When a customer or client doesn't pay, it can feel like you're out of options, watching your cash flow dry up while your financial stability takes a hit. The good news is, the law gives you a powerful set of legal remedies known as creditor’s rights, designed specifically to help you recover the money you are rightfully owed.

Your Fundamental Rights as a Creditor

For any business owner in Connecticut, the process of collecting a debt can be incredibly frustrating. You send invoice after invoice, and the silence on the other end is deafening. But you’re not powerless. The legal system provides a clear path for creditors to pursue payment, effectively turning an overdue bill into a recoverable asset.

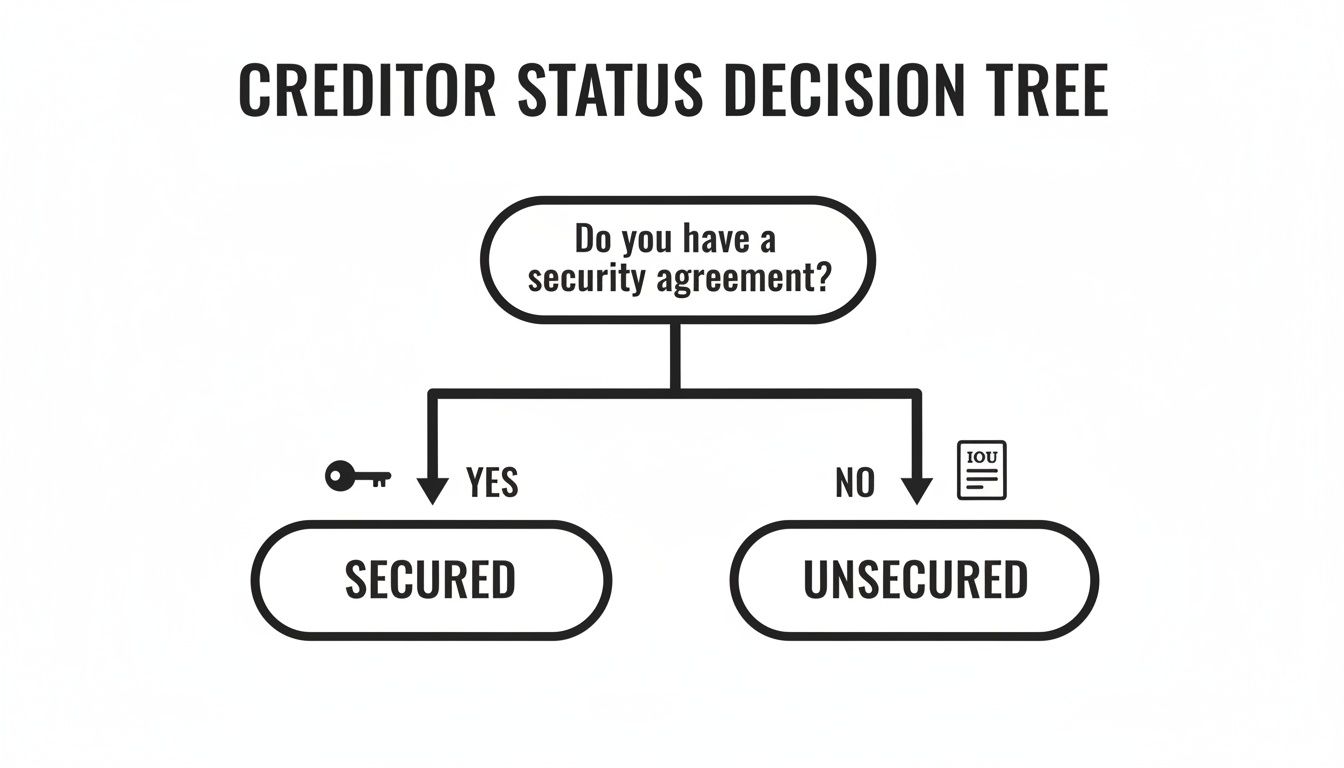

Think of your creditor’s rights as a legal toolkit. Each tool serves a specific purpose, and the key to protecting your business is knowing which one to use and when. The first, most critical question you have to answer is this: is your debt secured or unsecured?

The Core Distinction: Secured vs. Unsecured Claims

This single distinction is the bedrock of all creditor rights. It will shape your entire collection strategy from start to finish.

