You’ve won your case in court—a huge relief. But that piece of paper, the court order, isn't a check. It’s the starting line for the real race: turning that legal victory into actual money in your bank account. This is where learning how to collect on a judgment becomes absolutely critical.

Your First Moves After Winning a Judgment

It's tempting to relax after the judge's gavel falls, but that's a mistake I see far too often. The trial was just the first phase. The post-judgment process is where you actually recover your money, and it requires immediate, strategic action. You have some powerful legal tools available, but you have to use them correctly to avoid missteps that could derail your entire collection effort.

The Power of Docketing Your Judgment

Your very first move, before anything else, should be to "docket" the judgment. This is a formal step where you file the judgment with the court clerk, officially putting it on the public record.

Why is this so crucial? In most states, including Connecticut, a docketed judgment automatically creates a judgment lien on any real estate the debtor owns in that county—and even on property they might acquire later.

Think of it as putting a legal "boot" on their property. The debtor can't sell or refinance their home or land without paying you first. This simple, low-cost action immediately secures your claim and gives you incredible leverage. Often, it's the thing that finally forces a reluctant debtor to pay up.

Beginning the Asset Discovery Process

You can't seize what you can't find. So, at the same time you're docketing the judgment, you need to start hunting for the debtor's assets. This doesn't mean you need to immediately hire a private investigator or spend a fortune on legal fees. The initial intelligence-gathering phase can start with some simple, informal methods.

A few starting points I always recommend:

- Public Records Search: Dig into county land records, business filings with the Secretary of State, and other public documents. You'd be surprised what you can uncover.

- Online Investigation: A careful look at social media profiles (like LinkedIn for employment info) or a simple Google search can reveal business ventures, valuable personal property, or other financial clues.

- Informal Inquiries: If it's legally and ethically appropriate in your situation, sometimes just talking to mutual contacts can provide a breadcrumb trail.

This groundwork is what sets you up for successful formal collection actions down the road. It helps you identify the best targets so you're not just throwing money away on fruitless enforcement attempts.

Before diving into the nitty-gritty, it's helpful to have a clear checklist of what needs to happen the moment you have that judgment in hand. Speed is your ally here.

Immediate Post-Judgment Action Plan

| Action Item | Purpose | Critical Timing |

|---|---|---|

| Obtain Certified Copies | You'll need official copies of the judgment to file with various agencies. | Immediately |

| Docket the Judgment | Creates a lien on the debtor's real property in the county. | Within 24-48 hours |

| Send a Demand Letter | Formally notifies the debtor of the judgment and demands payment. | Within the first week |

| Begin Asset Search | Start informal investigations to identify bank accounts, employment, etc. | Concurrently |

| Prepare for Formal Discovery | Get ready to serve post-judgment interrogatories or schedule a debtor's exam. | Plan within first 30 days |

This plan keeps the momentum going and prevents the debtor from having time to hide assets.

"A judgment, standing alone, is not self-executing. The litigant must act affirmatively—armed with both legal tools and strategic intent—to pursue the fruits of litigation. This is where a paper victory becomes a real recovery."

The debt collection field is more competitive than ever. Before the pandemic, debt collection lawsuits had already hit a staggering 4.7 million cases filed in a single year in the U.S. Now, with consumer debt at record highs, that number is climbing again.

This just highlights how important it is to be proactive. As a new judgment creditor, acting quickly and decisively is your best advantage. Understanding your rights and the tools you can use is the first step toward a real recovery.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Finding a Debtor's Hidden Assets

Winning a judgment is a great first step, but it's just a piece of paper. The court confirms you're owed money, but it won't hand you a map to the debtor's assets. You simply can't collect on what you can't find.

This is where the real work begins. The asset discovery phase is the most critical part of any collection strategy—it's the intelligence-gathering mission where you figure out exactly where to send the marshal.

The smart approach is to start with simple, low-cost methods and only escalate to formal legal tools when necessary. A little investigative work upfront can save you a ton of time and money later, preventing you from wasting resources trying to garnish empty bank accounts or seize assets that don't even exist. It’s all about being methodical.

