A business owner wins a lawsuit, gets a judgment, and expects the money to follow. Then nothing happens. The customer who ignored invoices now ignores the judgment too. At that point, the judgment can feel like a framed piece of paper rather than a recovery tool.

That frustration is common in collections work. A court judgment establishes that the debt is legally owed, but it doesn't collect itself. If the debtor won't pay voluntarily, the creditor has to move into enforcement, and one of the most effective ways to do that is to reach cash already sitting in a bank account.

That is why creditors ask how to garnish bank account funds after judgment. They aren't looking for legal theory. They're looking for a path from unpaid receivable to recovered money.

Bank levies matter because they target the debtor's most liquid asset. That is not an edge-case tactic. Bank-account garnishment is a core part of judgment enforcement in the United States, and in Connecticut, court records suggest 30 to 40% of consumer-oriented civil judgments are enforced through post-judgment collection actions, including bank levies, as discussed in this analysis of bank-account garnishment practice.

Still, a bank garnishment isn't self-executing for the creditor. It demands accurate forms, the right court procedure, proper service, and a realistic understanding of exemptions. Connecticut adds another layer because the exemption process often requires active court handling rather than relying on broad automatic protections at the state level.

From Paper Judgment to Paid Invoice An Introduction

Most creditors reach this point after months of avoidable delay. You sold goods, extended trade terms, performed work, or funded a loan. You sent reminders, then demand letters, then suit papers. Eventually, the court entered judgment in your favor, and the debtor still didn't pay.

That is the moment when collection strategy becomes more important than the lawsuit itself.

A judgment gives you a legal advantage, but a bank account garnishment turns that advantage into pressure the debtor can't casually ignore. When a bank receives a valid levy, the issue stops being abstract. Funds can be restrained, exemption rights get triggered, and the debtor has to respond in a legal forum instead of dodging calls.

Why bank levies get results

For many debtors, the bank account is where business receipts, wages, transfers, and reserve funds sit in one place. Real estate may be encumbered. Equipment may be hard to sell. Accounts receivable may be uncertain. Cash in a deposit account is different. It is immediate, measurable, and often reachable.

That is why experienced creditors' counsel often consider a bank execution early once they have usable asset information.

A judgment changes the legal relationship. A levy changes the debtor's behavior.

Why precision matters in Connecticut

The process sounds simple when described casually. Get a judgment. Find the bank. Serve the papers. Collect the money.

In practice, mistakes derail levies all the time. The wrong bank. The wrong account holder name. Incomplete identifying information. Poor timing. Failure to respond when the debtor files an exemption claim. Connecticut procedure rewards creditors who are organized before the levy goes out.

If you're trying to understand how to garnish bank account funds the right way, start with one assumption: success usually depends less on aggression and more on preparation.

The Foundation for Garnishment Obtaining a Judgment and Finding Assets

You can't garnish a bank account in an ordinary commercial debt case just because an invoice is unpaid. You need a judgment first. That point sounds basic, but many business owners assume the delinquent balance itself gives them collection rights against the debtor's bank. It doesn't.

A judgment is the court's formal determination that the debtor owes the money. Once you have that order, you become a judgment creditor and gain access to post-judgment enforcement tools. If you need a concise overview of that status, this explanation of what a judgment creditor is is a useful starting point.

A judgment comes before execution

The path usually begins with a lawsuit for breach of contract, unpaid goods, unpaid services, guaranty liability, or another commercial claim. Some cases end in default because the debtor never appears. Others end in summary judgment, stipulation, or trial.

Once judgment enters, the case shifts from proving liability to enforcing payment.

That distinction matters because the evidence and tactics are different. Before judgment, you prove the debt. After judgment, you identify assets and use the court's enforcement process to reach them.

Asset location is where many creditors lose time

A levy works only if you can identify a bank with enough confidence to serve it properly. Guessing is expensive. Blind levies can produce nothing but marshal fees, delay, and a debtor who now knows enforcement is underway.

Post-judgment discovery is the tool that solves that problem.

Common discovery methods include:

- Interrogatories: Written questions asking the debtor to identify banks, account types, account signatories, and recent transfers.

