You won the case. The court entered judgment. The debtor still hasn't paid.

That gap between a legal win and actual recovery is where many creditors get stuck. A judgment tells you that you're owed money, but it doesn't put funds in your account. If the debtor owns real estate, though, you may have a way to convert that paper judgment into a true enforcement tool.

A judgment lien on real estate is often the most practical post-judgment tool available to a business owner, lender, or trade creditor. It doesn't always produce immediate payment. What it does is attach your claim to property, interfere with clean title, and force the debt into the center of any future sale or refinance discussion.

For creditors, that's an advantage. For debtors, it's a serious problem that shouldn't be ignored.

From Courtroom Victory to Secured Debt

A familiar scenario plays out like this. A vendor sues for unpaid invoices, spends the time and money to get judgment, and expects the pressure of a court order to bring payment. Instead, the debtor goes quiet, makes excuses, or claims there's nothing to collect.

That is where many creditors learn the hard lesson that a judgment isn't self-executing. It confirms the debt. It doesn't secure it.

When a debtor owns real estate, recording a judgment lien can change the posture of the case. The creditor moves from holding an unsecured claim to asserting an interest against property. In practical terms, that often means the debt can no longer be ignored when the owner wants to sell, refinance, transfer title, or clean up title issues during another transaction.

For business owners who are new to collections work, it helps to understand the difference between winning a lawsuit and becoming a judgment creditor. Those are related concepts, but they aren't the same thing strategically. The judgment is the court's ruling. The collection tools that follow are what give that ruling economic value.

A court judgment ends the liability fight. The collection process starts the enforcement fight.

In Connecticut, judgment liens can be highly effective because real estate creates a fixed target. Bank accounts move. Business entities get dissolved. Vehicles depreciate. Real property is different. It sits in public records, and title issues usually surface at exactly the moment the owner needs a transaction to close.

That is why creditors often focus on real estate first. Not because every lien leads to foreclosure, but because many liens produce payment long before foreclosure ever becomes necessary.

What Is a Judgment Lien on Real Estate

A judgment lien on real estate is best understood as an involuntary mortgage. The debtor didn't agree to it, didn't sign for it, and usually doesn't want it there. But once properly created and recorded, it places a legal encumbrance on the debtor's real property to secure payment of the judgment.

How the lien actually works

A recorded lien doesn't usually hand the creditor immediate possession of the property. Instead, it clouds title and preserves the creditor's place in line against the property. If the owner later tries to sell or refinance, the lien becomes part of the closing analysis.

That matters because real estate deals depend on clean title. Buyers want it. Lenders require it. Title insurers won't casually overlook a recorded judgment lien.

The practical effect is straightforward:

- The debt becomes secured by property once the lien is properly attached.

- The owner loses flexibility because transfers and refinancing become harder.

- The creditor gains leverage without necessarily filing an immediate foreclosure action.

Why creditors value judgment liens

Judgment liens have unusual staying power compared with many collection remedies. According to the American Bankruptcy Institute's explanation of judgment lien duration and scope, most judgment liens expire after a statutory period typically ranging from 7 to 10 years, depending on state law, and creditors can often renew them before expiration. That same source explains that the lien can attach not only to real estate owned when recorded, but also to property acquired later while the lien remains active, and that a recorded lien can affect all real estate owned by the debtor within the county where the lien is recorded.

Those features make judgment liens far more than symbolic collection devices. They can remain dormant for years and then become decisive when the debtor finally has equity, tries to close a sale, or acquires new property in the recording jurisdiction.

Practical rule: A judgment lien is often most effective when the debtor thinks time will solve the problem.

How this differs from other liens

Not every lien comes from the same place or works the same way.

| Lien type | How it arises | Typical purpose |

|---|---|---|

| Mortgage lien | By agreement of the owner | Secures a voluntary loan |

| Tax lien | By statute or government action | Secures unpaid taxes |

| Mechanic's lien | By statute after labor or materials are furnished | Secures payment for construction-related work |

| Judgment lien | By court judgment and proper recording | Secures payment of an adjudicated debt |

The key distinction is consent. A mortgage is voluntary. A judgment lien is not. It arises after litigation and exists because the creditor proved a debt in court.