Starting with Informal Investigation

Before you spend a dime on court filings, you can uncover a surprising amount of information on your own. This initial legwork often lays the groundwork for more powerful collection actions. I always start here—it’s cost-effective and often yields huge returns.

A few powerful starting points include:

- Public Records: Jump online and search the county land records. Does the debtor own any real estate? Check the Secretary of State’s website for business filings—you might uncover an ownership stake in an LLC or corporation.

- Strategic Online Searches: A person's digital footprint can be incredibly revealing. LinkedIn is a goldmine for identifying current and past employers, which is exactly what you need for a wage garnishment. A quick scroll through other social media might even reveal valuable personal property, like a new boat or an expensive car, that could be targeted for seizure.

- Skip-Tracing Services: For a relatively small fee, professional skip-tracing services can access databases the public can't. They can quickly find current addresses, phone numbers, and sometimes even known associates or potential employers.

This preliminary work helps you build a financial profile of the debtor. It gives you the clues you need to decide which formal legal tools will pack the most punch.

The Power of a Debtor's Examination

When your own digging hits a wall, your most powerful tool is the Debtor's Examination. In some places, it’s called a post-judgment deposition. This is a formal, court-sanctioned proceeding where you get to put the debtor under oath and force them to answer detailed questions about their finances. You can subpoena them to appear in court and, more importantly, to bring specific documents with them.

The key to a successful examination is all in the questions you ask. Asking, "Where do you bank?" is a rookie mistake. The debtor will likely just name a checking account with a few bucks in it. You have to be more strategic to uncover the full picture.

Forget generic questions. Instead, demand the debtor produce their most recent federal and state tax returns, the last six months of pay stubs, and all bank statements for the past year. These documents don't lie. They provide a roadmap to every source of income, every bank and investment account, and any significant assets they own.

This process lets you systematically map out a debtor’s entire financial life, including:

- The names and locations of all their banks.

- Details of their employment, including their salary and pay schedule.

- Information on any real estate, vehicles, or valuable personal property they own.

- Any interests in businesses, partnerships, or trusts.

Using Information Subpoenas Effectively

Sometimes, a full-blown debtor's examination is overkill, or maybe you want to gather intel without tipping off the debtor. This is where an information subpoena comes in handy. It’s a set of written questions sent directly to a third party you believe is holding the debtor's assets or information.

For instance, if you have a hunch the debtor banks at a specific institution, you can serve an information subpoena directly on that bank. The bank is then legally required to respond under oath, confirming whether the debtor has an account and revealing the balance. You can do the same thing with an employer to verify wages.

It's a highly efficient way to get precise financial data before you pull the trigger on a levy or garnishment. By combining these discovery methods, you can turn your judgment from a simple piece of paper into a powerful tool for recovery.