- Requests for production: Demands for bank statements, signature cards, loan applications, tax returns, bookkeeping records, and merchant processing reports.

- Depositions: Live testimony under oath, which is often the fastest way to pin down evasive debtors.

- Subpoenas to third parties: In the right situation, records from accountants, bookkeepers, payment processors, or counterparties can reveal where funds flow.

What to ask for in discovery

Generic requests usually produce generic objections. Targeted requests get better answers.

A practical set of requests often seeks:

| Discovery target | Why it matters |

|---|---|

| Names of all financial institutions | You need an actual service target, not a rumor |

| Account statements | They reveal balances, patterns, and whether exempt funds may be present |

| Signer and ownership records | Useful when accounts are held by entities, spouses, or affiliates |

| Incoming payment sources | Helps distinguish business revenue from potentially exempt deposits |

| Recent transfers between accounts | Important if the debtor is moving money after judgment |

Practical rule: If you don't know where the debtor banks, your first job isn't garnishment. It's intelligence gathering.

What actually works

In practice, the best post-judgment discovery requests are narrow enough to enforce and broad enough to expose movement of funds. Ask for current institutions, prior institutions, account ownership capacity, and records showing transfers in and out. If the debtor is a business, don't stop at checking accounts. Ask about savings accounts, money market accounts, merchant settlement accounts, and certificates of deposit.

What doesn't work is serving one set of vague discovery requests and waiting indefinitely. Judgment enforcement requires follow-up. If the debtor ignores discovery, you move to compel. If the debtor stonewalls at deposition, you pin down dates, institutions, and signatories one by one.

A bank levy is strongest when it is the final step in a sequence, not the first move made out of frustration.

