A client mentions a private deal after a review meeting. A friend asks whether you can introduce a few accredited investors to a startup raise. A family member offers you a small piece of a real estate syndication and says it's outside your day job, so compliance doesn't need to know.

That's how many private securities transactions begin. Not with an obvious scheme, but with a conversation that sounds informal, personal, and manageable.

For financial advisors and registered representatives, that instinct is dangerous. What feels like a side opportunity can become a Rule 3280 problem, an internal investigation, a Form U5 disclosure issue, and, in the worst cases, a FINRA enforcement matter. The hard part is that many advisors don't get in trouble because they meant to evade the rules. They get in trouble because they misclassified the activity, underestimated how broadly FINRA reads participation, or waited too long to disclose it.

The Growing Risk of Private Securities Transactions

The modern advisor works in a market where private offerings are everywhere. Clients hear about private credit, private equity, private real estate deals, startup rounds, promissory notes, and friends-and-family raises long before they ever hit a public platform. That means off-platform opportunities show up in ordinary professional relationships, not just in fringe situations.

The scale of that market matters. Global private market assets under management reached about $15 trillion in 2024, with projections to exceed $18 trillion by 2027, according to S&P Global's private markets overview. For advisors, the takeaway is simple. More private capital means more chances to be approached about transactions your firm doesn't already supervise.

Why these situations escalate quickly

A private securities transaction problem usually starts with one of three mistakes:

- An advisor treats it like a favor: making an introduction, forwarding materials, or answering investor questions.

- The deal feels personal rather than professional: a friend's company, a client's side venture, or a local real estate project.

- The advisor assumes compensation is the trigger: when in reality the analysis is often broader than “Did I get paid?”

That's why private securities transactions create career risk disproportionate to how casually they often begin. The advisor thinks the issue is disclosure. The firm sees potential selling away, supervision failures, and customer risk.

Private securities transactions are rarely discovered at the moment of disclosure failure. They're usually discovered later, after emails surface, investors complain, money moves, or a questionnaire answer doesn't match the record.

The real-world professional risk

When firms investigate these matters, they don't just ask whether you sold something. They ask who you introduced, what documents you handled, what you said to clients, whether your communications used firm systems, whether you received or expected compensation, and whether the transaction should have been on the firm's radar earlier.

That's why advisors need to treat private securities transactions as a frontline career issue, not a technical compliance footnote. In practice, the line between an outside activity and regulated securities participation is where many careers get damaged.