Secured Creditor: Let's say you sold heavy machinery to a construction company. As part of the deal, you had them sign a security agreement that specifically names the equipment as collateral for the loan. In this scenario, you are a secured creditor. You have a direct, legally recognized interest in that asset. If the company defaults, you have priority—it’s like holding a key to that piece of machinery.

Unsecured Creditor: Now, imagine you're a marketing consultant who provided services based on a standard invoice. If you don't have any collateral backing that invoice, you are an unsecured creditor. Your claim is absolutely valid, but it’s a general claim against the business, not tied to any specific asset. Your first job is to turn that general claim into something with more teeth: a court judgment.

Getting a handle on this difference is the first real step toward enforcing your rights. Being in a secured position puts you at the front of the line and opens the door to more direct methods of recovery. If you’re unsecured, your immediate goal is to legally validate your claim so you can access the powerful enforcement tools available to a judgment creditor.

If you’re a business owner struggling with unpaid debts, figuring out your creditor status is the starting point for taking back control. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Secured vs. Unsecured Debt: What It Means for Your Business

When you’re owed money, your ability to collect hinges on one critical question: is the debt secured or unsecured? Not all debts are treated the same under the law.

This single distinction determines your legal power, the collection tools you can use, and where you stand in line if other creditors are also trying to collect. For any business, understanding this isn't just a legal exercise—it's fundamental to managing risk, often decided the moment you extend credit.

The Power of Being a Secured Creditor

A secured creditor holds the strongest position because the debt is tied directly to a specific asset, known as collateral. This connection gives you a legal claim, or a lien, against that property.

Let's say your business finances a $100,000 piece of equipment for a customer. As part of the deal, you have them sign a security agreement. This document is your leverage; it makes the equipment itself the guarantee for the loan.

If that customer stops paying, you don’t have to get in the back of the line with everyone else they owe. Your security agreement gives you the right to go after the collateral directly. This often means repossessing the equipment, selling it, and using the proceeds to cover your loss.

Key Insight: Think of a security agreement as legally calling "dibs" on an asset. It turns a simple IOU into a real, tangible interest in property, giving you a massive advantage if the debt goes bad.

However, having the agreement is just the first step. To fully protect your claim against others, you need to "perfect" your security interest. You can learn more about this process in our deep dive on what it means to be a secured creditor.

Perfecting Your Security Interest

Perfection is simply the legal act of putting the public on notice that you have a claim on an asset. For most business assets, this is done by filing a UCC-1 financing statement with the correct state office, which is usually the Secretary of the State.

It’s a lot like recording the deed to a house. That UCC filing announces to the world that you have a lien on that specific piece of collateral. This is absolutely critical for establishing your priority over:

- Other creditors who might try to make a claim on the same asset.

- A bankruptcy trustee if the debtor files for bankruptcy.

- Anyone who tries to buy the asset from the debtor, unaware of your lien.

If you fail to perfect your interest, another creditor could file their own lien and legally jump ahead of you in line—even if your agreement was signed first.

As this shows, the path your collection efforts will take is set from the very beginning. It all comes down to whether you have a security agreement in place.

The Path of the Unsecured Creditor

An unsecured creditor, by contrast, is owed money without any collateral to back it up. This is a very common scenario for businesses.

Typical examples include:

- Suppliers providing materials or goods based on a simple invoice.

- Consultants, marketers, and other professionals billing for services rendered.

- Lenders who extended credit on a signature loan without taking any property as collateral.

Your claim is still perfectly valid, but it’s a general obligation. You have no right to any specific asset. This means that if the debtor defaults, your road to recovery looks quite different and is often much tougher.

Without collateral to repossess, your first goal is to turn that unpaid invoice or promissory note into a court judgment. That judgment is the key that unlocks the powerful legal tools you need to collect, like bank levies, wage garnishments, and property liens. Until you have it, you're mostly limited to sending letters and making phone calls.

The following table breaks down the fundamental differences between these two creditor statuses.

