When you’re buying a business, due diligence is your chance to look under the hood. It's the critical investigation you conduct to verify everything the seller has told you—from their financial health and legal standing to their day-to-day operations. This isn't just about ticking boxes; it's about making sure you don't inherit costly surprises after the deal is done.

Laying the Groundwork for a Successful Diligence Process

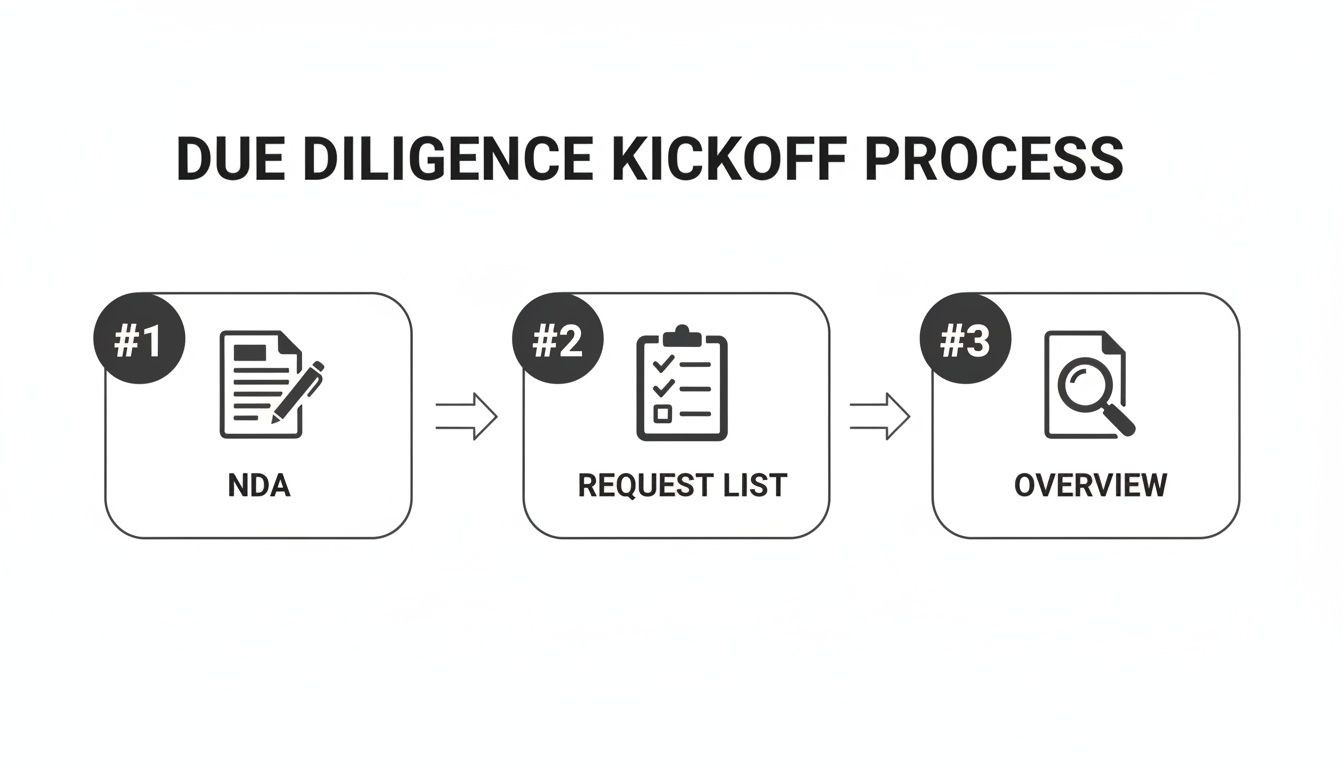

A successful acquisition is built on a solid foundation, and that foundation is laid long before you see the first P&L statement. Getting this initial stage right is about more than just gathering documents. It's about setting up a strategic framework to protect your investment from the very beginning.