What a judgment lien does not do

It doesn't guarantee payment. It also doesn't mean the property can always be sold to satisfy the debt. Exemptions, prior liens, ownership structure, and available equity all affect the result.

Still, creditors often make the mistake of dismissing judgment liens because they don't produce instant cash. That's the wrong lens. The value is often in influence, title pressure, and long-term positioning.

If the debtor owns meaningful real estate, a judgment lien can turn a stale receivable into an enforceable secured claim with real transactional consequences.

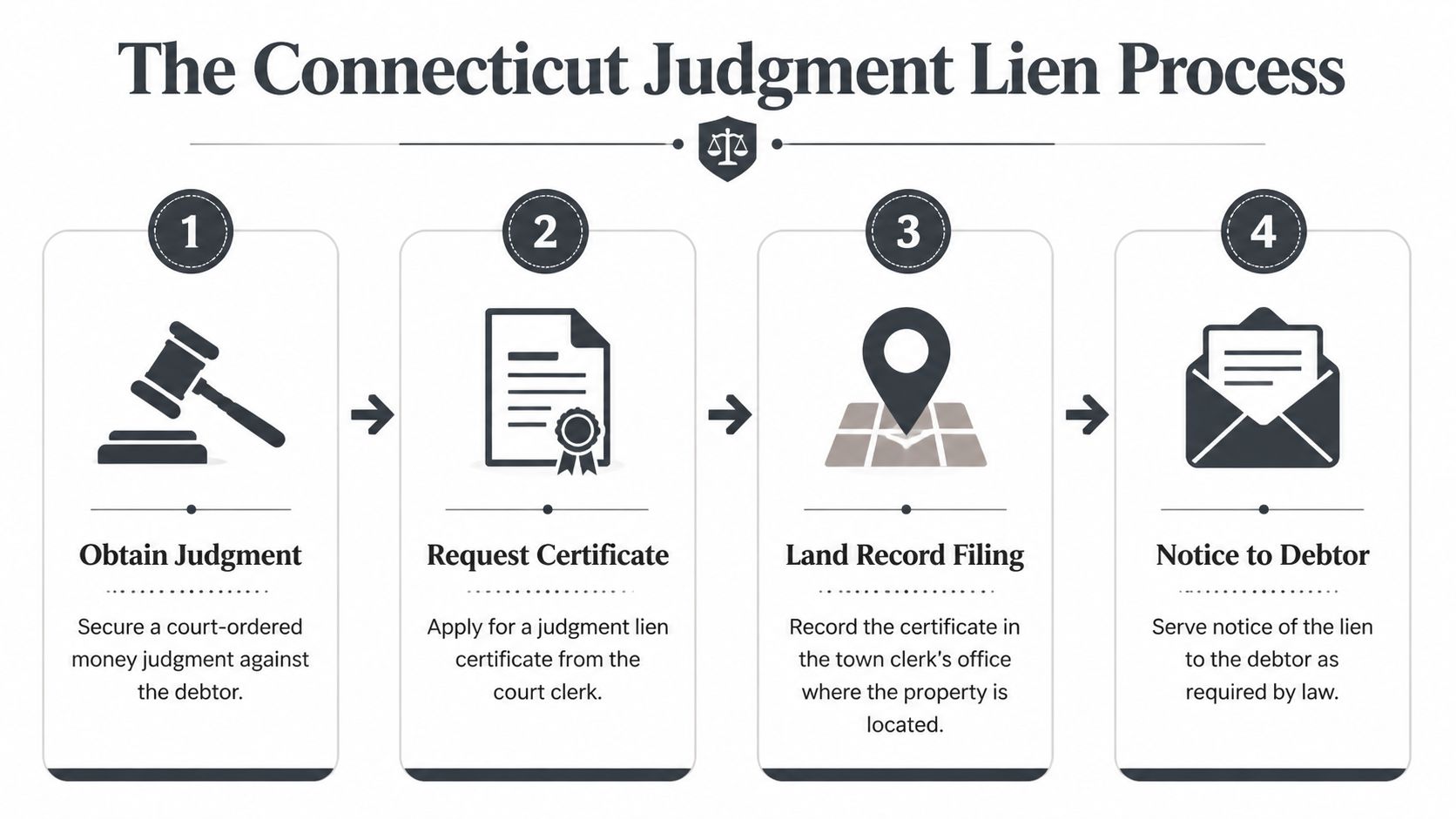

How to Place a Judgment Lien in Connecticut

In Connecticut, a judgment lien on real estate doesn't appear automatically just because you won in court. You have to take specific steps, and each one matters. A missed recording, an incomplete certificate, or filing in the wrong place can undercut the entire remedy.

