Think of a buy-sell agreement as a “business prenup.” It’s a foundational contract you create with your co-owners that spells out exactly what happens if one of you leaves the business—for any reason. This document is a cornerstone of smart business planning, ensuring a smooth transition of ownership during unexpected events.

Why Your Business Needs a Buy-Sell Agreement

Imagine your business is a sports team, and the co-owners are the star players. Each one is vital to winning. Now, what if a key player suddenly retires, gets injured, or decides to join a rival? Without a rulebook in place, the team could descend into chaos, arguing over who gets their spot and how to fill the gap. A buy-sell agreement is that rulebook.

This agreement is a proactive strategy. It’s a pre-negotiated roadmap that outlines exactly what happens when a co-owner exits, whether it’s a planned event like retirement or something completely unexpected like death, disability, or even personal bankruptcy.

Creating a Clear Path Forward

The core purpose of a buy-sell agreement is to eliminate ambiguity during what are often emotional, high-stakes situations. It establishes a clear, fair process for transferring ownership, which protects the company, the remaining owners, and the departing owner (or their family). By setting the terms when everyone is on the same page, you avoid costly and contentious disputes down the road.

This is especially critical for family-owned businesses and partnerships, where personal and professional lines can blur. Having an agreement in place is a common practice for businesses in the United States looking to ensure smooth transitions. For more on the crucial role of valuation in these agreements, you can find great insights on Stout.com.

A buy-sell agreement is your best defense against a "business divorce"—a messy, emotionally charged, and expensive ordeal that can easily end in litigation.

A well-drafted buy-sell agreement typically outlines a clear plan for several key scenarios. These pre-defined "triggering events" remove the guesswork and provide a structured response when ownership changes are necessary.

The table below summarizes the most common events that these agreements cover.

Key Scenarios Covered by a Buy-Sell Agreement

| Triggering Event | What It Means for the Business | How the Agreement Helps |

|---|---|---|

| Death | An owner's shares pass to their heirs, who may have no interest or expertise in running the company. | It can mandate that the estate sells the shares back to the company or remaining owners, often funded by a life insurance policy. |

| Disability | An owner becomes unable to contribute, creating a leadership and operational gap. | It defines what constitutes a disability and provides a mechanism for a buyout, ensuring business continuity. |

| Retirement | A planned exit that requires a smooth transition of ownership and responsibilities. | It sets a clear timeline and valuation method for the retiring owner's shares, allowing for a planned and funded buyout. |

| Divorce | An owner's shares could become part of a marital asset division, potentially bringing an ex-spouse into the ownership group. | It prevents shares from being transferred to a non-owner spouse by giving the company or other owners the right of first refusal. |

| Involuntary Transfer | An owner declares bankruptcy or has shares seized by creditors. | It allows the company or owners to purchase the shares before they fall into the hands of third parties, protecting the business from outside control. |

| Voluntary Departure | An owner decides to leave the business to pursue other interests or start a competing venture. | It establishes the terms for a buyout and can include non-compete clauses to protect the company's interests. |

By addressing these situations in advance, you ensure the business can navigate turbulent times without derailing its core operations or long-term vision.

The Foundation of Stable Governance

Beyond exit planning, a solid buy-sell agreement is a fundamental piece of your company's governance framework. It provides stability and reassures stakeholders—including employees, lenders, and clients—that the business has a well-thought-out plan for its future. For a deeper understanding of this topic, you can explore our resources on corporate governance best practices.

Essentially, it answers critical questions before they become urgent problems:

- Who can buy a departing owner’s shares? Does the company get the first option, or do the remaining partners?

- What is the value of the shares? The agreement specifies a predetermined valuation method to ensure a fair price.

- How will the buyout be funded? It can outline funding mechanisms, like life insurance policies or installment plans.

Without these pre-agreed terms, you're leaving the future of your business to chance. A buy-sell agreement ensures the continuity and health of the company you've worked so hard to build.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Choosing the Right Type of Buy-Sell Agreement

Once you see just how vital a buy-sell agreement is, the next question is: which one is right for my business? It’s not a one-size-fits-all situation. The best structure depends on your ownership setup, company size, and where you see the business going in the long run.