Secured vs Unsecured Creditor Rights at a Glance

| Feature | Secured Creditor | Unsecured Creditor |

|---|---|---|

| Basis of Claim | A security agreement granting rights to specific collateral. | A general promise to pay (e.g., invoice, promissory note). |

| Primary Remedy | Repossession or foreclosure on the collateral. | Must first obtain a court judgment. |

| Collection Tools | Self-help repossession (UCC), foreclosure sale. | Post-judgment enforcement (garnishments, levies, liens). |

| Priority in Bankruptcy | Paid first from the proceeds of the collateral. | Paid from remaining assets, often pennies on the dollar. |

| Risk Level | Lower. The collateral provides a direct source of recovery. | Higher. Recovery depends on the debtor's overall financial health. |

Understanding where you fall in this table is the first step toward building an effective collection strategy and protecting your bottom line.

Navigating these distinctions is crucial for protecting your business. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Your Toolkit for Enforcing a Connecticut Judgment

Winning your lawsuit is a huge milestone, but getting the judgment is only half the battle. That court order is a powerful piece of paper, but it won’t magically deposit money into your account. The real work begins now: using that judgment to actually collect the money you’re owed.

In Connecticut, a judgment gives you access to a specific set of legal tools designed to enforce the court’s ruling. Think of your judgment as the key, but you still have to know which doors to open. Knowing how to use these enforcement methods is what turns a paper victory into a financial recovery.

The Bank Execution: A Direct Line to Cash

One of the most powerful and immediate tools is the bank execution, often called a bank levy. This legal action allows you to go straight to the source and seize funds directly from your debtor's bank accounts.

Once you have your judgment, you can apply for a bank execution from the court. A state marshal takes that order and serves it on any bank where you believe the debtor keeps their money. The bank is then legally obligated to freeze the account and turn over any non-exempt funds, up to the full amount of your judgment. For a business creditor, this is often the quickest path to getting paid.

Real-World Scenario: Imagine you sold $25,000 in materials to a local builder who then ghosted you. After you win a judgment, an asset search locates their business checking account. With a bank execution, a marshal serves the bank, which freezes the account and sends you the funds, often satisfying the entire debt in one swift move.

Wage Executions: Intercepting Income at the Source

If your debtor is an individual earning a regular paycheck, a wage execution—or wage garnishment—is an excellent strategy. This lets you collect your debt by taking a portion of the debtor's earnings before they even touch it.

The process involves filing an application with the court post-judgment. Once approved, the order is served on the debtor's employer. The employer is then legally required to withhold a percentage of the employee's disposable income each pay period and send it directly to you. While Connecticut law caps the garnishment amount to leave the debtor with enough to live on, it creates a steady and reliable payment stream until your judgment is paid in full.

Property Liens: Securing Your Claim Against Real Estate

For larger judgments, or when the debtor owns property, filing a judgment lien is a smart, long-term move. A judgment lien officially attaches your debt to the debtor's real estate, like their house or a commercial building, making your claim public record.

To do this, the judgment is recorded in the land records for the town where the property sits. This lien essentially puts a "cloud" on the property's title, creating serious leverage.

- It blocks the debtor from selling the property without paying your judgment first, since a new buyer won’t accept a clouded title.

- It prevents the debtor from refinancing their mortgage, as lenders won’t issue a new loan until your lien is cleared.

This powerful tool effectively converts your unsecured judgment into a secured debt backed by a tangible, high-value asset. It may not lead to an immediate payout, but it secures your place in line and ensures you get paid when the property is eventually sold or refinanced. You can find more details in our guide that explains how to enforce a judgment in Connecticut.

Navigating judgment enforcement requires precision and an understanding of the legal process. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Advanced Collection Methods: Repossession and Foreclosure

If you’re a secured creditor, you have powerful tools that go far beyond a standard court judgment. When a debt is backed by collateral, your rights expand, giving you a more direct—and often faster—path to recovery without getting bogged down in a lengthy court process.

Two of the most effective strategies for secured creditors are UCC repossession and real estate foreclosure. These remedies let you target the specific property pledged as collateral, giving you a direct line to getting repaid when a borrower defaults. Knowing how and when to use them is crucial for protecting your financial interests.

UCC Repossession Without a Court Order

The Uniform Commercial Code (UCC) gives creditors a potent self-help remedy when the collateral is personal property—things like vehicles, equipment, or business inventory. Under the UCC, you have the right to repossess that collateral directly from the debtor after a default, often without needing a court order.

