A lot of people first encounter the Series 79 license at a career pressure point. They've moved beyond pure spreadsheet support, they're sitting in diligence calls, marking up drafts, helping with offering materials, and someone at the firm says, “You need to get registered.” That moment matters more than most candidates realize.

For junior bankers, associates moving into execution-heavy roles, and professionals entering a broker-dealer platform from corporate finance or private capital, the Series 79 isn't just another exam. It's the gate that lets you lawfully operate inside a defined investment banking lane. Without it, your title may suggest deal work, but your regulatory footing may not.

That distinction becomes even more important when teams expand beyond traditional banks. Plenty of professionals now move between boutiques, placement platforms, independent advisory structures, and firms trying to connect with fintech investors while building transaction pipelines. The commercial opportunity may look modern and flexible. The registration rules are not.

From a securities law perspective, the biggest mistake I see is treating the Series 79 as a test-prep problem only. Passing matters. But so do sponsorship, job scope, the line between advisory activity and securities sales activity, and what happens when you leave a firm under stress. Those issues can affect your ability to stay employed, move platforms, or defend your record later.

An Introduction to the Investment Banker's Gateway

A junior banker can spend months inside live transactions before anyone asks the question that controls what they are allowed to do. The analyst is on diligence calls, commenting on drafts, helping build valuation materials, and coordinating with counsel. Then the firm expects direct execution support, and registration stops being an HR item.

That is the point where the Series 79 license starts to matter in a practical way. It is the registration tied to a defined investment banking function inside a broker-dealer. For the professional, it affects staffing, compensation path, and mobility. For the firm, it affects supervision, permitted activity, and exposure if someone is doing regulated work without the proper license.

I tell clients to treat Series 79 as part of the full employment lifecycle, not just an exam target. Key issues often appear before the test is scheduled and after the employee leaves. Sponsorship has to align with the actual role. Day-to-day duties have to stay inside the registered scope. If the relationship ends badly, Form U5 language can follow the individual long after the seat is gone.

That risk is easy to miss in newer deal environments. A boutique may combine advisory work, capital raising, and business development under one title. A growth-stage platform trying to connect with fintech investors may move quickly from introductions to activities that look much more like regulated transaction work. The business model may be modern. The securities rules are still formal and unforgiving.

Why this credential changes your career lane

Series 79 places a professional in the investment banking representative category. That sounds straightforward, but the legal significance is narrower than many candidates expect. The license is tied to specific transaction-based functions, not general securities activity, and that line matters once a deal is live and regulators or firm counsel review who did what.

In practice, the registration question often turns on details. Did the employee merely support analysis, or did the employee participate in solicitation, structuring discussions, offering materials, or execution steps that required registration? Those distinctions are rarely academic during an internal review or a termination dispute.

A banker can understand the deal cold and still create a registration problem.

Where professionals usually get tripped up

The first problem is role drift. Titles such as “strategic finance,” “private capital,” or “corporate development adviser” often conceal work that edges into broker-dealer activity. A person may start with research and process support, then move into activities closer to live execution without a clean compliance review. That is a common setup for avoidable trouble.

The second problem is documentation. Firms do not always describe the role with enough precision at onboarding, and employees often assume the license analysis will be handled elsewhere. It should not be left that loose, especially if the person will touch offering documents, buyer outreach, or an M&A process shaped by a formal due diligence checklist for mergers and acquisitions.

The third problem comes at departure. Professionals often assume a strong deal record speaks for itself. It does not if a U5 disclosure suggests compliance concerns, unauthorized activity, or supervision issues. At that stage, the licensing question is no longer theoretical. It can affect the next offer, the next registration, and whether counsel needs to get involved quickly.