Picking the right model is critical. It will have a direct impact on everything from tax liabilities and funding to how much administrative work is involved.

Think of it like choosing a vehicle. A two-seat sports car is perfect for a duo, but it’s completely impractical for a large family. In the same way, the best agreement structure boils down to how many owners your business has and what its financial framework looks like. Let's walk through the three main models to find your best fit.

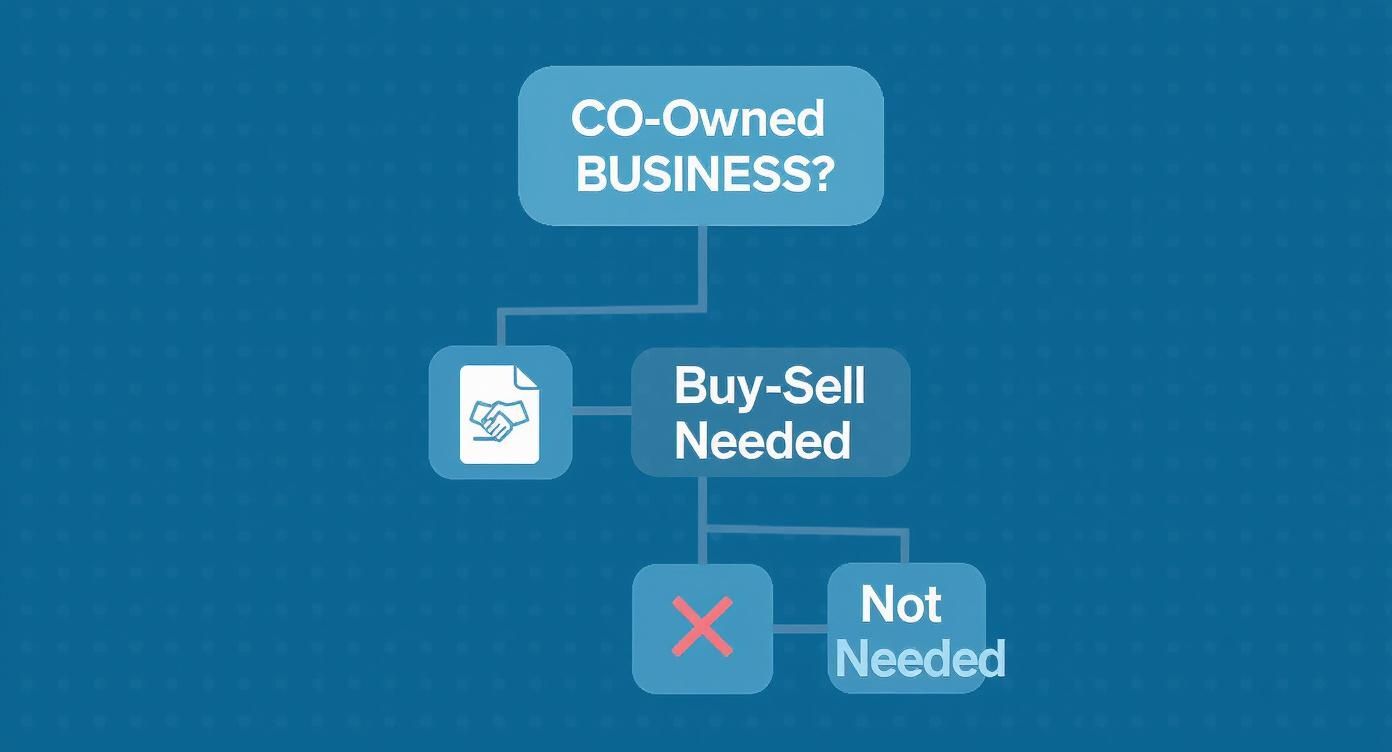

The infographic below gives you a quick visual to help decide if a buy-sell agreement is a must-have for your business.

As you can see, if your business has more than one owner, putting a buy-sell agreement in place isn't just a good idea—it's a foundational step to secure its future.

The Cross-Purchase Agreement Model

The Cross-Purchase Agreement is the simplest and most direct model, making it a great fit for businesses with just two or three owners. In this setup, the individual owners personally agree to buy the departing owner's shares directly from them or their estate.

