A business owner often learns about corporate resolutions at the worst possible moment. The loan package is ready. The lease terms are negotiated. The bank account should be opened that afternoon. Then someone across the table says they need a certified corporate resolution before they can proceed.

That request feels technical, but it isn't minor. It goes to a basic legal question. Who, exactly, had authority to bind the company?

If you've been asking what is a corporate resolution document, the short answer is this: it's the corporation's formal written record that a decision was properly approved and that specific people are authorized to carry it out. In practice, that document can decide whether a bank funds a transaction, whether a deal closes on time, and whether the company can defend itself later if the decision is challenged.

For Connecticut companies, the issue isn't just corporate housekeeping. It affects financing, governance, litigation posture, and collections risk. It also matters to lenders, investors, and financial professionals who need confidence that a transaction was authorized by the company itself, not just by a person with a title.

Your Bank Is Asking for What? An Introduction

A common scenario looks like this. A closely held corporation has outgrown its current office. The owners find a new location, negotiate favorable terms, and line up financing. Everyone is moving quickly until the bank asks for a certified resolution authorizing the account, the borrowing, and the individuals permitted to sign.

The owners are confused because they already agreed internally. One of them is the president. Another has always handled operations. From their perspective, the business made the decision days ago.

From the bank's perspective, none of that is enough.

Internal agreement isn't the same as corporate action

A corporation is a separate legal entity. That means the company doesn't act because an owner says it has acted. The company acts through legally recognized procedures, usually through its board, shareholders when required, and properly documented approvals.

A corporate resolution is the formal legal document that records specific binding decisions approved by a corporation's board of directors, shareholders, officers, or managers, and it is maintained in the minute book to support governance compliance and protect the corporate veil, as described by Mosey's discussion of corporate resolutions.

That distinction becomes very real when another party needs proof. Banks want it. Lenders want it. Counterparties in commercial deals want it. So do auditors, buyers in due diligence, and lawyers in litigation.

A title alone doesn't answer the authority question. The resolution is often the document that does.

Why this catches business owners off guard

Most business owners focus on operations first. They build revenue, hire staff, manage customers, and solve practical problems. Corporate records don't feel urgent until a transaction depends on them.

That's why resolution issues usually surface in one of these moments:

- A financing event when a bank wants proof that borrowing was approved.

- A real estate deal when a landlord or seller wants confirmation of signing authority.

- A dispute when someone claims an officer acted without authorization.

- A diligence review when a buyer or investor asks for the company's minute book.

If the records are incomplete, the problem isn't abstract. Closings get delayed. Counterparties lose confidence. Lawyers have to reconstruct approvals after the fact, which is always less clean than doing it correctly at the outset.