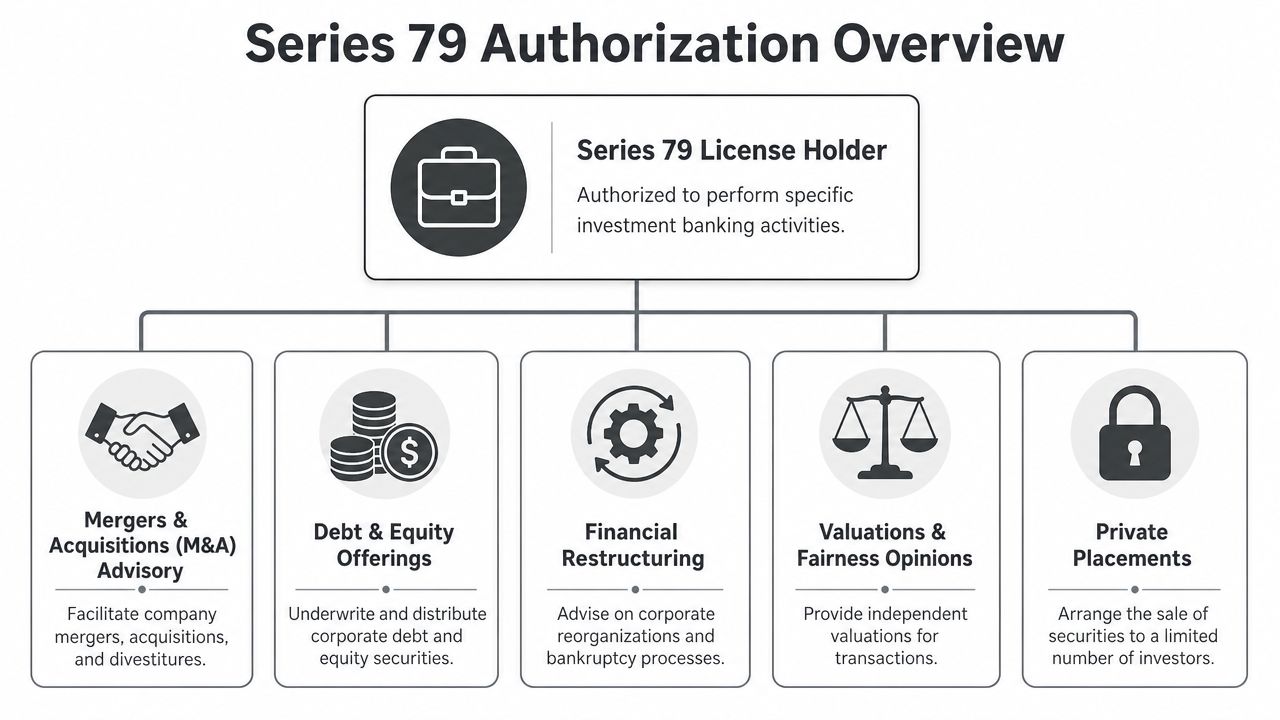

What the Series 79 License Authorizes

A banker joins a live sell-side process, helps shape the management presentation, comments on valuation, coordinates diligence calls, and speaks with potential buyers under supervision. In that setting, the Series 79 usually fits the job. If that same banker starts soliciting investors or functioning like a general securities salesperson, the analysis changes fast.

The Series 79 is the investment banking registration for transaction work inside a broker-dealer. It covers professionals involved in advising on and executing debt and equity offerings, mergers and acquisitions, tender offers, restructurings, and related corporate finance assignments. The point is narrower than many candidates assume. This license is tied to investment banking activity, not broad retail or institutional securities sales.

The core lane of authorized work

In practice, Series 79 work often includes:

M&A advisory: Supporting buy-side, sell-side, merger, and divestiture transactions.

Debt and equity offerings: Working on capital raises and underwriting-related execution.

Restructuring matters: Participating in distressed or strategic recapitalization transactions.

Tender offers: Assisting with regulated transaction processes involving acquisition offers.

Valuation-driven execution support: Contributing to diligence, analysis, and transaction materials.