This is a massive advantage, saving you significant time and legal fees. But this right comes with a critical string attached: the repossession absolutely must be peaceful.

Critical Limitation: You cannot "breach the peace" during a repossession. This means no force, no threats, no breaking into a locked garage, and no heated confrontations with the debtor. A peaceful repossession is the only way to stay on the right side of the law.

If a peaceful repossession isn’t possible—maybe the debtor hides the property or refuses to hand it over—you have to stop. Your next move is to seek a court order through a legal action called replevin. In a replevin action, the court orders the debtor to return the property, which then allows a state marshal to legally seize it on your behalf.

Foreclosure on Real Estate Collateral

When real estate is the collateral, the process for taking control of the property is called foreclosure. Unlike a UCC repossession, foreclosure is a formal legal process that must go through the courts. It’s the primary way a secured creditor can enforce their rights against a commercial building, a plot of land, or other real property.

In Connecticut, foreclosure generally takes one of two forms:

- Strict Foreclosure: This is the most common path in the state. The court establishes a "Law Day," which is the final, non-negotiable deadline for the debtor to pay the entire debt. If they fail to pay by that date, full ownership of the property transfers directly to you as the creditor, with no public sale.

- Foreclosure by Sale: In this scenario, the court orders the property to be sold at a public auction. The money from the sale is first used to pay off your mortgage debt. Any leftover funds are distributed to other lienholders or, if any remains, back to the debtor. This method is usually preferred when the property has significant equity.

Each approach has distinct strategic benefits. You can find more details in our guide on foreclosing a lien in Connecticut.

Of course, these aren't the only strategies available. For creditors thinking about using third-party help, it's vital to understand the legal requirements, and resources like a Debt Collection Agency License Guide can be useful.

Successfully executing these advanced collection methods demands strict adherence to legal procedure. One wrong move can open the door to legal challenges from the debtor and expose you to liability.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How a Debtor's Bankruptcy Filing Changes Everything

Receiving a bankruptcy notice can feel like a dead end for an unpaid debt. After all your efforts to collect, a bankruptcy filing instantly stops all collection activity in its tracks. While it completely changes the rules, it doesn’t automatically mean you’ll never see a dime—it just means you need a new game plan, and you need it fast.

The moment a debtor files for bankruptcy, an automatic stay goes into effect. This is a powerful federal court injunction that freezes nearly all collection activities against the debtor and their property. As a creditor, you must immediately cease all attempts to collect.

This includes:

- Making phone calls or sending demand letters

- Filing or continuing a lawsuit

- Enforcing a judgment with wage garnishments or bank levies

- Starting repossession or foreclosure proceedings

Ignoring the automatic stay, even by mistake, can bring serious penalties from the bankruptcy court. It is a strict, legally binding order to stand down and let the court’s process unfold.

The Different Chapters and Your Strategy

The type of bankruptcy chapter filed will determine what happens next and what your chances of recovery look like. It's critical to find bankruptcy filings and understand which path the debtor has taken. The three you'll see most often are Chapter 7, Chapter 13, and Chapter 11.

Chapter 7 Bankruptcy (Liquidation): Often called a "straight bankruptcy," a court-appointed trustee sells the debtor's non-exempt assets. The cash from that sale is then paid out to creditors based on a strict priority system. For a business, this usually means it closes its doors for good.

Chapter 13 Bankruptcy (Individual Reorganization): This chapter is for individuals who have a regular income. The debtor creates a repayment plan lasting 3 to 5 years to pay back all or part of their debts. As a creditor, you might receive payments over the course of the plan.

Chapter 11 Bankruptcy (Business Reorganization): This is most common for businesses that want to stay open while they reorganize their finances. The business proposes a plan to repay creditors over time, and creditors typically have the right to vote on whether to approve it.

The Hierarchy of Creditors and Filing a Proof of Claim

In bankruptcy, not all creditors are created equal. The law follows an "absolute priority rule" that creates a clear pecking order for who gets paid first.

Key Takeaway: Secured creditors are at the front of the line. Since their debt is attached to specific collateral, their claim is tied directly to the value of that asset. Unsecured creditors are paid from whatever is left over, which often means they recover only a small fraction of what they're owed—if anything at all.

