A customer says your sales team promised one thing and delivered another. A departing advisor takes client information and starts calling former accounts. A competitor claims your marketing crossed the line from aggressive into deceptive. In Connecticut, those disputes often don't stay limited to breach of contract, employment, or regulatory issues. They turn into claims under the Connecticut Unfair Trade Practices Act, usually called CUTPA.

That matters because CUTPA gives plaintiffs an advantage. It can pull an ordinary business dispute into a broader unfair trade practices case with exposure that goes beyond the underlying transaction. For financial professionals, the analysis gets even more complicated because securities and advisory work often sits inside a regulated environment, but regulation doesn't automatically take CUTPA off the table.

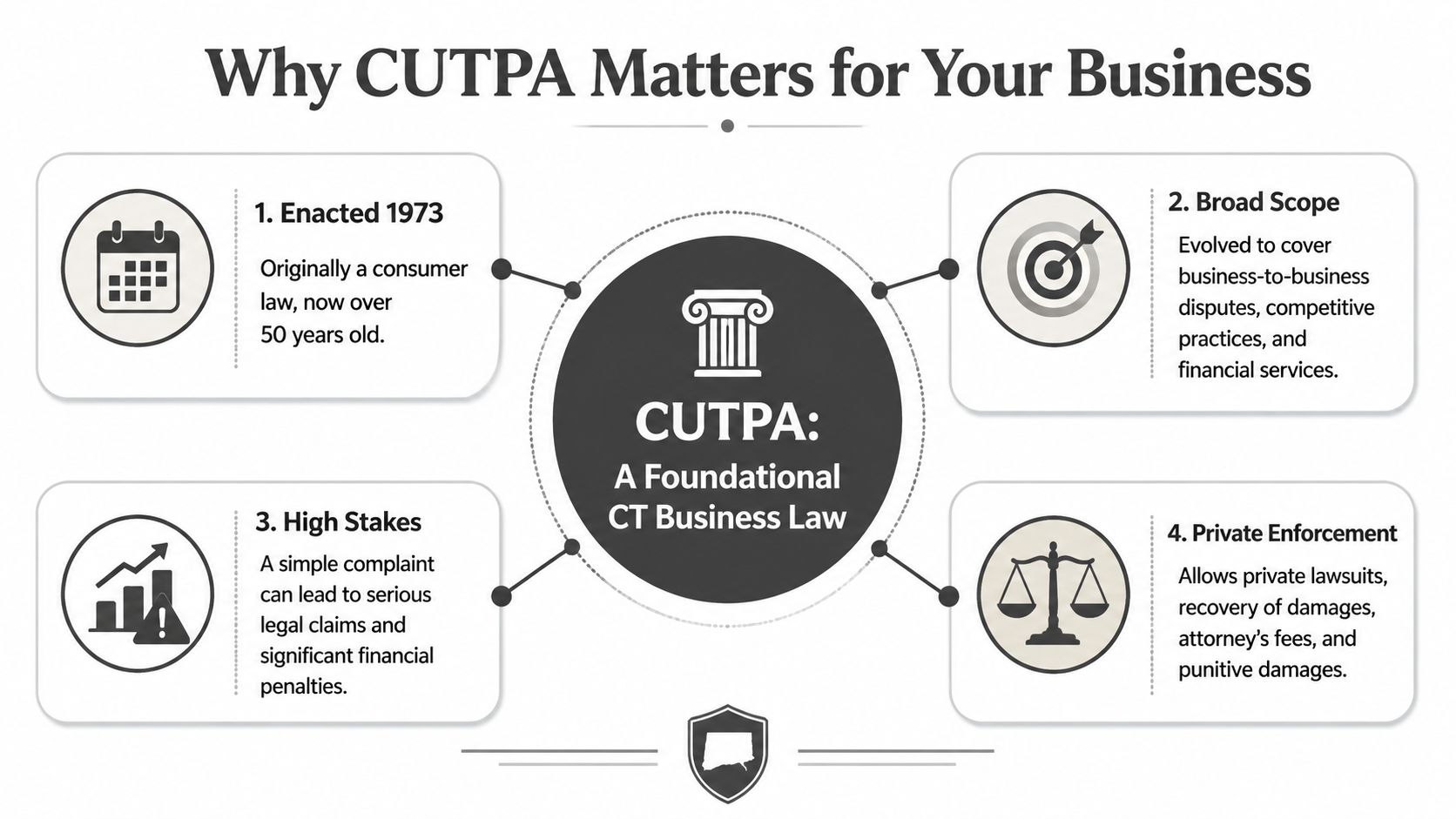

Why CUTPA Matters for Your Connecticut Business

CUTPA is one of the most important statutes in Connecticut business litigation. It was enacted in 1973, and over time it has evolved from a consumer protection measure into a broad business tort statute that reaches nearly all business conduct in the state, not just traditional consumer transactions, as discussed in this Connecticut unfair competition and trade secrets overview. That same source notes that CUTPA's remedial structure allows private enforcement and supports claims for damages, attorney's fees, punitive damages, and injunctive relief.

