside the company.

Strong confidentiality practice is procedural. It depends on who has access, when they get it, and what happens if the deal falls apart.

Allowing valuation momentum to override deal quality

A seller may receive an attractive headline price and assume the hard part is over. Often the opposite is true. A high initial number can mask weak financing, aggressive post-closing adjustments, or indemnity terms that shift too much risk back to the seller.

Legal counsel doesn't replace the broker's market role. Counsel pressure-tests whether the economics are real once the contract language catches up to the business conversation.

A practical legal review often focuses on:

- Representations and warranties. Are they broad enough to create open-ended exposure?

- Indemnification structure. What claims survive, for how long, and subject to what limits?

- Earnouts and seller financing. Are payment triggers objective and enforceable?

- Restrictive covenants. Are non-compete and non-solicit obligations reasonable and tied to the actual transaction?

- Closing conditions. Can the buyer walk too easily, or delay without consequence?

Owners who want a closer look at that protective role should review how a business sales attorney supports transaction planning and closing.

Why proactive counsel changes outcomes

When legal counsel is engaged early, the seller usually gets better process discipline. The broker can market the opportunity more confidently because major legal defects have already been identified or addressed. The owner can answer buyer questions with less improvisation. The final negotiation becomes narrower because fewer problems surface late.

That isn't theoretical. It's how value is preserved in real deals. A connecticut business broker may bring the buyer to the table. Legal counsel helps make sure the terms on the table are ones you can safely accept.

Frequently Asked Questions About Business Brokers

Is a business broker the same as an M&A advisor

Not always. A broker usually focuses on marketing privately held businesses, screening buyers, managing inquiries, and helping move small to mid-sized deals forward. An M&A advisor often handles more complex transactions, broader buyer outreach, and deeper financial process management. The right choice depends on deal size, complexity, and the required attributes of the buyer universe.

Do I always need a Connecticut business broker to sell my company

No. Some owners sell directly to a known buyer, a partner, family member, or key employee. But a direct sale carries trade-offs. You may have less price tension, weaker buyer screening, and a less disciplined confidentiality process. If you're considering a sale without a broker, be realistic about whether you can manage outreach, filter buyers, and keep the business running at the same time.

How long does it take to sell a business

There isn't one reliable timeline that fits every transaction. The process can take many months, especially if financial records need cleanup, the buyer needs financing, or diligence surfaces legal issues. Owners make the timeline longer when they wait to organize records, delay responses, or sign an LOI before they understand the likely closing obstacles.

What should I prepare before meeting a broker

Prepare current financial statements, recent tax returns, key contracts, lease documents, ownership records, and a clear explanation of how the business operates without depending entirely on you. You don't need a perfect package on day one, but you do need enough information for a serious conversation about marketability and risk.

Should my lawyer talk to my broker

Yes. A coordinated broker-lawyer relationship usually leads to a cleaner process. The broker should know how legal issues may affect marketing and buyer messaging. The lawyer should understand how the broker plans to run the process so legal review supports, rather than slows, the deal.

Conclusion Your Strategic Partnership for a Successful Sale

Selling a business isn't just a pricing exercise. It's a coordinated legal and commercial process that tests your records, contracts, confidentiality practices, and negotiating discipline. The right connecticut business broker can create a credible market, manage buyer flow, and keep a deal moving. That matters. But it isn't enough by itself.

The strongest sales happen when the owner, broker, and legal counsel work as a team with distinct roles. The broker drives exposure and buyer engagement. The owner keeps operations stable and presents the business accurately. Legal counsel identifies structural risk, secures advantageous terms in the LOI and purchase agreement, and helps prevent a promising deal from becoming a costly mistake.

For many owners, this transaction represents years of work, reputation, and personal financial planning. That isn't the moment for vague responsibilities or improvised decision-making. It's the moment for careful broker selection, disciplined preparation, and legal review that starts early enough to matter.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.