Start with a final money judgment

You need a court judgment for money damages. No judgment, no judgment lien. That sounds obvious, but creditors sometimes try to shortcut the process by treating a demand letter, settlement breakdown, or unpaid invoice as if it can be recorded against real estate. It can't.

Once judgment enters, the next step is to turn that judgment into a properly recorded lien under Connecticut General Statutes § 52-380a. In practice, that means preparing a Judgment Lien Certificate that complies with the statute and recording it in the correct land records.

Record in the right town land records

In Connecticut, land records are maintained at the town level. That point matters. A lien recorded in the wrong municipality won't attach to the property you thought you reached.

The certificate generally needs to identify the judgment creditor, the judgment debtor, the court, the amount of the judgment, and the property being encumbered with enough specificity for the land records. The document then has to be recorded in the town where the debtor's real property is located.

A practical checklist looks like this:

- Confirm the judgment is final and enforceable.

- Identify the debtor's real estate holdings through land records, title work, or asset investigation.

- Prepare the judgment lien certificate to match Connecticut statutory requirements.

- Record it in each relevant town clerk's office where the debtor owns real estate.

- Serve or provide required notice consistent with Connecticut procedure.

If you're pursuing enforcement after judgment, it also helps to understand the broader set of remedies discussed in how to enforce a judgment. A lien is often strongest when paired with other post-judgment tools rather than treated as the only collection option.

Location controls attachment

One of the most important strategic points is that real estate lien attachment is location-specific. The general rule from other jurisdictions is consistent with what creditors experience in practice: a judgment lien works like a floating lien that becomes effective only when properly docketed or recorded in the right land records, and it is strictly jurisdiction-specific. As explained in Fullerton Law's discussion of county-specific judgment lien attachment, a lien recorded in one county will not attach to real estate in another county.

Connecticut uses town land records rather than a county land record system for this purpose, but the strategic lesson is the same. If the debtor owns property in more than one town, you don't get statewide coverage by recording once.

Record where the land is. Then verify the indexing. Assumptions are expensive in post-judgment work.

What works and what doesn't

Some creditors record quickly, which is good, but do almost no asset review first. Others spend months investigating and never record at all. Neither approach is ideal.

What usually works is targeted speed:

- Search first, then record fast: Confirm ownership and basic title conditions before spending filing fees and service costs.

- Prioritize equity-bearing property: A lien against fully encumbered property may provide little advantage.

- Record in every relevant municipality: If the debtor owns property in Hartford and Stamford, one filing doesn't protect the other.

- Check names carefully: Entity suffixes, middle initials, and judgment debtor identity issues can create avoidable disputes later.

What doesn't work is treating the process as clerical. Judgment lien work is legal work. The details determine whether the lien later survives scrutiny during a sale, refinance, or foreclosure fight.

A Connecticut-specific caution

Connecticut creditors should also think beyond the initial recording date. A lien that isn't tracked, renewed when necessary, or followed up with active enforcement can lose practical value over time. Good judgment enforcement isn't just filing a document. It is monitoring the file, the debtor, and the property for the event that facilitates collection.

That event is often a pending sale.

The Impact of a Lien on Property Title and Sales

Once recorded, a judgment lien changes the property's title profile immediately. The debtor may keep using the property, but title is no longer clean. That is where the strategic advantage comes from.

Why title companies care

A buyer wants marketable title. A lender wants a predictable collateral position. A title insurer wants to issue a policy without inheriting obvious risk. A recorded judgment lien disrupts all three.

