Merchant cash advances are generally structured to be legal sales of future revenue, not loans. But if a court decides the contract is really a loan, the deal can fall under usury law, and in New York that can be a major problem because the commercial usury ceiling is 25%.

That's the part many business owners miss when they ask, Are MCA loans legal? The useful question isn't just whether the product exists lawfully in the market. The key question is whether the agreement you signed will hold up when the relationship breaks down, payments tighten, and the funder starts enforcing default remedies.

A lot of businesses reach this point after the same sequence. Revenue dips. Daily or weekly withdrawals start interfering with payroll, rent, inventory, or tax payments. The funder says the contract is ironclad because it's not a loan. The owner starts wondering whether that label controls anything. In a dispute, labels matter far less than contract substance.

That's where the legal analysis starts. Courts look at risk allocation, repayment terms, default triggers, and whether the funder bought receivables or just dressed up a high-cost loan in MCA language.

What Makes an MCA Legally Different From a Loan

A business owner usually asks this question after the withdrawals start hurting. Sales have slowed, payroll is coming up, and the funder insists the contract is a purchase of receivables, not a loan. In court, that label helps only if the contract shifts risk to the funder.

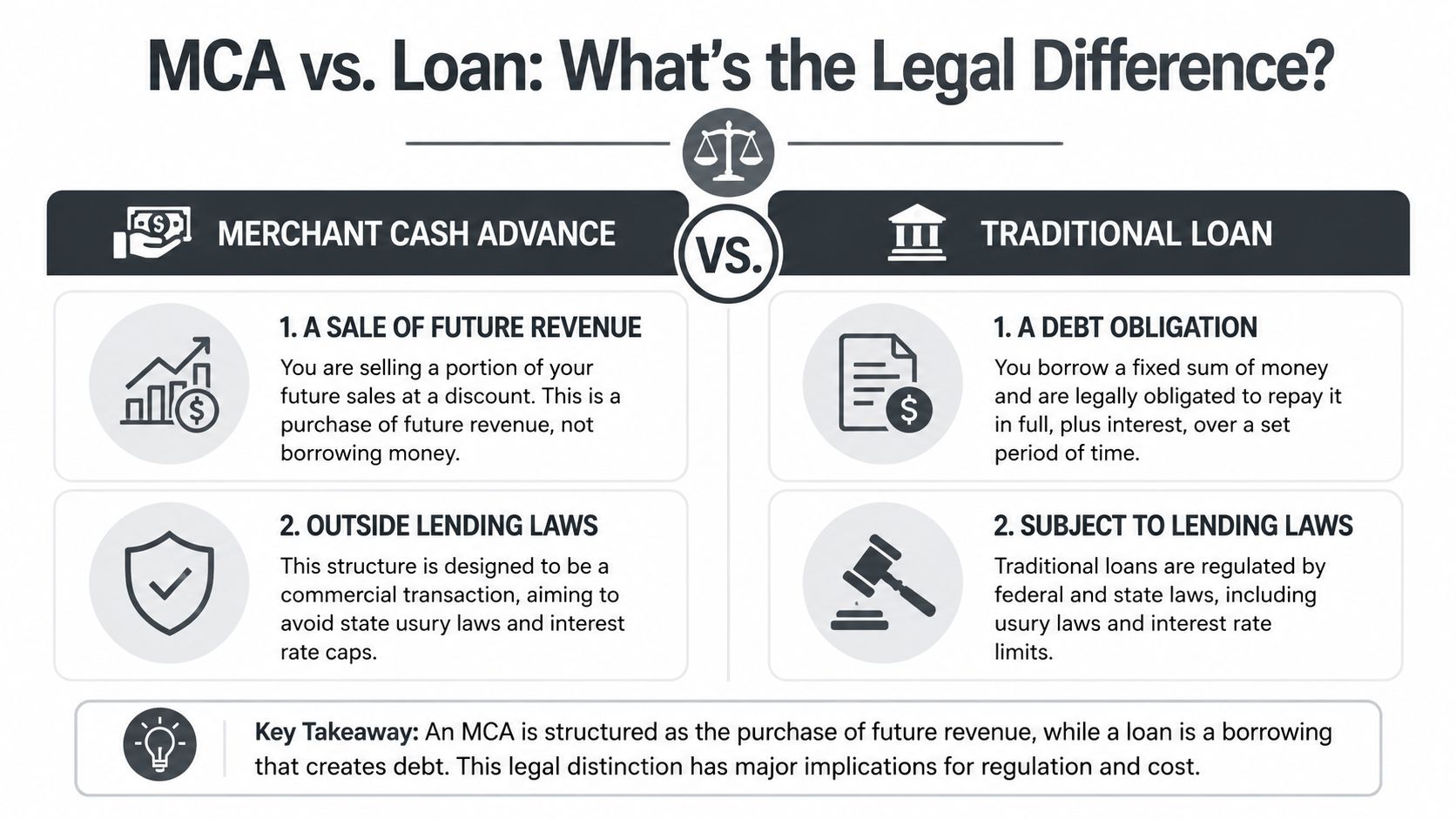

An MCA is drafted as a sale. The funder pays a purchase price now in exchange for a stated percentage of future receivables. A loan works differently. The borrower takes on a debt and must repay principal and interest on set terms.

That distinction matters because a true receivables purchase does not promise the funder full repayment in all events. The funder is supposed to win when the business generates receipts and take the downside risk if receipts fall short. If the contract leaves the business on the hook no matter what happens, the deal starts to look like credit dressed up in MCA terminology.

From a litigation standpoint, the pressure point is simple. Did the funder buy a fluctuating revenue stream, or did it create a fixed repayment obligation and keep lender-style remedies as backup?

I tell clients to ignore the marketing words at first and read the risk allocation. Terms like "purchase price," "purchased amount," and "future receivables" do not decide the case by themselves. Courts and defense counsel look at whether the business had any real chance to pay less, or pay more slowly, if revenue declined.

Several contract features usually separate a real sale from a disguised loan:

