An unpaid invoice can turn into a financing problem fast. A Connecticut contractor finishes a job, a supplier ships materials, or a business extends credit on agreed terms, and then the payment stops. Payroll still has to run. Vendors still need to be paid. The debtor may promise to “get this cleared up next week,” but your advantage wanes every day you wait.

That's where a lien becomes practical, not theoretical. A lien is a legal claim against property that secures payment of a debt. Used correctly, it changes the conversation from “please pay me” to “you now have a title, asset, or financing problem that has to be addressed.”

For Connecticut creditors, the most common business-related categories are straightforward in concept even if the rules are exacting in application. A mechanic's lien is the tool construction participants use to secure payment tied to improved real estate. A judgment lien comes after you've already won in court and want to attach that judgment to real property. A commercial lien often refers, in practice, to a security interest in business assets, commonly perfected through a UCC filing against personal property rather than real estate.

Each one serves a different purpose. Each one has different prerequisites, filing locations, and enforcement consequences. And if you're trying to understand how to file a lien in Connecticut, the hardest part usually isn't finding a form. It's choosing the right remedy, meeting the correct deadline, and preparing a filing that will hold up when the other side starts looking for defects.

Securing Your Right to Payment in Connecticut

A lien matters most when ordinary collection pressure has stopped working. The owner won't release funds. The developer says the draw is delayed. The borrower has assets on paper but no urgency to pay. At that point, the question isn't whether you're owed money. It's whether you can secure that claim in a way that affects the debtor's property rights.

A lien does exactly that. It puts a legal encumbrance on identified property, which can complicate a sale, refinance, or other transfer until the debt is resolved. That's why creditors often care as much about lien strategy as they do about the underlying invoice. If you'd like a broader grounding in where liens fit within creditor remedies, the concept overlaps with what it means to be a secured creditor.

The three business situations that come up most often

In Connecticut practice, these are usually the categories worth separating at the outset:

| Lien type | What it attaches to | Typical use case |

|---|---|---|

| Mechanic's lien | Improved real estate | Unpaid construction, labor, services, or materials |

| Judgment lien | Real property | You already obtained a court judgment |

| Commercial or UCC lien | Personal property such as equipment, inventory, or receivables | A secured transaction or commercial credit arrangement |

The mistake well-informed clients make isn't usually ignorance. It's assuming these remedies are interchangeable. They aren't.

What a lien does, and what it doesn't

A lien offers a strategic advantage. It's not self-executing payment. Filing one can create serious pressure because owners, lenders, and buyers dislike clouds on title and disputes over asset priority. But the lien only helps if it fits the debt, the property, and the procedural rules governing that type of claim.

Practical rule: The right lien on the wrong asset is nearly as ineffective as no lien at all.

That's why Connecticut creditors should approach lien rights backward from the asset. Start with what the debtor owns, then ask what legal vehicle reaches it. Real estate claims and personal property claims travel through different systems, involve different records, and create different enforcement paths.

Determining Your Eligibility to File a Lien

Before preparing anything, decide whether you have lien rights. That sounds obvious, but many failed filings start with an eligible debt and an ineligible claimant, or an eligible claimant using the wrong procedure.

Mechanic's lien eligibility turns on the work and the relationship

For construction-related claims, the most reliable workflow is still the basic one described in this industry guide on mechanics lien filing steps: verify lien rights under the applicable statute, gather the contract and proof of work, serve any required preliminary notice, complete the lien form with the unpaid amount and a precise property description, record it in the correct office, and serve the owner and any other required parties.

That sequence is useful because it highlights the threshold issue first. Verify lien rights before you draft anything. In Connecticut, that usually means confirming that the labor, services, or materials furnished are the kind the statute protects, and that your contractual position supports the claim. General contractors, subcontractors, and suppliers may all have plausible claims in the right circumstances, but “plausible” is not the same as “perfectible.”

If your transaction concerns personal property rather than improved real estate, you may not be dealing with a construction lien at all. In that case, the better frame is often a secured transaction and a UCC filing, which is discussed in this overview of how to file a UCC lien.

Judgment liens require a prior judgment

A judgment lien is different in kind. You don't get one because someone owes you money. You get one because you already reduced that debt to a court judgment and then took the additional step of attaching that judgment to real property. If you skip the lawsuit and move straight to filing, you're using the wrong remedy.

That distinction matters in negotiations. A client may say, “We have a signed contract and unpaid invoices, so let's file a lien on their building.” Sometimes that means a mechanic's lien. Sometimes it means no present lien right at all, at least not until litigation produces a judgment.

Don't collapse different lien concepts into one

If you want a simple outside reference that distinguishes among common real estate liens, it's useful as a classification tool. The practical takeaway is that the word “lien” covers several legal mechanisms, and Connecticut creditors should be careful not to import the rules of one type into another.

