You may be at the point where the headline terms are settled, the buyer is serious, and everyone is focused on price. Then the structure question lands on the table. Asset purchase or stock purchase? For many Connecticut deals, that choice affects value almost as much as the number on the first page.

Business owners often assume this is a technical legal issue to be handled late in the process. It isn't. Structure affects taxes, liability exposure, employee transitions, contract assignments, and whether the closing becomes smooth or painfully slow. It also shapes the purchase agreement from the first draft forward.

For buyers, the wrong structure can mean inheriting problems they didn't expect. For sellers, the wrong structure can turn an otherwise strong deal into a tax or post-closing mess. If you're weighing a sale or acquisition, it helps to understand the practical consequences before letters of intent harden into positions. A strong starting point is getting counsel involved early in the acquisition process, especially if you're evaluating control, risk, and continuity issues with a business acquisition attorney.

The Billion-Dollar Question for Your Business Sale

The first real question in many deals isn't what the business is worth. It's what, exactly, is changing hands.

If you sell stock, the buyer steps into ownership of the existing company. The entity remains in place. That can preserve continuity, but it also means the buyer is purchasing the company with its history attached. If you sell assets, the buyer picks up identified business assets and only the liabilities the buyer agrees to assume. The seller's entity remains behind.

That difference sounds simple. In practice, it drives nearly every important negotiation point.

Why this decision changes the whole transaction

A buyer looking at a manufacturing company in Connecticut may care most about equipment, inventory, customer relationships, and a clean liability profile. That buyer often leans toward an asset deal because it allows selectivity.

A seller who has spent years building a company with stable contracts, trained employees, and a recognizable operating platform may push for a stock deal because it usually offers cleaner continuity and can be easier to execute.

Practical rule: If you treat structure as a drafting detail instead of a business decision, you usually give up leverage too early.

Business owners get tripped up. They negotiate price first, then try to solve structure after expectations are already fixed. That approach rarely works well. Structure should be discussed alongside price, working capital, indemnification, and transition obligations.

Connecticut context matters

National articles often stop at general tax and liability principles. Connecticut deals usually require a more local lens. Real estate transfer issues, state-level licensing, contract assignment problems, and industry-specific approvals can push a transaction toward one format or the other. That's especially true for professional practices, closely held service businesses, and owner-operated companies with key employees concentrated in one market.

A good structure doesn't just look efficient on paper. It has to close cleanly under the facts of the business you own or plan to buy.

What Are You Actually Buying A High-Level Comparison

Before getting into tax and risk, it helps to anchor the basic difference. A stock purchase transfers ownership of the company itself. An asset purchase transfers selected property and business rights out of that company.

Here is the simplest side-by-side view.

| Issue | Stock Purchase | Asset Purchase |

|---|---|---|

| What changes hands | Shares or membership interests in the target entity | Specific assets identified in the purchase agreement |

| Legal entity after closing | Same entity continues with new ownership | Seller entity remains; buyer takes transferred assets |

| Liabilities | Buyer typically takes the entity with its liabilities inside it | Buyer usually assumes only listed liabilities |

| Contracts and permits | Often stay with the existing entity, subject to deal documents and change-of-control issues | Often require separate assignment, transfer, or consent |

| Employees and benefits | Usually more continuity | Often require new hiring and transition planning |

| Documentation burden | Often more streamlined at transfer level | Often heavier because each asset category may need separate conveyance documents |

Stock purchase means you buy the box

In a stock deal, the company keeps owning what it owned before closing. The buyer acquires the equity. From an operational standpoint, that can be attractive because the target's business stays in the same legal shell.

That simplicity is one reason many sellers prefer it. There's often less retitling of assets and fewer separate transfer documents. If you want a quick conceptual summary of how asset-level transfers are documented, this overview of an asset purchase agreement is a useful companion.

Asset purchase means you pick the contents

In an asset deal, the purchase agreement becomes a map. It needs to identify what the buyer is taking, what stays behind, and which liabilities, if any, are being assumed.

That can include:

- Tangible property: Equipment, inventory, furniture, vehicles, and fixtures.