That description matters because firms often title people broadly while assigning them very specific functions. Analysts, associates, vice presidents, and principals who spend their time on execution generally fall within the intended scope. Drafting materials, coordinating diligence, building valuation support, organizing data rooms, and helping manage a deal process are all consistent with the license when done through a registered firm and under proper supervision.

Borderline tasks require more care. Fairness opinion support, private placement work, and investor-facing communications can sit inside the Series 79 function or outside it depending on what the person does. The legal risk usually turns on details: who made the contact, what was said, whether compensation is tied to sales activity, and whether the firm documented the role correctly.

Where the line gets crossed

The Series 79 does not authorize every securities-related activity. It does not turn an investment banker into a general registered representative for all purposes.

The recurring problem is solicitation. A professional may describe the role as “helping with introductions” or “supporting the raise,” but regulators and employer counsel will examine conduct, not labels. If the person is actively marketing securities to investors, discussing terms in a way that looks like selling, or functioning outside the investment banking lane, another registration may be required. That issue becomes especially sensitive in private placements, growth capital raises, and hybrid roles that blend advisory work with capital formation.

I have seen this become a dispute after the employment relationship has already soured. At that point, the question is no longer academic. It can affect internal discipline, the language used on a Form U5, and the professional's ability to move to the next platform without baggage.

For transaction teams, process discipline helps define the boundary. Operational resources on mastering M&A due diligence can improve execution, and legal review should run alongside that work when personnel are participating in buyer or investor communications. A well-built M&A due diligence checklist for mergers and acquisitions also helps firms assign tasks cleanly so registered activity does not drift into something else.

Practical takeaway

The Series 79 authorizes specialized investment banking work. It supports deal execution, issuer-side advisory functions, and transaction analysis inside a broker-dealer. It does not, standing alone, solve every registration question created by capital raising activity, investor contact, compensation design, or a messy departure from the firm. Those are the points where compliance input, and sometimes counsel, should come in before the record gets harder to fix.

Deconstructing the Series 79 Exam Structure

A candidate gets 30 minutes into the Series 79 and realizes the problem is not memorization. The exam is testing whether the person can read a transaction fact pattern the way a junior banker would read a live assignment, under time pressure, with enough judgment to separate relevant details from noise.

That is why weak prep often comes from the wrong model of the test. Candidates who treat it like a broad securities licensing exam usually waste time on material outside the investment banking function. Candidates who treat it like a pure banking technical interview also miss the regulatory framing built into the questions. The exam sits between those two approaches. It tests applied investment banking work inside a regulated broker-dealer role.

