You've filed the paperwork for a new company, opened a bank account, and started using “LLC” after the business name. Then the terminology starts to blur. Are you the owner, a partner, a shareholder, a manager, or a member?

For an LLC, the answer is straightforward. The owner is called a member. That sounds simple, but the label matters because it ties directly to your rights, your tax treatment, your authority inside the company, and the limits of your personal liability.

That question comes up often with Connecticut founders, family businesses, real estate investors, and small operating companies. They usually aren't looking for a vocabulary lesson. They want to know who controls the business, who gets paid, who signs, what happens if someone leaves, and whether personal assets are protected if a dispute or debt problem arises.

Starting Your Business The Role of the LLC Member

If you're forming a business and asking what is a member in an llc, you're already at an important decision point. In an LLC, the owners are formally known as members, not shareholders and not partners. That terminology reflects the LLC's hybrid structure. It borrows limited liability concepts from corporate law and flexibility from partnership law.

LLCs have become a dominant choice for small businesses for good reason. The IRS notes that there are approximately 21.6 million active LLCs in the United States, accounting for nearly 43% of all small businesses, and the U.S. Census Bureau reported 5.6 million new business applications in 2025, a 7.7% rise from 2024. LLCs make up a significant share of those formations, according to the IRS overview of limited liability companies.

For a Connecticut business owner, the practical point is this. Once you become a member, you're not just holding a title. You're stepping into a legal and economic role that should be defined carefully from the outset.

A quick definition from a form website usually won't answer the questions that matter in practice. Founders often use drafting tools and planning resources early in the process, and something like TheLawGPT can help people organize their thinking around business documents. But the actual structure of your ownership and governance still needs to fit your company, your co-owners, and Connecticut law.

If you're still in the formation stage, it helps to review the mechanics before filing anything final, especially if more than one owner is involved. A practical starting point is understanding the Connecticut formation process itself, including the filing and governance issues discussed in this guide to LLC formation in Connecticut.

The Fundamental Role of an LLC Member

A member is an owner with an equity interest in the LLC. That ownership interest usually carries a right to profits, a share of losses, and some level of voting or management authority. The exact scope depends on the operating agreement, not just on assumptions made at the beginning of the business.

Why the term member matters

The easiest way to understand the role is to compare it to two familiar models.

A corporate shareholder owns part of a corporation but often has limited day-to-day control unless that shareholder also serves as an officer or director. A partner in a general partnership may have direct management authority, but that role can also carry broad personal exposure for business obligations.

An LLC member sits in the middle of those models. The member owns part of the company like a shareholder, but the member may also participate directly in running the business, more like a partner. That mix is what makes LLCs attractive to closely held businesses.

Members are owners. Employees, bookkeepers, consultants, and even founders who help launch the company are not members unless the company documents actually grant them membership interests.

Who can be a member

LLCs are flexible about ownership. Members can be individuals, corporations, other LLCs, trusts, or non-U.S. residents, which is one reason LLCs are used in everything from family companies to layered investment structures, as explained by LLC University's discussion of LLC members.

That flexibility creates opportunity, but it also creates complexity. If one LLC owns another LLC, or a trust holds the ownership interest, the company needs clean internal records and clear drafting on authority, transfers, and succession. Otherwise, people end up fighting over who can vote, who can sign, and who is entitled to distributions.

Ownership is not the same as job title

A member may work in the business every day, or may function more like a passive investor. By contrast, someone can hold an important operational title without owning any part of the company.

That distinction matters in real life:

- A founder may not be a sole owner if another person was granted a membership interest.

- A manager may not be a member if the LLC uses outside management.

- A spouse or investor may be a member even if that person never comes into the office.

For that reason, businesses should never rely on verbal understandings alone. If ownership exists, it should be documented clearly and consistently in the operating agreement and related records.

Exploring the Rights and Duties of LLC Members

Being a member comes with benefits, but it also brings real obligations. Most disputes in closely held companies aren't about the label itself. They arise because the members never defined what ownership means in practice.

Financial rights and access rights

A member usually expects to share in the economic upside of the business. That can include profit allocations, distributions when approved, and access to certain company information needed to understand the company's finances and governance.

The operating agreement should answer questions such as:

- How profits and losses are allocated

- When distributions may be made

- Whether distributions follow ownership percentages or a negotiated formula

- What records members may inspect

- What happens if one member contributes more money later

If those issues aren't addressed, disagreements tend to appear when the business starts making money, not when everyone is optimistic at the start.

