So, you've won your lawsuit. That's a huge step, but as any seasoned business owner knows, a court judgment isn't the same as cash in the bank. This is where post-judgment interest comes in, and it’s a concept you absolutely need to grasp.

Think of it this way: post-judgment interest is the fee the debtor pays for the privilege of holding onto your money after a court has officially ordered them to pay up. It’s compensation for the delay.

Why This Is More Than Just a Legal Formality

Getting a judgment is one thing; getting paid is another. The gap between the judge's gavel and the money hitting your account can be frustratingly long. Post-judgment interest isn't just a minor detail—it's a critical tool to protect the real value of your win.

This interest makes you, the judgment creditor, whole again. If the debtor had paid on time, you could have put that capital to work—investing it, clearing other debts, or fueling your business growth. Post-judgment interest accounts for that lost opportunity and fights back against inflation.

The Real-World Power of a Ticking Clock

Beyond just making sure your award doesn't lose value, post-judgment interest lights a fire under the debtor. With every passing day, the amount they owe climbs higher. This creates a powerful financial incentive for them to stop stalling and settle the debt.

This is especially true in a shifting economy. In the U.S. federal system, for instance, the rate is tied to the 1-year Treasury yield. We saw that rate jump from less than 1% to over 4% between 2022 and 2023. On a $1 million judgment, that’s the difference between the debt growing by $10,000 a year versus more than $40,000 a year. Suddenly, dragging their feet becomes a very expensive strategy for the debtor.

Protecting Your Company’s Bottom Line

At the end of the day, actively pursuing post-judgment interest is a core part of safeguarding your company's financial health. It turns that piece of paper from the court into a hard asset that holds its value.

Here’s what it really does for you:

- Preserves Your Win: It acts as a shield against inflation, ensuring the money you're awarded tomorrow has the same buying power it does today.

- Creates Urgency: The constantly growing debt total puts pressure on the debtor to pay up, which can drastically shorten your collection timeline.

- Maximizes Your Recovery: It ensures you get every penny you are legally and financially entitled to, including fair compensation for the wait.

Leaving post-judgment interest on the table is like letting the debtor use your money for free. A proactive approach is the only way to turn that court order into real capital for your business.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Connecticut’s Rules for Interest After Judgment: What You Need to Know

While federal courts play a guessing game with interest rates tied to ever-changing Treasury yields, Connecticut gives creditors and debtors a much clearer, more predictable path. The state has its own set of rules for interest after judgment, and they’re refreshingly straightforward.

This approach brings a welcome stability to the process. There’s no need to constantly check economic indicators or worry about market fluctuations; the rules are set by state law.

The Bedrock: Connecticut General Statutes

The core of Connecticut's post-judgment interest system is found in two key laws: Connecticut General Statutes § 37-3a and § 37-3b. These statutes establish a fixed interest rate, which means the percentage applied to your judgment is locked in. It won’t change, regardless of what the broader economy does tomorrow, next month, or next year.

This fixed rate applies across a wide range of legal victories, giving creditors strong, consistent protection.

- Commercial Litigation: Think of disputes between two businesses.

- Contract Disputes: When someone breaks a signed agreement and a judgment is awarded.

- Personal Injury Awards: Compensation granted to someone who has been injured.

This consistency makes everything from the initial calculation to the final collection effort much simpler. To get a better handle on the state's broader regulations, you can learn more about Connecticut debt collection laws and how they might affect your specific situation.