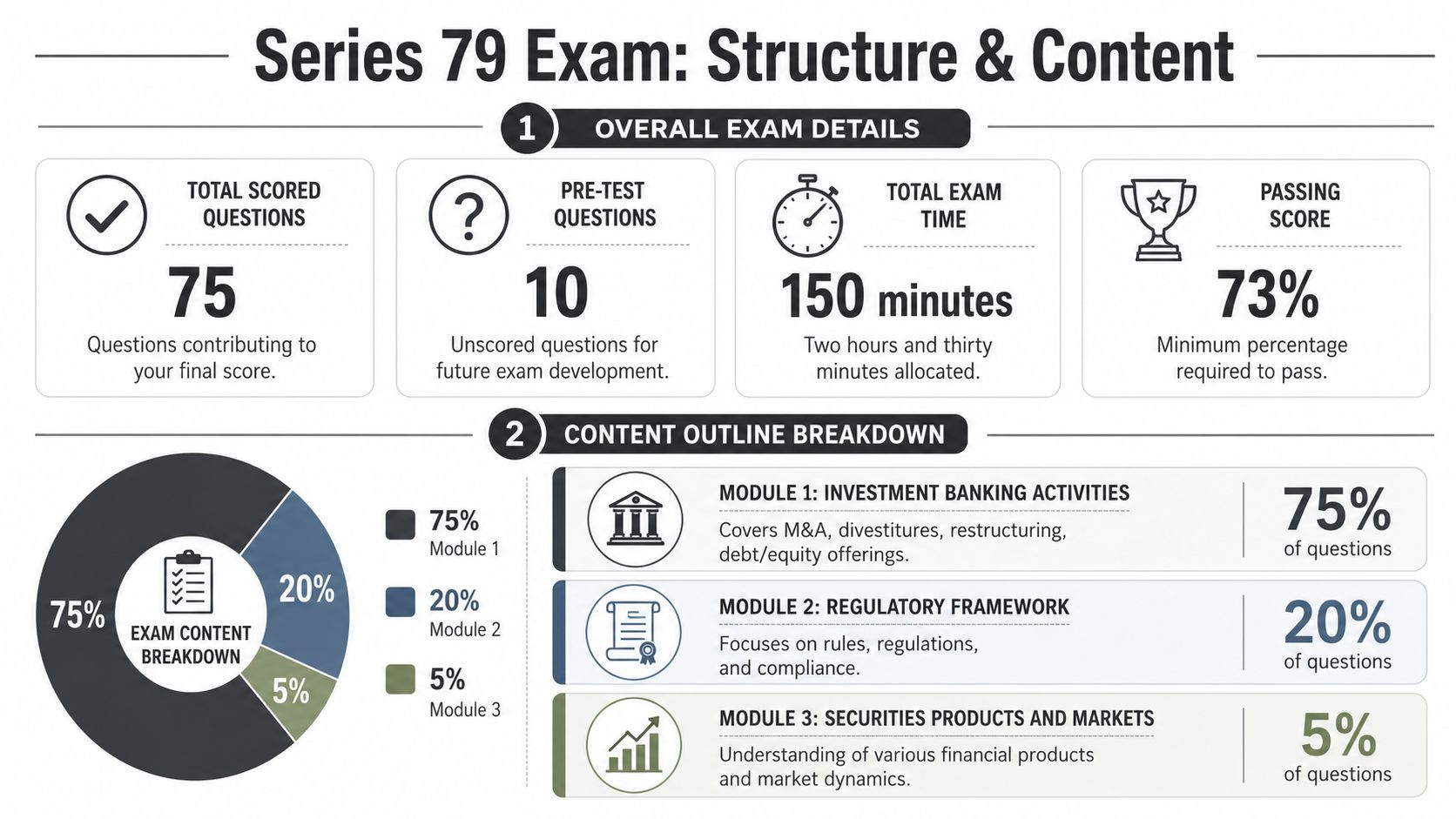

The current format is a 75-question exam with a 2 hour 30 minute testing window, and secondary prep sources note that candidates often spend about 60 to 100 study hours preparing, according to Wall Street Prep's Series 79 exam overview.

How FINRA weights the content

The exam is organized around three working categories:

- Collection, analysis, and evaluation of data: about 49%

- Underwriting, new financing transactions, types of offerings, and securities registration: about 27%

- M&A, tender offers, and restructurings: 24%

That weighting matters because it shows what FINRA expects from an entry-level investment banking representative. Nearly half the exam is concentrated in analytical work. A candidate who can recite isolated rules but cannot read financial information, transaction materials, or diligence facts in context is likely to struggle.

What the weighting means in practice

The largest category reflects the nature of the job. Investment banking work starts with gathering information, testing assumptions, and evaluating how documents and data affect the transaction. The exam mirrors that workflow. Questions often reward candidates who can identify the issue hidden inside a longer fact pattern rather than candidates who merely remember a definition.

The financing category tests whether the candidate understands how offerings are structured and documented within the banker's role. That includes process, sequence, and the practical purpose of the documents involved. In practice, I see candidates lose points by studying terms in isolation instead of understanding how a financing moves from planning to execution.