For a business owner, that means a dispute that looks routine at first can become much more serious. A vendor disagreement may become an unfair competition claim. A customer complaint may turn into litigation alleging deception. A fight between advisors over client solicitation may be framed as misuse of confidential information plus unfair trade practices.

It reaches far beyond retail consumer disputes

Many business clients still assume CUTPA is mainly a statute for consumer complaints against stores or home improvement contractors. That view is outdated. In practice, Connecticut lawyers regularly evaluate CUTPA in disputes involving sales practices, competition, misrepresentations, customer communications, and conduct surrounding ongoing commercial relationships.

If your company markets services, negotiates contracts, handles customer complaints, or competes for accounts, CUTPA is already part of your risk environment.

A useful starting point is to review how unfair and deceptive conduct is treated in broader Connecticut business disputes, including on Kons Law's discussion of deceptive and unfair trade practices.

Why sophisticated businesses pay attention early

CUTPA changes settlement posture. It also changes how internal documents, marketing language, and employee conduct will be viewed if a dispute matures into a claim.

Practical rule: If a fact pattern involves pressure tactics, omissions, misleading comparisons, or sharp dealing, assume someone will at least explore a CUTPA theory.

That is especially true in finance. Broker-dealers, RIAs, advisors, and branch managers often focus on federal or FINRA compliance first. They should. But a Connecticut CUTPA claim may still arise from the same events, especially where the complaint isn't limited to the regulated transaction itself and instead targets surrounding conduct such as recruiting, marketing, disclosures, or post-termination solicitation.

Defining a Violation The Cigarette Rule Test

CUTPA is broad because the legal standard is broad. Connecticut courts apply the cigarette rule, under which a practice may be unfair if it offends public policy, is immoral or unscrupulous, or causes substantial injury. A strong showing on one factor or meeting any two of the three can be sufficient, and a plaintiff only needs to show an ascertainable loss, meaning a measurable loss of money or property, without proving the precise amount of that loss, as reflected in Connecticut General Statutes § 42-110b and related authority.

What the three factors mean in practice

The first factor asks whether the conduct offends public policy. In plain terms, courts look at whether the conduct runs against established legal or regulatory norms. A business doesn't need to commit a separate statutory violation every time, but conduct that brushes up against existing legal standards is more vulnerable.

The second factor looks at whether the conduct is immoral, unethical, oppressive, or unscrupulous. Many business defendants find this aspect surprising. They may say, correctly, that there was no outright lie. But if the overall conduct looks manipulative, one-sided, or intentionally unfair, that may still create risk.

The third factor focuses on substantial injury. The question isn't limited to whether someone was angry or inconvenienced. The question is whether the conduct caused a real commercial injury that the plaintiff can tie back to the practice at issue.

Malice isn't required

CUTPA doesn't only target obvious fraud. A company can create exposure through sloppy disclosures, sales scripts that overpromise, silence about a material limitation, or aggressive post-sale conduct.

Consider these examples:

- A service contract with hidden limitations: The contract technically includes the limitation, but the sales process strongly implies broader coverage. That mismatch can invite a CUTPA theory.

- A product comparison that leaves out a key fact: The statement may not be false, but if it creates a misleading impression, the risk rises.

- A complaint handling process that stonewalls the customer: Post-transaction conduct matters. Businesses sometimes overlook that.

A CUTPA analysis often turns on the overall impression created by the conduct, not just whether one sentence was literally accurate.

Ascertainable loss is a lower hurdle than many expect

Businesses often assume a plaintiff needs a fully developed damages model before bringing a CUTPA claim. That's not how the statute works. The plaintiff must show a measurable loss of money or property, but not the exact amount at the outset.

That matters in early motion practice. It also matters in demand letter response strategy. If the other side can identify a concrete loss tied to the challenged conduct, dismissal isn't always easy.