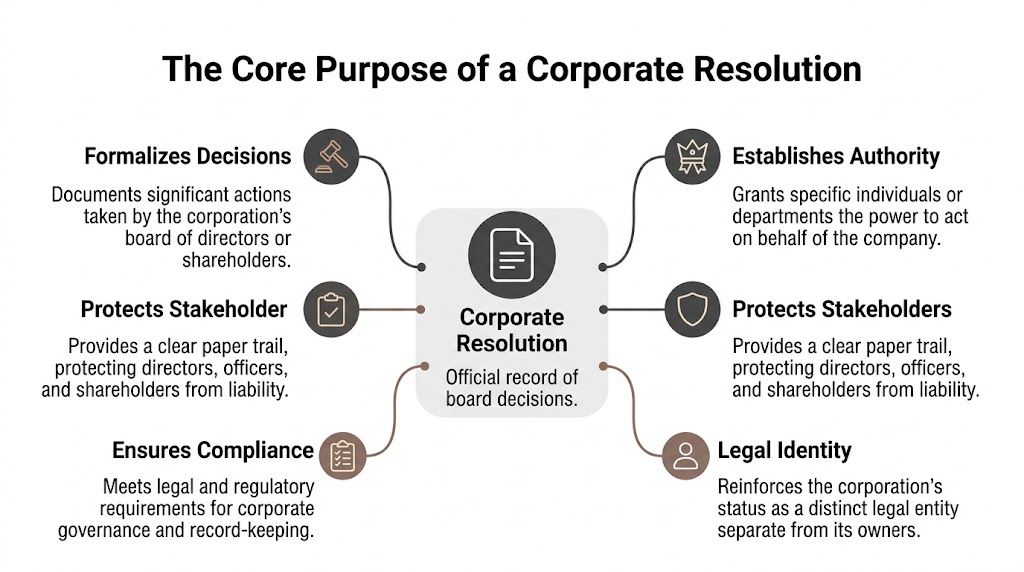

The Core Purpose of a Corporate Resolution

A corporate resolution gives a transaction a clean legal foundation. It shows that the corporation, acting through the right decision-makers, approved a specific course of action and gave defined authority to carry it out.

The corporation needs a documented act, not an assumption

Connecticut business owners often hear some version of this after a dispute starts: "Who approved this?" A signed contract or loan package may show who put pen to paper, but it does not always prove that the corporation authorized the act in the first place.

That gap matters.

A corporation exists separately from its shareholders, directors, and officers. To preserve that separateness, the company needs a formal record showing that the entity made the decision through the proper channel. A resolution supplies that record. It ties the action to board approval, shareholder approval, or other required corporate approval under the governing documents and applicable law.

The minute book works as the corporation's permanent record of those acts. If counsel, a lender, an auditor, or a Connecticut court later needs to examine authority, the resolution is often one of the first documents reviewed. A broader discussion of board structure, officer roles, and internal controls appears in this overview of corporate governance.

What a resolution actually does

A properly drafted resolution usually performs several jobs at once:

- Confirms approval. It shows that the required corporate body approved a defined action.

- States the scope of authority. It identifies who may sign, borrow, sell, settle, or otherwise act for the corporation.

- Creates evidence. It preserves a dated record of what was authorized and on what terms.

- Supports corporate separateness. It helps show that the business is being run as a corporation, not as an owner's informal extension.

In practice, those functions become most important when someone is challenging the corporation's conduct. Creditors examine resolutions when they evaluate whether a debt was properly incurred. Opposing counsel examines them when authority is disputed. Courts examine them when the facts suggest sloppy governance, backdated approvals, or commingling between the company and its owners.

Why this matters in litigation and creditors' rights disputes

Many articles stop at "the bank needs this form." That is only part of the story.

In litigation, a resolution can help establish that a contract, guaranty, borrowing, settlement, or asset transfer was validly authorized. In a collection case, it can support the enforceability of the underlying obligation and reduce room for an authority defense. In a veil-piercing claim, clean resolutions and complete records help show that the corporation observed formalities and operated as a real entity with its own decision-making process.

Poor documentation creates the opposite inference. If the file contains only vague minutes, unsigned notes, or a title with no matching approval, the corporation may have a harder time proving authority. That can complicate enforcement, delay recovery, and give an adversary another argument to use.

| Question a resolution answers | Why lawyers, lenders, and courts care |

|---|---|

| Who approved the action? | Confirms the proper corporate actor approved it |

| What was authorized? | Limits later disputes about scope |

| When was it approved? | Establishes timing and sequence |

| Who could implement it? | Supports the signer or officer's authority |

| Were formalities followed? | Helps defend against alter ego and governance attacks |

At Kons Law, this is often where the practical trade-off becomes clear. Spending a little time to approve and record a transaction correctly is far less expensive than reconstructing authority after a default, lawsuit, or closing problem.

Practical rule: If a transaction could later be enforced, challenged, audited, or scrutinized in court, the corporation should have a written resolution that matches the action actually taken.

Specificity matters. "Financing discussed" does not authorize a particular loan. "Officer approved to sign" may be too vague if the deal involves a major asset sale, a line of credit, or litigation settlement authority. The better practice is to identify the transaction, the parties, the approved terms or limits, and the person authorized to act.

When Your Corporation Absolutely Needs a Resolution

The safest approach is to assume that any material action taken in the corporation's name should be checked for formal approval requirements before anyone signs. Businesses get into trouble when they decide first and document later.

