Your branch manager asks a simple question after a client complaint: “Was this trade solicited or unsolicited?” If your file is thin, that question stops being simple.

For financial advisors, solicited vs. unsolicited is not a vocabulary exercise. It affects suitability exposure, supervision, arbitration strategy, transition disputes, Form U5 language, and sometimes whether a CFP Board inquiry gains traction. In practice, the core issue is proof. Who initiated the idea, what exactly was said, and what record exists to back it up?

Many advisors learn this distinction at the product desk or in annual compliance training. They usually confront its importance when a relationship sours, a firm reviews text messages, or a departing advisor is accused of soliciting clients too early. By then, the facts are already being framed by someone else.

Defining Solicited vs Unsolicited in Your Practice

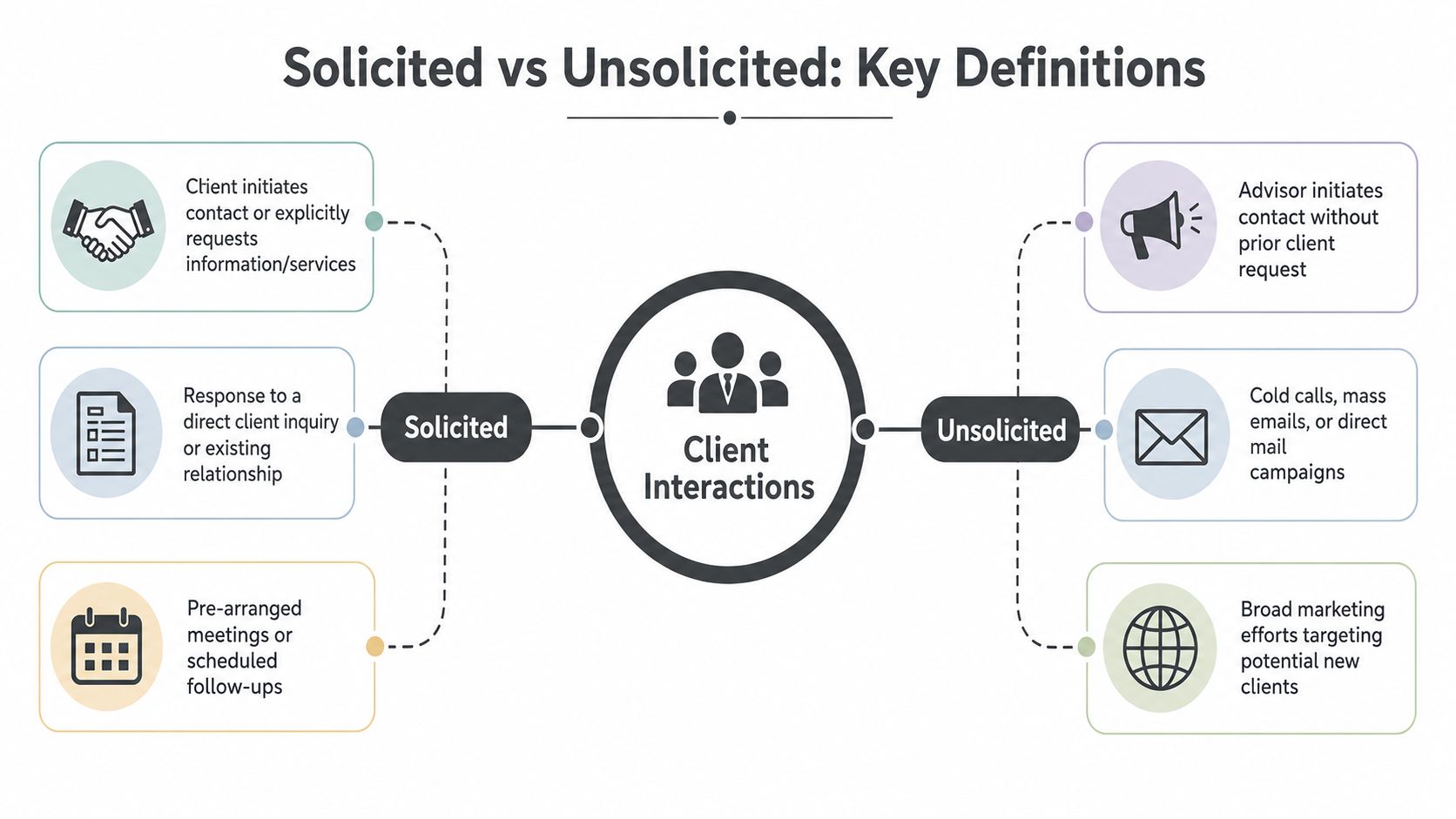

In a brokerage setting, the working question is straightforward: did the broker recommend the transaction, or did the customer initiate it? That classification carries direct compliance consequences. Trade confirmations commonly reflect the distinction with labels such as “SOL” for solicited and “UNSOL” for unsolicited, and those labels matter because solicited trades are tied to suitability review while unsolicited trades are generally treated as client-initiated orders, as summarized in this discussion of solicited and unsolicited trades.

That definition sounds clean until you apply it to actual conversations. A client calls and asks, “What do you think about adding something safer?” If you respond with general education, you may still be in a lower-risk zone. If you identify a specific security, recommend size, timing, or strategy, you may have crossed into a recommendation. The label on the order ticket should follow the substance of the interaction, not the preference of the representative or the branch.

Two contexts where advisors get into trouble

The first context is transactions. A solicited trade can trigger recommendation-based duties. An unsolicited trade usually narrows the broker's role to execution, but only if the record supports that the client brought the idea and pushed the decision.

The second context is employment and transitions. Advisors often use “solicitation” in a very different sense when they leave a firm. There, the dispute is not about a trade recommendation. It is about whether the advisor improperly contacted or encouraged clients to move accounts in violation of policy, contract, or a non-solicitation agreement.

| Context | Core question | Main risk | Best evidence |

|---|---|---|---|

| Securities trade | Who originated the idea for the transaction? | Suitability claim, supervisory criticism, arbitration exposure | Order ticket, trade confirmation, emails, notes, call records |