That doesn't always mean a sale is impossible. It often means the sale cannot close unless the lien is paid, released, bonded around where permitted, or otherwise resolved through a negotiated closing arrangement.

For the property owner, that's where the lien stops being an abstract legal problem and becomes a transaction problem.

Priority decides who gets paid

Not all liens are equal. Payment order usually depends on priority, and priority often turns on recording sequence and lien type. A judgment lien can be powerful and still sit behind a first mortgage, tax obligations, and other earlier encumbrances.

That is why a creditor should never confuse a recorded lien with guaranteed recovery. If senior liens consume all available equity, the judgment lien may pressure the debtor but produce little from a forced sale.

A quick title-oriented review before aggressive enforcement should answer at least these questions:

| Question | Why it matters |

|---|---|

| Is there a mortgage ahead of the judgment lien | Senior debt may absorb sale proceeds |

| Are there tax claims or municipal liens | Some liens outrank nearly everything |

| How much equity appears available | Little equity means weak foreclosure economics |

| Is there a pending sale or refinance | That can create immediate settlement leverage |

A lien with no equity behind it may still create negotiation value, but it is not the same asset as a lien backed by salable property.

The pressure point is often the closing table

Many debtors ignore collection letters for months and then suddenly become responsive when a title search reveals the lien. That reaction is common because real estate transactions run on deadlines. Buyers lock rates, sellers schedule moves, and lenders issue commitment letters with conditions. A lingering lien can stall the entire deal.

This is part of why liens matter so much in consumer and commercial credit risk. According to the LexisNexis Risk Solutions liens and judgments report, 14.3 million people in the U.S. have a lien or judgment on file within the past 7 years, and consumers with that history are 1.7 times more likely to default on future debts. For creditors and lenders, that reinforces what title and collections practice already shows. Liens don't just reflect old disputes. They affect present transactions and future credit decisions.

Why many sales get delayed rather than killed

In practice, most lien-affected real estate matters don't end with a dramatic foreclosure fight. They end in one of four ways:

- Full payoff at closing: The cleanest outcome. Proceeds satisfy the lien and the creditor releases it.

- Negotiated reduction: The creditor accepts less than the full balance to avoid delay or because equity is limited.

- Escrow holdback: Funds are held while a dispute over amount, priority, or documentation gets resolved.

- Failed deal: The parties can't clear title in time, and the transaction collapses.

For homeowners trying to understand the seller-side pressure, practical consumer-facing guidance like Property Nation's advice for lien-affected homeowners can help frame the title and sale issues in plain language.

If the property is already in distress or tied to foreclosure proceedings, related title complications become even more pronounced. Those issues are discussed further in liens on foreclosures.

Removing or Challenging a Judgment Lien

A property owner who discovers a judgment lien usually wants the same thing. Get it off the title as fast as possible. The right path depends on whether the lien is valid, whether the debt can be resolved, and whether the property has enough protected equity to limit enforcement.

Option one pays the debt and demands a release

The cleanest solution is full payment. Once the judgment is satisfied, the creditor should execute and record the proper release documentation so the land records no longer show an active lien.

That sounds simple, but the paperwork matters. Paying without obtaining a clear release can leave a title issue hanging around longer than it should. Debtors should insist on documented satisfaction and confirm that the release is recorded where the lien was filed.

Option two negotiates around the problem

A negotiated resolution is common, especially when a sale is pending or equity is limited. Creditors may accept a reduced lump-sum payment to avoid delay, litigation expense, or uncertainty about actual recovery. Debtors often prefer that route because it clears title faster than a contested court proceeding.

A comparison helps:

| Approach | Main advantage | Main drawback |

|---|---|---|

| Pay in full | Clears the issue cleanly | Requires full funds now |

| Negotiate settlement | May reduce total payout | Creditor doesn't have to agree |

| Payment plan with conditional release | Can preserve a transaction | Terms must be drafted carefully |

| Challenge the lien in court | Can eliminate an invalid lien | Costs time and money |

For property owners trying to address liens before listing or closing, more general consumer guidance such as Buys Houses' piece on addressing liens before selling can be useful as a practical checklist, even though local law always controls.