To have any hope of recovery, you must take one critical action: file a proof of claim with the bankruptcy court. This is the official form that tells the court who you are, what you're owed, and why. If you miss the court’s deadline to file this claim, your debt won't be recognized in the case, and you will lose any right to payment.

Navigating the complexities of a bankruptcy case requires careful attention to deadlines and procedures. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Getting Ahead of the Problem: Proactive Steps and When to Get Help

The best way to handle a problem debt is to prevent it from happening in the first place. While Connecticut law offers plenty of tools for collecting what you're owed, a little foresight can save you an enormous amount of time, money, and headaches down the road.

It all starts with your paperwork. Your credit applications, contracts, and service agreements are more than just formalities—they are the foundation of your rights as a creditor. A solid credit application lets you properly screen new customers. A clear contract locks in your payment terms, interest for late payments, and the debtor's responsibility for collection costs.

For any significant transaction, a security agreement is your single most powerful tool.

Spotting a Credit Risk Early

Good paperwork is just the start; you also have to stay alert. Customers don’t usually default out of the blue. There are almost always warning signs, and catching them early gives you a chance to protect yourself by tightening credit or pausing work.

Keep an eye out for these red flags:

- Shifting Payment Patterns: A reliable customer who always paid on time suddenly starts falling behind.

- Small, Partial Payments: Instead of clearing invoices, they start sending sporadic, small amounts.

- Going Silent: Your calls and emails about the overdue balance are suddenly met with silence.

- A Pattern of Excuses: They always have a new reason why the payment is "on its way" but never arrives.

The moment you spot these behaviors, it's time to act. Stop extending more credit and shift your focus from making sales to collecting what's owed. Continuing to sell to a high-risk account only digs a deeper hole.

Knowing When to Call a Professional

You can handle the initial collection calls and letters on your own, but there are definite points where you need to bring in legal help. Trying to navigate the legal system alone can lead to expensive mistakes and lost opportunities.

You should contact an attorney as soon as:

- The debtor argues about the debt or threatens to sue you.

- You need to enforce a security agreement by repossessing collateral or foreclosing on property.

- You get a notice that the debtor has filed for bankruptcy.

- The amount owed is large enough that the risk of losing it is greater than the cost of legal help.

A strategic approach is key to protecting your assets. An experienced attorney can evaluate your position, navigate the legal system, and implement the most effective strategies to enforce your rights as a creditor and recover what you are owed.

Protecting your business from bad debt requires both foresight and decisive action. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181 for guidance.

Your Top Questions About Creditor Rights in Connecticut

When you're trying to recover money you're owed, you're bound to have questions. Here are some of the most common issues we see Connecticut business owners face, along with the straightforward answers you need.

How Long Do I Have to Collect a Debt in Connecticut?

The clock is always ticking. In Connecticut, you generally have six years to file a lawsuit on a written contract. If your agreement was verbal, that window shrinks to just three years. It's critical to take legal action before that deadline passes, or you could lose your right to collect entirely.

However, once you secure a court judgment, the game changes. A judgment gives you a much longer runway for collection—it’s typically enforceable for at least twenty years and can often be renewed. This allows you to use powerful tools like liens and garnishments for a long time to come.

Can I Go After a Debtor's House or Car?

Yes, but it’s not always simple. The answer depends entirely on whether your debt is secured or unsecured. If the house or car was pledged as specific collateral for your loan, you have a direct path to foreclosure (for real estate) or repossession (for a vehicle).

If you’re an unsecured creditor, you first need to win a judgment in court. You can then place a lien on the debtor’s property, but Connecticut's "exemption" laws come into play. These laws protect a certain amount of equity in a person's primary home and value in one car, shielding them from seizure. An attorney’s help is vital to figure out what assets are actually collectible.

Should I Accept a Settlement for Less Than I'm Owed?

This is a classic business calculation. A prompt, guaranteed partial payment is often far more valuable than a long, expensive legal battle that you might not even win—especially if the debtor is teetering on the edge of bankruptcy.

Before you accept any offer, you need to weigh the pros and cons. Think about the debtor's financial health, the certainty of getting cash in hand now, and whether your debt is secured. It's always wise to have an attorney review a settlement offer to make sure the agreement is solid and you aren't sacrificing too much leverage.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.