Understanding FINRA Rule 3280 and Selling Away

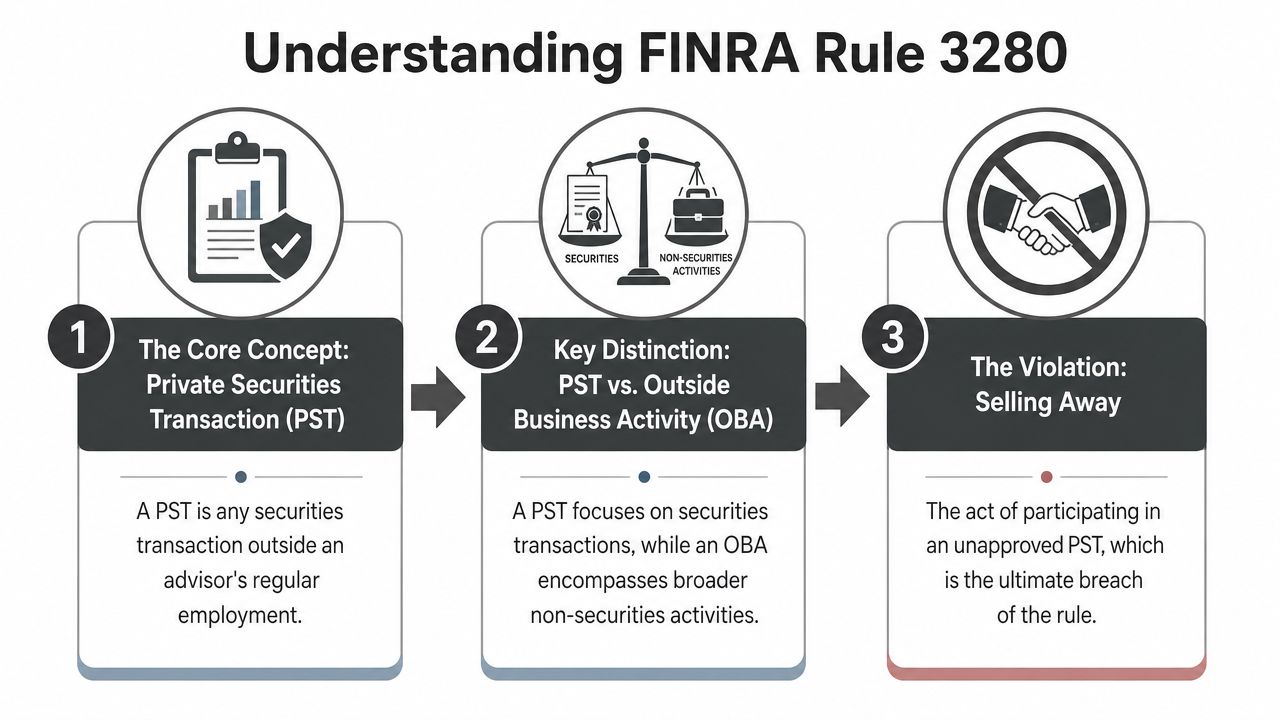

FINRA Rule 3280 is the starting point. It governs private securities transactions by associated persons.

“Private securities transaction” means any securities transaction outside the regular course or scope of an associated person's employment with a member. See FINRA Rule 3280.

That definition sounds compact, but it carries major consequences. If you intend to participate in a covered transaction, the rule requires prior written notice to your firm. If you may receive selling compensation, you must obtain written approval before participating.

What a PST is, and what it is not

An advisor's first analytical question should be this: is the activity a securities transaction, or is it some other outside business activity?

If the activity involves a securities transaction outside your firm, Rule 3280 is in play. If it's a non-securities side business, a different outside activity analysis may apply. Advisors often blur those categories, especially when the investment is packaged informally.

Here is the practical distinction:

| Activity type | Core question | Why it matters |

|---|---|---|

| Private securities transaction | Are you participating in a securities transaction away from the firm? | Rule 3280 may require notice, approval, supervision, and books-and-records treatment |

| Outside business activity | Are you engaged in outside work or a business role that is not itself a securities transaction? | Different firm processes may apply |

When the facts suggest the investment may be a security, don't rely on labels like “side deal,” “friends-and-family note,” or “real estate opportunity.” Labels don't control the regulatory analysis.

For a broader discussion of how securities-related misconduct gets framed in disputes and investigations, see this overview of securities fraud issues.

Participation is broader than most advisors expect

The phrase that catches people is “participating in any manner.” Advisors often think they are safe if they didn't formally recommend the product or didn't take a commission. That's not how firms or regulators typically analyze these situations.

FINRA risk guidance makes clear that firms are expected to detect possible PST activity through surveillance tools and that the rule can be triggered by participation in any manner. That broad reading is one reason firms increasingly invest in controls aimed at conflicts, communications, and employee activity patterns. Technology-focused compliance resources on preventing insider misconduct with AI are useful in that context because they reflect how modern firms think about surveillance, not just disclosure forms.

An advisor doesn't need to close the sale personally to create a Rule 3280 problem. Introductions, follow-up communications, capital-raising support, and deal facilitation can all become part of the participation analysis.

What “selling away” means in practice

“Selling away” is the phrase advisors know, but many use it too narrowly. In practice, selling away is the unapproved participation in a private securities transaction outside the firm. It's the conduct firms associate with hidden deal flow, off-platform fundraising, and customer exposure the firm didn't authorize or supervise.