A valid debt doesn't automatically create a lien right. The legal path depends on the asset, the statute, and whether your claim arises from work, contract, or judgment.

Eligibility analysis isn't paperwork. It's strategy. If you get this part wrong, everything that follows is built on a defective assumption.

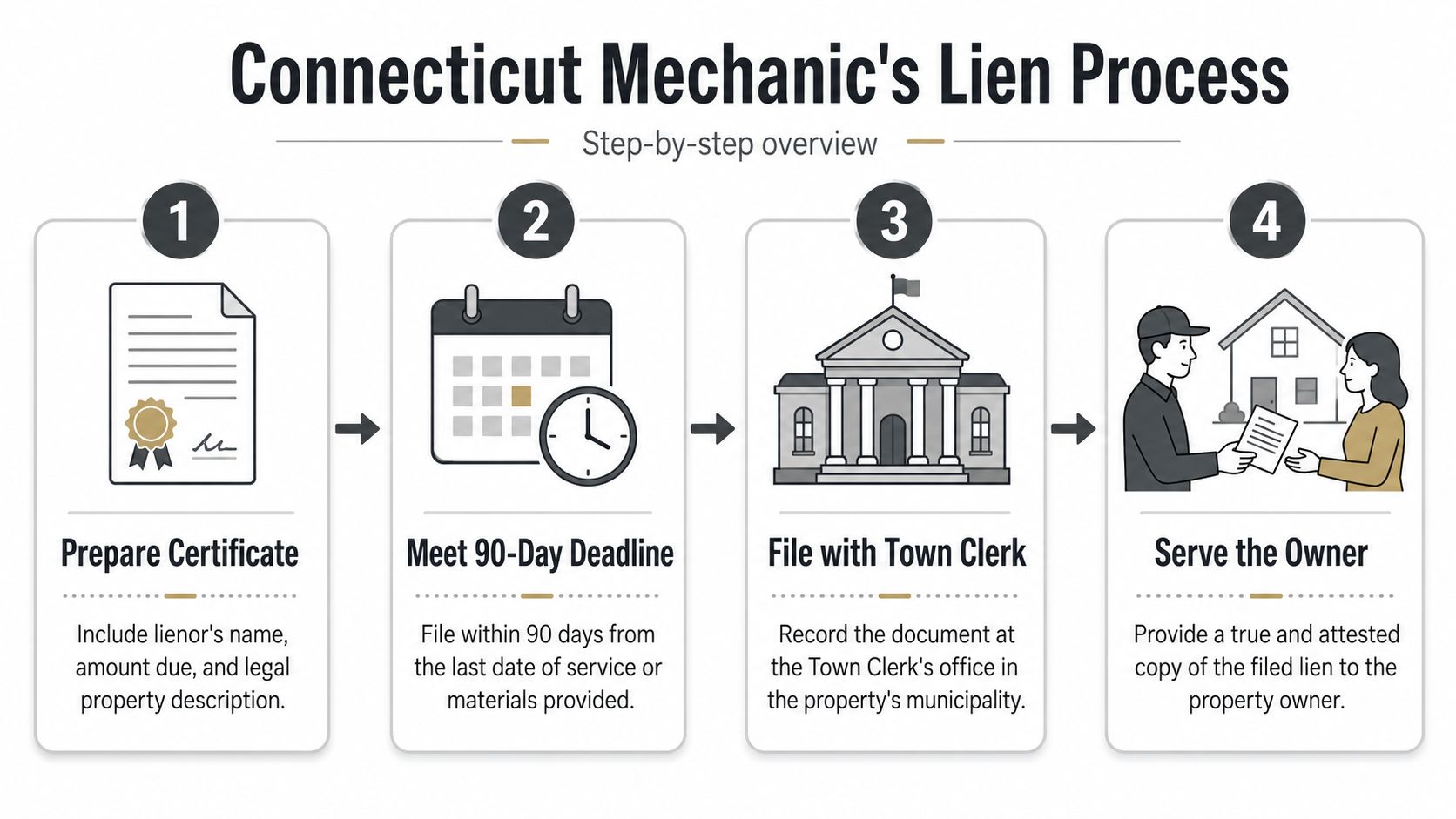

The Connecticut Mechanic's Lien Process Step by Step

For unpaid construction claims, the mechanic's lien is usually the most direct pressure point available. But it only works if you treat it as a precision filing. Courts don't usually rescue a claimant who was roughly correct.

Start with the certificate, not the argument

The content of lien filings tends to be highly standardized across jurisdictions. One statutory example from Florida requires the lienor's name, the contracting party, a description of labor or materials, the legal property description, the owner's name, key dates, and the unpaid amount, illustrating the broader point that lien success depends on exact content, correct office selection, and proper fees and timing, as reflected in this discussion of statutory lien content and filing requirements.