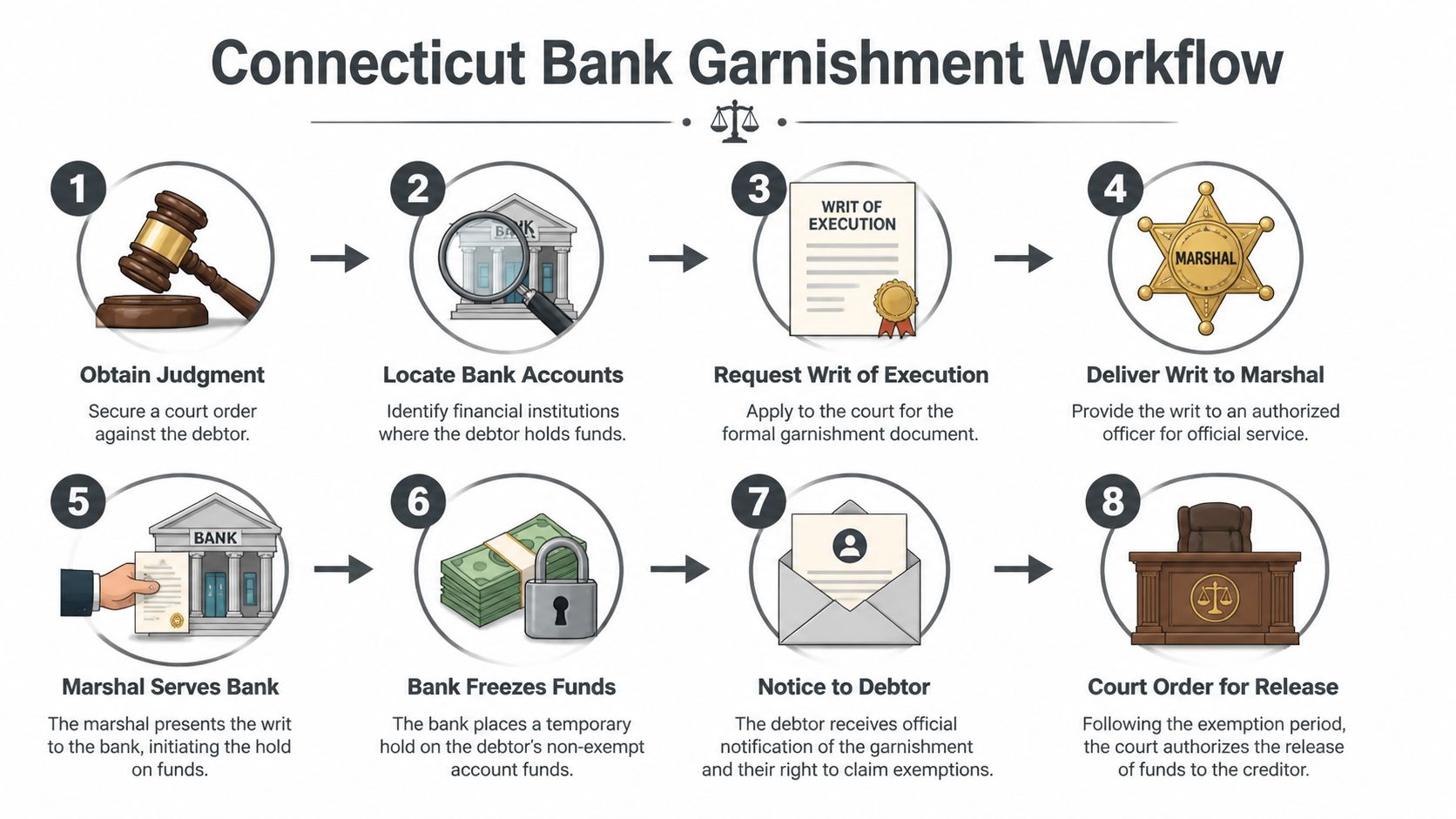

The Connecticut Bank Garnishment Process A Creditor's Workflow

A Connecticut bank execution succeeds or fails on paperwork, timing, and service details. By the time a client reaches this stage, the hard part should not be proving the debt. The hard part is turning a judgment into a bank restraint without giving the debtor an avoidable procedural opening.

Step one begins with the court file, not the bank

The process usually starts in the same Connecticut Superior Court file where the judgment entered. The creditor applies for a post-judgment execution, confirms the current amount due, checks for any stay, and makes sure the debtor name matches the judgment exactly.

That last point causes more trouble than many business owners expect.

If the judgment is against "ABC Industrial Services, LLC," the execution should not refer to a trade name, a shortened name, or an affiliated company. The bank and the marshal work from the legal identity in the papers. If your caption, balance, or debtor information is sloppy, the levy can fail before the bank ever reaches the account.

Service runs through the marshal

Connecticut does not let the creditor serve the bank directly in the ordinary course. A Connecticut State Marshal or other proper officer typically handles service and the return. That means your instructions to the marshal matter as much as the application itself.

Good marshal instructions identify the debtor clearly, name the financial institution precisely, and attach any reliable identifying information you have. Poor instructions produce delay, mis-service, or an execution that expires before anyone gets useful traction.

For a broader explanation of post-judgment collection tools, see this overview of how to enforce a judgment.

The workflow that works in practice

I tell creditors to treat a bank execution as an operations process with legal consequences. In Connecticut, that usually means:

Confirm the judgment is presently enforceable

Check the unpaid balance, post-judgment interest if applicable, and whether any stay, appeal, or bankruptcy filing blocks collection.Match the debtor to the right legal name and tax identity

This matters most with LLCs, closely held companies, and debtors who use several business names.Target the correct financial institution

Use records, not assumptions. A bank named in stale records may no longer hold meaningful funds.Prepare the execution papers with exact party information

Small drafting errors create expensive delays.Give the marshal complete service instructions

Include all known addresses, account references, and debtor identifiers that may help the bank locate accounts.Follow the service through to return and response

Do not assume silence means the levy worked. Confirm what was served, when it was served, and whether the bank identified an account.

Timing affects recovery

A signed execution is not something to leave sitting in a file. Delay gives the debtor time to move funds, close accounts, or change institutions. It also creates internal confusion on the creditor side, especially if the payoff figure changes while the papers remain unused.

I have also seen creditors narrow their instructions too much. If you know one account number, provide it. But the better practice is usually to identify the debtor thoroughly and direct attention to all deposit accounts held in that debtor's legal name or tax identity, so the bank is not boxed into reviewing only one account reference.