The strategic transaction category covers M&A, tender offers, and restructurings. Those questions usually turn on role clarity. Who is acting for whom, what stage the deal is in, what the representative is permitted to do, and which transaction features change the analysis. That is also the part of the exam that best signals later compliance risk. Professionals who are fuzzy on transaction boundaries during the licensing stage are often the same ones who run into internal scrutiny later when their actual duties expand or shift.

A study priority framework

If I were advising a candidate, I would set priorities in this order:

- Master the analytical core first. Spend the most time on financial materials, transaction summaries, and document-driven questions.

- Build process knowledge for offerings. Learn how underwriting and financing transactions are structured from start to finish.

- Drill strategic transaction fact patterns. Focus on M&A, tender offers, and restructurings until the sequence and participant roles are familiar.

This order tracks the exam's weighting, but it also tracks professional risk. A person who studies the job as it is performed usually retains the material better and makes fewer mistakes after registration.

One caution about prep materials

Question banks are useful for pacing and pattern recognition. They are less useful when a candidate has no working grasp of how an engagement unfolds, what each document is doing, or where the registered representative's role begins and ends.

That distinction matters beyond exam day. The Series 79 is part of a regulated career record, not just a testing milestone. If a firm later questions whether a banker handled assigned functions appropriately, weak understanding of role boundaries can become a supervision issue, a disciplinary issue, or language on a Form U5. Candidates should prepare with that larger professional context in mind.

A Practical Plan for Passing the Exam

A common mistake shows up before the first practice question. A banker accepts a role, gets staffed on live transactions, and assumes the licensing piece will sort itself out. Then the start date moves, sponsorship takes longer than expected, or the actual job includes activities the person is not yet permitted to handle. That is how an exam issue turns into an employment and compliance issue.

Start with the practical gatekeeping issues

Before building a study plan, confirm two things with the firm. First, confirm that the firm will sponsor the registration tied to the work you are expected to perform. Second, confirm what you may do before the license is in place.

Titles are not enough. I have seen professionals hired into "investment banking" roles where the business expected broader activity than the registration covered, or expected participation in functions that should wait until licensing is complete. Those mismatches create avoidable risk for both the employee and the firm.

This matters even more in hybrid roles. If your work could drift toward investor contact, selling activity, or side business activity, get clear guidance early. Questions around outside activity and transaction-based compensation can overlap with private securities transactions compliance issues long before anyone is thinking about a Form U5.

Build a study plan that survives a live deal schedule

The candidates who pass are usually not using exotic methods. They use a calendar, protect study time, and adjust quickly when they identify weak spots.

A workable plan usually includes:

- A fixed weekly schedule: Put study blocks on the calendar like client calls. If study time is "whenever work slows down," it usually disappears.

- Topic sequencing based on job exposure: Candidates with strong modeling skills often still need more repetition on rules, documentation, and offering process mechanics.

- Timed practice: Pace matters. Candidates who know the material can still underperform if they rush fact patterns or spend too long on a narrow question.

- Error tracking: Separate content gaps from reading mistakes. Those are different problems and should be corrected differently.

One sentence of practical advice: study on the schedule you can maintain during an active deal cycle, not the schedule you wish you had.

What tends to work

Use question banks to diagnose weaknesses, not to chase a score. If you miss a question, identify whether the problem was terminology, transaction sequence, document purpose, or confusion about who does what in the deal.

Condensed outlines are useful if they lead to active recall. Passive rereading usually gives candidates false confidence. Full-length practice sessions also matter because they expose concentration problems that do not appear in shorter drills.

What wastes time

Some habits look productive and are not.

- Memorizing isolated definitions: The exam tests application in context.

- Assuming live deal work is enough: Experience helps, but it rarely covers the full tested range.

- Waiting for a calmer month at the office: Banking rarely offers one on command.