Annual formalities are not optional

All U.S. corporations are legally required to hold annual meetings and document resolutions in their records, and the Sarbanes-Oxley Act of 2002 intensified board approval requirements for public companies, affecting over 4,000 publicly traded firms, as explained by Northwest Registered Agent's corporate resolution overview.

Even if your company is privately held, the broader lesson is straightforward. Formal approvals are part of doing business through a corporation.

Transactions that commonly require a resolution

Some events trigger requests for resolutions so frequently that they should be anticipated rather than treated as surprises.

- Opening or closing a bank account. Financial institutions want confirmation that the corporation approved the account and designated authorized signers.

- Borrowing money. A lender will usually require approval of the debt itself, the loan documents, and the people authorized to sign and deliver them.

- Entering a major lease. Commercial landlords often want assurance that the person signing has corporate authority.

- Buying or selling significant assets. Real estate purchases and other important acquisitions should be tied to a specific approval.

- Issuing stock or changing ownership structure. Equity moves affect control and economics, so they shouldn't happen informally.

- Appointing or removing officers. Titles matter less than documented authorization. The resolution helps establish both.

- Electing directors or filling vacancies. Governance changes belong in the formal record.

- Amending bylaws. Internal governing rules should be updated through proper procedure, not by custom or assumption.

- Approving a merger or acquisition. These transactions draw close scrutiny in diligence and often require multiple layers of approval.

- Authorizing contract signers. If someone will execute recurring agreements on behalf of the corporation, the company should define that authority clearly.

Where businesses make avoidable mistakes

The most common mistake is overreliance on custom. A founder says, "I've always signed these documents." That may be true. It still doesn't answer whether the company formally authorized the action.

Another problem is using one resolution for every situation. Counterparties often reject generic forms because they don't identify the transaction with enough precision.

What works better is matching the document to the event:

| Business event | Better practice |

|---|---|

| New bank account | Resolution naming the bank and signers |

| Term loan or line of credit | Resolution approving debt and execution authority |

| Real estate lease | Resolution approving lease terms and signer |

| Officer appointment | Resolution naming title, role, and effective date |

Banks and counterparties don't ask for resolutions to create inconvenience. They ask because they need proof that the company itself approved the transaction.

For Connecticut businesses, that planning mindset saves time. Before the company applies for financing, signs a lease, changes leadership, or closes a significant contract, someone should ask a simple question: has the corporation authorized this in writing?

Anatomy of a Corporate Resolution Document

A corporate resolution isn't complicated once you know what each part is doing. The document follows a predictable structure, and each section serves a legal function.

Corporate resolutions must be adopted through a board vote at a meeting with a quorum, typically a simple majority, and their standard structure includes a heading, whereas recitals, and resolved clauses, as described in Indeed's explanation of corporate resolutions.

The heading and identifying information

The heading should identify the company clearly. That usually means the full legal name of the corporation and a title that tells the reader what the document is.

Examples include:

- Resolution of ABC Manufacturing, Inc.

- Board Resolution Authorizing Commercial Loan

- Unanimous Written Consent of the Board of Directors of XYZ Holdings, Inc.

The opening also usually includes the date. If the action was taken at a meeting, the meeting date matters. If the action was taken by written consent, the effective date should be clear.

The whereas clauses

The whereas clauses are the recitals. They provide context.

They answer questions like:

- Why is the corporation acting?

- What transaction is under consideration?

- What background facts support the action?

These clauses don't authorize anything by themselves. They set the stage so the operative language that follows makes sense.

A recital for a financing matter might note that the company seeks a line of credit for working capital and that a lender requires formal authorization. A recital for a lease might identify the premises and the business purpose for occupying them.

The resolved clauses

This is the heart of the document. The resolved clauses state the action being approved.

The language should be specific. Broad wording creates risk because it can leave room for argument over what was authorized.