The first real step is executing a strong Non-Disclosure Agreement (NDA). This is a non-negotiable. An NDA is a legally binding contract that protects the seller’s sensitive information—customer lists, financials, trade secrets—that they're about to share with you. No serious seller will open their books without one, and it establishes a professional tone for the entire negotiation.

Creating Your Due Diligence Request List

With the NDA signed, your next move is to draft a comprehensive due diligence request list. This is the formal document you’ll send to the seller that outlines every single piece of information you need to review. Think of it as your investigative roadmap, meticulously organized to ensure nothing gets missed.

This list is what turns your abstract goal of "due diligence" into a concrete set of tasks. It guides the seller on what to provide and when. We typically structure these requests to cover all critical aspects of the business, as a well-organized kickoff is the best way to avoid expensive mistakes down the road.

The process really does follow a logical sequence: secure the information with an NDA, demand it with a structured request list, and then begin your high-level review.

Core Due Diligence Focus Areas at a Glance

To make your request list effective, it's helpful to categorize your investigation. Here is a simplified look at the main areas we focus on when guiding clients through an acquisition.

| Category | Objective | Key Documents to Review |

|---|---|---|

| Financial | Verify the company's financial health and profitability. | 3-5 years of tax returns, P&L statements, balance sheets, cash flow statements, accounts receivable/payable aging reports. |

| Legal | Identify any legal risks, liabilities, or compliance gaps. | Corporate formation documents, bylaws, shareholder agreements, business licenses, permits, litigation records, key contracts. |

| Operations | Understand how the business runs day-to-day and assess its operational risks. | Employee records, organizational charts, key customer and supplier contracts, intellectual property documentation (patents, trademarks), inventory records. |

This table provides a starting point, but a thorough request list will be far more detailed, tailored specifically to the target company and its industry.

The Importance of a Structured Approach

Starting with an organized, methodical approach does more than just make the process efficient. It sends a clear signal to the seller that you are a serious, professional buyer. We often see that a buyer's level of preparation directly influences the seller's cooperation.

A crucial part of this is establishing a secure virtual M&A Data Room where all documents are uploaded and managed. This keeps everything organized, tracked, and protected. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

A well-crafted due diligence request list does more than just gather documents. It forces the seller to get their own house in order, and any disorganization or gaps that appear are, in themselves, a critical piece of information for you as the buyer.

This preliminary work sets the stage for a much deeper investigation. For more information on the document that often precedes this stage, you might be interested in our guide on what is a letter of intent.

A Deep Dive into the Financial and Legal Details

Once the initial groundwork is complete, it's time to roll up our sleeves. This is where the core of your buying a business due diligence really begins, focusing on the two pillars of any healthy company: its financial records and its legal standing. This isn't just a quick review; we're conducting a forensic-level examination to see if the reality matches the seller’s claims.

We always start with the financials. A single profit and loss statement simply won't cut it. You need to see a minimum of three to five years of complete tax returns, audited financial statements (if they exist), and the company's internal bookkeeping. Looking at the business over a longer period helps us identify trends, flag inconsistencies, and understand its true performance beyond any one-off good years.

Scrutinizing the Financials

The top-line numbers can be deceptive. The real story is always found in the details. For instance, don't just accept a total accounts receivable figure at face value. We need to request an accounts receivable aging report. This document is critical because it tells us who owes money and, more importantly, how long those debts have been outstanding.

A large number of accounts over 90 days past due is a serious red flag, pointing to collection issues or even customer disputes. Likewise, we need to dig into how inventory is valued. Is it a standard method like FIFO or LIFO, or is the company using a creative valuation to hide obsolete stock? The goal is to trace actual cash flow, not just reported profits, to find the company’s true financial pulse.

- Tax Returns vs. Financial Statements: We’ll compare federal and state tax returns against the company's internal books. Any significant gaps can be a sign of aggressive accounting or, in worst-case scenarios, fraud.

- Debt and Liabilities: You'll need a detailed schedule of every debt the company holds, from bank loans to lines of credit. We must understand the interest rates, payment terms, and any "change-of-control" clauses that could be triggered by your purchase.

- Customer Concentration: We analyze sales records to see what percentage of revenue comes from their top customers. If a few clients make up the bulk of the business, losing just one of them after you take over could be catastrophic.