As noted earlier in the article, execution papers also have a limited effective life. Treat service as a coordinated step, not an administrative errand.

A fast levy helps only if the papers are accurate enough for the bank to match the right debtor.

Connecticut creditors need to plan for the next procedural turn

This is the part many generic bank garnishment articles miss. Connecticut is not a self-executing exemption state from the creditor's perspective. Serving the bank is only one stage of the workflow. A successful creditor prepares for what happens after restraint, including the likelihood that the debtor will raise exemption issues or ownership objections.

That affects how you draft, how you identify the debtor, and how quickly you respond after service. A creditor who treats the levy as finished once the marshal serves the bank usually loses time. A creditor who expects a second round of procedure is in a much stronger position.

What works and what fails

| What works | What fails |

|---|---|

| Exact debtor name and reliable identifiers | Trade names, nicknames, or incomplete entity names |

| Bank target based on records you can defend | Rumor, guesswork, or outdated payment history |

| Prompt coordination with the marshal | Letting signed papers sit unused |

| Broad enough instructions to capture reachable deposit accounts | Instructions limited to one account label when the debtor uses several |

| Planning for post-service disputes | Assuming service on the bank ends the process |

Creditors usually recover more consistently when they treat a Connecticut bank execution as a disciplined sequence. Precision gets results. Sloppiness gets another round of motion practice and another month without payment.

After the Levy Bank Holds Exemptions and Debtor Rights

Service on the bank is not the end of the matter. It is the start of the contested part.

Once the levy hits, the bank reviews its records, identifies the debtor account if it can, and places a hold on funds subject to the execution. From the creditor's perspective, that is progress. From the debtor's perspective, it is the first moment the judgment becomes operationally disruptive.

Banks move quickly once they have a valid order

In many states, once a creditor files a writ and the garnishment packet reaches the bank, transmission and account restraint happen quickly. One summary of the process notes that garnishment packets are often transmitted to banks within 1 to 3 business days, with banks freezing accounts within 2 to 3 business days of receipt, and that banks in the United States honored approximately 85 to 90% of garnishment orders within 48 hours of receipt in 2022, with efficient systems producing same-day or next-business-day freezes in a substantial share of cases. That same source also notes that the average period between judgment and first bank garnishment in commercial cases in Connecticut and neighboring states compressed to roughly 25 to 35 days over the prior decade. See this discussion of collecting a court judgment from a deposit account.

For a creditor, the practical lesson is simple. If you have the right bank and good identifying information, delays often come from defects in your process, not from the concept of garnishment itself.

