An investment dispute rarely starts with a dramatic courtroom moment. It usually starts with a missed payment, a capital call that doesn't happen, a partner who diverts an opportunity, a broker-dealer that changes compensation terms, or a regulator's inquiry that suddenly turns an internal problem into a business-threatening one.

For business owners and financial professionals, investment dispute resolution is less about abstract legal doctrine and more about protecting value. The core question is usually practical. Where should this fight happen, how quickly can it be contained, what records will control the outcome, and how much collateral damage will the dispute cause while it's pending?

When Investments and Partnerships Go Wrong

A common pattern looks like this. Two parties invest in a venture with a strong term sheet, a decent operating agreement, and optimism about growth. Then performance drops, reporting gets thin, one side stops honoring key obligations, and each side thinks the other changed the deal after money was already committed.

At that point, many clients make the same mistake. They treat the dispute as if the only issue is whether they're right on the facts. That's almost never enough. The forum, the contract language, the timing of notice, the quality of the paper trail, and the available interim remedies often matter just as much as the underlying breach.

That's especially true when the relationship still has some value. A joint venture may be salvageable. A compensation dispute with a departing financial advisor may be resolvable without a scorched-earth filing. A private investment conflict may call for a demand and structured negotiation before anyone files a claim. In partnership settings, the first move often determines whether the case becomes a solvable business dispute or an expensive personal war. For a useful overview of that dynamic, see this discussion of business partnership dispute resolution.

The first questions that actually matter

Before drafting a complaint or arbitration demand, answer these:

- What governs the dispute: Is the claim driven by contract, securities rules, employment terms, corporate documents, or an investment treaty?

- Where must it be filed: Court, private arbitration, FINRA, mediation, or an international forum?

- What needs to happen first: Notice, cure opportunity, internal escalation, mediation, or a cooling-off period?

- What business risk sits beside the legal claim: Frozen accounts, investor pressure, reputational damage, employee departures, or regulatory follow-on issues?

Practical rule: The strongest party at the outset usually isn't the party that's most offended. It's the party that preserved documents early, chose the right forum, and made the first procedurally correct move.

What works and what usually backfires

What works is disciplined sequencing. Preserve records. Review the dispute clause. Identify any pre-filing requirements. Decide whether advantage stems from speed, confidentiality, injunctive relief, or settlement pressure.

What backfires is impulsive escalation. Threatening litigation without checking the forum clause can weaken your position. Sending a vague demand can lock you into an underdeveloped theory. And airing the dispute publicly may satisfy emotion while damaging the economics of a later settlement.