- Revenue-based adjustment: The agreement should allow remittances to rise and fall with receipts, not just in theory but through a workable process the business can use.

- No hard maturity date: If receivables come in slowly, the contract should not convert that slowdown into an automatic breach just because a target date passed.

- Risk of non-collection: If the business genuinely fails and receivables never materialize, the funder should bear at least some of that loss instead of having an automatic right to full repayment.

Those are the same practical features business owners should understand before signing any merchant cash advance agreement and funding structure. They also become the first places litigators look when default notices, confessions of judgment, guaranty claims, or ACH enforcement efforts appear.

One more point gets missed often. The legal issue is usually enforceability, not whether MCAs exist as a business product. A merchant cash advance can be lawful in general and still become vulnerable in a specific case because the agreement promises variable payments on one page and fixed repayment on the next.

That internal contradiction is where many disputes are won or lost.

The Three-Factor Test Courts Use to Recharacterize MCAs

A business owner usually sees this issue for the first time after trouble starts. Sales dip, the daily ACH stays the same, a default notice arrives, and the funder insists the company owes the full purchased amount no matter what happened to revenue. At that point, the label on page one matters less than the legal test a court will apply.

Courts do not decide these cases by asking whether the document says "purchase" or "loan." They examine whether the funder took the risk that receivables might never come in. If the agreement shifts that risk back to the merchant through fixed payments, short deadlines, and broad default rights, the MCA can be recharacterized as a loan. That is the enforceability problem many businesses miss.

New York decisions are cited often in MCA litigation because they frame the dispute in practical terms. The recurring question is whether collection depends on receivables or whether repayment is effectively mandatory. If a court treats the deal as a loan, defenses that were irrelevant under a true sale theory can become central very quickly.

Reconciliation clause

The first question is whether reconciliation exists in a real, usable form. A reconciliation clause is supposed to let remittances rise and fall with actual receipts. In litigation, I do not stop at whether the clause appears in the contract. I want to know whether the merchant could realistically use it, how often it could be invoked, what records were required, how fast the funder had to respond, and whether the funder honored those requests in practice.