That principle applies directly in Connecticut. If you're filing a mechanic's lien here, prepare the certificate as though an adversary will review every word looking for a defect, because that's exactly what happens when the owner decides to challenge it.

Your draft should accurately identify:

- The claimant who furnished labor, services, or materials

- The amount claimed as unpaid

- The property with a precise legal description, not a casual street reference

- The owner and relevant contracting party, stated consistently with your underlying documents

A certificate that overstates, misidentifies, or describes the wrong parcel creates trouble that's often impossible to fix later.

Treat the deadline as immovable

Connecticut creditors often lose their advantage by waiting until settlement talks fail. That's backwards. Calendar the filing deadline as soon as payment trouble appears.

For mechanic's liens, timing is unforgiving. If your right depends on the date labor or materials were last furnished, you should identify that date early, preserve proof supporting it, and draft backward from the recording deadline. Last-minute filing invites errors in property description, ownership information, and service.

File from a checklist, not from memory. Lien rights are lost on administrative mistakes as often as on legal disputes.

Record in the right office and complete service correctly

A mechanic's lien on Connecticut real estate is recorded in the Town Clerk's office for the municipality where the property is located. That filing location matters. A properly prepared certificate filed in the wrong place doesn't secure the claim against the property you intended to reach.

After recording, service matters too. The filing process is not complete just because the document is on record. The owner must receive the required copy through the proper method. Service mistakes are common because claimants focus on recording and treat notice as an afterthought.

For a more focused discussion of this remedy, this resource on filing a mechanics lien is useful if your dispute is squarely in the construction context.

A practical working checklist

When clients ask how to file a lien in Connecticut construction matters, this is the shortest accurate answer:

- Confirm that the claim qualifies under Connecticut mechanic's lien law.

- Collect the contract file including invoices, change orders, delivery records, and proof of work.

- Draft the certificate carefully with the correct parties, amount, and legal property description.

- Record it with the proper Town Clerk in the municipality where the property sits.

- Serve the owner properly with the required copy and preserve proof of service.

What works is disciplined preparation. What doesn't is treating the lien as a pressure letter you can clean up later. You usually can't.

Filing Judgment and Commercial Liens in Connecticut

A supplier wins a Connecticut contract case, but the debtor still does not pay. A lender has valid loan documents, but the borrower's value sits in equipment and receivables, not real estate. Those are different collection problems, and the filing strategy needs to match the asset you are trying to reach.

Judgment liens reach real property after court

A judgment lien applies after you already have a money judgment and want that judgment to attach to the debtor's Connecticut real estate. The sequence matters. You do not use a judgment lien to prove the debt. You use it to improve your position once the court has already ruled in your favor.

In practice, the value of the lien depends on the property. A judgment lien against heavily mortgaged real estate may create settlement pressure but little immediate recovery. A lien against property with equity can affect a sale, refinance, or title review and give the creditor real negotiating power. For the Connecticut procedure, filing requirements, and effect on title, see this guide to a judgment lien on real estate in Connecticut.

Timing and accuracy both matter here. Before recording anything, confirm the debtor's exact name, confirm the judgment details, and confirm that the debtor owns the property you plan to encumber. Creditors often spend money recording a lien against property that is jointly owned, already overencumbered, or no longer in the debtor's name. That is a collection decision, not just a paperwork issue.

Commercial liens on personal property usually mean UCC filings

For business assets other than real estate, the usual tool is a UCC-1 financing statement. That filing is common in equipment finance, inventory lending, secured vendor arrangements, and deals where accounts receivable serve as collateral.

The strategic difference from a judgment lien is important. A UCC filing usually arises from a security agreement made before default, not from winning a lawsuit after default. If the paperwork was done correctly at the front end, the creditor may already have a secured position in the borrower's personal property. If it was not, filing late may not fix the problem.

Connecticut creditors should pay close attention to collateral description, debtor naming, and filing location under the UCC system. Small errors can create large priority disputes. A trade name instead of the debtor's legal name, an overbroad or vague collateral description, or a lapse in continuation can leave a creditor unsecured at the moment priority matters most.

Choosing the right lien for the asset

Use this framework before you file:

| If your goal is to reach | Typical tool |

|---|---|

| Connecticut real estate tied to unpaid construction work | Mechanic's lien |

| Connecticut real estate after winning a lawsuit | Judgment lien |

| Business assets such as inventory, equipment, or receivables | UCC filing or other secured transaction remedy |

The main risk in this area is a category error. Creditors sometimes try to force a construction dispute into a commercial filing strategy, or assume a court judgment automatically reaches business assets without an additional enforcement step. It does not.