Imagine two partners, Alex and Ben, who co-found a tech startup in Hartford. They sign a cross-purchase agreement and each takes out a life insurance policy on the other. If Alex were to pass away, Ben would use the insurance payout to buy Alex's shares from his estate. Just like that, Ben becomes the sole owner, and the business keeps running smoothly.

Key Takeaway: The big win with a cross-purchase agreement is that the remaining owners get a "step-up" in their cost basis for the shares they buy. This can lead to serious tax savings if they decide to sell their stake down the road.

But this model gets messy fast as you add more owners. If a business has five partners, each one would need an insurance policy on the other four—that's 20 separate policies to manage. The administrative headache alone makes it a non-starter for most larger firms.

The Entity-Purchase Agreement Model

Also known as a Redemption Agreement, the Entity-Purchase Agreement is a much cleaner solution when you have several owners. Here, the business entity itself—the LLC, corporation, or partnership—agrees to buy back the shares of a departing owner.

Let's picture an established Connecticut accounting firm with six partners. Instead of having the partners buy policies on each other, the firm itself purchases one life insurance policy on each partner. If a partner retires or becomes disabled, the firm uses its own funds or the insurance proceeds to redeem their shares. Those shares can then be retired or split among the remaining owners.

This approach centralizes everything, requiring only one agreement and one funding source per owner, which cuts down on the administrative burden significantly. It’s an efficient way to handle ownership changes in a bigger group. For a deeper dive into how ownership is defined, you might find our guide on what is a shareholder's agreement helpful.

The Hybrid or Wait-and-See Model

The Hybrid Agreement offers the ultimate flexibility, blending elements from both the cross-purchase and entity-purchase models. Usually, this structure gives the business the first crack at buying a departing owner's shares (the redemption part).

If the company passes on the opportunity—maybe cash flow is tight or it's not the right strategic move—the remaining owners then get the option to buy the shares themselves (the cross-purchase part).

This "wait-and-see" approach is perfect for growing companies where the future is hard to predict. It lets the owners and the business make the smartest decision when a trigger event actually happens, instead of being locked into a rigid plan made years earlier. That adaptability makes it a popular choice for businesses on a growth trajectory.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Key Clauses Every Agreement Should Contain

A powerful buy-sell agreement is more than just a template; it’s a meticulously built document where every single clause serves a strategic purpose. Think of it as the detailed schematic for a critical piece of machinery. If parts are missing or vague, the whole system can fail right when you need it most.

Let's break down the essential components that make an agreement robust, enforceable, and genuinely protective of your business. These clauses work together to create a clear, predictable process, removing the guesswork—and potential for conflict—when an ownership change is on the horizon.

Defining the Triggering Events

The heart of any buy-sell agreement is its list of triggering events. These are the specific, pre-defined circumstances that activate the contract and kick off the buyout process. Ambiguity here is a recipe for disaster, so these clauses have to be crystal clear.

Common triggers include:

- Death or Disability: Specifies exactly what happens to an owner's shares if they pass away or become permanently unable to contribute to the business.

- Retirement: Outlines a planned, orderly exit strategy for owners who are ready to step away.

- Voluntary Termination: Covers the scenario where a partner decides to leave the business for their own reasons.

- Involuntary Termination: This addresses the tough situations, like an owner's personal bankruptcy, a felony conviction, or a divorce settlement that could transfer shares to an ex-spouse.

Each event needs to be defined with precision. For instance, "disability" shouldn't be a vague concept. It should be explicitly defined, often by referencing the inability to perform duties for a specific number of consecutive months.

Establishing the Business Valuation Method

Perhaps the most contentious part of any buyout is landing on a fair price. A well-drafted buy-sell agreement removes this friction by establishing a business valuation method long before anyone thinks about leaving. This ensures everyone agrees on how to value the company while they're still on good terms, preventing heated disputes down the road.

A common pitfall, however, is setting a fixed value and then forgetting about it. A 2018 study highlighted that failing to regularly update the valuation is a major source of disputes, as the old price may not reflect the business's current worth. You can learn more about the critical role of valuation in buy-sell agreements from Stout.