A clause that works only on paper does not help much. If the funder can keep pulling the same daily amount unless the merchant clears procedural hurdles that are hard to meet during a cash crisis, a judge may view the payment stream as fixed in substance.

That is one reason courts compare MCA language to ordinary debt instruments. A true purchase of receivables should not operate like a promissory note that requires repayment on stated debt terms.

Indefinite term

The second question is whether the agreement has a genuine open-ended term. If the funder bought a percentage of future receivables, payment should take as long as it takes for those receivables to be generated.

A stated expected delivery date is not always fatal by itself. The problem starts when the contract turns that estimate into a practical maturity date. If missing the projected timetable triggers default, extra fees, confessions of judgment, or aggressive collection, the funder is acting more like a lender waiting for a fixed balance to come due.

This factor matters because it exposes the actual bargain. A sale depends on future performance. A loan expects repayment by a deadline.

No recourse tied solely to bankruptcy or business failure

The third question is who bears the downside if the business fails without fraud or misconduct. In a true sale, the funder accepts at least some risk that receivables may dry up. In a disguised loan, the contract usually gives the funder a path to full recovery anyway.

Look closely at default provisions. If bankruptcy, insolvency, a shutdown, or a drop in operations automatically accelerates the full amount and triggers personal guaranty liability, that cuts against true-sale treatment. The same is true when the agreement says the funder purchased future receivables but also treats any interruption in business as an immediate breach.

That mismatch drives a lot of litigation. The contract promises contingency on the front end and certainty on the back end.

True sale vs disguised loan checklist

| Characteristic | True Sale (Likely Legal) | Disguised Loan (High Risk) |

|---|---|---|

| Repayment basis | Tied to actual receivables | Functions like fixed repayment |

| Reconciliation | Real and accessible adjustment mechanism | Nominal clause or no meaningful adjustment |

| Term | Open-ended, depends on revenue flow | Fixed maturity date or payoff deadline |

| Business failure risk | Funder shares risk of downturn | Merchant effectively guarantees repayment |

| Bankruptcy treatment | No automatic default solely because of bankruptcy | Bankruptcy or insolvency triggers immediate default |

| Collection posture | Enforces receivables purchase rights | Uses remedies consistent with debt collection |

Why these three factors matter in practice

No single clause decides the case. Courts read the agreement as a whole, and they also look at how the parties performed under it.

That second point gets overlooked. A contract can contain MCA wording and still be enforced like a loan if the funder never adjusted withdrawals, treated an estimated term as a hard deadline, and pursued full collection after the business failed. In other words, recharacterization risk comes from both the paper and the conduct.

For a business owner, the practical question is simple. If revenue falls sharply tomorrow, can payments fall with it, or will the funder still demand the same dollars on the same schedule with default remedies waiting in the background? That answer usually tells you how a court will view the agreement.

Navigating State MCA Laws Especially in Connecticut

A Connecticut business owner can lose an MCA dispute even before the court reaches the true-sale-versus-loan fight. I see that happen when the contract looks polished, the withdrawals start, revenue drops, and only then does anyone check whether the provider followed state registration and disclosure rules. By that point, the compliance file matters almost as much as the contract.

State law changes the pressure points in these cases. Some states focus on disclosures. Others require registration and regulate how providers market and collect these products. Those rules do not answer the recharacterization question by themselves, but they often shape settlement value, injunction requests, and how much room the funder has to enforce aggressively.

California and Connecticut take different routes

California has built a disclosure-focused system for commercial financing and also restricts unfair, deceptive, or abusive conduct. That means an MCA provider can face regulatory exposure even if it drafted the agreement to look like a receivables purchase.

Connecticut uses a registration-and-disclosure model. MCA providers doing business there must register with the banking commissioner and provide defined disclosures about the transaction's economics, including the amount provided, how repayment works, and broker compensation, as described in this review of MCA disclosure laws and non-compliance risks.

That distinction matters in litigation. In California, the fight often centers on what was disclosed and whether the provider's conduct was deceptive. In Connecticut, I would also want to know whether the provider was properly registered before it ever funded the deal.