- Intangible rights: Trademarks, customer lists, software rights, goodwill, and domain-related business assets.

- Contract rights: Assigned customer contracts, leases, vendor agreements, and licenses where transfer is permitted.

- Excluded property: Cash, certain receivables, litigation claims, or legacy records the seller keeps.

Which one is simpler

At a high level, stock purchases are usually simpler to transfer, while asset purchases are usually cleaner for risk selection. Neither is automatically better. The better structure is the one that matches the business, the liability profile, and the parties' bargaining power.

Buy the entity when continuity is the priority. Buy the assets when precision is the priority.

That distinction becomes sharper once taxes enter the negotiation.

The Tax Consequences Tug of War

The tax fight often sits underneath the entire asset purchase vs stock purchase debate. Buyers and sellers usually want opposite things.

For a buyer, an asset deal is often more attractive because the acquired assets can usually be remeasured to fair market value, and most acquired goodwill can be amortized over 15 years under U.S. tax law, which can create stronger future deductions, as explained in Sage's discussion of fixed assets in M&A and the stock versus asset purchase impact. In a stock purchase, the buyer generally inherits the target's existing tax basis and depreciation schedules, so the purchase price usually doesn't create that same new tax shield.

That difference has real economic weight in larger transactions. The same operating business can produce very different post-closing tax deductions depending on structure.

Why buyers often push for asset treatment

A buyer doesn't just look at purchase price. A buyer looks at after-tax return. If the buyer can step up the basis of acquired assets and amortize goodwill, the buyer may accept a higher headline price because part of the cost may be recovered through future deductions.

That doesn't mean every buyer should insist on an asset deal. If the target's contracts, permits, or workforce structure make an asset deal hard to execute, the operational cost may outweigh the tax benefit. But as a negotiating matter, the buyer usually starts by asking what tax value can be captured.

Why sellers often resist

Sellers often prefer a stock deal because it can be taxed more like a capital gain transaction rather than triggering entity-level tax consequences for certain corporations, a point also noted in the same Sage analysis linked above. In practical terms, sellers may see an asset sale as economically worse even if the purchase price looks similar.

That's why structure negotiations often turn into price negotiations. If the buyer gets the tax benefit of an asset deal, the seller may ask to be paid for giving it up.

For owners trying to understand the seller side of that equation, this overview of the tax implications of selling a business is a helpful non-firm resource.

How this gets resolved in real deals

The tug of war usually resolves in one of three ways:

Price adjustment

The buyer pays more for a stock deal because the buyer isn't getting basis step-up.Structure compromise

The parties accept an asset deal because the liability profile supports it, but the seller negotiates harder on cash at closing or post-closing protections.Selective flexibility

The parties narrow what's being sold, adjust working capital mechanics, or reframe transition obligations to balance the tax cost.

Deal insight: The tax result doesn't live in isolation. It changes bargaining power across price, indemnity, and timing.

For Connecticut business owners, early modeling matters. If your company owns appreciated assets, has goodwill value tied to operations, or operates through an entity where tax treatment is especially sensitive, structure should be evaluated before a letter of intent is signed.

Navigating Liability and Unseen Risks

Liability is where the clean theory of a transaction meets the messy history of an operating business.

In a stock purchase, the buyer acquires the target's equity and takes on all liabilities, including unknown or contingent ones. In an asset purchase, the buyer typically acquires only the assets and liabilities it expressly agrees to assume, which makes the structure a strong tool for selective risk control, as summarized by DeWitt's overview of asset purchase versus stock purchase.

What buyers worry about in a stock deal

When you buy stock, you buy the company's past. Some liabilities are obvious. Others don't show up until after closing.

Typical areas of concern include:

- Tax exposure: Prior filings, payroll issues, sales tax problems, or unresolved audits.

- Employment claims: Wage disputes, misclassification allegations, discrimination claims, or restrictive covenant fights.

- Litigation risk: Pending lawsuits, threatened claims, and disputes that haven't matured yet.

- Operational legacy issues: Environmental conditions, customer refund patterns, product claims, or regulatory history.

In Connecticut deals, I pay close attention to state tax compliance, employment practices, and industry licensing. A target may look healthy from a revenue standpoint and still carry historic problems that become expensive only after ownership changes.