A lawyer's practical advice

Treat the exam as one part of a larger regulated career record. The passing score matters, but so do the circumstances around your registration, your assigned duties, and the communications that document both. If your responsibilities expand while you are studying, do not improvise. Confirm with compliance and your supervisor what activities are permitted and what must wait.

That advice has a career reason, not just an exam reason. Problems that begin as informal role creep can later be framed as supervision failures, licensing violations, or questions about judgment. Those issues do not disappear after you pass. In the wrong fact pattern, they follow you to termination paperwork and future registration reviews.

Series 79 vs Other Key FINRA Registrations

The licensing confusion around the Series 79 license usually comes from people asking the wrong question. They ask which exam is “better.” The useful question is which registration matches the work you're performing.

For most investment banking professionals, the true comparison is not prestige. It's scope. The Series 79 is for specialized transaction activity. The Series 7 is broader and may be required when the role includes direct securities marketing or sales activity that goes beyond the investment banking lane.

Series 79 vs Series 7 at a Glance

| Attribute | Series 79 (Investment Banking) | Series 7 (General Securities) |

|---|---|---|

| Primary function | Specialized investment banking activity tied to offerings, M&A, tender offers, and restructurings | Broader general securities activity |

| Typical role profile | Investment banking analyst, associate, M&A or capital raising professional | Registered representative engaged in broader securities sales activity |

| Regulatory focus | Deal execution and transaction-related competence | Broader securities business functions |

| Investor marketing | May not be enough by itself if the person is actively marketing offerings to investors | May be required depending on the activity |

| Relationship to SIE | SIE is required for registration | SIE is also part of the qualification path |

This is why many professionals moving into hybrid roles need careful analysis. A banker can be properly positioned for advisory work under one registration and still be under-registered for another part of the job.

The SIE is foundational, not optional

The SIE sits underneath the specialist registration structure. It doesn't replace the Series 79, and it doesn't authorize investment banking activity by itself. It's the base-level securities knowledge requirement that must be paired with the job-specific registration path.

That distinction matters for career changers who pass the SIE first and assume they're now broadly cleared for regulated activity. They are not. The SIE helps open the door. It doesn't define your lane.

Where firms and employees mismatch expectations

One recurring issue in disputes is that firms describe roles loosely while compliance obligations remain precise. A banker may be told, informally, that “everyone here does a bit of everything.” That's not a regulatory category.

Your license should match your actual conduct, not the marketing language in your job description.

Professionals considering outside business activity, private placements, or hybrid advisory models should also understand how transaction work can create risk under firm rules and FINRA scrutiny. For related issues, this discussion of private securities transactions and associated risks is often worth reviewing before a role expands beyond standard internal deal execution.

The practical takeaway

If your work is centered on advising issuers and executing transactions, the Series 79 is the natural fit. If your role includes broader securities sales functions, investor-facing solicitation, or activity outside that narrow lane, the analysis changes. At that point, the right answer may involve more than one registration, tighter supervision, or a redesign of the role itself.