Option three attacks the lien itself

Not every judgment lien is valid. Debtors should look at both the underlying judgment and the recording process.

Potential challenge points may include:

- Defective original service: If the court never acquired proper jurisdiction, the judgment itself may be vulnerable.

- Recording errors: An improperly prepared or improperly indexed lien can create serious enforceability issues.

- Expiration problems: A creditor who misses a deadline may lose the benefit of the lien.

- Wrong property or wrong debtor: Similar names and title mistakes create real problems in practice.

A challenge should be deliberate, not reflexive. Some objections are strong. Others only irritate the creditor while increasing fees.

Option four evaluates exemptions and bankruptcy issues

Even a properly recorded lien may face limits. As Anthem Law explains in its discussion of real estate liens and exemptions, homestead exemptions can protect part of the debtor's primary-residence equity from forced liquidation, and ownership structure can materially affect whether a lien attaches at all. The same source notes that in some states, a judgment against only one spouse may not create a valid lien against property owned jointly as tenants by the entirety.

That doesn't answer every Connecticut question, but it highlights the right analytical approach. Before assuming a lien can be enforced through sale pressure or foreclosure, examine the equity, exemption issues, and title vesting.

Bankruptcy may also alter the picture. In some cases, a debtor can seek to avoid a judgment lien that impairs an exemption. That is highly fact-specific and should never be treated as automatic.

If you're dealing with timing issues tied to duration or enforceability, it also helps to review how long a judgment lasts, because expiration and renewal questions often affect both creditor power and debtor defenses.

Next Steps for Creditors and Business Owners

A judgment lien on real estate is powerful because it sits at the intersection of litigation, title, and timing. It is not always the first remedy to use, and it is rarely the only one worth considering. But when the debtor owns real property, it is often the tool that changes the case from ignored judgment to active resolution.

For creditors deciding whether to record

Start with discipline, not momentum. Creditors often waste money by recording liens against property that lacks sufficient equity, is exempt, misidentified, or strategically unimportant.

A better approach is to ask the hard questions first:

Where is the debtor's real estate located

In Connecticut, that means identifying the right municipalities for land record filing.Is there enough equity to justify the effort

A lien on paper is one thing. Recoverable value is another.Will title pressure likely produce payment

A debtor trying to refinance next month is different from a debtor sitting on vacant property with no transactions pending.Are other remedies moving in parallel

Bank executions, discovery, and settlement pressure often work better when combined with lien strategy.

For lenders and national creditors

Multi-state enforcement complicates lien management quickly. The timing rules, renewal periods, and interest rules don't line up neatly from one jurisdiction to another. As reflected in the Texas State Law Library's discussion of judgment lien timing and state differences, creditors managing property interests across states may face different durations and related enforcement variables, including examples such as Texas at 10 years and Maryland at 12 years with a 10% judgment interest rate.

That is where portfolio management matters. A creditor with assets to chase in several states shouldn't treat judgment liens as one-time filings. They need a calendar, monitoring process, and state-specific renewal plan.

The creditor who records once and forgets about the file often loses leverage at the moment it should have matured into payment.

For debtors and business owners facing a lien

Ignoring the problem is usually the most expensive option. A recorded lien tends to surface at crucial junctures, during a closing, refinance, acquisition, investor review, or title update. By then, deadlines compress and negotiating power narrows.

If a business owner or homeowner is trying to understand the practical side of clearing title, broad overviews like DIL Group Buyers' help for homeowners facing liens can help frame the options before getting local legal advice.

Three moves usually make sense early:

Verify the lien details

Check the judgment, recording information, property description, and debtor identity.Assess whether the lien is enforceable

Exemptions, ownership structure, equity, and deadlines all matter.Open a negotiation before a transaction deadline hits

A creditor is often more flexible before a closing crisis than during one.

The practical takeaway

For creditors, the value of a judgment lien on real estate is a significant advantage backed by public records. For debtors, the risk is that a problem left alone becomes a title barrier at exactly the wrong time.

Handled properly, a lien can secure a real path to collection. Handled poorly, it can become a wasted filing or a preventable title dispute. The difference is almost always in the details.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.