Practical rule: Members should know the difference between having a right to share in profits and having a right to immediate cash. Those are not always the same thing.

Management rights and voting power

Some LLCs give all members voting authority on major business matters. Others centralize control in a manager or management group. Either way, major decisions should be spelled out with care.

Examples include:

- Admitting a new member

- Borrowing significant funds

- Selling major assets

- Changing tax elections

- Merging, dissolving, or winding down the company

In a small Connecticut business, informal decision-making often works until it doesn't. The first serious disagreement tends to expose how little structure was in place.

The liability side matters just as much. The liability shield operates on a ring-fencing principle. Members generally cannot be held personally liable for company debts, judgments, or acts committed by other members or employees. But that protection can be lost if the company fails to maintain separate entity status or if a member personally guarantees an obligation, as discussed in Clemta's explanation of LLC member liability and operating agreements.

A personal guaranty can bypass the comfort many owners think the LLC name automatically gives them.

If a creditor is pursuing a member's economic interest rather than the company's assets, the legal remedy may involve a charging order. For Connecticut businesses and creditors alike, that issue is easier to understand with a working knowledge of what a charging order is.

Duties members owe

Members also need to think about conduct, not just entitlements. In many LLCs, especially closely held ones, members owe duties tied to loyalty, care, honesty in dealing, and compliance with the governing agreement.

What tends to go wrong?

- Self-dealing transactions where one member benefits without disclosure

- Using company opportunities personally instead of offering them to the LLC

- Poor recordkeeping that blurs the line between company and personal assets

- Unapproved withdrawals from the business account

- Side agreements that conflict with the operating agreement

A well-drafted operating agreement won't eliminate conflict, but it gives the business a framework for resolving it before litigation becomes the only path left.

Member Types and Common Management Structures

The next question after ownership is control. Not every member has the same role in daily operations, and not every LLC should be run the same way.

Single-member and multi-member LLCs

A large share of LLCs are solo-owned. Approximately 64 to 70% of all LLCs are single-member entities, while 20 to 23% have exactly two members and only 13% have three or more, according to Business Initiative's LLC size statistics. The same source notes that the IRS places no limit on the number of members, and LLCs represented 72.7% of all U.S. partnership returns in Tax Year 2023.

For a single-member LLC, governance is simpler. One owner makes the calls, takes the risk of bad decisions, and usually doesn't need elaborate voting mechanics. But solo owners still need clean records and thoughtful operating terms because lenders, courts, and counterparties often examine whether the owner treated the LLC as a separate business.

A multi-member LLC is where careful drafting becomes essential. The moment two or more people own the company, you need a system for deadlocks, buyouts, capital calls, authority limits, and exits.