That's why Rule 3280 matters so much. It isn't just a notice rule. It is a gatekeeper rule.

Navigating the Notice and Approval Process

The right time to disclose a potential private securities transaction is before you become involved in it. Not after the first investor meeting. Not after documents are circulated. Not after funds are committed.

What your written notice should cover

A usable notice should be specific enough for compliance to evaluate risk without having to reconstruct the deal from scattered follow-up emails.

Include at least these points:

The issuer or venture involved

Identify the company, fund, syndication, note program, or other vehicle.Your proposed role

State whether you plan to introduce investors, discuss the opportunity, circulate materials, attend meetings, answer questions, invest personally, or help with capital raising.Compensation details

Say whether you will receive compensation, referral fees, equity, profit participation, expense reimbursement, or anything else of value. If the answer is no, say no plainly.Who the potential investors are

Note whether firm clients, former clients, personal contacts, family members, or business associates may be involved.How the activity will occur

Explain whether communications will happen by email, text, calls, in-person meetings, pitch decks, or subscription materials.

What the firm is deciding

If compensation may be involved, Rule 3280 requires written approval before participation. If approved, the firm must treat the transaction as one it executed itself for supervision and recordkeeping purposes under the rule. That's the part many advisors miss. Approval isn't just permission. It can pull the activity into the firm's supervisory system.

A mature compliance process usually asks:

- Customer exposure: Are firm customers involved or likely to become involved?

- Conflict profile: Does the activity create divided loyalties, compensation conflicts, or misuse-of-position concerns?

- Operational impact: Will the advisor's outside involvement interfere with firm duties?

- Supervisory feasibility: Can the firm practically monitor and document the activity?

If you want a broader framework for how firms build these controls, this discussion of corporate compliance programs is a helpful complement to the Rule 3280 analysis.

A simple notice template

Use this as a starting point and adapt it to your firm's procedures:

Subject: Notice of Proposed Private Securities Transaction

I am providing prior written notice of a proposed activity that may constitute a private securities transaction. The issuer or investment vehicle is [name]. My anticipated role would be [describe role precisely].

I [will / will not] receive compensation or any other financial benefit in connection with this activity. If any compensation may be received, it would be in the form of [describe].

Potential participants may include [describe categories]. My anticipated communications or involvement would include [describe]. I have not participated in the activity pending the firm's review and any required approval.

What works and what doesn't

What works is early, overinclusive disclosure. What doesn't work is trying to simplify the facts because you think compliance will overreact.

Firms usually become more concerned when they learn the actual role later than when they see a complete disclosure at the start.

A few practical rules help:

- Disclose before contact expands: If you think you may speak with investors, disclose first.

- Use the firm's process: Don't rely on an informal conversation with a branch manager.

- Preserve records: Keep the notice, related communications, offering materials, and any firm response.

- Update the notice: If your role changes, your disclosure should change too.

Practical rule: If you're asking yourself whether the activity is “really” participation, you're already in territory where written notice is the safer move.

Common Compliance Pitfalls and Hidden PSTs

Most problematic private securities transactions don't look dramatic in real time. They look routine, social, or incidental. That's why the hidden cases are the ones that catch experienced advisors off guard.

The introduction that became participation

An advisor gets a call from a longtime friend launching a private company raise. The friend says, “I'm not asking you to sell it. Just connect me with a few people who might be interested.” The advisor makes introductions, forwards a deck, and joins a call to help “explain the opportunity.”

From the advisor's perspective, that may feel like networking. From a regulatory perspective, those acts can look like participation.

The finder's fee that was not “just a thank you”

Another advisor introduces a business owner to a private note offering. Later, the issuer offers a referral payment or a piece of equity “for helping open doors.” The advisor didn't see themself as selling anything. But once compensation enters the picture, the issue becomes much more difficult to defend.

Even when compensation never materializes, the facts still matter. FINRA's guidance on outside business activities and private securities transactions emphasizes that firms are expected to surveil for PSTs through tools such as questionnaires, email review, organizational documents, written supervisory procedures, and training. It also reflects that Rule 3280 can be triggered by participation “in any manner,” even without selling compensation.