Uncovering Hidden Legal Exposures

Running parallel to our financial review is an equally important legal investigation. A business that seems financially sound can quickly become a liability trap if it's mired in legal problems. A key part of our job is to perform thorough legal due diligence to protect you from inheriting someone else’s mess.

Our legal review begins with the company's formation documents—the articles of incorporation, bylaws, and shareholder minutes. These documents confirm that the company is in good standing with the state and that the seller actually has the authority to sell it.

We also have to verify who owns the intellectual property (IP). This means ensuring trademarks are properly registered, patents are valid, and any proprietary software or trade secrets belong to the company itself—not a founder or a former employee. Any ambiguity here puts the company’s core value at risk.

A business's legal health is defined not just by the lawsuits it's facing, but by the ones it isn't. A lack of clear contracts, proper corporate governance, or IP protection is a ticking time bomb, waiting to become future litigation.

Finally, we have to meticulously examine all material contracts. This isn't just about a quick read-through; it's about understanding precisely how these agreements will impact you as the new owner.

Key Contractual Considerations:

- Transferability: Do key customer and vendor contracts have assignment clauses that require consent before they can be transferred to you? This is a classic "gotcha" that can bring a business to a halt right after you buy it.

- Employee Agreements: We need to see all employment contracts, especially non-compete and non-solicitation agreements. Are the key people who run the business locked in, or can they walk out the door—and take clients with them—the day after closing?

- Leases and Loans: Real estate leases and loan agreements often contain "change of control" provisions. These can trigger an automatic default or give the landlord or lender the right to terminate the agreement simply because the business was sold.

This deep dive is all about painting an accurate, unvarnished picture of the company’s real-world financial and legal health before you sign on the dotted line. To get more comfortable with the numbers, take a look at our guide on how to read a balance sheet.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Evaluating Daily Operations and Human Capital

Financial statements and legal documents show you where a business has been, but they don't always reveal where it's going. The real value—and risk—of an acquisition often lies in the company's day-to-day operations, its internal systems, and, most critically, its people. A core part of your buying a business due diligence is getting under the hood to see how the engine actually runs.

The numbers on a spreadsheet are just the output. What you're really buying are the systems and people that produce those numbers. Are the sales processes effective? Is the technology holding the business back? Answering these questions gives you a clear-eyed view of the company you will inherit on day one.

The Human Element: People, Culture, and Key Dependencies

A business is nothing without its team. Understanding the workforce is absolutely essential, as a revolving door of employees, poor morale, or an over-reliance on one or two key people can sink an otherwise healthy company after you take over.

If the seller agrees, you may get the chance to speak with key employees. These aren’t interrogations. They are your chance to get a feel for the company culture and identify who is truly indispensable. You need to know who runs the most important client relationships, who keeps the operations running smoothly, and who holds decades of institutional knowledge. The unexpected departure of even one of these individuals can have a serious impact on your investment.

- Employee Roster: Get a full list of employees with their positions, salaries, and start dates. This helps map out the organizational chart and compensation structure.

- Key Personnel: Who are the top performers and decision-makers? Crucially, are they bound by strong employment agreements, or could they walk out the door the day after the closing?

- Culture and Morale: Look for red flags like high turnover rates or unresolved employee disputes. These are often symptoms of deeper operational problems.

A detailed review of employment contracts and company policies is non-negotiable. Our guide on employment agreement review provides more specific insight on what to look for in these vital documents.

Uncovering Risky Operational Dependencies

Beyond the team itself, you must dig into the company’s relationships with its customers and suppliers. A common mistake we see is a buyer failing to recognize the risk of concentration.

For example, discovering that 50% of the company's annual revenue comes from a single customer should set off alarm bells. You have to find out if that relationship is secured by a long-term contract or if it's based on a personal friendship with the current owner. If it's the latter, that revenue could evaporate the moment you take possession.

The strongest businesses are built on a diversified foundation. A broad customer base, multiple supplier options, and a well-cross-trained team are the signs of an operation built to last—not one balanced precariously on a few key relationships.