Using Legal Tools To Enforce Your Judgment

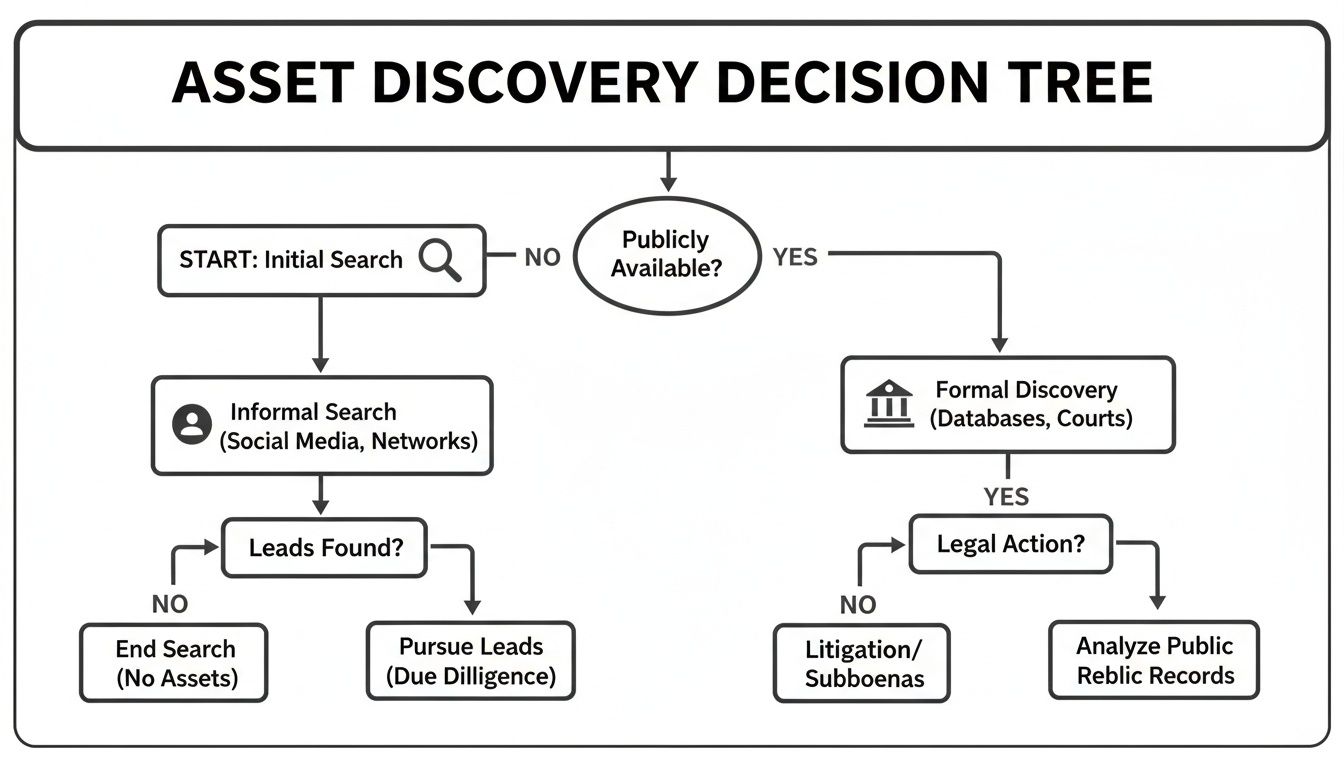

Once you've managed to locate the debtor's assets, you've hit a major milestone. Now, it's time to switch from investigator to enforcer. This is where you bring the court's authority to bear, legally seizing those assets to finally get paid what you're owed. Each legal tool serves a specific purpose, and picking the right one for the right asset is the secret to a successful collection strategy.

This decision tree gives you a bird's-eye view of the asset discovery process, which is the essential groundwork you must lay before deploying the enforcement tools we're about to cover.

As the chart shows, real success starts with a structured approach. You need to blend your own research with formal legal discovery to build a complete financial picture before you can make your move.

The Workhorse Of Collection: A Writ Of Execution

The foundational legal document for almost every enforcement action is the Writ of Execution. You can think of it as a direct command from the court to a law enforcement officer—usually a state marshal in Connecticut—giving them the authority to seize the debtor's property to satisfy your judgment.

You can't just go take a debtor's things yourself; that's a fast track to getting sued. Instead, you get this writ from the court clerk and then deliver it to the marshal along with very specific instructions, known as a levy. These instructions have to be crystal clear, identifying the debtor and the exact asset you're targeting, whether it’s a bank account, a paycheck, or a piece of equipment.

A common mistake I see creditors make is giving vague instructions. A marshal won't go on a fishing expedition for you. You have to provide precise details, like the bank's full name and branch address or the employer's official legal name, to make sure the levy actually works.

The Game-Changer: Executing A Bank Levy

One of the most powerful and immediate collection tools in your arsenal is the bank levy, sometimes called a bank garnishment. This action allows you to freeze and seize funds straight from the debtor’s bank accounts. When you give the marshal a Writ of Execution with instructions to levy a specific bank, that institution is legally required to freeze the debtor's accounts up to the amount of your judgment.