What Connecticut businesses should check

If the business is in Connecticut, review the file with enforceability in mind, not just with an accounting lens.

- Provider registration: Was the MCA company registered with the banking commissioner when it offered or funded the transaction?

- Required disclosures: Did the provider disclose the amount advanced, the repayment method, and any broker compensation in a form the statute requires?

- Mismatch between pitch and paper: Did the sales process describe flexible revenue-based remittances while the contract imposed fixed withdrawals and hard default triggers?

- Post-funding conduct: After revenue dropped, did the provider honor the structure it sold, or did it collect like a conventional lender?

- Broker involvement: If a broker was paid, was that compensation disclosed, and did the broker's communications create additional misrepresentation issues?

For a broader summary of the state-by-state framework, see Kons Law's overview of merchant cash advance regulation.

A registration or disclosure violation will not automatically void every MCA. But it can change the case. It may support affirmative claims, weaken the funder's equitable position, and give the business better ground to challenge fees, collection tactics, or enforcement remedies.

Why this matters for contested cases

The practical mistake is treating state compliance as a side issue. In a disputed MCA, it is often part of the main liability and enforcement analysis.

If the provider failed to register, omitted required disclosures, or used sales materials that do not match the contract it is suing on, those facts can reinforce the broader argument that the transaction was not administered as a legitimate purchase of receivables. They also give the business arguments that do not depend entirely on winning the recharacterization issue. In Connecticut, that can be the difference between defending a collection case on the funder's terms and forcing a more balanced fight.

Common Red Flags in Merchant Cash Advance Agreements

A business owner usually does not call counsel because the contract used the phrase "purchase of receivables." The call comes after daily withdrawals keep hitting despite a sales drop, a default notice cites a technical breach that has nothing to do with receivables, or the owner learns a personal guaranty reaches much further than expected. By that point, the legal question is no longer abstract. The question is whether the agreement was written and enforced like a true sale, or whether a court may treat it like a loan.

Contract terms that deserve immediate scrutiny

Some clauses matter because they increase collection pressure. Others matter because they undercut the funder's main legal position if a dispute reaches court.

Confession of judgment language: This is an aggressive enforcement device. In the right setting, it can let a creditor obtain judgment without ordinary motion practice or trial. If your agreement includes it, review what a confession of judgment means in practice and whether the clause is even usable under the governing law.

A reconciliation clause that exists only on paper: Many MCA contracts say remittances will rise or fall with receivables. The key question is whether the contract gives a clear method, a real timetable, and workable standards for adjustment. If the process is vague, discretionary, or loaded with obstacles, that cuts against the idea that payment is truly contingent.

A personal guaranty that covers ordinary nonpayment: A limited guaranty for fraud, diversion of receivables, or other bad acts is easier to defend. A guaranty that effectively makes the owner backstop the entire purchased amount, even if the business merely underperforms, looks much more like loan risk shifted to the merchant.

Defaults triggered by routine operational changes: Watch for defaults tied to changing processors, moving bank accounts, taking other financing, experiencing a general adverse change, or missing paperwork deadlines unrelated to receivables. Those provisions give the funder a way to accelerate collection without proving that receivables were withheld.

Drafting problems that create litigation risk

In contested MCA cases, courts often read the full agreement against the funder's labels. I pay close attention to internal contradictions because they often reveal what the parties were really doing.

A contract may open by describing a sale of future receivables, then switch to debt language in the remedy provisions. Terms like "loan amount," "repayment," "balance due," or fixed remittance schedules are not harmless drafting sloppiness if they match the way the deal operated in practice. The same goes for remedies that look like standard lender protections rather than buyer rights tied to a receivables purchase.

Red flags include:

- Sale language in the recitals, but debt language in payment and default sections

- Fixed ACH withdrawals with no meaningful tie to actual revenue

- Security interests that sweep far beyond the receivables supposedly sold

- Remedies that guarantee the funder full recovery regardless of business performance

- Owner liability that continues after ordinary business failure, not just misconduct

If the funder's downside disappears in the contract, the argument that it bought a contingent asset gets much weaker.