Deciding how to value the business is a crucial step. The right method depends on your company's specifics, but it's important to understand the trade-offs between simplicity and accuracy.

Comparison of Business Valuation Methods

| Valuation Method | How It Works | Pros | Cons |

|---|---|---|---|

| Agreed-Upon Value | The owners periodically agree on a fixed value for the business and document it. | Simple and straightforward. | Often neglected and becomes outdated, leading to an unfair price. |

| Formula-Based Value | Uses a formula, such as a multiple of earnings (EBITDA) or book value. | Provides a clear, objective calculation. | Can be rigid and may not capture intangible assets or market changes. |

| Appraisal Process | Requires a neutral, third-party appraiser to determine the fair market value at the time of the trigger. | Most accurate and reflective of current market conditions. | Can be costly and time-consuming. |

Ultimately, choosing the right method is about balancing your business’s needs with your partners' preferences for either a simple calculation or a more comprehensive, market-based assessment.

Outlining the Funding Mechanism

Once a price is set, the next question is a big one: where will the money come from? An agreement is incomplete without a clear funding clause. Without a plan, the remaining owners or the company itself could face a severe financial strain, jeopardizing the very business you're trying to protect.

Important Insight: An unfunded agreement is often just an empty promise. The funding mechanism is what gives the contract teeth and ensures the buyout can actually happen.

Common funding strategies include:

- Life and Disability Insurance: This is a very common and effective method. The company or the owners buy policies on each other. When triggered, the proceeds provide immediate, tax-free cash to fund the buyout.

- Installment Payments: The agreement can stipulate that the purchase price will be paid out over time. This makes the buyout more affordable for the remaining owners but provides less immediate cash for the departing owner or their family.

- Cash Reserves: The business can systematically set aside funds in a dedicated account to prepare for a future buyout.

Implementing Transfer Restrictions and Dispute Resolution

Finally, two protective clauses are non-negotiable. First, transfer restrictions are essential. They prevent owners from selling or giving their shares to an outsider without the consent of the other owners. This often takes the form of a Right of First Refusal, giving the company or remaining owners the first chance to buy the shares. This clause is vital for keeping ownership within your trusted circle.

Second, a dispute resolution clause outlines what to do when disagreements pop up. Rather than heading straight to costly litigation, this clause can require mediation or binding arbitration. This provides a more efficient and private way to resolve conflicts over the agreement’s terms.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Securing Your Business During Mergers and Acquisitions

Most people think of a buy-sell agreement as just an internal tool for handling a partner's exit. While that’s true, its strategic value goes much deeper, especially when your business enters the high-stakes world of mergers and acquisitions (M&A).

In an M&A scenario, that agreement transforms from a simple succession plan into a powerful asset. It can make your company significantly more appealing to potential buyers.

Put yourself in an acquirer’s shoes. They’re hunting for stability, clear governance, and minimal risk. A solid buy-sell agreement is a signal that your company is organized and has already untangled complex ownership questions. It shows foresight and maturity—two very attractive qualities.

Making Your Business an Attractive Target

When a potential buyer starts their due diligence, one of the first things they’ll tear into is your ownership structure. They need to know exactly who owns what and whether any hidden disputes or liabilities could blow up the deal.

A buy-sell agreement gives them clear, immediate answers.

By pre-defining ownership stakes and rules for transferring them, you remove a huge question mark. This clarity alone makes your business a much simpler and more attractive target for acquisition.

A business with a clear ownership roadmap is a lower-risk investment. Your buy-sell agreement is proof that your house is in order, which can directly boost a buyer's confidence and, potentially, the price they’re willing to pay.

This kind of preparation tells a potential partner that you've planned for the future—not just for internal shuffles but for major strategic moves. It proves you're ready for the next level.

Streamlining the Due Diligence Process

The due diligence phase of any M&A deal is notoriously intense. Acquirers have to verify every single detail of your company’s legal and financial health, and it can be a long, draining process.

A well-drafted buy-sell agreement simplifies this entire ordeal.