| Advisor transition | Did the advisor improperly invite clients to move business? | Injunction request, Form U5 language, contract dispute | Timing of communications, scripts, device records, CRM entries |

What works and what fails

A lot of advisors think “unsolicited” means the client ultimately said yes. That's wrong. A trade can still be solicited even if the client approved it quickly or called first for a general discussion.

Practical rule: If you supplied the actionable idea and steered the execution, assume reviewers may treat it as solicited unless the record clearly shows otherwise.

What works is a file that captures the origin of the idea in plain language. What fails is a file that uses the right code and the wrong facts. Regulators, arbitration counsel, and firms all know that mislabeling often happens after the fact.

Why This Distinction Is Critical for Your Career

The cost of getting this wrong isn't abstract. It shows up in customer arbitrations, internal reviews, termination memoranda, and the language a firm places on your regulatory record.

Classification changes the legal frame

When a broker recommends a trade, the legal analysis changes. That is why firms care so much about whether a transaction was solicited or unsolicited. A recommendation opens the door to suitability arguments and to scrutiny of what the advisor knew, what alternatives were discussed, and whether concentration, frequency, or product complexity should have triggered added review.

Misclassification also creates a credibility problem. In a dispute, opposing counsel will compare the coding on the order with the surrounding communications. If the messages sound like a sales push but the ticket says “UNSOL,” the argument becomes larger than one trade. It becomes a supervision and honesty issue.

It affects how others judge your conduct

A useful analogy comes from outside brokerage practice. Academic research on credit ratings found that unsolicited ratings averaged 0.9 notches lower on a 1-to-9 scale and were more conservative because they relied on public information rather than issuer-provided information, according to this academic paper on solicited and unsolicited ratings. That matters here for one reason. Once an event is labeled “unsolicited,” reviewers may ask whether the decision-maker had limited information, or whether the label is being used defensively because the full recommendation record is weak.

That dynamic shows up in employment disputes too. Firms frequently frame alleged solicitation during a departure as dishonesty, disloyalty, or disregard of policy. When that story reaches a Form U5 disclosure issue, the problem is no longer local. It can affect recruiting, licensing conversations, and how future firms view your risk profile.