The same principle applies to the supply chain. If the business relies on a single, exclusive vendor for a critical part or material, you are completely exposed. Any price hike, quality control issue, or business failure on their end becomes your problem overnight.

Technology and Physical Asset Condition

Your operational due diligence must also include a practical review of the company's physical and digital assets. This is about more than just checking a list of equipment off a spreadsheet; it’s about assessing its true condition and fitness for purpose.

Key areas for inspection include:

- Physical Assets: You need to physically inspect major equipment, machinery, and the facility itself. Is everything well-maintained, or are you walking into immediate and expensive repair bills?

- Technology Stack: Review all the software, IT infrastructure, and digital systems. Are licenses current and legitimate? Is the technology secure and efficient, or is it an outdated mess that will stifle growth?

- Sales and Marketing Channels: Analyze exactly how the business finds and converts customers. Dig into the performance of its website, ad campaigns, and social media presence to confirm they are actually generating revenue.

This analysis is vital for creating a realistic post-acquisition budget and uncovering hidden operational strengths or weaknesses. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Identifying Red Flags and Building Your Advisory Team

Knowing when to walk away from a deal is every bit as important as knowing when to close. When you're buying a business, due diligence is your primary defense. It’s not just about confirming the good stuff; it’s about uncovering the red flags that signal a bad investment before it’s too late. Overlooking these warnings can lead to serious financial losses and operational headaches down the road.

You’re not looking for a perfect business—it doesn’t exist. Your real goal is to separate the manageable issues from the fundamental, unfixable flaws. These are the genuine deal-breakers, and they often show up across the company’s finances, operations, and key personnel.

Common Red Flags to Watch For

Some warning signs are glaring, while others are much more subtle. For instance, a seller who seems disorganized or is slow to provide documents might just be overwhelmed. Or, they could be hiding something. The key is to look for patterns of risk that tell a bigger story.

- Chaotic Financial Records: If the books are a mess, you simply can't trust the numbers. Inconsistent reporting, a heavy reliance on undocumented cash transactions, or an inability to produce basic financial reports are all major warning signs.

- Heavy Customer Concentration: Be extremely cautious if you find that one or two clients generate over 40% of the company's revenue. Losing just one of those accounts after the acquisition could cripple the business almost overnight.

- Unexplained Revenue Dips: A sharp or steady decline in sales requires a bulletproof explanation. If the seller gives you vague answers like "market shifts" without any hard data to back it up, that’s not good enough.

- Key People Ready to Exit: You need to know if the core team is staying. If you learn that essential managers, top salespeople, or the lead engineer plan to leave after the sale, you're not buying a functional business. You're buying a shell that could quickly fall apart.

Deciding what's a manageable problem versus a deal-breaker is where experience really counts. A high customer concentration might be managed with a new sales strategy and a solid contract, but an unexplained revenue dip with no good answers is often a reason to walk.

The most dangerous red flags aren't the problems you can see; they're the ones hidden by a seller's reluctance to provide clear information. Resistance itself is data. It tells you exactly where you need to dig deeper.

You Don't Have to Do It Alone

Making these critical judgment calls isn't something you should ever do by yourself. The sheer complexity of a business acquisition requires a team of seasoned advisors. Trying to navigate dense legal contracts, forensic accounting, and operational assessments on your own is a recipe for disaster. Building the right team is one of the most important investments you’ll make.

The need for expert guidance is precisely why due diligence has become such a critical component of any M&A transaction. The growth of the global market for these services shows just how essential this step is for successfully managing risk.

Assembling Your Core Advisory Team

Your advisory team’s job is to translate thousands of data points into a clear ‘go’ or ‘no-go’ recommendation. Each member has a distinct and vital role.

- The Business Attorney: Think of your attorney as the quarterback of the entire due diligence process. They will draft and review the Letter of Intent (LOI), manage the document request list, scrutinize every contract for risks and liabilities, and ultimately draft the definitive purchase agreement that protects your interests.