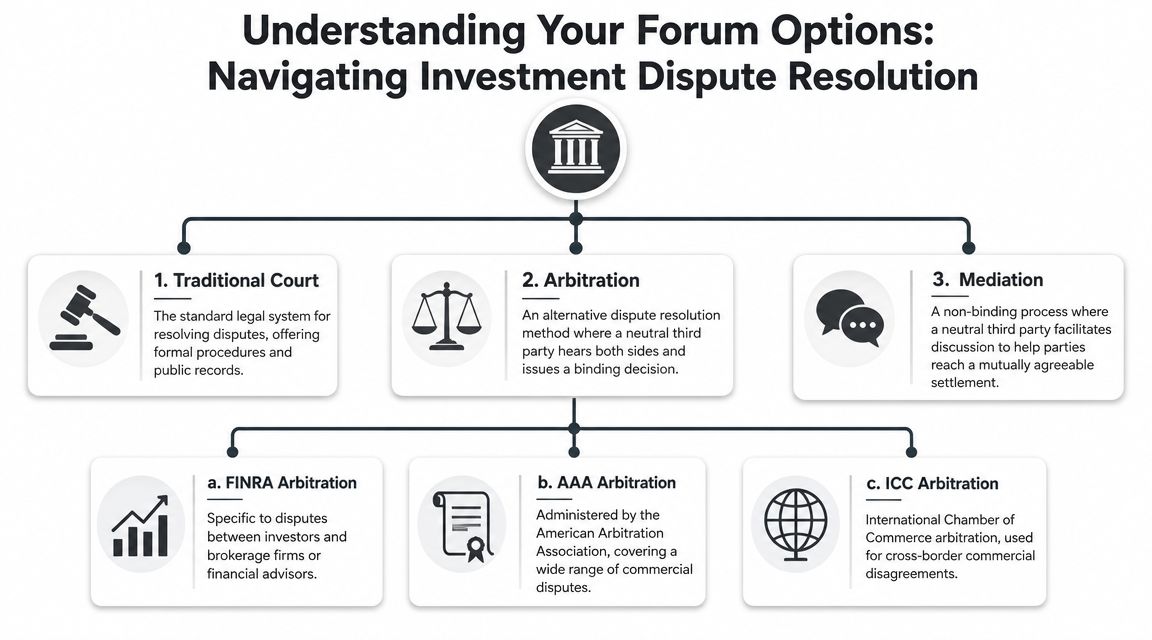

Understanding Your Forum Options

The biggest source of wasted legal spend in investment disputes is filing in the wrong place, or preparing for the wrong kind of proceeding. Courts, commercial arbitration, FINRA arbitration, mediation, and investor-state arbitration all serve different purposes. Their authority comes from different sources, and each one changes the pressure points of the case.

Traditional court

Courts remain the default forum when there's no enforceable arbitration clause, when emergency injunctive relief is essential, or when a statute creates a court-based remedy. Courts are public. Procedure is formal. Discovery is often broader than in arbitration. That can help if the key evidence sits with the other side.

Courts also create pressure through motion practice and public filings. Sometimes that's useful. Sometimes it's destructive. If the dispute touches sensitive investor communications, personnel issues, or confidential compensation structures, publicity can become its own problem.

Commercial arbitration

Commercial arbitration exists because discerning parties often want a private, contract-driven alternative to court. The authority usually comes from the agreement itself. A clause may call for AAA, JAMS, or ICC administration, define the seat of arbitration, and specify how arbitrators are selected.

For cross-border matters, commercial arbitration is far from niche. In 2024, the ICC reported 831 new arbitration cases, 1,789 pending arbitration cases at year-end, and a total caseload value of US$354 billion, which the ICC described as the highest ever total value of cases pending at year end in its 2024 dispute resolution statistics. That scale matters because it shows how often serious investment and commercial conflicts are routed into arbitration rather than national courts.

Commercial arbitration often works well when parties need decision-makers who can handle complex deal structures, valuation disputes, earn-out fights, or cross-border enforcement concerns. A practical comparison of process choices appears in this guide to alternative dispute resolution vs litigation.

FINRA arbitration

FINRA arbitration is its own world. It applies to many disputes involving customers, brokerage firms, registered representatives, compensation issues, promissory notes, team transitions, and other securities industry conflicts. Its authority usually comes from FINRA rules, industry registration, account agreements, or employment-related documents that tie the parties into the FINRA system.

This forum is highly specific. That specificity cuts both ways. It can be efficient because the process is familiar to industry participants. But a generic commercial strategy often misses the issues that drive outcome in securities disputes, such as disclosures, supervisory records, production data, communications with clients, and the practical consequences of Form U5 language.

In financial industry cases, the forum is not just a venue decision. It shapes how the story is told, which records matter most, and whether the dispute stays a compensation fight or expands into a regulatory problem.

Investor-state arbitration and mediation

Investor-state arbitration is different from both court litigation and ordinary commercial arbitration. Its authority comes from treaties, investment laws, or state contracts that permit an investor to bring claims against a state. It's designed for cross-border disputes involving state conduct, regulation, expropriation-type claims, and treaty protections.

Mediation belongs in this list because it isn't merely an off-ramp after a failed case. In many matters, it's a first-order strategic choice. It can preserve counterpart relationships, reduce public damage, and surface business solutions that a tribunal cannot order.

Choosing the Right Battlefield

Once the available forums are identified, the next task is choosing the one that advances the business objective instead of just satisfying the legal instinct to fight. Some disputes require public court intervention. Others benefit from the privacy and narrower procedure of arbitration. Some financial industry claims effectively belong in FINRA from the start. Cross-border sovereign disputes sit in an entirely different category.

Investor-state proceedings show how substantial these cases can be. By the end of 2023, the total number of known ISDS cases reached 1,332, with roughly one third involving energy supply and extractive industries, according to UNCTAD's ISDS facts and figures. That matters because it confirms these disputes often arise where projects are capital-intensive, heavily regulated, and exposed to policy shifts.