The career flashpoints advisors underestimate

Three problem areas come up repeatedly:

- Form U5 language: Even if the firm lacks a final adjudication, it may still draft a narrative that forces you to defend your conduct later.

- Arbitration posture: The side that controls the classification early often shapes the theory of the case.

- Professional standards reviews: CFP Board inquiries and internal ethics reviews tend to focus hard on client communications, contemporaneous notes, and consistency.

The issue is rarely just what happened. The issue is what the documents let the other side say happened.

A strong defense usually starts before any dispute exists. Advisors who document the origin of ideas, preserve communications, and use compliant language during transitions are much harder to paint into a corner.

Real-World Scenarios A Comparative Analysis

Definitions don't protect you. Fact patterns do. The difference between solicited and unsolicited often turns on a few sentences, the timing of a follow-up, or whether the advisor moved from education into a recommendation.

Trade discussions that cross the line

Consider these side-by-side examples.

| Scenario | More likely classification | Why |

|---|---|---|

| Client calls and says, “Buy 500 shares of XYZ today.” Advisor confirms basic execution details and places order. | Unsolicited | The client brought the security and direction. |

| Client calls and says, “I have cash. Any ideas?” Advisor recommends a specific product and allocation. | Solicited | The advisor originated the actionable investment idea. |

| Client asks about a product discussed at a prior review. Advisor says, “I still recommend it, and this is the time to add.” | Solicited | The advisor renewed and advanced the recommendation. |

| Client emails after reading market news and asks for execution of a specific trade with no recommendation request. | Often unsolicited | Best case if the written record stays narrow and execution-focused. |

The hard cases sit in the middle. A client may start the conversation, but the advisor turns it into a recommendation through product selection, urgency, comparative analysis, or sizing guidance.

Departure communications that create avoidable claims

The same comparative approach helps in transition disputes.

Lower-risk announcement

- Purpose: Inform the client that the advisor has changed firms.

- Content: New contact information, neutral notice, no urging.

- Tone: Administrative, not persuasive.

- Timing: Sent after legal and firm-policy review.

Higher-risk communication

- Purpose: Prompt an account move.

- Content: “You should move quickly,” “I can take care of the transfer,” or criticism of the former firm.

- Tone: Sales-oriented or fear-based.

- Timing: Sent before the advisor is permitted to contact clients, or from questionable devices or accounts.

That difference may sound obvious on paper. In real life, advisors often blur it by trying to be “helpful.” Helpful language is what gets quoted back to you later.

Phrases that tend to increase risk

These statements often create problems because they sound like recommendations or active solicitation:

- “I think you should…” That phrase is classic recommendation language.

- “The best move is…” It suggests comparative judgment and direction.

- “Let me tell you what to buy.” No compliance department will save that wording.

- “Transfer now so you're protected.” In a transition dispute, that can look like improper inducement.

Safer phrasing is narrower and more factual.

- “You asked me to place this order.”

- “I can explain the mechanics and risks, but the decision is yours.”

- “This message is to notify you of my new contact information.”

Good defense language is plain, boring, and easy to verify later.

What arbitrators and reviewers usually examine

When the story is contested, decision-makers often focus on consistency across records. They compare:

- Order coding against emails and texts.

- Call notes against the customer's account of the discussion.

- Transition timelines against phone logs, CRM entries, and device usage.

An advisor can survive a bad fact. It is much harder to survive a bad fact pattern plus inconsistent records.