What asset deals do better

Asset purchases let buyers define the perimeter. That doesn't eliminate risk, but it changes the battlefield.

A well-drafted asset agreement should identify:

| Focus area | Buyer objective in an asset deal |

|---|---|

| Transferred assets | Describe exactly what is being acquired |

| Assumed liabilities | Limit assumption to listed obligations |

| Excluded liabilities | State what remains with seller |

| Post-closing cooperation | Require help with records, claims, and third-party notices |

This selective approach is one reason buyers often prefer asset deals when a business has operated for many years, changed ownership internally, or lacks clean records.

What still doesn't disappear

An asset deal is not a magic eraser. Buyers still need to diligence successor liability theories, fraud risks, and practical exposure tied to ongoing operations. If the buyer continues the same business with the same people, same trade name, and same customer-facing model, some risks can still follow in substance even if the documents try to leave them behind.

That's why the paper matters.

A weak indemnity package won't fix a bad structure choice, and a good structure choice won't fix poor diligence.

The contract terms that carry the load

In either structure, risk allocation usually turns on representations, warranties, disclosure schedules, indemnification terms, and post-closing access to records. In a stock deal, those protections often need to be broader because the buyer is stepping into the entire entity. In an asset deal, the drafting burden shifts toward precise definitions of excluded and assumed liabilities.

If the business has any history that makes you uneasy, don't let the seller dismiss the issue as “standard.” Liability allocation is never standard when the facts aren't.