Common CUTPA Claims in Business and Finance

The patterns that generate CUTPA claims are usually familiar. What changes is the label attached to them and the remedies that may follow.

In ordinary commercial disputes

A manufacturer advertises one specification, but the delivered product doesn't perform to that standard. A distributor substitutes a different product line. A company spreads misleading statements about a competitor's services during a bid process. Those are all the kinds of facts that can support a CUTPA count when the conduct goes beyond a simple contract breach.

Another recurring issue is deceptive sales framing. If the pitch says, "this fee covers everything," while internal practice adds charges the customer wouldn't reasonably expect, the dispute may become more than a billing disagreement.

Online reputation practices can create their own problems. There is nothing improper about asking satisfied customers for honest feedback. But companies should be careful not to filter, pressure, or mischaracterize reviews in a way that creates a misleading public impression. Businesses trying to boost your Google reviews should focus on authentic review generation, clear request language, and internal controls over who responds and what gets promised.

In finance and advisor disputes

In the financial services space, the fact patterns often involve relationships, transition events, and communications around trust.

A common example is a departing advisor who takes confidential client information and uses it to solicit accounts for a new firm. Another is a marketing pitch that overstates how an advisory program works, minimizes restrictions, or presents a product as safer or more flexible than it really is. Form U5 disputes can also create CUTPA risk when the surrounding conduct includes allegedly false representations, strategic pressure, or business interference beyond the filing itself.

These cases are rarely just about one statement. They usually involve a sequence of acts, such as recruiting promises, compensation discussions, account transitions, customer messaging, and internal restrictions.

For businesses trying to reduce exposure, fraud prevention principles still matter. This broader discussion of preventing business fraud is a useful reminder that documentation, access controls, and prompt internal review often shape the outcome long before a complaint is filed.

Client-side lesson: If the dispute involves confidential information, customer communications, and competitive harm at the same time, expect CUTPA to be part of the pleading strategy.

The Regulated Conduct Exemption Explained

For financial professionals, the most misunderstood part of CUTPA is the statutory exemption for transactions "otherwise permitted under law as administered by any regulatory board or officer." The Connecticut Department of Consumer Protection explains that this exemption is important in heavily regulated settings, but it is not a blanket immunity, and it may not protect deceptive conduct outside what the regulator specifically permits, as described on the Connecticut DCP CUTPA page.

What the exemption actually does

The exemption narrows CUTPA in some regulated environments. It does not erase it. That distinction is where many defense strategies either succeed or fail.

If a claim attacks conduct that a regulatory framework specifically allows or governs, the exemption may be a serious issue for the plaintiff. But if the challenged behavior sits outside that permitted conduct, CUTPA may still apply.

A useful way to think about it is to separate the regulated transaction from the surrounding business behavior.

Where firms get this wrong

A broker-dealer may assume that because securities activity is extensively regulated, any related claim is automatically exempt. That's too broad. The better question is narrower: what exactly was permitted, by whom, and does the plaintiff's claim target that conduct or something adjacent to it?

Examples help:

- More likely to raise the exemption: The core complaint attacks a transaction handled within an established regulatory framework, with required disclosures and procedures.

- Less likely to be exempt: The complaint targets deceptive marketing used to obtain the client, misleading statements about the advisor's services, improper solicitation tactics, or conduct during a transition that the regulator did not specifically authorize.

- Mixed scenario: Part of the case may involve regulated conduct, while another part focuses on separate business behavior. Those cases need careful parsing.

Regulation and CUTPA often coexist. Compliance with one body of rules helps, but it doesn't automatically answer every unfair trade practices allegation.

For advisors, registered representatives, and firms handling termination disputes or customer complaints, precision matters. A broad "we're regulated" defense is often weaker than a disciplined analysis of what conduct was permitted and what conduct was not.

Navigating a Claim Standing Remedies and Damages

Once a CUTPA claim is asserted, the first practical question is usually who can sue. CUTPA isn't limited to consumers. Businesses can bring claims too, so long as they can show the required measurable loss tied to the challenged conduct. That is one reason competitor disputes, vendor disputes, and post-employment business fights so often include a CUTPA count.

What a plaintiff may seek

The remedy picture is what gives CUTPA much of its force. The statute's broad remedial design supports private enforcement and allows claims for damages, attorney's fees, punitive damages, and injunctive relief, as noted earlier in the article from the Connecticut business litigation source discussing CUTPA's role in commercial disputes.