Instead of wading through a messy web of handshake deals or informal promises, the buyer can review one, legally-binding document. It clearly lays out:

- Ownership Percentages: Exactly who owns how much.

- Transfer Restrictions: Rules that prevent shares from being sold off to unknown third parties.

- Valuation Methodology: The agreed-upon formula for calculating the company's worth.

This provides a stable foundation for the deal and gives potential partners a predictable path forward. With the global M&A market seeing activity jump by 18% year-over-year to reach $1.5 trillion in the first half of 2024, having a buy-sell agreement is a key advantage. In this active market, it helps structure successful deals. You can find more insights on the current state of the M&A market from Cassels.

Setting the Stage for Negotiation

Beyond just due diligence, the agreement also helps set the initial terms for the acquisition itself. The valuation methods and terms laid out in your buy-sell can serve as a starting point for negotiation.

Of course, an acquirer will do their own valuation. But having a pre-agreed formula shows that the owners are on the same page and have a realistic view of their company's value.

This united front is critical. Often, early M&A talks are captured in a preliminary, non-binding document, which you can learn more about in our article on what is a letter of intent. A strong buy-sell agreement ensures all owners are aligned from the start, preventing internal squabbles from killing a promising deal before it even gets off the ground.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Common Mistakes to Avoid When Drafting Your Agreement

A poorly drafted buy-sell agreement can easily cause more trouble than it prevents. In some cases, it's even worse than having no agreement at all. Think of it like building a bridge with flawed blueprints—it might look fine on paper, but it’s guaranteed to collapse under the slightest pressure. To make sure your agreement actually protects your business, it’s critical to sidestep a few common but costly errors.

These mistakes can turn a document designed for clarity and security into a fast track to bitter disputes and financial hardship. Steering clear of these pitfalls is the only way to create a contract that works as intended when you need it most.

Relying on Generic Online Templates

One of the biggest temptations is to download a generic buy-sell agreement template from the internet. While these documents can seem comprehensive, they are never tailored to your specific business, your industry, or the unique laws here in Connecticut. A template can't possibly account for the nuances of your partnership or the specific goals you and your co-owners have.

Using a one-size-fits-all document almost always leads to vague terms, unenforceable clauses, and critical gaps. For instance, a template might lack a clear definition of "disability," which could spark a long and expensive argument over when a buyout should even be triggered. Professional legal counsel is essential to customize the agreement to your exact needs.

Failing to Fund the Agreement

An agreement without a clear and practical funding plan is really just an empty promise. You can have the most detailed buyout terms in the world, but if the remaining owners don't have the cash to make the purchase, the document is worthless. This is a surprisingly common oversight that can force a business to take on crippling debt or even sell off assets just to meet its obligations.

Critical Reminder: An unfunded buy-sell agreement doesn't solve a problem; it creates a new one. The contract establishes a legal obligation to buy, and without a funding mechanism like life insurance or a dedicated cash reserve, you risk defaulting on that obligation.

Imagine a partner passes away, and the business is suddenly on the hook to pay their estate $500,000. Without a funding plan, the company might have to drain its operating cash, putting its ability to pay employees and suppliers in jeopardy.

Using an Unfair or Outdated Valuation Method

Deciding on a business valuation method is a cornerstone of any buy-sell agreement, but choosing the wrong one—or failing to update it—can breed deep resentment. A common mistake is to set a fixed dollar value in the agreement and then forget about it for years. A business that was worth $1 million at its start might be worth $5 million a decade later, but the outdated agreement could force a sale at that original, drastically lower price.

Similarly, relying on a rigid formula based on book value might not capture your company's true worth, as it ignores intangible assets like brand reputation or intellectual property. The fairest approach is often to require a professional appraisal at the time of the trigger event or to schedule regular reviews to update an agreed-upon value.

Forgetting to Review and Update Regularly

Finally, treating your buy-sell agreement as a "set it and forget it" document is a recipe for future conflict. Businesses evolve. New partners might join, financial situations change, and the company's value will fluctuate. An agreement drafted five years ago may no longer reflect the current reality of your business.

Best practice is to review your agreement every three to five years, or after any significant company event, such as:

- A major change in company valuation.

- The addition or departure of an owner.