Connecticut is not a self-executing exemption state

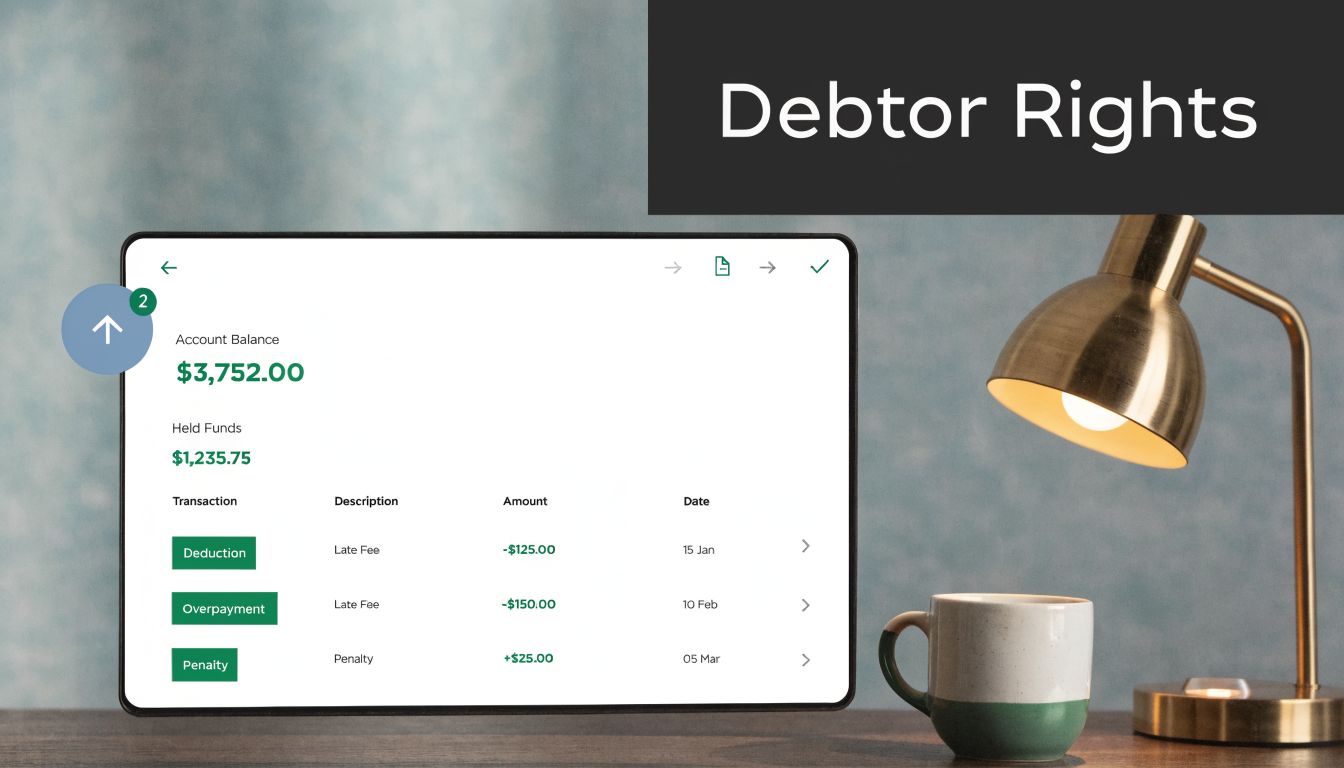

Connecticut, however, differs from states that build automatic account protections directly into the levy process. In Connecticut, the creditor often has to be ready for a debtor-filed exemption claim rather than relying on broad self-executing state exemptions to sort things out automatically.

That distinction matters because the burden often shifts quickly to paperwork, tracing, and court response. If the debtor claims exempt funds, the creditor should be prepared to review statements, identify the nature of deposits, and decide whether to contest the claim, narrow the demand, or stand down as to certain funds.

What funds raise exemption issues

A creditor should expect scrutiny when the account contains direct deposits tied to protected federal benefits. The most familiar examples include Social Security and similar benefit streams that receive federal protection.

One key federal protection is the lookback for certain federal benefits. The source above discussing state exemption structures notes that Connecticut lacks self-executing exemptions beyond federal benefit protections such as up to 2 months' deposits of Social Security. See the National Consumer Law Center discussion of protecting wages, benefits, and bank accounts from judgment creditors.

That does not mean every dollar in the account is automatically untouchable. It means the creditor should avoid assuming that a frozen balance is fully collectible solely because the bank placed a hold.

Practice note: A levy that ignores obvious benefit tracing issues can create avoidable motion practice and cost more than it recovers.

The creditor's job during the hold period

Connecticut creditors should think of the hold period as an evidence phase. Your work is no longer only about obtaining the levy. It is about defending the levy where appropriate and narrowing it where necessary.

Useful creditor actions during this phase often include:

- Reviewing account records fast: If the debtor produces statements, inspect deposit descriptions and transfer patterns instead of reacting from the caption alone.

- Distinguishing source from balance: An account balance doesn't tell you whether the funds are reachable. The deposit history does.

- Preparing a focused court response: If you oppose an exemption claim, explain why specific deposits are not protected. Broad accusations usually don't help.

- Avoiding overreach: If part of the account is plainly exempt, acknowledge that and preserve credibility on the rest.

Why digital records complicate modern levies

Many exemption disputes no longer involve a simple paycheck and a local branch account. Funds move through mobile banking, peer-to-peer transfers, online lenders, payroll processors, and linked digital platforms. That makes source tracing more document-heavy than many creditors expect.