This move can be a total game-changer because it often happens with zero warning to the debtor. The first they might know about it is when their debit card gets declined. That sudden financial shock is often enough to bring a previously unresponsive debtor to the negotiating table almost overnight.

A successful bank levy does more than just capture funds; it sends a powerful message that you are serious about collecting and have the legal firepower to do it. It shifts the balance of power decisively back to you.

Tapping Into Income With Wage Garnishment

If your debtor has a steady job, a wage garnishment is another incredibly effective tool. This is a court order served directly on the debtor's employer, compelling them to withhold a portion of the debtor's earnings each pay period and send that money directly to you.

The process itself is straightforward, but it demands precision. You have to correctly identify and serve the employer's payroll department or its registered agent for service. Once they're served, the employer is legally obligated to comply. It's important to remember, though, that federal and state laws put strict limits on how much can be garnished to ensure the debtor still has enough income to cover basic living expenses.

Securing Your Claim With Judgment Liens On Real Estate

As we've touched on, simply docketing your judgment creates an automatic lien on any real estate the debtor owns in that county. This is a powerful, if passive, collection tool. It effectively secures your debt against the property, which means the debtor can't sell or refinance it without paying you first.

While a lien doesn't put cash in your pocket tomorrow, it offers fantastic long-term security. If the debtor ever tries to sell the property, your judgment will pop up during the title search, and the title company will demand it be paid off before the sale can close. In certain situations, you might even be able to force a sale of the property through a legal process known as foreclosure, though this is a more complex undertaking. You can learn more about the complexities of foreclosing a lien in our detailed guide.

Comparing Judgment Enforcement Remedies

With several tools available, choosing the right one depends entirely on the type of asset you've located. The table below breaks down the most common remedies to help you decide which path makes the most sense for your situation.

| Enforcement Tool | Target Asset | Best For... | Key Challenge |

|---|---|---|---|

| Bank Levy | Bank Accounts | Getting a quick, one-time payment when you know where the debtor banks. | The account may have insufficient funds or be closed. |

| Wage Garnishment | Employment Income | Securing a steady, long-term stream of payments from an employed debtor. | The debtor may change jobs, or the garnished amount per paycheck is small. |

| Property Lien | Real Estate | Long-term security; ensuring you get paid if the property is ever sold. | It's a passive tool; payment isn't immediate and may take years. |

| Writ of Execution | Physical Property | Seizing valuable non-exempt assets like vehicles, equipment, or inventory. | Locating valuable assets and the high costs of seizure and sale. |

Each method has its place in a well-rounded collection strategy. A bank levy offers speed, a wage garnishment provides consistency, and a property lien gives you security. Your attorney can help you deploy them in the most effective sequence to maximize your recovery.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Navigating Debtor Defenses and Exemptions

Just because you have a judgment doesn't mean every asset a debtor owns is fair game. Debtors have legal shields, and understanding them isn't just about following the rules—it's about being strategic.

Knowing what you can't touch from the outset saves you from wasting time and money chasing assets that are legally out of reach. It's the difference between an efficient collection and a frustrating, expensive dead end.

Both federal and state laws fiercely protect a debtor's basic rights. If you try to seize protected property or get too aggressive, you could find yourself facing court sanctions or even a lawsuit. This is where precision matters.

Understanding Exempt Property

The law carves out certain assets to ensure debtors can maintain a basic standard of living. These legally protected assets are called exemptions. While the specifics vary wildly from state to state, some categories are nearly universal.

For example, a debtor can often protect:

- A portion of their home equity: Known as the homestead exemption, this protects a certain dollar amount of value in their primary residence.

- A primary vehicle: Most states let a debtor keep at least one car up to a certain value, ensuring they have transportation.

- Retirement funds: Money in qualified accounts like 401(k)s and IRAs is almost always heavily shielded from creditors.