A strong resolved clause usually addresses:

- The transaction or decision being approved

- The person or persons authorized to act

- Any limits on authority

- Any supporting documents they may execute

- The effective date, if needed

Approval language should track the real transaction. If the company is borrowing from a named bank, the resolution should identify the lender and the type of borrowing.

A sample excerpt

RESOLVED, that the Corporation is authorized to obtain financing from the proposed lender on terms approved by the authorized officer; and

RESOLVED FURTHER, that the President and Treasurer are each authorized to negotiate, execute, and deliver the loan agreement, promissory note, security documents, and related certificates on behalf of the Corporation; and

RESOLVED FURTHER, that all prior actions taken consistent with these resolutions are ratified and approved.

That language is only a sample. Real drafting should fit the transaction, the bylaws, and the company's governance structure.

Adoption language and signatures

A resolution also needs to show that it was adopted. That usually appears as a statement that the measure was approved unanimously or by the required vote.

The certification piece matters. Someone, often the secretary or another authorized officer, may need to certify that the resolution was duly adopted and remains in effect. That certification is often what the bank or counterparty relies on.

If your company structure is more complex and overlaps with officer roles used in other entities, a practical reference point is this discussion of limited liability company officers, especially when businesses operate several affiliated entities and need clarity about who holds which authority in which entity.

Quick reference table

| Component | Purpose |

|---|---|

| Heading | Identifies the corporation and nature of the action |

| Date | Fixes when the action was taken or became effective |

| Whereas clauses | Provides background and business context |

| Resolved clauses | States the decision and grants authority |

| Voting statement | Shows the approval met procedural requirements |

| Signature or certification block | Confirms authenticity and allows third parties to rely on the document |

What doesn't work is borrowing a template and filling in only half the facts. Resolutions fail when they are generic, internally inconsistent, or disconnected from the governing documents. The cleaner approach is to draft the record the way an outsider would need to read it later, without guessing.

The Approval Process Under Connecticut Law

A lender asks for a board resolution before closing. The company sends a signed page, but the minute book does not show who approved it, whether a quorum was present, or whether the signer still held office on that date. In a routine transaction, that may cause delay. In litigation or a collection action, it creates a real argument that the corporation never authorized the act at all.

Start with the governing documents

Under Connecticut practice, the approval process starts with the corporation's own records. The certificate of incorporation, bylaws, and any existing shareholder agreements usually answer the first questions that matter: who has authority to approve the action, what notice is required, whether directors may act by written consent, and what vote is needed.

That review should happen before anyone signs the resolution.

State law sets the outer rules. The bylaws usually control the mechanics. If those two do not line up cleanly, the corporation should address that conflict before relying on the resolution for a loan, major contract, asset sale, or officer appointment. For businesses sorting out when internal approval is enough and when a state filing is also required, this guide on how to amend articles of organization helps clarify the distinction across entity types.

Meeting procedure and quorum

If the board acts at a meeting, the record should show proper notice, attendance, quorum, the motion presented, and the vote taken. Those points sound procedural because they are procedural. They are also the first points examined when a bank, trustee, judgment creditor, or opposing counsel tests the corporation's authority.

Connecticut companies often get into trouble here by treating minutes as an afterthought. A one-page resolution attached to incomplete minutes leaves gaps. Those gaps matter later. If the file does not show that the directors were properly convened and authorized to act, the corporation may have a harder time proving the transaction was valid, and a creditor may have a harder time enforcing it.

That is one reason I advise clients to draft the minutes and the resolution as a matched set.

Written consent can be the better option

Many closely held corporations do not need a formal meeting for every approval. If the bylaws and applicable law permit action by written consent, unanimous written consent is often the cleaner record.

It works well when timing is short, the directors already agree, or the action is narrow and concrete, such as opening a bank account, authorizing a specific borrowing, or appointing an officer. It is less effective when the board needs discussion, disclosures must be aired, or the company anticipates future conflict among owners. In those situations, a real meeting and fuller minutes usually create the better record.

Drafting speed should not come at the expense of proof. Some companies use document automation software to standardize approvals, which can help with consistency, but the final document still has to match the corporation's actual governance requirements and the facts of the transaction.