Navigating Modern Communication and Digital Gray Areas

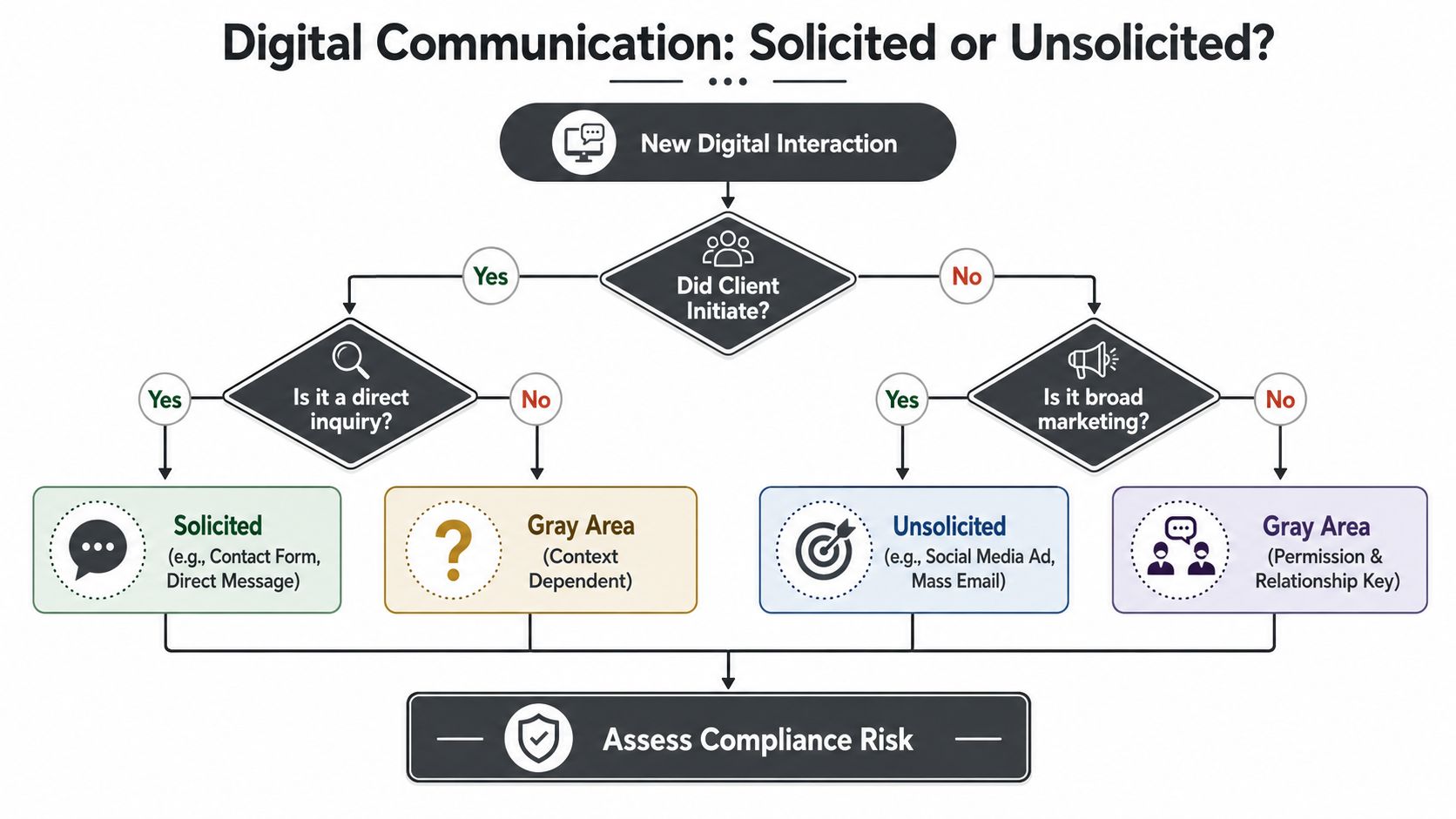

The most difficult questions today don't arise from branch desk conversations. They arise from website forms, LinkedIn messages, webinar follow-ups, referral texts, and AI-assisted communications.

Inbound contact does not end the analysis

Advisors often assume an inbound message automatically makes the conversation solicited in the safe sense. It doesn't. The better question is narrower: what exactly did the client request, and how far did your response go?

Practitioners often need answers to fact-specific questions like when a message becomes solicited if the contact began through a website form, as noted in this discussion of scenario-based content gaps. That same issue sits at the center of modern compliance reviews.