- Tools of the trade: A certain value of equipment or tools necessary for their job is also typically off-limits.

Before you even think about levying an asset, you have to figure out if it's exempt. Trying to seize a debtor’s protected retirement fund is a non-starter and a complete waste of legal fees.

Wage Garnishment Limits and Protections

Wage garnishment is a go-to tool, but it's also one of the most regulated. You can’t just take a debtor's entire paycheck. The federal Consumer Credit Protection Act (CCPA) puts a hard ceiling on what you can take from someone's disposable earnings.

As a general rule, you can garnish the lesser of two amounts:

- 25% of the debtor's disposable weekly earnings.

- The amount by which their earnings exceed 30 times the federal minimum wage.

And that's just the federal floor. States can, and often do, offer even greater protections. They might lower the percentage or shield more income entirely. A detailed grasp of Connecticut debt collection laws is absolutely critical to make sure any garnishment you pursue is compliant.

The Problem of Fraudulent Transfers

So, what happens when a debtor sees a judgment coming and suddenly "gifts" their boat to their brother-in-law? This is a classic move called a fraudulent transfer. The law sees right through it—it’s an illegal attempt to hide assets from a legitimate creditor.

If you can show a transfer was made to hinder, delay, or defraud you, the court can "claw back" the asset. The judge can simply void the transaction, pulling the asset back into the debtor's name so you can legally seize it.

A fraudulent transfer isn't just a clever maneuver; it's a direct attempt to evade a legal obligation. Courts have broad powers to reverse these transactions and penalize debtors who engage in them, ensuring that creditors have a fair chance at recovery.

Navigating these defenses requires a sharp legal eye. The sheer volume of disputes is telling; in a recent year, debt collection complaints in the U.S. hit 109,900, with companies responding to 97% of them. That statistic alone shows why careful, by-the-book collection is so important—one wrong move can easily trigger a formal complaint. You can find more insights on these consumer protection trends on electroiq.com.

By understanding exemptions and anticipating defenses like fraudulent transfers, you can focus your efforts on assets that are actually recoverable. It’s about building a smarter, more effective collection plan from day one.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

The Long Game: Renewing Judgments and Knowing When to Hire Help

Winning a judgment can feel like you've crossed the finish line, but in reality, the clock has just started ticking. It's a critical mistake to think your work is done. Many debtors are pros at hiding assets and playing a waiting game, hoping you'll simply forget or give up.

They know that judgments have a shelf life. If you don't stay on top of it, your hard-won legal victory could vanish into thin air. This is where mastering the long game—understanding judgment renewals and recognizing when to bring in a professional—becomes the final, crucial step in actually getting paid.

Why Judgments Expire and How to Renew Yours

A judgment isn't a permanent claim. State laws put a statute of limitations on them, usually for a period of 10 to 20 years, to keep them from hanging over a debtor's head forever. If you haven't collected the full amount before that clock runs out, your legal right to enforce the debt is gone. Poof.

This is exactly why renewing your judgment is so important. It’s a formal legal process where you file a motion with the court before the original judgment expires. This action effectively resets the timer, giving you another full term to continue your collection efforts.

The process isn't overly complicated, but it has to be done right. You'll typically need to:

- File a specific application or motion for renewal.

- Provide a sworn statement detailing the original judgment amount.

- Clearly account for any payments you've already received and all the interest that has accrued.

Forgetting to track your judgment's expiration date is one of the most painful—and avoidable—mistakes a creditor can make. To get a better handle on these timelines, you can learn more by reading about how long a judgment lasts in our detailed article. Staying proactive is the only way to ensure a debtor can't just wait you out.

When to Handle Collections Yourself vs. Hiring a Professional

Should you hire a collection attorney or go it alone? The answer often boils down to a simple cost-benefit analysis. If you've got a straightforward case—say, you’ve already found the debtor's bank account or know where they work—you might be able to handle the paperwork yourself.

But the moment things get complicated, the value of professional help becomes incredibly clear.