The comparison that clients actually need

| Criterion | Court Litigation | Commercial Arbitration | FINRA Arbitration | Investor-State Arbitration |

|---|---|---|---|---|

| Source of authority | Statute, common law, procedural rules | Contract and arbitration rules | FINRA rules, account or industry obligations | Treaty, investment law, or state consent |

| Public or private | Usually public | Often more private than court | Not the same as public court litigation, but not fully insulated from broader consequences | Commonly subject to transparency issues and public scrutiny concerns |

| Discovery | Often broad | Usually more limited and targeted | Structured around forum practice and the specific dispute | Often document-heavy and procedurally complex |

| Decision-maker | Judge or jury, depending on claim | Arbitrator or panel chosen through agreed process | Arbitrator panel within FINRA framework | Specialized tribunal |

| Best use case | Emergency relief, statutory claims, cases needing broad discovery | Contract-heavy, cross-border, confidential business disputes | Securities industry customer, employment, compensation, and promissory note disputes | Cross-border disputes involving state action and protected investments |

| Main risk | Cost, delay, publicity | Upfront filing and arbitrator costs, limited appeal | Industry-specific procedure can punish weak documentation | Jurisdiction fights, treaty prerequisites, and extended procedural battles |

A practical way to decide

Use these filters first:

- Need for immediate court power: If assets, trade secrets, client relationships, or governance control are at risk right now, court may be necessary.

- Need for confidentiality: If the case involves investor communications, internal compensation structures, or reputational sensitivity, arbitration may better protect the business.

- Need for industry expertise: FINRA often makes sense where the dispute turns on brokerage practice, supervision, client servicing, or compensation grids.

- Cross-border enforceability: If counterparties or assets are spread across jurisdictions, arbitration may offer better enforcement planning than a domestic judgment.

For advisors and firms in the securities space, forum selection becomes highly tactical. A dispute over deferred compensation may look like a contract case on paper, but in practice it can also affect registration, recruiting, internal investigations, and future production. That's why firms and advisors should understand the FINRA arbitration process before taking a hard position.

What clients often underestimate

They underestimate second-order effects.

A business owner may focus on recovering money and miss the strategic advantage created by a confidentiality provision. A financial advisor may focus on defending a promissory note claim and miss the long-term consequences of disclosure language that affects future employment. An investor may push for arbitration without realizing that a poorly drafted pre-dispute notice can hand the other side a threshold defense before the merits are ever reached.