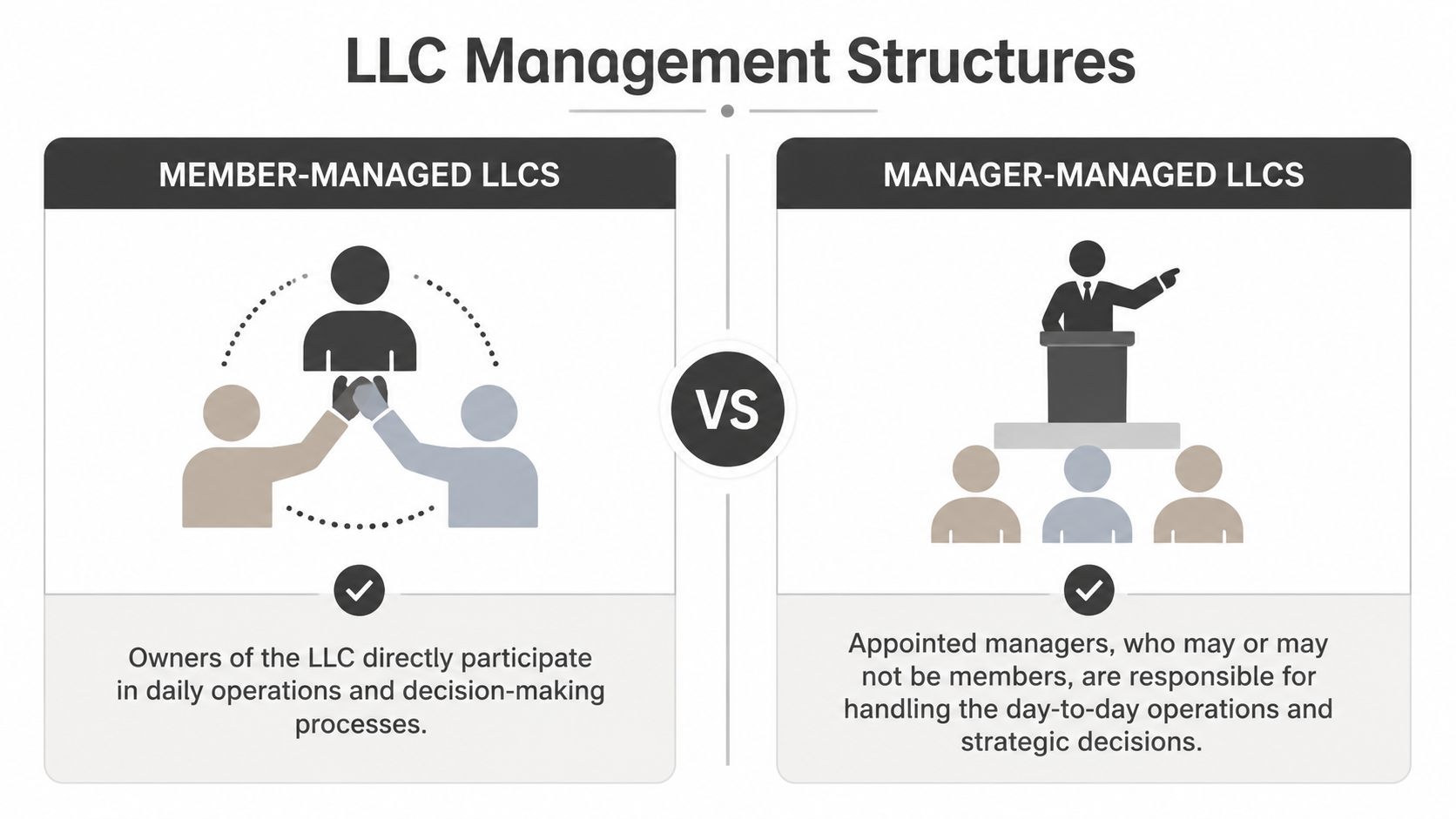

Member-managed versus manager-managed

These two models create very different businesses.

| Structure | Who runs daily operations | Best fit |

|---|---|---|

| Member-managed LLC | The members directly handle operations and decisions | Small owner-operated businesses |

| Manager-managed LLC | Appointed managers run the business, whether or not they are members | Businesses with passive owners, investors, or layered leadership |

In a member-managed LLC, each member typically has a direct role in operations. This works well for small professional firms, family businesses, and startup ventures where the owners are actively involved.

In a manager-managed LLC, authority is delegated. That can be one member, a non-member executive, or a defined management group. This structure is often better when some members are investors rather than operators.

Businesses run into trouble when they choose a manager-managed structure on paper but keep acting like everyone has equal day-to-day authority.

What works and what doesn't

A member-managed model usually works when:

- The owners trust each other

- The business is operationally simple

- Decision-making needs to be quick

- Everyone expects to stay active

A manager-managed model often works better when:

- Some owners are passive

- The company has multiple locations or departments

- One person has stronger operating expertise

- The members want tighter signing authority

What doesn't work is a mismatch between the paperwork and the actual business. If vendors, employees, and lenders are hearing directions from five different people, the company doesn't have a governance model. It has a risk problem.

For a closer look at one of these structures, this discussion of a member-managed limited liability company is a helpful companion.

How Ownership Interests and Taxation Work in an LLC

Ownership in an LLC isn't measured by stock certificates. It's usually expressed as a membership interest, often stated as a percentage or units defined in the operating agreement.

How membership interests are created

A member's ownership stake is typically tied to a capital contribution. That contribution may consist of cash, property, or services if the company agreement allows it. The agreement should say what each member contributed, what percentage or units each member received, and whether future contributions are mandatory or optional.

That sounds basic, but many ownership disputes start with an undocumented promise. One person says, “I was supposed to get a third.” Another says, “You were getting profits only after you hit certain milestones.” Without a written agreement, those arguments become expensive very quickly.