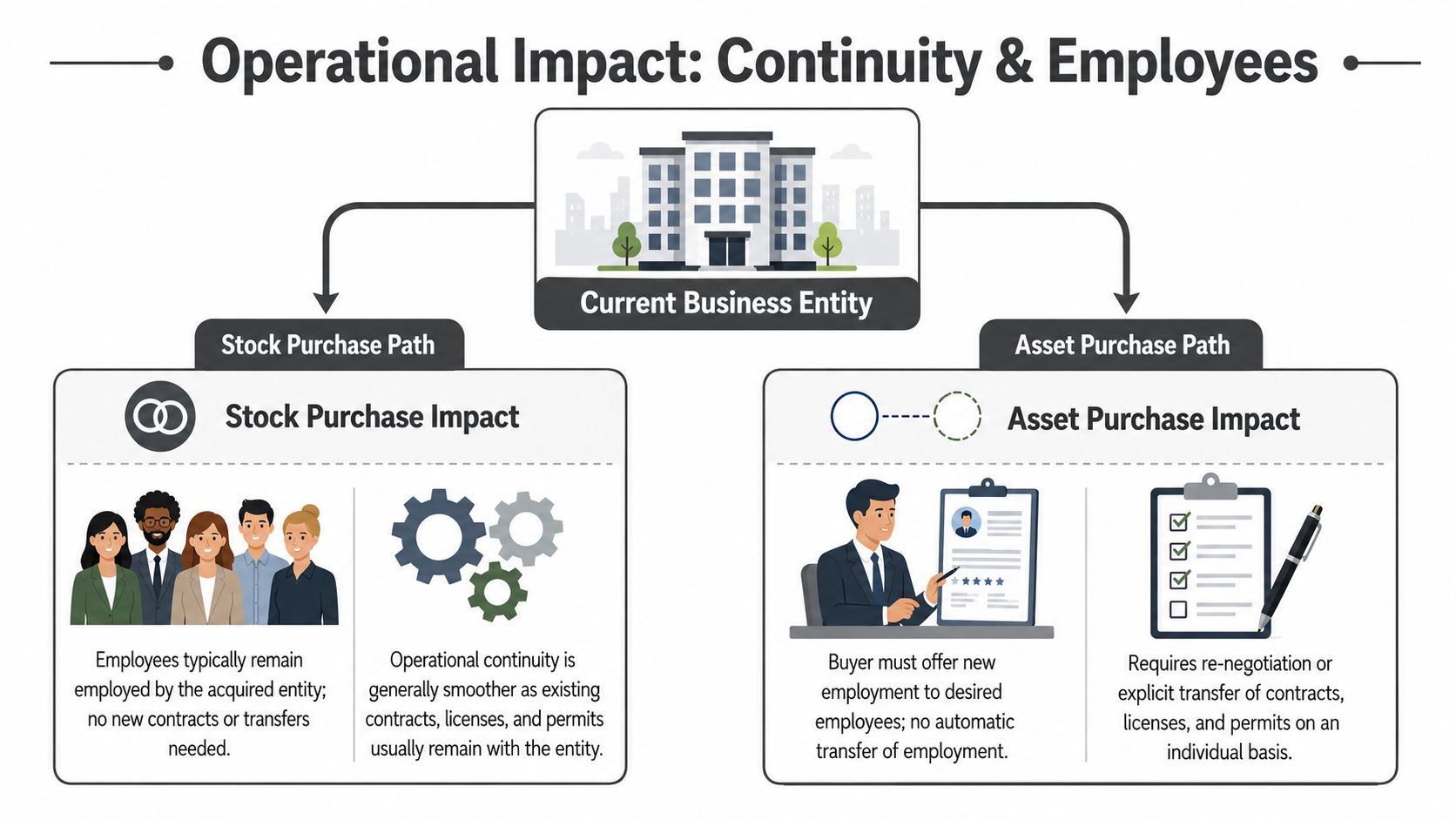

Operational Continuity and Employee Transfers

A deal can look perfect financially and still stumble because operations don't move cleanly. That happens more often than many owners expect.

Stock purchases generally preserve existing employee relationships, contracts, and benefit plans. Asset purchases often require the buyer to rebuild those systems or re-paper them one by one, creating significant execution hurdles, especially in relationship-driven service businesses, as discussed by Odyssey Advisors in its analysis of stock purchase versus asset purchase.

Why continuity often favors stock deals

When the legal entity remains in place, the business usually keeps moving through the same vessel. That matters in industries where the value of the company sits in relationships, not machinery.

A stock transaction may better preserve:

- Client-facing stability: Customers keep dealing with the same entity.

- Benefit-plan continuity: Existing plan structures may remain in place, subject to deal-specific handling.

- Contract position: Agreements already held by the entity may avoid assignment work, though change-of-control review still matters.

- Regulatory posture: Licenses and permits tied to the entity may be easier to maintain than in an asset transfer.

This is especially relevant for Connecticut advisory practices, professional service firms, and regulated businesses where personal relationships and approvals drive enterprise value.

Where asset deals create friction

In an asset purchase, the buyer may need to offer employment to desired employees, move payroll systems, address accrued benefits, sort out restrictive covenants, and line up contract assignments. If a key customer contract requires consent and the customer hesitates, the operational risk becomes immediate.

The same goes for landlords, lenders, and counterparties. They may use an assignment request as a means to renegotiate terms. That can delay closing or reduce the value of the acquired business on day one.

A careful review of employment documents is often central to this analysis. For businesses where key personnel hold revenue relationships or proprietary know-how, an employment agreement review can be just as important as the financial diligence.

On the ground: The buyer who ignores employee and contract transfer mechanics usually ends up renegotiating under deadline pressure.

Questions that should be answered before signing

Operational diligence should test these points early:

Who are the employees the buyer must keep?

Not just the people with titles. The people who hold customer trust, technical systems knowledge, or vendor relationships.Which contracts need consent?

A contract can survive in a stock deal but still require notice or approval because of a change-of-control clause.What happens to benefit obligations?

Transitioning plans, accrued time, commissions, and bonuses can become unexpectedly sensitive.Which permits are personal to the entity or owner?

In Connecticut, local and state licensing issues can decide whether an asset deal is practical.

For many service businesses, this section matters more than the tax discussion. A structure that saves taxes but disrupts employees, clients, or licenses can still be the wrong deal.