For business owners trying to understand why account records can be hard to interpret, these broader digital privacy challenges help explain why modern financial data is fragmented across platforms and devices.

If you need a broader legal backdrop for collection activity in the state, this overview of Connecticut debt collection laws provides additional context.

What not to do after service

Creditors often create their own problems.

- Don't assume the bank did all the legal analysis for you. A bank hold is not a judicial ruling on exemptions.

- Don't ignore debtor filings. If the debtor claims exemption and you fail to respond thoughtfully, you may lose reachable funds by default.

- Don't treat every transfer as concealment. Some are ordinary transactions. Focus on facts you can prove.

- Don't conflate pressure with advantage. A hard levy is useful. An indefensible levy is expensive.

The strongest creditors treat post-levy work as part of enforcement, not as an annoying detour after the main job is done.

Enforcement Challenges and Advanced Collection Strategies

A levy that looks straightforward on paper can collapse for reasons that have nothing to do with the debt itself. The debtor may claim mistaken identity. The bank may report no match. The account may be jointly held. The deposit history may show exempt funds mixed with business receipts. Or the debtor may move money between institutions faster than the creditor expected.

Those issues don't mean the collection effort failed. They mean the first levy exposed the next problem to solve.

Common defenses and how creditors should think about them

Some debtor responses deserve serious attention. Others are delay tactics dressed up as legal objections. The key is knowing the difference.

A few examples:

| Debtor position | Creditor response |

|---|---|

| "This isn't my account" | Compare name, address, tax ID, and account records before pressing forward |

| "All funds are exempt" | Demand account statements and trace deposits rather than accepting labels |

| "The money belongs to my spouse or partner" | Examine account title, deposit sources, and ownership evidence |

| "The bank has nothing" | Consider whether the debtor uses another institution or shifted funds before service |

Joint accounts and empty levies

Joint accounts create recurring friction. A levy may reach an account held with another person even though ownership of the funds inside that account is disputed. The practical fight is usually evidentiary, not conceptual. Who deposited the money, and can anyone prove it cleanly?

An empty levy can still be useful. It may reveal that the debtor no longer banks where expected, that the account is routinely swept, or that a business shifted operations to another institution. Good creditors use that information to refine the next move instead of declaring the process broken.

Creditors collect more effectively when they treat each failed levy as discovery, not defeat.

Successive levies and smarter sequencing

When the first service doesn't produce enough, a creditor may need successive enforcement steps. That can include a second bank levy, wage execution if applicable, subpoenas to related entities, or supplementary proceedings aimed at tracing transfers.

The strongest approach is usually staged:

- Start with current intelligence: Use recent statements, payment records, or third-party documents, not assumptions from the original lawsuit.

- Target likely non-exempt funds first: A levy that predictably hits protected benefits invites avoidable resistance.

- Sequence the pressure: Sometimes a bank levy works best when paired with information subpoenas or pending turnover requests.

- Document every decision: If the debtor later challenges the process, a clear paper trail matters.

Regulatory scrutiny is rising

Creditors also need to think beyond state procedure. Bank garnishments have drawn regulatory attention as potentially unfair practices. One discussion of that trend notes that the Consumer Financial Protection Bureau is scrutinizing bank garnishments, and that creditors are responding by using tiered levies, documenting benefit tracing, and relying on pre-judgment arbitration clauses, which can reduce legal challenge rates by up to 50%, according to this Fordham Law review discussion of bank-garnishment reform and creditor strategy.

Whether or not every creditor uses arbitration, the larger lesson is sound. Modern enforcement needs to withstand not only a motion from the debtor, but also scrutiny over whether the creditor acted carefully around exempt funds.

Multi-state issues complicate even local collections

Many Connecticut businesses deal with debtors who bank elsewhere, operate in several states, or move funds through affiliates. If you're assessing cross-border enforcement exposure, a broad survey of state debt collection regulations can help identify where procedures and exemptions diverge.

That kind of comparison is useful because the right collection strategy in one state may be clumsy or ineffective in another. A creditor should never assume that a successful Connecticut workflow ports neatly into another jurisdiction.