Key drafting points include:

- Initial ownership percentages

- Whether sweat equity is recognized

- Rules for dilution

- Transfer restrictions

- Buyout terms if a member exits, dies, or becomes disabled

Because LLC members can be individuals, corporations, other LLCs, trusts, or non-U.S. residents, ownership can become layered fast. That flexibility is useful in transaction planning, but it also requires explicit rules on withdrawal, dissociation, and transfer to preserve continuity, as noted in the earlier LLC member overview from LLC University.

How the default tax rules generally work

Tax treatment is one of the main reasons people choose LLCs.

Under default federal tax rules, a single-member LLC is generally treated as a disregarded entity unless it elects corporate tax treatment. A multi-member LLC is generally taxed as a partnership. In both cases, profits and losses typically pass through to the owners instead of being taxed first at the entity level under the default regime.

That pass-through framework is attractive, but business owners shouldn't reduce the issue to “LLCs avoid taxes” or “LLCs are always simpler.” The real analysis depends on how the company earns revenue, how members are compensated, whether profits are distributed, and whether a corporate election makes sense for the specific business.

If the operating agreement doesn't match the tax reporting position, the accounting work gets harder and the dispute risk rises.

For many owners, it makes sense to coordinate the legal and accounting sides together rather than treating them as separate projects. If a business needs help evaluating member compensation, entity classification, and reporting processes, a directory like Hire Tax Accountants can be a useful starting point for finding tax support.

Ownership does not mean direct ownership of company assets

Members own an interest in the LLC itself. They do not directly own each item of LLC property. That distinction matters in financing, litigation, divorce, probate, and collections matters.

A business owner may say, “I own half the building because I own half the LLC.” Legally, the LLC owns the building if title is in the LLC's name. The member owns a membership interest, not the underlying asset. That difference becomes very important when someone wants out, a creditor shows up, or the company needs to refinance.

Essential Guidance for Connecticut LLCs

For Connecticut companies, the generic national advice on LLCs only gets you so far. State law controls the formation and internal operation of the entity, and that means the operating agreement must fit Connecticut realities rather than a one-size-fits-all template.

Why generic templates often fail

A downloadable form may look efficient, but it usually breaks down in one of three places:

- It doesn't match the actual deal among the owners

- It ignores state-specific default rules

- It says very little about exits, disputes, and authority

That last problem is the most common. Businesses often spend time on ownership percentages and almost none on what happens if a member stops working, wants to sell, files bankruptcy, gets divorced, or dies. Those are not edge cases. Those are ordinary business contingencies.

Connecticut businesses need tailored governance

Connecticut companies also need to pay attention to newer structural options. An emerging development is the conversion of multi-member LLCs to series LLCs, a structure available in Connecticut since 2024 legislation. According to Wolters Kluwer's discussion of LLC member rights and responsibilities, this model allows members to segregate assets into protected series without forming separate entities, and it saw a 25% adoption surge among mid-sized Connecticut firms in early 2026.

That doesn't mean a series LLC is automatically the right move. It means Connecticut owners now have another planning tool, especially when one enterprise holds distinct assets, projects, or risk buckets. But that structure demands customized governance. Asset segregation on paper won't help much if the records, contracts, and internal practices are sloppy.

Connecticut LLCs are usually best protected by boring discipline. Signed agreements, clean books, clear authority, and consistent separation between the company and the owners.

Another practical point is that business structures evolve. Ownership changes, managers are added, and capital terms are revised. When that happens, companies often need to update their public filings as well as their internal documents. If your company's structure has changed, it helps to understand the process for amending articles of organization.

Securing Your Business's Future in Connecticut

A member in an LLC is the owner of the business, but ownership is only the starting point. Key legal questions involve authority, economic rights, duties, transfers, tax treatment, and the strength of the liability shield in actual operation.

For Connecticut businesses, those issues should be resolved in writing, early, and with enough detail to survive stress. A solid operating agreement does more than state percentages. It allocates control, defines exits, reduces ambiguity, and gives the company a workable structure when business conditions change.

Good governance also doesn't stop with legal drafting. A well-run company should align its contracts, accounting, recordkeeping, and operational systems. In many businesses, that includes practical risk management outside the legal documents too, such as strengthening business cybersecurity so internal records, financial data, and company communications remain protected.

Understanding the role of an LLC member is the first step. Implementing it correctly is where businesses protect themselves.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.