The real estate deal that didn't feel like a securities issue

A representative joins a real estate syndication with several acquaintances. There's a manager, an operating agreement, and pooled capital, but no one uses securities-law vocabulary. Later, questions arise about who solicited whom and whether anyone associated with a member firm helped place the interests.

That's a classic pitfall. Advisors often assume “real estate” means “not securities.” Sometimes that assumption is wrong.

The personal investment that became a firm issue

A representative invests alongside a client in a private placement and discusses it casually over time. The advisor never thought of the investment as distribution activity because they were investing personally. But once the advisor's professional relationship intersects with the opportunity, the firm may view the matter very differently.

Here's where firms typically focus their review:

Who first raised the opportunity

Did the advisor bring it to a client, or did the client bring it to the advisor?What communications followed

Were there emails, texts, forwarded decks, subscription documents, or summaries?Whether the advisor's status mattered

Did the investor rely on the advisor's industry role, judgment, or access?How the activity was described internally

Did the advisor omit it from questionnaires or disclosures?

Advisors often defend these matters by saying, “I was only helping.” That phrase usually hurts more than it helps, because it concedes involvement while minimizing the regulatory significance of the conduct.

The lesson isn't that every outside investment is forbidden. It's that advisors need sharper instincts about when informal involvement starts to look like regulated participation.

Consequences of Non-Compliance and Form U5 Damage

When a firm discovers a possible PST issue, the first phase is usually internal, not public. Compliance, legal, or supervision staff gather emails, texts, attestations, account records, offering materials, and witness interviews. By the time the advisor is asked for an explanation, the firm often already has a working theory of the case.

That stage matters because it shapes everything that follows. If the firm concludes the advisor engaged in unapproved private securities transactions, the matter can move quickly from an internal review to termination, a Form U5 filing, and a referral or response to FINRA.

The Form U5 problem

For many advisors, the most immediate long-term damage isn't the first interview. It's the language that ends up on the Form U5.

A U5 that references selling away, unapproved private securities transactions, inaccurate compliance questionnaires, or customer-related outside investments can become the first thing a future firm notices. Recruiting slows down. Transitions become harder. Explanations have to be repeated in every serious conversation.

For a fuller discussion of how these disclosures affect careers, see this guide to Form U5 and FINRA issues.

How the dominoes fall

The progression often looks like this:

| Stage | What usually happens |

|---|---|

| Internal inquiry | The firm asks for documents, explanations, and interview participation |

| Employment action | Heightened supervision, leave, resignation pressure, or termination |

| Regulatory attention | FINRA requests information and reviews whether formal action is warranted |

| Registration fallout | U5 disclosures and later U4/U5 consequences affect future employment |

What makes private securities transactions especially damaging is that the fact pattern often invites secondary allegations. A firm may start by asking about an undisclosed transaction, then expand the review to questionnaires, customer communications, outside accounts, complaint handling, and the use of firm resources.

FINRA investigation risk

Once FINRA gets involved, the matter becomes more formal and more dangerous. The advisor may receive document requests, requests for on-the-record testimony, or other demands that require careful handling. Many advisors underestimate how much their first written response can shape the investigation.

A PST investigation is rarely just about one deal. Regulators and firms examine judgment, disclosure accuracy, supervision history, and whether the advisor can be trusted going forward.

Potential outcomes vary with the facts, but they can include fines, suspensions, or a bar from association with a FINRA member. Even where the matter doesn't end in the harshest sanction, the reputational and employment consequences can be severe.

The practical mistake is waiting to take the matter seriously until FINRA sends a formal request. By then, key records may be scattered, the firm may already have framed the issue negatively, and the U5 language may already be in motion.

Defense Strategies for FINRA Investigations

A private securities transaction investigation can still be defended effectively, but the defense has to start early and it has to be disciplined. Improvisation is usually what creates the worst record.