A website contact form asking for an appointment is one thing. A direct message asking whether a specific private deal is suitable is another. The first may support general follow-up. The second can quickly move into recommendation territory if the advisor responds with product-specific guidance instead of routing the matter through approved channels and proper documentation, especially in contexts involving private securities transactions.

A practical way to classify digital interactions

Use a simple decision path:

- Client initiated broad contact: You likely have permission to respond, but not unlimited permission to recommend.

- Client requested factual information: Keep the response factual and preserve the original inquiry.

- Advisor added a product suggestion or strategic judgment: Treat that as recommendation-sensitive.

- Message was mass-distributed or campaign-driven: It is far more likely to be viewed as unsolicited outreach.

Social and AI create a supervision problem

Social media creates hidden records and hidden risks. A “like” on a market post probably means little by itself. A direct reply saying, “DM me and I'll show you the best way to position before earnings,” is very different. Compliance reviewers won't focus on the platform name. They'll focus on the function of the message.

AI tools raise the next wave of problems. If an advisor uses AI to draft outreach, summarize chats, or suggest follow-up language, the firm still needs to know who initiated the communication, what the client asked, and whether the final message became promotional or advisory. The technology may accelerate the workflow, but it does not change the underlying classification problem.

If AI drafts the message, the advisor still owns the recommendation and the record.

The firms handling this well build controls around channel use, approval, retention, and escalation. The firms handling it poorly treat digital communication as informal and reconstructable. It rarely is.

Compliance and Documentation Best Practices

In a solicitation dispute, your best witness is usually the record you created before anyone expected a fight.