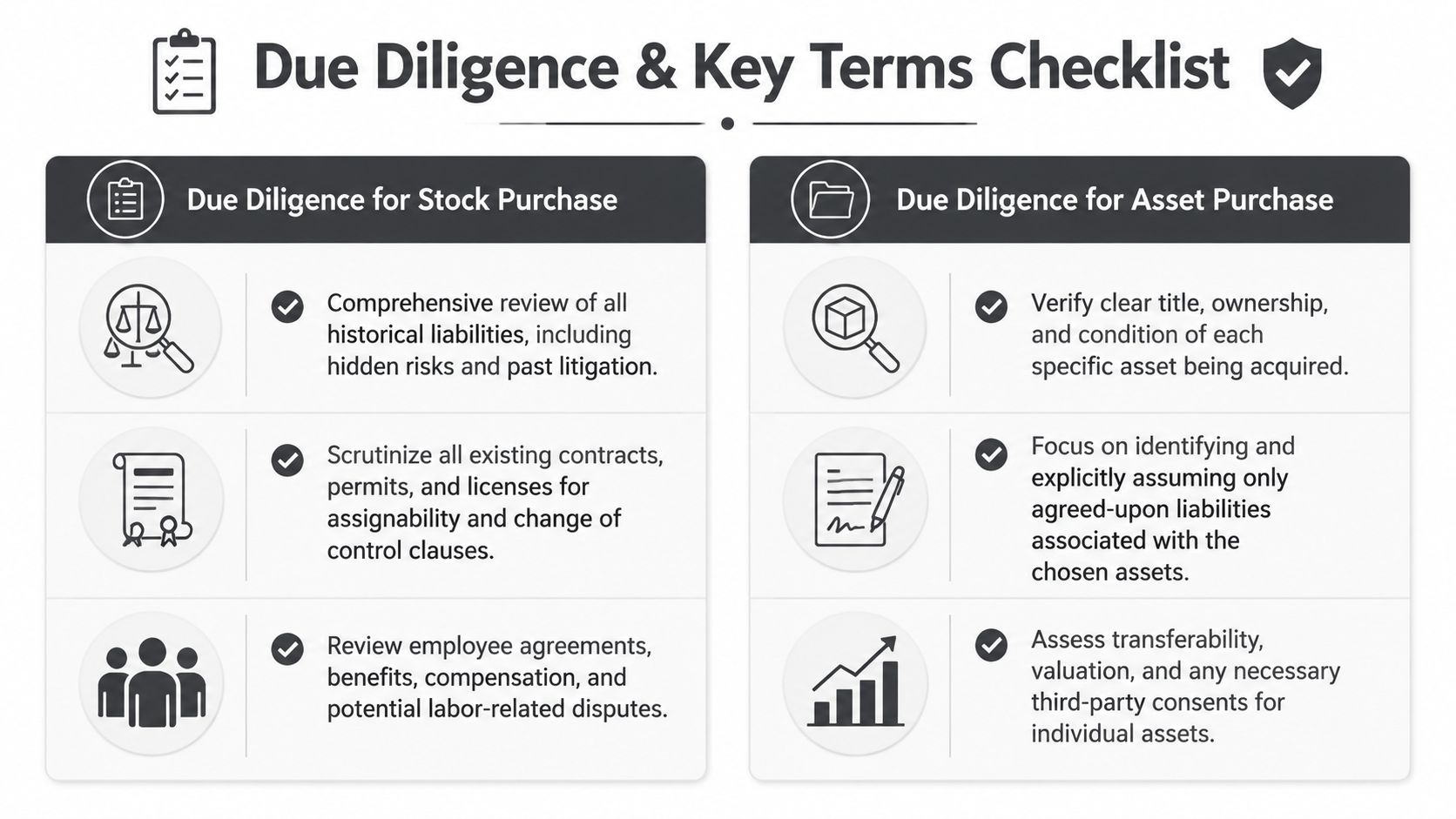

Due Diligence Checklists and Key Deal Terms

Due diligence should change with the structure. If it doesn't, the team is probably using the wrong checklist.

In a stock purchase, diligence needs to examine the full entity because the buyer is stepping into it. In an asset purchase, diligence can narrow around title, transferability, and the liabilities connected to the specific assets being acquired.

A broader framework for organizing that process appears in this M&A due diligence checklist, but the practical focus shifts sharply depending on structure.

Stock purchase diligence

For a stock deal, I want the buyer's diligence team thinking like an owner of the entire box. That means historical, corporate, and compliance review.