A collection attorney does more than just file paperwork. They navigate complex legal landscapes, overcome sophisticated debtor tactics, and apply relentless, strategic pressure that an individual creditor often cannot sustain.

It’s probably time to call in an expert when you’re facing scenarios like these:

- Hidden or Complex Assets: The debtor is self-employed, runs multiple LLCs, or has assets cleverly tied up in trusts.

- Fraudulent Transfers: You have a gut feeling the debtor has illegally shifted assets to friends or family just to dodge you.

- Debtor is Out of State: Chasing down a debt across state lines requires a whole different legal process called domestication.

- Bankruptcy Filings: The second a debtor files for bankruptcy, all collection efforts must stop. You need a lawyer who knows bankruptcy court to have any chance.

An experienced attorney has the tools to run deep asset searches, conduct aggressive debtor's examinations, and even unwind fraudulent transfers. They live and breathe the procedural details that can make or break a collection case.

If your efforts have stalled or the case seems even a little bit tricky, bringing in an expert is a smart investment in getting your money back.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Frequently Asked Questions About Collecting on a Judgment

Once you have a judgment in hand, the real work often begins. It's totally normal to have a ton of questions about what comes next. The legal procedures, tight deadlines, and strategic moves can feel like a maze. Here are some straightforward answers to the questions I hear most often from clients trying to figure out how to collect on a judgment.

What If I Can't Find Any Assets?

This is easily one of the most common and frustrating roadblocks. You've won in court, but it feels like you're chasing a ghost. Don't throw in the towel if your first few searches come up empty.

It’s entirely possible the debtor is a pro at hiding their money, or maybe their financial picture has simply changed since your dispute began. This is exactly when you need to bring out the bigger legal tools. A debtor's examination, for instance, forces them to sit down under oath and answer detailed questions about their finances.

An experienced collection attorney also has access to powerful investigative databases that aren't available to the public. These tools can often uncover bank accounts, property, or income streams the debtor thought were well-hidden.

How Much Does It Cost to Collect a Judgment?

The cost really depends on how hard the debtor fights back and how complex their finances are. Some steps, like docketing your judgment to create a lien, involve minor court filing fees. But the more aggressive actions will have associated costs.

You should probably budget for a few things:

- Marshal/Sheriff Fees: You have to pay the professionals to serve legal papers and execute things like bank levies or wage garnishments. These fees usually fall in the $50 to $200 range for each attempt.

- Court Filing Fees: If you need to renew your judgment down the road or file motions to compel the debtor to cooperate, expect to pay more court costs.

- Attorney Fees: If you bring in a lawyer, their fee structure can vary. Some work on an hourly basis, while others might offer a flat fee for specific actions. A common arrangement is a contingency fee, where the attorney takes a percentage of whatever they successfully recover for you—often between 25% and 40%.

The good news? Many of these expenses can be legally added to the judgment amount. These are called "post-judgment costs," which means the debtor is ultimately responsible for reimbursing you for the money you spend to collect.

Can a Debtor Just Refuse to Pay?

Sure, a debtor can refuse to write you a check. But they can't refuse the legal consequences. That judgment is your official authority to take action, with or without their cooperation.

Their refusal won't stop you from garnishing their paycheck, levying their bank account, or slapping a lien on their house. If a debtor actively ignores a court order—like skipping a scheduled debtor's examination—you can go back to the judge and ask for a contempt of court order. That can lead to fines or even jail time, which is usually a pretty powerful motivator.

What Happens If the Debtor Moves Out of State?

This is a classic move, but it's not a get-out-of-jail-free card. When a debtor skips town, you can’t just enforce your Connecticut judgment in their new home state. You first have to "domesticate" it.

This process involves registering your judgment with the court system in the debtor's new state. Once it's domesticated, it becomes a fully enforceable order in that new jurisdiction. From there, you can use all the collection tools allowed under that state's laws to go after their assets. It adds an extra legal step, which is why this is a perfect time to have an attorney who knows the ins and outs of interstate collections.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.