Start with an independent fact review

The first task is to build your own timeline before responding in detail. That means identifying every communication channel used, every investor contact, every offering document, and every compensation discussion, even if compensation was never paid.

Counsel should review the facts with the same questions the firm or FINRA will ask:

- What exactly did you do

- When did you first know the activity might involve a security

- Did any firm client or prospective client become involved

- What did you disclose, and when

- Are there questionnaire answers or attestations that now look incomplete

This review often changes the defense strategy. Some cases are best defended by showing the conduct never reached the level of participation. Others are better approached by acknowledging imperfect judgment while emphasizing the absence of intent, customer harm, or compensation.

Control the written record

Many advisors damage their position by sending quick explanatory emails to a branch manager, HR, or compliance. Those messages are usually drafted under stress, without full document review, and with phrasing that can later be read as an admission.

A better approach is deliberate and coordinated. In securities matters, written responses should be treated like advocacy, not casual correspondence. Where the matter is moving toward testimony or a formal response, advisors should understand the broader dispute framework, including proceedings discussed in this overview of the FINRA arbitration process.

Prepare for testimony and U5 negotiations

If the matter advances, on-the-record testimony preparation becomes critical. Advisors need to be able to explain the chronology, define their role precisely, and avoid careless shortcuts such as calling something “just a favor” or “not really an investment.” Those phrases often create more exposure than they remove.

There is also a separate but related defense track with the firm. If termination or resignation is on the table, counsel may be able to address the wording of the Form U5, the characterization of the conduct, and whether the record fairly reflects disputed facts.

The best defense posture is neither denial nor panic. It is a documented, credible narrative supported by records, consistent terminology, and disciplined responses.

What effective counsel actually does

In these matters, legal counsel can serve several practical functions at once:

- Fact development by gathering the complete record before the firm defines it for you

- Risk triage by distinguishing fixable disclosure failures from facts that suggest broader exposure

- Response management so emails, interview statements, and document productions don't create new problems

- Strategic negotiation with the firm over employment separation and U5 wording

Kons Law represents financial professionals in FINRA-related disputes and investigations, including U5 matters, arbitration, and regulatory defense. In the right case, that kind of focused counsel can help limit both the immediate damage and the long-tail career consequences.

Best Practices and the Future of Compliance

The strongest rule for advisors is simple. When in doubt, disclose early. Most PST problems become serious because the advisor waited, minimized, or tried to solve the issue informally.

A practical self-check

Before getting involved in an outside deal, ask yourself:

- Am I dealing with an investment that could be a security

- Will I introduce, discuss, circulate, explain, or facilitate the opportunity

- Could a client, former client, or prospect become involved

- Might I receive any benefit, now or later

- Would I be comfortable seeing the full fact pattern summarized by my firm on a U5

If any of those questions gives you pause, disclosure should happen before activity starts.

Training also matters, but only if it is concrete. Generic annual attestations don't fix much by themselves. Firms and advisors both benefit from examples, scenario analysis, and practical reinforcement. Resources on effective compliance training strategies are useful when they focus on recognizable fact patterns instead of abstract policy language.

What may change under proposed Rule 3290

Another issue advisors should watch is the proposed FINRA Rule 3290. As discussed in this analysis of the proposed rule change, the proposal is currently under consideration and would create a unified rule for outside activities. It could narrow reporting requirements toward “investment-related” conduct and change how some activities at unaffiliated advisers are classified.

That doesn't mean current obligations have disappeared. It means firms and advisors with hybrid business models should pay close attention to transitional risk. A changing framework often creates exactly the kind of confusion that leads people to misclassify conduct.

What actually works

The advisors who stay out of trouble usually follow a few habits consistently:

- They over-disclose rather than under-explain

- They treat introductions as potentially regulated conduct

- They keep personal investing separate from client-facing influence

- They answer questionnaires carefully and update prior disclosures when facts change

Private securities transactions remain one of the clearest examples of a preventable securities compliance problem that can still derail a career when handled casually.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.