- The Certified Public Accountant (CPA): Your CPA is your financial detective. They go far beyond just looking at tax returns; they conduct a "quality of earnings" analysis to verify the seller's true cash flow. They’ll dig into the financial statements, assess inventory, confirm accounts receivable, and spot any questionable accounting practices.

- The Industry Consultant (Optional): For businesses in niche or technical fields, an industry-specific consultant can be invaluable. They can assess the condition of specialized equipment, evaluate proprietary technology, or offer insights into market dynamics that a generalist would almost certainly miss.

Delegating effectively is the key to success here. Your attorney manages the legal framework, your CPA validates the numbers, and you can then focus on the big-picture strategic and operational fit. This team approach ensures every stone is turned, protecting you from costly mistakes and giving you the confidence to move forward.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

From Findings to Closing the Deal

As your due diligence investigation wraps up, your focus needs to shift from discovery to decisive action. All that research isn't just a collection of facts anymore—it's the foundation for your final negotiations and the legal framework that will protect your investment.

This is where your careful review of documents, financials, and operations truly pays off. You're turning what you’ve learned into real value at the negotiating table and embedding safeguards directly into the final purchase agreement.

Consolidating Your Findings into a Diligence Report

The first move is to organize everything you and your advisory team have uncovered into a clear, comprehensive diligence report. This isn't just a list of problems. A good report summarizes all significant findings, both positive and negative, giving you a complete picture of the business you’re about to buy.

Think of this report as having two critical jobs. First, it gives you and your partners a bird's-eye view, helping you make that final go/no-go decision with confidence. Second, it becomes the factual basis for any renegotiation with the seller. A well-documented finding is far more powerful than a vague concern.

Your report needs to be specific. It should categorize issues by area—financial, legal, operational—and, wherever possible, put a number on the impact. Instead of just noting "some inventory is old," a strong report would state, "An estimated $50,000 in inventory is obsolete, showing no sales in the past 24 months." That's the kind of detail that drives action.

Leveraging Findings to Renegotiate the Deal

Armed with your diligence report, you can approach the seller from a position of strength and clarity. While not every small issue warrants a price change, significant discrepancies or undisclosed liabilities absolutely do.

You have a few ways to address what you’ve found:

- Purchase Price Reduction: The most direct route. If your diligence uncovers $100,000 in unrecorded liabilities, you have a solid basis to request a dollar-for-dollar reduction in the purchase price.

- Seller Holdback or Escrow: For risks that are still up in the air, like a pending lawsuit, you can require a portion of the purchase price to be held in an escrow account. These funds are set aside to cover a potential loss and are released to the seller only if the risk doesn't come to pass.

- Seller-Financed Adjustments: Did you find that a critical piece of equipment is on its last legs? You can negotiate for the seller to cover the replacement cost or adjust the deal terms to reflect that future expense.

The key is to frame these requests as a direct result of the facts uncovered during diligence, not as last-minute haggling. When you can tie every request back to a specific, documented finding, you maintain a professional and objective position.

The goal of renegotiation isn't about "winning" every point. It's about recalibrating the deal to reflect the business's true condition. A fair deal is one where the price and terms accurately account for the real-world risks you’ve uncovered.

Finalizing the Definitive Purchase Agreement

Once you and the seller agree on the revised terms, it’s your attorney’s turn to translate everything into the definitive purchase agreement. This is the final, legally binding contract that governs the entire transaction. It’s your last and most important line of defense.

The findings from your diligence directly shape the protections we build into this document. For a deeper look into how these agreements are structured, our guide on what is an asset purchase agreement is a great resource.

A critical section of this agreement is the Representations and Warranties ("reps and warranties"). These are legally binding statements of fact made by the seller about the business—for example, that the financial statements are accurate, there is no undisclosed litigation, and all taxes have been paid. If any of these statements prove false later, you have legal recourse to seek damages from the seller even after the deal has closed.

Technology now plays a huge role in verifying these details. An incredible 75% of companies now use technology for compliance monitoring, and up to 81% apply it to customer due diligence, as noted in an in-depth global compliance study from PwC. This shows just how much M&A relies on data-driven risk assessment.