Maintaining Your License and Navigating Form U5 Risks

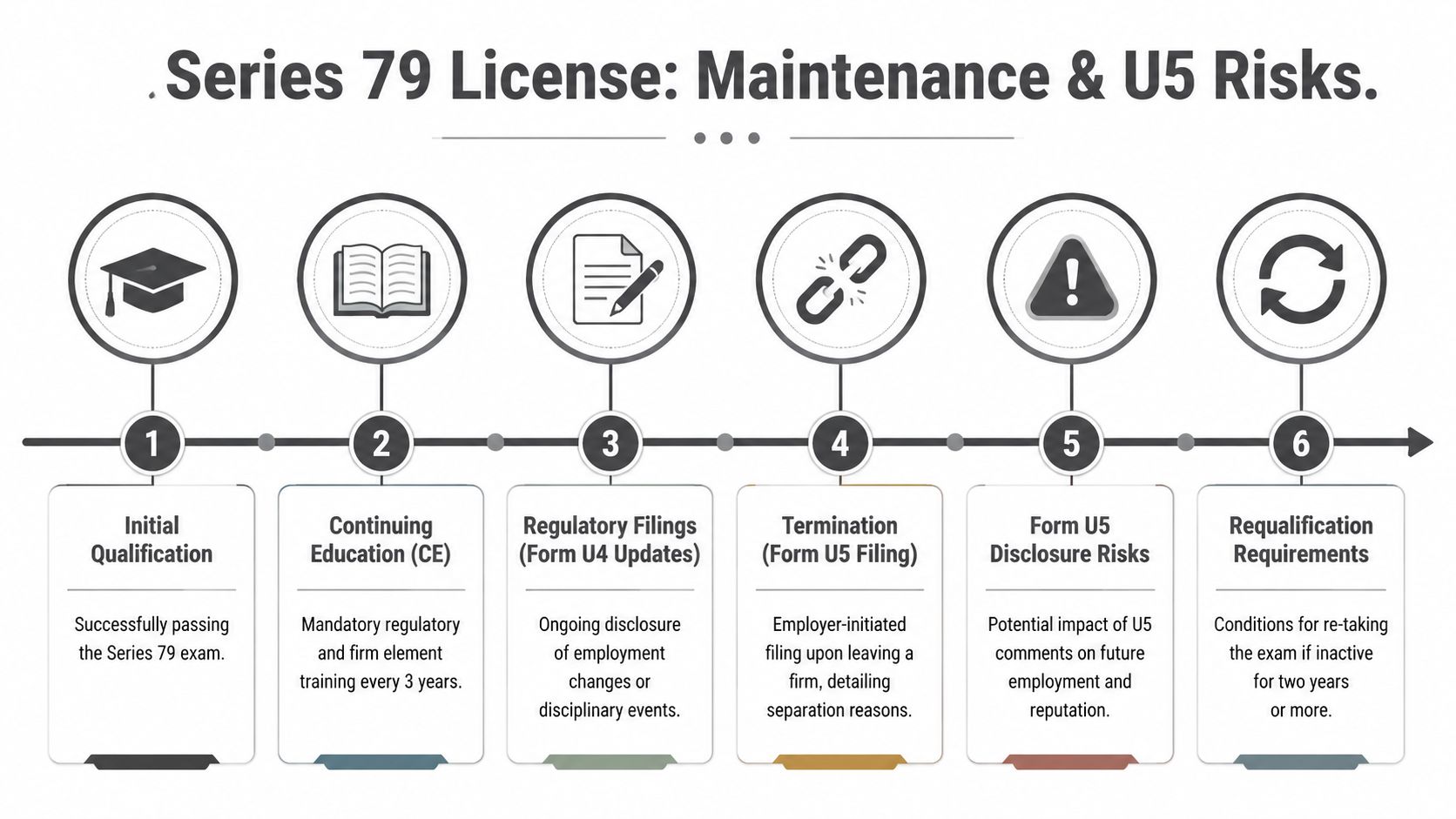

Most candidates put all their energy into passing the exam and almost none into preserving the registration. That's backwards. In practice, some of the most consequential legal problems arise after the exam, especially when a banker leaves a firm, moves into a non-member role, or exits under strained circumstances.

The critical point is simple. A Series 79 registration remains active only while the individual is employed by a FINRA-member firm or SRO, and if the person leaves and does not find qualifying employment within two years, the registration can lapse, requiring re-examination, as summarized by Kaplan in its Series 79 FAQ guidance.

Why career transitions create hidden exposure

A lot of junior and mid-level bankers assume their license is effectively “theirs” once earned. That's not how the registration works. It is maintained through an associated relationship with the right kind of firm. If you move into private equity, corporate development, consulting, family office work, or an independent structure outside a FINRA-member platform, the clock matters.