Priority items usually include:

- Entity and governance records: Formation documents, ownership records, meeting approvals, and authority to sell.

- Capitalization: Who owns what, whether any rights are outstanding, and whether anyone can object or block.

- Liability history: Tax matters, litigation, employment disputes, compliance issues, and old claims that may reappear.

- Contracts and controls: Material agreements, debt documents, restrictive covenants, insurance, and internal operating practices.

The key contract terms in stock deals often include broader representations and warranties, more extensive disclosure schedules, and stronger indemnity mechanics because unknown liabilities are part of the central risk.

Asset purchase diligence

For an asset deal, the question isn't “what could be wrong with the company?” It's “what exactly am I buying, can it be transferred, and what obligations travel with it?”

That usually means:

| Diligence item | Why it matters in an asset deal |

|---|---|

| Title and ownership | Confirms seller actually owns each asset being sold |

| Liens and encumbrances | Identifies secured claims that must be released or addressed |

| Assignability | Tests whether contracts, leases, and licenses can move |

| Asset condition and records | Helps avoid disputes over missing, impaired, or unusable property |

In asset deals, the drafting pressure lands on the schedules. If an asset, contract, or liability isn't clearly addressed, someone will argue about it later.

Deal terms that deserve special attention

Regardless of structure, there are several provisions that do most of the practical work:

- Purchase price adjustments: These can protect against closing-day surprises in working capital or debt-like items.

- Covenants before closing: They keep the seller from materially changing the business while approvals are pending.

- Indemnification architecture: Survival periods, baskets, caps, and claim procedures determine whether a remedy has value.

- Access and transition support: Post-closing cooperation can be critical if customer files, accounting records, or licenses need follow-up.

The best due diligence memo is the one that changes the documents before closing, not the one that merely describes the risk after the fact.

A disciplined process doesn't guarantee a good outcome. But weak diligence almost guarantees expensive surprises.

Making the Right Choice in Connecticut

There isn't a universal winner in the asset purchase vs stock purchase decision. The right structure depends on the business, the parties, and the points each side is willing to trade.

For a Connecticut buyer, I'd usually start with four practical questions.

Start with risk, not preference

First, how much history are you willing to inherit? If the target has complicated operations, old liabilities, thin records, or unresolved tax and employment issues, an asset structure may offer cleaner control. If the company has a strong record, stable compliance, and valuable continuity, a stock purchase may be worth the additional diligence burden.

Second, what makes the business valuable? If the value sits in contracts, permits, employees, and continuity of operations, stock treatment may fit better. If the value sits in selected accounts, equipment, intellectual property, or a business line the buyer wants to carve out, an asset deal often makes more sense.

Connecticut-specific pressure points

Connecticut deals also need a local review that generic national guides often skip.

Consider these examples:

- Real estate inside the business: If company-owned real estate is part of the transaction, transfer-tax and recording issues should be examined early because the structure can change how the transfer is implemented and documented.

- State and local licensing: Certain businesses can't assume that a permit or approval will move smoothly in an asset transfer.

- Employment concentration: In closely held Connecticut businesses, a small group of employees may carry most of the customer goodwill. If their transition isn't secured, legal structure won't save the deal economics.

- Closely held ownership issues: Family businesses and partner-owned entities often have consent, governance, or authority issues that can complicate a stock sale.

A decision framework that works in practice

If you're a seller, ask:

- Do I need continuity and closing simplicity?

- Am I prepared for asset-level carve-outs and excluded liability disputes?

- Would a stock deal better preserve value after taxes and transition costs?

If you're a buyer, ask:

- Do I trust the company's historical records enough to buy the entity?

- Are third-party consents manageable if I buy assets instead?

- Which structure gives me the cleaner post-closing operating platform?

The best structure is the one that aligns economics, risk allocation, and closing mechanics. If one of those three breaks, the deal usually gets repriced or stalls.

A good lawyer doesn't just label one structure “buyer friendly” or “seller friendly.” The job is to pressure test the business facts, identify where value can leak out, and document the transaction so the deal survives contact with closing and post-closing reality.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.