Roles at adoption

The chair or presiding director runs the meeting. The secretary, or another proper officer, records what happened and certifies the corporate record when needed. Those jobs become important when a dispute turns on whether authority existed on a specific date.

In Connecticut litigation, that issue appears more often than business owners expect. A clean approval record helps show the corporation acted as a separate legal entity with observed formalities. A thin or inconsistent record gives an opponent room to argue the opposite, especially in veil-piercing disputes or cases involving contested debts.

The best approval process is disciplined and boring. That is the point. If a stranger had to read the file three years later in a courtroom or a workout negotiation, the file should answer the authority question without guesswork.

Legal Stakes and Preservation Best Practices

Corporate resolutions become most important when things go wrong. That is why they deserve more attention in litigation and creditors' rights work than they usually get.

Missing records create leverage for the other side

Existing commentary often misses the collections angle, but it matters. Poor record-keeping contributed to 25% of veil-piercing cases in U.S. state courts from 2010 to 2020, and missing resolutions can invalidate creditor claims in litigation and regulatory disputes, as noted in Eques Law's discussion of corporate resolutions and creditors' rights.

For a business owner, that means informal governance can threaten the liability shield. For a creditor, it means missing approvals can complicate enforcement, especially when the debtor claims the transaction was never properly authorized.

What preservation actually looks like

A useful recordkeeping system isn't elaborate. It is disciplined.

- Keep a current minute book. Maintain signed resolutions with related minutes and certifications.

- Match records to transactions. If the company signs a loan, lease, or major contract, the approval record should be easy to locate.

- Use consistent naming. File by entity name, transaction type, and date so the right document can be retrieved quickly.

- Store digital copies securely. Many companies use board portals, document management systems, or document automation software to standardize forms and reduce drafting errors.

- Review authority periodically. Signatory changes, officer turnover, and ownership shifts can leave old resolutions outdated.

What works and what doesn't

What works is proactive governance. Draft the resolution before the closing. Confirm the bylaws. Make sure the certification matches the final documents.

What doesn't work is assembling records only after a dispute starts. By then, opposing counsel, an auditor, or a lender may already see the gaps.

This is also the point where legal counsel can add real value. Some businesses handle routine resolutions internally. Others need help when authority is disputed, records are incomplete, or the issue intersects with financing, collections, or litigation. For companies weighing whether to handle those matters internally or externally, this explanation of corporate counsel provides a practical frame.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Frequently Asked Questions About Corporate Resolutions

Is a corporate resolution the same as meeting minutes

No. Minutes record what occurred at a meeting. A resolution records the formal decision that was adopted. Sometimes the resolution appears within the minutes. Sometimes it is attached as a separate document. The important point is that the approval itself must be clear.

Do small Connecticut corporations really need them

Yes. Closely held corporations often assume informal agreement is enough because the owners know each other and make decisions quickly. That approach becomes risky when a bank, investor, buyer, court, or creditor asks for proof of authority.

Can a corporation approve a resolution without holding a meeting

Often yes, if the governing documents and applicable law allow action by unanimous written consent. That method can be efficient, but it still requires proper documentation and signatures.

Are LLCs required to use corporate resolutions

An LLC is a different entity type, so the rules aren't identical. Still, LLCs often use similar written approvals for major actions because lenders, counterparties, and investors want the same clarity about authority.

How specific should a resolution be

Specific enough that an outsider can tell what was approved and who may act. Vague language causes problems. The cleaner practice is to identify the transaction, the authorized signer, and any practical limits on authority.

Who usually signs the document

That depends on the corporation's structure and the purpose of the document. Often a secretary or other officer certifies that the resolution was duly adopted. For transaction use, the certifying signature matters because the third party is relying on it.

If your company needs help with governance records, transaction authority, internal approvals, or a dispute involving challenged corporate action, Kons Law advises Connecticut businesses, lenders, and financial professionals on the legal and practical side of getting these issues right. To discuss your matter, call (860) 920-5181.