Preserve the recommendation trail

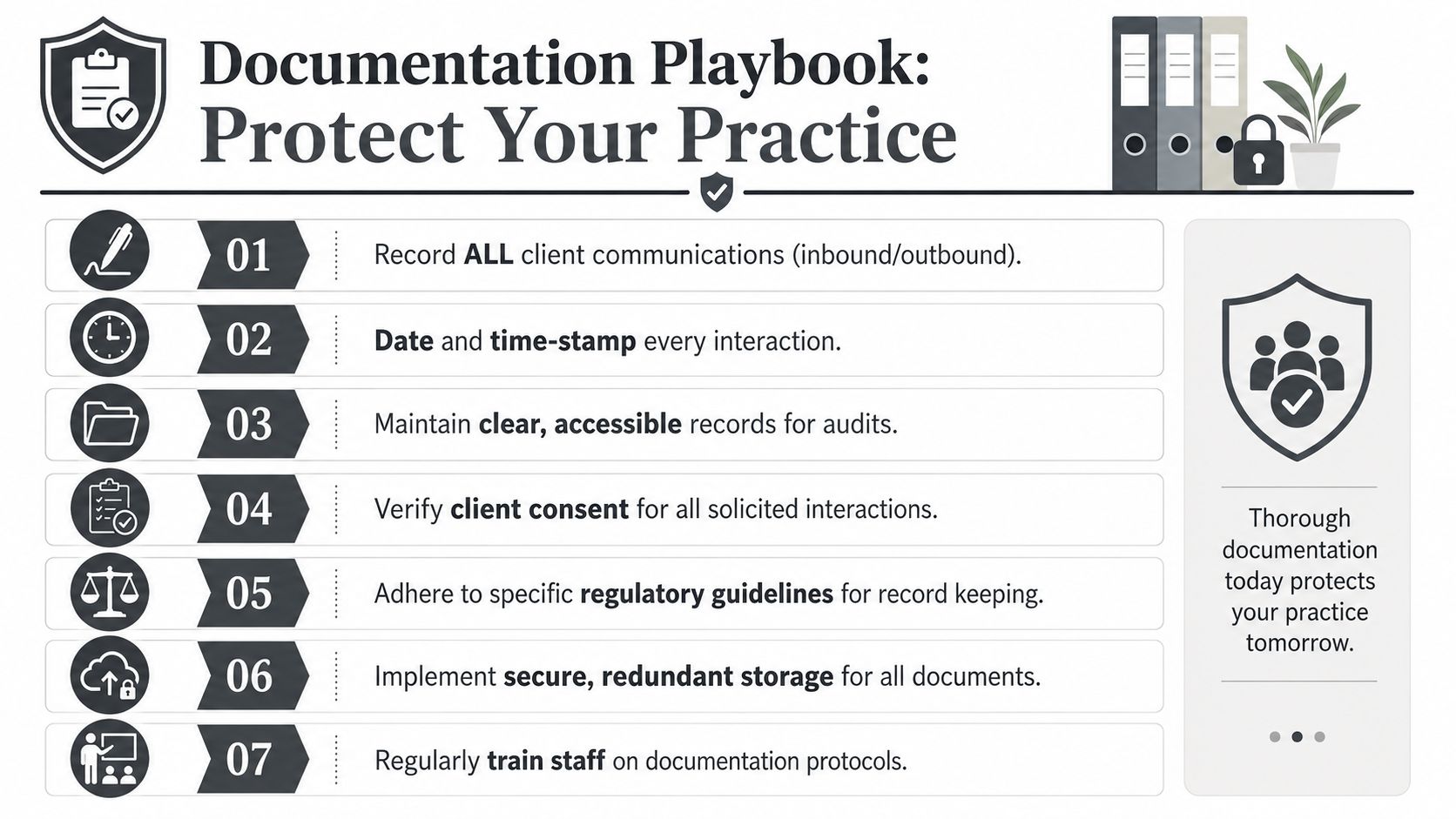

The most actionable point for defense is simple. Firms need to preserve the recommendation trail, including the trade confirmation, order ticket, and communications, because misclassifying a trade as unsolicited when it was broker-recommended can directly change liability exposure and whether a suitability claim is viable, as explained in this practitioner summary on preserving trade records.

That means documentation cannot be an afterthought. If the client initiated the trade, your notes should say so clearly. If you recommended the trade, the file should reflect the basis, the discussion, and the reason the recommendation fit the client's profile.

A defensible advisor file

The strongest files usually contain a mix of structured records and plain-language notes:

- Origin note: Record who initiated the conversation and how. “Client called requesting purchase of XYZ after reading issuer release.”

- Scope note: Capture whether the discussion stayed execution-only or moved into advice.

- Channel record: Preserve the email, text, CRM log, or approved messaging record.

- Order support: Make sure the order ticket coding matches the substance.

- Follow-up memorialization: Send a compliant recap when appropriate.

Supervisory habits that actually help

Some firms overcomplicate this. The basics still matter most.

- Use approved channels. Off-channel messaging creates evidence gaps and often forces the advisor to rely on memory.

- Write notes for a skeptical reader. If a branch examiner or arbitrator read your note in isolation, would it make sense?

- Train on edge cases. Generic annual training misses website inquiries, social replies, referrals, and transition scripts.

- Audit coding against communications. The easiest time to catch a mismatch is before a complaint arrives.

A clean “UNSOL” mark with no supporting record is weaker than many advisors think.

Documentation should be contemporaneous, specific, and dull. Dull records win credibility contests.

Litigation Strategies for Solicitation Disputes

Once an allegation surfaces, speed matters. Advisors often make the problem worse by sending explanatory emails, editing notes, or contacting clients to “clear things up.” That usually creates fresh evidence and new theories.

First moves that protect the defense

Start with preservation. Secure emails, texts, CRM notes, call logs, calendars, and any supervisory communications. If the dispute involves a departure, preserve the timeline of device use, announcements, and client contacts. If it involves a trade, isolate the records showing whether the customer or broker initiated the idea.

Then test the accusation against the documents. In many cases, the strongest defense is not a broad denial. It is a narrower point: the communication was administrative, educational, or customer-directed, and the file supports that characterization. That approach is often more persuasive than trying to argue every statement was harmless.

Common pressure points in these cases

- U5 and termination narratives: Challenge overbroad language early and with documentation.

- Arbitration claims: Force precision about who said what, when, and through which channel.

- Restrictive covenant allegations: Examine whether the communication fits the contract language and the actual facts surrounding the contact, especially where a claimed restrictive covenant breach depends on timing and wording.

The advisors in the strongest position usually did one thing right long before the dispute began. They created records that a neutral third party can trust.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.