This issue becomes especially serious when the departure wasn't planned. A reduction in force, internal dispute, compensation fight, or compliance disagreement can quickly turn a manageable job change into a registration problem.

Form U5 is often the real battleground

When a registered person leaves, the firm files a Form U5. That filing can shape how future employers, regulators, and counterparties view the departure. If the language is vague, accusatory, or framed in a way that suggests misconduct, the practical fallout can be severe even before any formal proceeding begins.

In my experience, professionals often focus on severance, deferred compensation, or transition logistics while overlooking the U5 until it's already on file. That's a mistake. Once problematic language appears, fixing the damage is harder.

For professionals dealing with this issue directly, this discussion of Form U5 disputes and FINRA considerations is a useful starting point.

A U5 doesn't just close out your prior registration record. It often becomes the first document the next firm studies when deciding whether to hire you.

A practical maintenance checklist

If you hold a Series 79 and your employment status may change, focus on these points early:

- Confirm your association status: Know whether you remain linked to a FINRA-member firm at every stage of a transition.

- Review departure communications carefully: Informal emails and HR language can later shape the U5 narrative.

- Document the actual reason for separation: If the stated reason is incomplete or misleading, preserve your records.

- Coordinate before signing transition documents: A release or resignation letter can interact with later regulatory positions.

- Assess the next role's structure: Moving to an unregistered platform may be fine commercially, but it can still affect your registration timeline.

Where legal counsel often becomes necessary

Not every departure requires a lawyer. Many are routine. But once termination language becomes contentious, allegations appear, compensation is withheld, or the next employer raises concerns about the U5, the matter has already entered a higher-risk category.

That's especially true when the separation involves compliance complaints, internal investigations, or disputed communications with clients, investors, or counterparties. At that point, the registration issue is no longer administrative. It becomes reputational and legal.

When to Consult Counsel on Registration and Compliance

The most valuable legal advice in this area is often preventive. By the time a banker receives a regulatory request, sees a damaging U5 entry, or learns that a new employer is hesitating because of prior disclosures, the available options are narrower and more expensive.

You should consider consulting securities counsel when the issue stops being purely clerical and starts affecting your ability to work, move firms, or explain your record. That line arrives sooner than many professionals think.

Situations that call for prompt legal review

Some scenarios deserve immediate attention:

- You expect a difficult termination. If management tension, internal complaints, or compensation disputes are escalating, assume the exit documents matter.

- Your Form U5 may contain harmful language. Even short phrasing can trigger long-term hiring and disclosure consequences.

- A firm says your activities may have exceeded your registration. That issue can become both an employment matter and a regulatory matter.

- You've received a FINRA inquiry or document request. Early response strategy matters.

- You're moving into a gray-area role. Hybrid advisory, capital introduction, and private transaction activity need careful analysis before the move, not after.

Why waiting usually makes the problem worse

Professionals sometimes delay because they believe involving counsel looks aggressive. In securities practice, that's often the wrong instinct. Thoughtful counsel can help narrow disputes, preserve records, shape communications, and reduce the chance that a preventable issue becomes a formal allegation.

It also helps to remember that many registration disputes overlap with employment law, contract rights, deferred compensation, promissory note exposure, and internal supervisory issues. A narrow “test and license” view misses the bigger picture.

Early legal review is often less about fighting and more about preventing an avoidable filing, statement, or admission from following you for years.

One final practical point

If your concern involves customer identity procedures, supervisory expectations, or broader compliance questions connected to your role, review the applicable firm obligations carefully. Issues that start as operational questions can become disciplinary issues if the record suggests you ignored red flags. For a related compliance topic, see this discussion of FINRA Rule 2090 and know-your-customer obligations.

The Series 79 can be a valuable and necessary credential. But the exam is only one part of the story. The significant professional risk usually lies in how the registration matches your actual duties, how your firm supervises those duties, and what gets written about you when the relationship ends.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.