In practical terms, a plaintiff may seek:

- Compensatory relief: Recovery tied to the loss allegedly caused by the unfair conduct.

- Injunctive relief: A court order aimed at stopping the challenged practice.

- Fee shifting: Exposure doesn't stop with the underlying dispute.

- Punitive remedies: In the right case, the pressure increases significantly.

When attorney's fees and punitive damages are in play, even a modest underlying dispute can become expensive to defend.

Why early case framing matters

A CUTPA case is often won or lost early through framing. Was this only a contract dispute, or was there something deceptive, coercive, or unfair about the way the business acted? Did the company preserve documents showing clear disclosures and good-faith handling, or is the record filled with internal messages that make the conduct look worse?

Defense strategy usually turns on a short list of questions:

- What conduct is being challenged

- Can the plaintiff identify a measurable loss

- Does a regulatory exemption argument apply to part of the claim

- Would a judge view the conduct as ordinary commercial friction or something sharper

That analysis should happen immediately after a demand letter, complaint, or threatened filing. Delay usually makes the record worse, not better.

Proactive CUTPA Compliance for Your Business

Most CUTPA problems don't start in the courtroom. They start in sales language, onboarding documents, compensation discussions, customer follow-up, and internal shortcuts that someone thought were harmless.

Focus on the conduct that creates the claim

The best compliance approach is practical. Review the words your business uses to win work, not just the forms legal approved years ago. Test whether your people describe products and services the same way your contracts and disclosures describe them.

This is especially important in regulated industries, where teams sometimes assume formal compliance documents solve everything. They don't. Customer-facing language, advisor recruiting conversations, transition communications, and complaint responses all matter. Businesses that want a stronger framework should also understand the broader role of regulatory compliance in reducing litigation risk.

CUTPA Risk Mitigation Checklist

| Action Area | Key Compliance Check | Status (To Do / In Progress / Complete) |

|---|---|---|

| Marketing materials | Confirm claims are accurate, supportable, and consistent with actual service delivery | To Do / In Progress / Complete |

| Sales process | Review scripts, emails, and pitch decks for omissions or overpromises | To Do / In Progress / Complete |

| Contracts and disclosures | Make sure limitations, fees, restrictions, and conditions are stated clearly | To Do / In Progress / Complete |

| Complaint handling | Create a written escalation path for customer complaints and document responses | To Do / In Progress / Complete |

| Employee transitions | Limit access to confidential information and define post-departure protocols | To Do / In Progress / Complete |

| Competitor communications | Prohibit unsupported statements about competing products or firms | To Do / In Progress / Complete |

| Financial services supervision | Compare marketing and client-facing statements against approved compliance language | To Do / In Progress / Complete |

| Record retention | Preserve emails, notes, and drafts that show what was said and when | To Do / In Progress / Complete |

What usually works and what doesn't

These steps usually help:

- Tight review of marketing copy: If a claim sounds broader than operations can support, revise it.

- Training tied to real scenarios: Sales staff and advisors need examples, not abstract warnings.

- Prompt complaint review: Small disputes become larger when a business dismisses them too quickly.

These approaches usually fail:

- Boilerplate disclaimers as a cure-all: Fine print doesn't always fix a misleading overall message.

- Fragmented supervision: Legal, compliance, and sales can't work from different scripts.

- Silence after a problem surfaces: A weak response often becomes part of the claim.

Good CUTPA prevention isn't about sounding cautious. It's about making sure the business actually behaves the way it markets itself.

When to Contact Business Litigation Counsel

Three situations should put a Connecticut business on notice.

First, someone accuses your company of deception, unfair competition, misleading marketing, or misuse of confidential information. Second, a regulated business assumes the exemption solves the problem without closely analyzing the actual conduct at issue. Third, a dispute that began as contract, employment, or customer-service friction starts including allegations about unfair methods or deceptive practices.

Those are the moments to involve counsel early, especially if the matter touches advisor transitions, Form U5 issues, customer solicitations, or competitive business conduct. A fast legal review can help preserve documents, narrow the issues, evaluate exemption arguments, and avoid admissions that make a later defense harder.

If your dispute is already moving toward litigation, it also helps to assess it through the lens of broader business dispute strategy, including the issues discussed by a business litigation lawyer.

CUTPA is powerful because it gives plaintiffs a flexible way to characterize business conduct as unfair. For that reason, the best response is rarely improvised. It should be deliberate, fact-specific, and grounded in how Connecticut courts and regulators view commercial behavior.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.