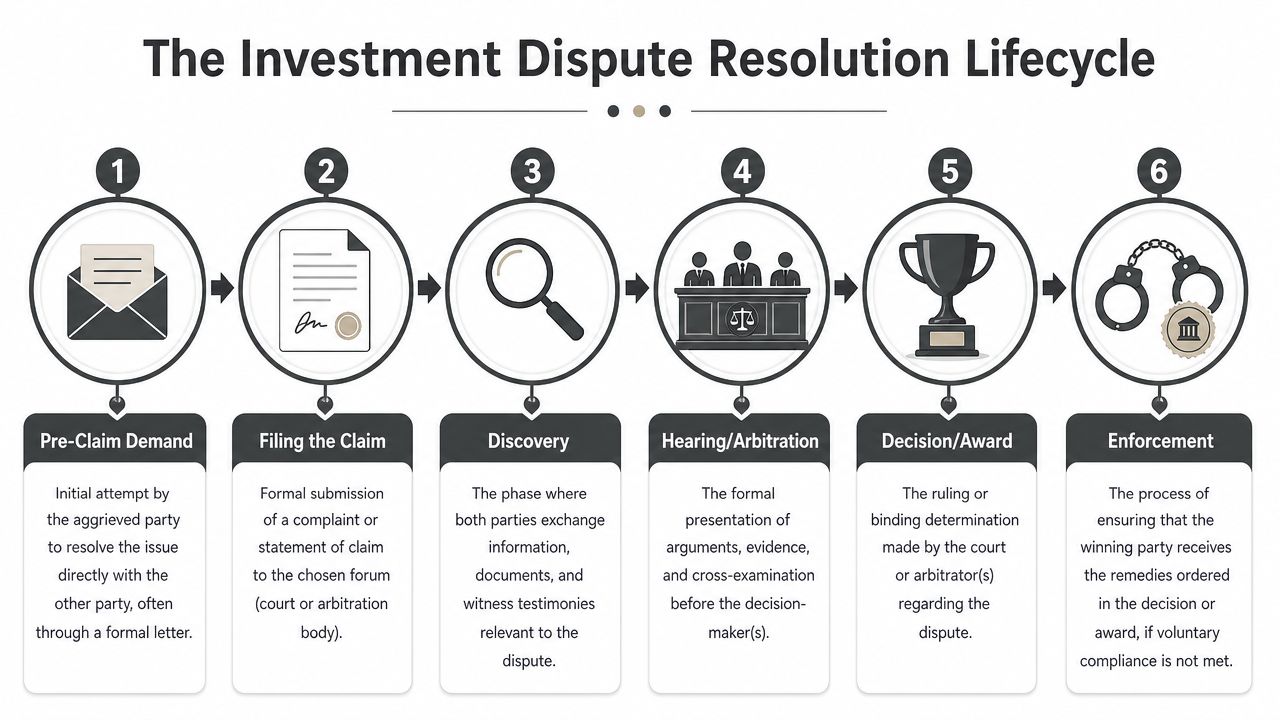

The Typical Dispute Resolution Process

Most disputes follow the same broad arc even when the forum changes. The details differ, but the core sequence is familiar. The party with the better process discipline usually gains an advantage early, long before the hearing.

Pre-claim work

Strong cases often begin with detailed preparation. Counsel reviews the contract set, notices, amendments, side letters, email traffic, and internal records to identify the claims that fit the governing documents. That sounds obvious, but many parties act on grievance first and contract second.

Early work usually includes a preservation step, a demand letter if appropriate, and a forum analysis. In some matters, that period also serves a business purpose. It gives the other side a chance to cure, buy out, restructure, or narrow the dispute before formal positions harden.

Filing and threshold fights

Then comes the formal filing. In court, that means a complaint. In arbitration, it usually means a demand or request under the applicable rules. In treaty-based matters, pre-filing requirements can matter as much as the claim itself.

Many modern investment dispute clauses build in procedural gateways. ICSID notes in its overview of mediation in treaties that newer clauses can require detailed notice content and pre-arbitration amicable procedures, and failure to satisfy notice-and-cooling-off requirements can trigger admissibility or jurisdiction disputes. In practice, that means a rushed filing can create avoidable delay and cost.

The opening phase is where avoidable mistakes happen. Parties file too fast, notice too little, or commit to a damages theory before the documents are fully organized.

Discovery and hearing

Discovery is where budget discipline either survives or collapses. Court litigation often allows broader requests, third-party subpoenas, and more extensive deposition practice. Arbitration usually narrows the field. That can reduce cost, but it can also hurt a party that needs broad access to the other side's records.

The hearing phase reflects the forum's personality. Court trials are formal and public. Arbitrations are often more concentrated, with fewer procedural layers between the evidence and the decision-maker. FINRA proceedings have their own rhythms and expectations, particularly around customer files, supervisory material, communications, and damages presentation.

Award, judgment, and enforcement

Winning on paper isn't the end. The final phase is collection, compliance, or enforcement. A judgment or award has value only if it can be turned into payment, specific performance, corrected disclosures, or some other concrete result.

That's why the case should be built backward from the remedy. If the target is money, think about collectability early. If the target is business separation, think about transition restrictions and client communication issues early. If the target is reputational repair, shape the record with that end in mind from the beginning.

Drafting Ironclad Dispute Resolution Clauses

The dispute resolution clause is often treated like boilerplate. That's a drafting mistake with expensive consequences. When the relationship breaks down, this clause determines where the fight happens, how quickly it starts, who decides it, and what procedural obstacles sit in the way.

A strong clause doesn't guarantee victory. It does something more realistic and more valuable. It reduces uncertainty.

Terms that deserve careful drafting

The basic elements should be explicit, not implied:

- Forum selection: Specify court, arbitration, FINRA where applicable, or a tiered process.

- Seat and venue: For arbitration, identify the seat and hearing location if that matters.

- Governing law: Choice-of-law fights consume time and money. Resolve them in advance.

- Arbitrator structure: State whether the matter goes to one arbitrator or a panel.

- Scope: Clarify whether the clause covers tort, statutory, equitable, and affiliate-related claims.

Businesses that use form agreements should also review whether the dispute clause fits the transaction. A consulting engagement, investment side letter, operating agreement, and recruiting package for a financial advisor should not all use the same template language. If you're reviewing starting points, resources like these top 12 consulting contract templates can help identify common clause architecture, but the final language should be suited to the actual deal and risk profile.

Pre-arbitration steps can help or hurt

Mandatory pre-filing steps are powerful when drafted well and dangerous when drafted lazily. A notice requirement can force the claimant to crystallize the theory of breach. A cooling-off period can create room for business resolution. A mediation requirement can prevent a manageable dispute from becoming procedural trench warfare.

But these provisions only work if they're clear. Ambiguous sequencing creates satellite litigation over whether the claim was ripe. Overly rigid language can let a counterparty exploit technical defects without addressing the merits.