- Significant changes in tax law.

- Taking on substantial new debt.

Regular updates ensure the document remains relevant, fair, and aligned with what the owners actually want, preventing it from becoming an obsolete source of conflict.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How to Finalize Your Buy-Sell Agreement

By now, you see that a buy-sell agreement isn't just another document to file away. Think of it as a living blueprint for your company’s future—a plan that ensures stability when things change. It’s what protects the business, the remaining owners, and the family of a departing owner.

The next step? Turning that understanding into action.

Your Next Steps Checklist

Getting this process started is simpler than you might think. Just follow a few straightforward steps to build your agreement on a solid foundation.

- Schedule a Meeting with Co-owners: The first move is getting everyone in the same room. Talk about why this agreement is so important and get a firm commitment from the whole team to see it through.

- Gather Key Financial Documents: You'll need to pull together your business’s financial statements, tax returns, and any existing ownership agreements. This paperwork is the bedrock of the valuation process.

- Engage Professional Advisors: This is absolutely not a DIY project. The single most important investment you can make in this process is getting the right guidance.

Assembling Your Professional Team

A rock-solid buy-sell agreement is a team effort, requiring both legal and financial expertise. You'll need a business attorney to draft a contract that’s legally sound and tailored to your specific situation and Connecticut law. For a deeper dive into what they bring to the table, you can learn more about what a business lawyer does in our guide.

Working alongside your lawyer, a CPA can offer critical advice on the tax implications of different agreement structures. A financial advisor is also key to helping you set up the funding mechanism, whether that's life insurance policies or another method. Taking these steps ensures your agreement isn’t just a piece of paper—it’s a practical, enforceable plan for when you need it most.

If you’re ready to protect your business with a professionally crafted agreement, it’s time to seek expert guidance. To discuss your business law matter, contact Kons Law at (860) 920-5181.

Frequently Asked Questions About Buy-Sell Agreements

Even after you grasp the basics, it's natural to have practical questions when you start thinking about putting a buy-sell agreement in place. Getting answers to these common concerns can give you the confidence to move forward and protect what you've built.

Let's walk through a few of the questions we hear most often from business owners.

How Often Should We Update Our Buy-Sell Agreement?

A buy-sell agreement is not a "set it and forget it" document. Your business is constantly changing, and your agreement needs to keep pace. Think of it as a living document that has to adapt.

As a general rule, you should plan on a formal review of your buy-sell agreement every 3-5 years. But you also need to revisit it immediately after any major company event—like a significant shift in valuation, bringing on a new owner, or taking on a large amount of debt.

Letting an agreement get stale is one of the biggest mistakes we see. An outdated valuation can create the exact kind of expensive, relationship-damaging dispute you were trying to avoid in the first place.

Can a Buy-Sell Agreement Be Used for an LLC?

Yes, absolutely. People often associate these agreements with corporations or traditional partnerships, but they are just as critical for Limited Liability Companies (LLCs). For an LLC, the buy-sell provisions are typically built right into the operating agreement or drafted as a separate, standalone contract.

The core purpose is exactly the same, no matter the business structure. The agreement lays out the rules for what happens to a member's ownership interest when a triggering event occurs, protecting the remaining members and keeping the business running smoothly.

What Happens If We Can't Agree on a Business Valuation?

Valuation disputes are probably the #1 source of conflict in a buyout. That's precisely why a well-drafted buy-sell agreement forces you to decide on the valuation method in advance, while everyone is still on good terms. Your agreement should spell this process out clearly.

If a disagreement still pops up, the agreement’s dispute resolution clause kicks in. This provides a clear roadmap for what to do next, which might include:

- Mandatory Third-Party Appraisal: Requiring a neutral, certified appraiser to determine the fair market value.

- Averaging Multiple Appraisals: Each side hires their own appraiser, and a third is brought in to break a tie or average the figures.

- Mediation or Arbitration: Forcing the owners to work through the disagreement with a neutral mediator or go to binding arbitration, which is far less costly and time-consuming than a lawsuit.

By building these mechanisms in from day one, you create a clear, enforceable procedure for getting past one of the most emotional and difficult parts of any business separation.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.