Red flags outside the four corners

The paper matters. So does performance.

If the funder refuses reconciliation requests, keeps taking the same daily amount during a revenue collapse, or declares default the moment the merchant asks for an adjustment, those facts can matter as much as the written clause. In litigation, I look for the mismatch between what the agreement promises and what the funder did. A contract drafted to preserve contingency can still be enforced like a fixed repayment obligation. That is where recharacterization arguments gain traction.

Broker emails can also become evidence. If the sales pitch promised "no personal risk," "flexible payments," or "not a loan," but the signed package and collection conduct show the opposite, those communications may support fraud, deceptive practices, or recharacterization arguments depending on the forum and the facts.

What usually fails as a standalone defense

Cost alone rarely carries the case. A high factor rate or expensive payoff number may explain why the deal hurt the business, but it does not by itself prove the agreement is unlawful if the transaction is a true receivables purchase.

The stronger defense is narrower and more concrete. Identify the terms that removed real contingency, the remedies that guaranteed repayment, and the conduct showing the funder collected as if it were a lender. Those are the facts that tend to matter when a court decides whether the MCA is enforceable as written.

Your Options When Contesting an MCA

Once problems start, waiting usually helps the funder. A business that acts early can improve its position, preserve evidence, and avoid letting the default narrative harden against it.

The first move is practical, not dramatic. Gather the full contract package, every addendum, payment authorizations, bank records, broker communications, renewal offers, and all default notices. You need the paper trail before you can assess whether the deal is vulnerable on recharacterization, disclosure, or enforcement grounds.

Start with the contract's own procedures

If the agreement contains a reconciliation provision, use it. Make the request in writing. Be precise. Ask for an adjustment tied to actual receivables and keep proof of delivery. If the funder ignores the request or imposes obstacles that make reconciliation illusory, that response may matter later.

Then compare what the contract promises with what transpired:

- Review remittance behavior: Were withdrawals tied to revenue, or did they function as fixed payments?

- Track default escalation: Did the funder declare default based on a technicality rather than an actual failure to turn over receivables?

- Document pressure tactics: Save call logs, emails, ACH notices, and any threats involving immediate judgment or account freezes.

Put every key request in writing. Oral discussions disappear. Written requests create a record.

Build leverage before litigation if possible

Many MCA disputes are won or lost before a complaint is filed. A strong pre-litigation position can come from identifying one or more of these issues:

- Recharacterization risk: The agreement functions like a loan, not a true sale.

- Disclosure failures: Required economic terms weren't properly disclosed.

- Registration problems: The provider may not have complied with state requirements.

- Improper collection conduct: The funder enforced rights the contract or law didn't allow.

That doesn't mean every business should stop paying immediately. That decision is highly fact-specific and can create its own risk. But it does mean you shouldn't assume the funder's first legal position is the final one.

Know what a legal challenge is trying to prove

A useful defense often has a focused objective. You may be trying to show the MCA is unenforceable as written. You may be trying to narrow collection remedies. You may be trying to force a real reconciliation, negotiate an exit, or defend against aggressive enforcement after default.

Clear goals matter. So does speed. Once judgments, account restraints, or sweeping UCC-based collection efforts begin, the cost of fixing the problem rises quickly.

Next Steps Protecting Your Business and Finding Help

The most important takeaway is simple. The answer to Are MCA loans legal depends far less on the product label than on the contract's substance. A true sale of future receivables can be lawful. A contract that guarantees repayment, strips out risk, and ignores state compliance rules may face serious enforceability problems.

That's why business owners should read MCA documents with two questions in mind. First, does the funder share receivables risk? Second, did the provider follow the registration, disclosure, and conduct rules that apply where your business operates?

If you're still weighing funding options, it also helps to compare MCAs against other sources of capital that don't require giving up equity. A practical starting point is Credit for Startups' non-dilutive guide, which outlines alternatives that may be worth reviewing before signing a high-pressure receivables deal.

If you already signed, don't assume you're stuck. Many businesses have more room to challenge these agreements than they think, but that only becomes clear after a careful review of the documents, payment history, and enforcement posture.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.