That's one reason forum clauses deserve independent attention. A well-drafted forum selection clause can remove doubt about venue and reduce the chance of expensive threshold motion practice before the actual dispute is even reached.

Drafting advice that matters in practice: write the clause as if the relationship will end badly and both sides will read every verb against each other.

What strong drafting looks like

Strong drafting is concrete. It names the forum, states the governing law, defines the covered disputes, and coordinates notice, mediation, and filing steps in the right order.

Weak drafting relies on broad labels like “any disputes will be resolved amicably” or “the parties may arbitrate.” That kind of language invites fights over whether arbitration is mandatory, whether mediation is required, and whether a court can still hear parallel claims. With significant capital at risk, ambiguity becomes a weapon.

Strategic Considerations for Financial Professionals

Financial professionals face a type of investment dispute resolution that general business articles often miss. The dispute is rarely confined to one lawsuit or one arbitration. It may involve compensation, restrictive covenants, promissory notes, client communication issues, internal reviews, U5 language, and regulator attention all at once.

That's why a narrow “win the case” mindset is often inadequate.

The dispute is usually bigger than the pleading

In this sector, a compensation claim can affect recruiting. A Form U5 issue can affect future employment. An internal review can trigger document demands that later shape arbitration strategy. The practical problem isn't just whether the claimant can prove a breach. It's whether the record created during the dispute will damage licenses, reputation, or future earning capacity.

That broader lens matters. Commentary on access to justice in investment dispute settlement notes that for financial professionals, dispute resolution often involves parallel risks like regulatory scrutiny and reputational harm, not just the merits of the claim, in this discussion from the Wolters Kluwer Arbitration Blog. For advisors and firms, that's not a side issue. It's often the main issue.

Five pressure points worth managing early

- Document discipline: Preserve texts, emails, CRM entries, compensation records, and policy acknowledgments before narratives shift.

- Disclosure strategy: Don't treat U5 language or internal findings as an afterthought. Those records can outlast the arbitration itself.

- Forum alignment: A promissory note defense, team transition dispute, or compensation claim may require a different approach than a customer case.

- Settlement timing: Early settlement can be smart, but only after the documents, disclosure effects, and downstream regulatory consequences are understood.

- Witness selection: In financial cases, testimony from supervisors, recruiters, compliance personnel, and damages experts can outweigh broad rhetorical themes.

A business solution may outperform a legal win

Sometimes the best result is not a fully litigated award. It may be corrected language, a structured payout, neutral separation terms, or a resolution that allows both sides to move on without escalating to a regulatory event.

That's particularly true for advisors with portable books and firms trying to control client attrition. Public conflict can undermine the economics for everyone involved. Even marketing and client communication become relevant during these disputes. For firms thinking through how public-facing messaging affects trust during sensitive events, this guide for financial services marketers offers useful perspective on how financial audiences interpret communications.

Counsel has to understand both the case and the industry

A generic litigator may understand motion practice but miss the industry-specific risks. A pure employment lawyer may miss the effect of regulatory records. A lawyer handling these matters needs to account for the overlapping systems at work. FINRA procedure, employment terms, compensation structures, internal investigations, and public-facing consequences.

One option for those issues is Kons Law, which represents investors and financial professionals in securities arbitration, business disputes, and related regulatory matters. The important point is less the name of the firm than the type of counsel required. You want counsel who understands that these disputes often begin as private business conflicts and evolve into licensing, disclosure, and reputation problems if mishandled.

Conclusion Your Next Steps

Investment dispute resolution is a strategic business decision long before it becomes a legal filing. The right answer depends on the contract, the forum, the remedy, the quality of the records, and the broader business risks tied to the dispute.

Some matters belong in court because immediate relief is the priority. Others belong in arbitration because privacy, expertise, and enforceability matter more. For financial professionals, the analysis is even more layered because compensation disputes, U5 issues, internal reviews, and regulator attention can all move together.

There's also a broader shift worth taking seriously. ICSID has highlighted a visible move toward investment mediation and early conflict management in its discussion of best practices in investment dispute management. That reflects a more useful question for many businesses and investors. Not whether a claim can be filed, but rather which process protects value, controls risk, and preserves relationships where possible.

The practical lesson is straightforward. Don't wait until the filing deadline or the emergency hearing to think about forum, notice, evidence, and business impact. Review dispute clauses before signing. Preserve records at the first sign of conflict. And when a dispute surfaces, build a strategy around the end result you want, not just the accusation that triggered the fight.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.