Kons Law handles creditors' rights, commercial disputes, and filing strategy in this area. That can matter where the best path is not a single lien, but a coordinated approach involving suit, judgment enforcement, and secured-creditor remedies.

Critical Mistakes That Can Invalidate Your Lien

The most common assumption I see is that a lien is valid if the debt is real. That's not how courts treat lien claims. A lien can fail even when the invoice is justified.

The defects that cause the most damage

Some mistakes are obvious only after the other side attacks them:

- Wrong property description. If the parcel is described inaccurately, the lien may be misindexed or challenged as ineffective.

- Missed preliminary notice. In jurisdictions that require it, skipping a mandatory pre-lien notice can invalidate the claim altogether, as noted in the earlier discussion of the mechanics lien workflow.

- Filing in the wrong office. A proper document recorded in the wrong place still leaves you unsecured.

- Unsupported amount claimed. If you can't trace the number to contracts, invoices, change orders, and proof of service, the claim becomes vulnerable.

Louisiana's Private Works Act is a useful illustration of the larger principle. It requires a written, signed lien statement that reasonably identifies the property and owner and includes the outstanding amount plus a reasonable itemization of that amount, as discussed in this analysis of strict lien form and content defects. The point for Connecticut creditors is not that Louisiana law controls here. It's that courts often care intensely about form, identification, and itemization.

Owners can attack a bad lien quickly

A flawed lien doesn't just sit there until foreclosure. In some jurisdictions, the owner can move aggressively to strike it. Washington law is a strong example. It allows an owner, contractor, lender, subcontractor, or claimant to ask the superior court to declare a lien frivolous, made without reasonable cause, or clearly excessive, with an expedited hearing set no earlier than 6 and no later than 15 days after service under Washington's lien challenge procedure.

A lien that looks aggressive on paper can collapse quickly if the amount is overstated or the supporting documents are weak.

Connecticut creditors should take that lesson seriously even when the challenge mechanism differs. If your filing reads like a tool for influence without proof, you invite immediate motion practice, fee exposure, and lost negotiating credibility.

What disciplined claimants do differently

The strongest liens are usually boring. The amount is documented. The dates line up. The property description was pulled carefully. The service record is preserved. Nothing is inflated in an attempt to create settlement pressure.

What doesn't work is trying to convert a business dispute into a title problem before the file is ready. Precision is the strategy.

What to Do After Your Lien Is Filed

Once the lien is recorded, the strategic phase begins. That's when many creditors either become too passive or too aggressive. Both are mistakes.

Use the lien to negotiate from a stronger position

A recorded lien often changes who gets involved. Owners who ignored invoices may call immediately. Lenders start asking questions. Title companies raise exceptions. Buyers may hesitate. That doesn't guarantee payment, but it puts the debt into a context the other side can't ignore.

In such cases, a measured demand can work well. You already have the encumbrance in place. Now you use it to frame a short path to resolution, usually payment, payoff terms, escrow, or another documented arrangement.

In real estate-heavy markets, lien exposure also matters to investors evaluating transaction risk. If you follow broader market commentary, even forward-looking pieces such as these insights from InvestorMode on 2026 investing underscore why title clarity and asset-level encumbrances remain central to deal execution. From a creditor's perspective, that's why a properly filed lien can provide significant influence disproportionate to the filing effort.

Calendar enforcement immediately

A recorded lien is only a means of influence unless it is timely enforced. One neutral industry guide notes that foreclosure action is typically required within about 6 months to 1 year, depending on the state, and missing that deadline can destroy enforceability, as explained in this discussion of lien enforcement timing.

That rule captures the central post-filing reality. Once the lien is in place, you should track at least these items:

- Negotiation window so settlement efforts don't drift

- Enforcement deadline for foreclosure or equivalent action

- Release process so the lien is removed promptly once paid

The filing date is not the finish line. It starts the next calendar.

For Connecticut creditors, that means building the litigation plan early. If payment doesn't arrive, you need to be ready to foreclose or take the next enforcement step before the lien loses force.

Release the lien properly once paid

When the debt is resolved, clear the record. A satisfied lien that remains on title can create avoidable disputes and, in some cases, expose the claimant to unnecessary risk. The release should be handled with the same care as the original filing because sloppy closeout undermines your credibility in the next matter.

Some disputes can be managed internally. Others shouldn't be. If the lien is contested, the amount is substantial, the property description is uncertain, multiple creditors are involved, or foreclosure is becoming likely, legal help is no longer optional. If you've filed a lien and need to take the next step, or if you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you need guidance on how to file a lien in Connecticut, enforce a recorded claim, or evaluate whether a mechanic's lien, judgment lien, or UCC filing is the right creditor remedy, contact Kons Law at (860) 920-5181.