Finally, the agreement must lay out a clear process for obtaining third-party consents. Many vital contracts, such as office leases or major client agreements, contain "anti-assignment" clauses. This means you need formal permission from the other party to transfer the contract to you, the new owner. Failing to manage this process can jeopardize the entire transition.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Answering Your Key Due Diligence Questions

When you're looking to buy a business, due diligence is often the most demanding and uncertain part of the journey. Clients often come to us with similar questions about the timeline, costs, and potential roadblocks. Getting clear answers upfront helps you move forward with confidence.

How Long Does Due Diligence Usually Take?

One of the first things every buyer wants to know is how long this will take. The honest answer from a legal perspective is: it depends entirely on the deal.

For a smaller, less complicated business, we can often complete a thorough review in 30 to 45 days. But for a larger company with intricate operations, multiple locations, or valuable intellectual property, the process can easily take 60 to 90 days, sometimes longer.

Several factors will dictate your timeline:

- The Seller's Organization: This is the biggest variable. A seller who has already compiled documents in a virtual data room can cut weeks off the timeline. A disorganized seller creates delays.

- Business Complexity: A local retail store is far simpler to vet than a manufacturing business with supply chain agreements, environmental regulations, and labor contracts.

- Third-Party Cooperation: We are often waiting on outside parties. The speed at which banks, landlords, or government agencies respond to our requests for information or consent is out of our direct control.

- The Depth of Your Review: A basic financial and legal check is faster than a comprehensive investigation that includes site visits and extensive operational analysis.

While closing quickly is always appealing, remember that diligence is about being thorough, not fast. It is far better to spend an extra week uncovering a critical issue than to close a bad deal and regret it for years.

What Does Due Diligence Typically Cost?

Think of due diligence costs as a direct investment in de-risking your acquisition. The budget will vary based on the size and complexity of the business you're targeting. A good rule of thumb is to expect to spend between 1% to 3% of the transaction value on your advisory team.

For smaller deals under $1 million, these costs might fall in the $10,000 to $30,000 range. For larger, multi-million dollar acquisitions, the fees for a full team of experts can easily surpass $100,000.

Your primary costs will be the professional fees for your core advisors:

- Business Attorney: Your legal counsel handles the review of all contracts, corporate records, and legal compliance, while also drafting the purchase agreement.

- CPA/Accountant: Your accountant is essential for financial due diligence and often a quality of earnings report, which verifies the company's true profitability. This is a critical expense that confirms what you are actually buying.

- Specialized Consultants: Depending on the business, you might need an environmental auditor, an IT security specialist, or other industry-specific experts to evaluate particular risks.

Think of due diligence costs not as an expense, but as an insurance policy. Spending $25,000 to uncover a $200,000 hidden liability is an investment that yields an immediate and substantial return.

What Should I Do if a Seller Is Uncooperative?

An evasive or uncooperative seller is one of the most serious red flags in any transaction. When a seller drags their feet on providing documents, gives vague answers, or refuses to share key information, you have to proceed with extreme caution.

Your first move is to have your attorney send a formal, specific request for the missing items. Sometimes, a direct communication from legal counsel is all it takes. If the resistance continues, it usually means one of two things: the seller is either hiding a major problem or is not truly committed to the sale.

Here is how we advise clients to handle this situation:

- Get Specific: Vague requests get vague answers. Instead of asking for "all contracts," ask for "all signed customer contracts with a value over $5,000 executed between January 1, 2022, and the present." This is much harder to sidestep.

- Focus on the Resistance: A seller’s reluctance is a road map. If they are fighting you on providing financial statements or employee records, that’s exactly where the biggest risks are likely buried.

- Set a Firm Deadline: We can communicate that without certain key documents by a specific date, you will have to pause the diligence process or terminate the Letter of Intent.

- Be Prepared to Walk Away: In the end, you cannot force a seller to be transparent. If they refuse to provide the information you need to make a sound decision, your best move is to walk away. Buying a business based on incomplete information is a recipe for disaster.

Navigating the complexities of buying a business requires expert guidance.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.