The advanced version of how to garnish bank account funds isn't about being more aggressive. It is about being more selective, better documented, and harder to knock off course.

Navigating the Complexity When to Hire Legal Counsel

Some judgment creditors can handle pieces of the process internally. Few should handle all of it that way.

The risk isn't only filing the wrong paper. A greater risk is losing time, service fees, financial advantage, or collectible funds because the process was treated as clerical when it was strategic. Bank garnishment sits at the intersection of court procedure, marshal service, exemption law, account tracing, and sometimes bankruptcy or multi-state enforcement.

Situations where self-help becomes expensive

Legal counsel becomes especially important when any of the following appears:

- The debtor files an exemption claim: That turns a levy into a contested court matter.

- The account is jointly held or business related: Ownership questions get fact-specific quickly.

- The debtor operates through multiple entities: You may be dealing with alter ego or transfer issues, not simple account restraint.

- The levy comes back empty despite signs of cash flow: That usually means the investigation needs to deepen.

- A bankruptcy filing appears: Collection activity can stop immediately, and mistakes here are costly.

If your company is already at the judgment-enforcement stage, speaking with a judgment collection attorney often saves more than it costs because the lawyer can sequence the work instead of reacting to each obstacle separately.

A practical checklist for creditors

Keep the sequence straight:

- Obtain the judgment

- Locate the debtor's bank assets

- Apply for execution

- Coordinate service through the proper officer

- Monitor the bank response

- Address exemption claims promptly

- Pursue release of non-exempt funds

- Reassess if the first levy underperforms

The best time to involve counsel is before the first failed levy teaches the lesson for you.

The bottom line

A bank levy is one of the most direct ways to convert a paper judgment into actual recovery. It also punishes sloppy lawyering and sloppy creditor administration. If the account identification is weak, the service instructions are incomplete, or the creditor mishandles exemptions, the process can stall fast.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Frequently Asked Questions on Bank Account Garnishment

Can I garnish an account at an out-of-state bank

Sometimes, but not automatically. The answer depends on where the bank is located, where the account relationship is legally maintained, and what enforcement procedure the other state requires. A Connecticut judgment may need to be domesticated or otherwise recognized before an out-of-state levy can proceed.

The practical point is that interstate enforcement is often a separate project, not a minor variation on a Connecticut levy.

Can I garnish a business bank account the same way as a personal account

The overall idea is similar, but business accounts usually create more identification and ownership issues. You need the exact legal entity name, and you need to know whether the judgment runs against the entity, an individual guarantor, or both.

Business accounts also tend to involve more transaction volume, more transfers, and more disputes about whether funds belong to affiliates or third parties.

How long does the process take

There isn't one fixed timeline because asset discovery, court processing, marshal coordination, bank response, and exemption claims all affect speed. Some levies move quickly when the creditor has strong bank information and the debtor doesn't contest the process. Others slow down because the account match is weak or exemption issues require court review.

The best way to shorten the timeline is to do the asset work before you request the execution.

What if the bank says it found no account

That doesn't always mean the debtor has no money there. It may mean the name was off, the identifying information was incomplete, the account was closed, or the debtor banks elsewhere. Treat a no-match result as information. Then update your discovery plan.

Can I keep levying if the first attempt didn't satisfy the judgment

Often yes, assuming the judgment remains enforceable and no stay applies. A first levy that yields little or nothing may justify additional discovery, another bank execution, or use of a different enforcement remedy.

Should I warn the debtor before serving the bank

That depends on your strategy. In some cases, advance notice prompts payment. In others, it prompts account movement. If the debtor has already ignored the judgment, many creditors prefer to complete the levy process first and deal with the response afterward.

What is the biggest practical mistake creditors make

They move too early with too little information. The second biggest mistake is the opposite. They wait too long after getting good information and lose momentum.

A well-timed levy depends on current account intelligence, accurate papers, and a plan for what happens after the freeze.

If you're holding a judgment and still haven't been paid, you don't need more delay or vague collection advice. You need a practical enforcement strategy that fits Connecticut procedure and the realities of bank levies, exemptions, and post-judgment recovery. To discuss your business law matter, contact Kons Law at (860) 920-5181.