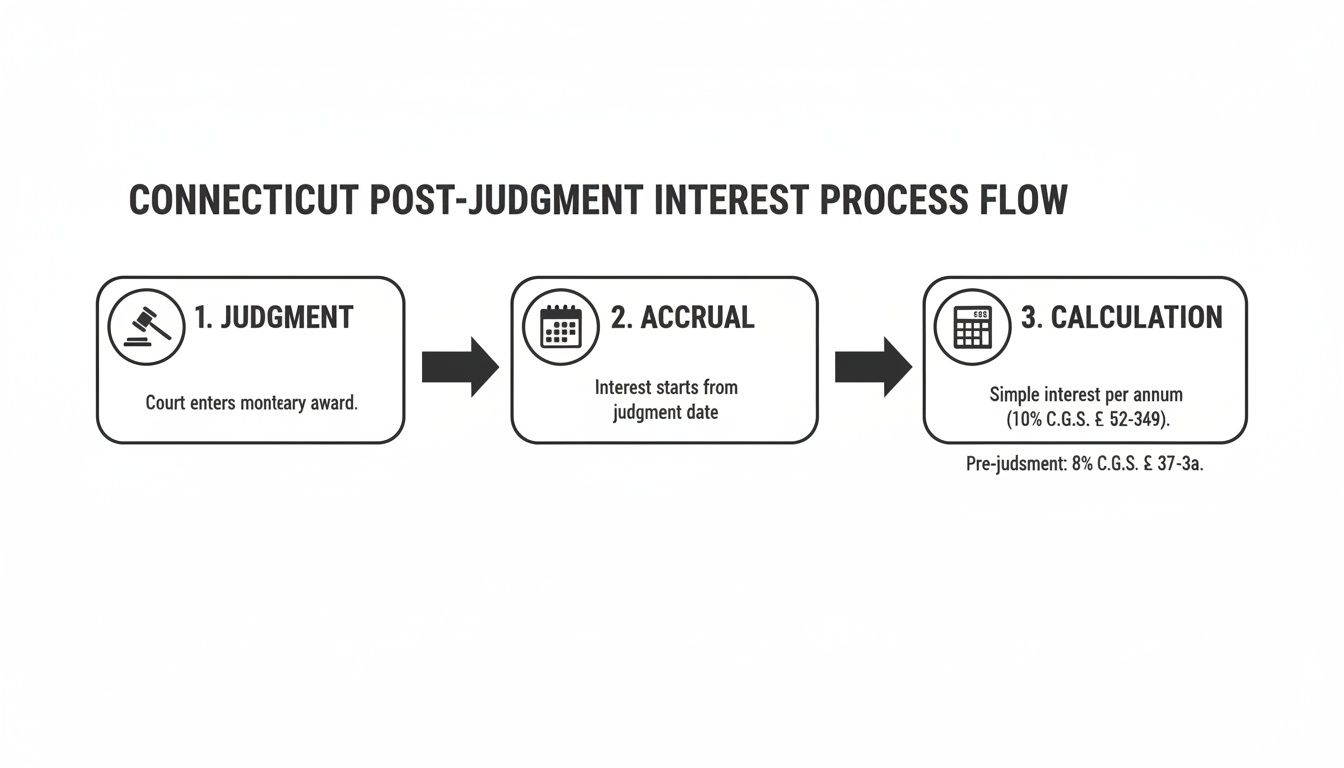

When Does the Interest Clock Start Ticking?

One of the most important concepts here is accrual—a fancy word for the exact moment when interest starts building on the judgment amount. It’s the starting pistol for the financial clock.

In Connecticut, the clock starts on the date the court officially renders its judgment. This isn't the day you filed the lawsuit or even the day a jury reached a verdict. It’s the specific date the judgment becomes a formal, legal order of the court.

The date of judgment is the trigger. From that day forward, every single day of non-payment adds to the total amount owed. It methodically increases both the value of the creditor's claim and the liability of the debtor.

How This Affects Your Business Strategy

Understanding these rules isn't just an academic exercise; it gives you a real-world advantage. Knowing that Connecticut uses a fixed statutory rate allows you to plan with precision. You can calculate exactly what you're owed at any point in the future, which is incredibly valuable when you’re negotiating a settlement or planning your next move.

This clear legal framework empowers you to assert your rights with confidence. There’s no room for debate about the rate or when it started. That clarity strengthens your position, whether you're sending a demand letter that includes the accrued interest or filing for a bank execution to seize funds. It turns your legal victory into a tangible, growing financial asset.

How To Accurately Calculate What You Are Owed

Knowing the rules behind interest after judgment is one thing, but actually crunching the numbers is where you take back control. The good news is that the calculation itself isn’t complex legal wizardry. It’s based on a straightforward simple interest formula.

The formula is a classic for a reason: Principal x Rate x Time. In the context of a Connecticut judgment, each piece of that puzzle is clearly defined, leaving no room for guesswork.

Breaking Down the Simple Interest Formula

Let's quickly take apart that equation so it’s crystal clear:

- Principal: This is the original judgment amount the court awarded you. Think of it as your starting line.

- Rate: This is the annual interest rate set by Connecticut law. It’s a fixed percentage, which means the growth is predictable and steady.

- Time: This is the clock that starts ticking the moment the judgment is entered and stops the day you get paid. For accuracy, it's usually calculated down to the day.

This simple math ensures you are compensated for every single day the debtor delays payment, systematically increasing what you are legally owed.

The process is linear and predictable, starting with the judgment and ending with a final calculation.

As you can see, it’s a direct path from the court's decision to your final payout.

A Real-World Calculation Example

Let's make this tangible. Imagine your business wins a $100,000 judgment on January 1, 2024. If the debtor waits five full years to pay, how does that interest add up? Using Connecticut's 10% annual statutory rate, the interest accrues steadily.

Below is a simplified table showing how that debt grows year after year.

| Year After Judgment | Principal Owed | Annual Interest Accrued | Total Balance Owed |

|---|---|---|---|

| 1 | $100,000 | $10,000 | $110,000 |

| 2 | $100,000 | $10,000 | $120,000 |

| 3 | $100,000 | $10,000 | $130,000 |

| 4 | $100,000 | $10,000 | $140,000 |

| 5 | $100,000 | $10,000 | $150,000 |

After five years, the original $100,000 debt has grown by $50,000 in interest alone. This is money you are entitled to collect, and it highlights why you shouldn't just let an unpaid judgment sit. Remember, this interest continues to build for the entire enforceable lifespan of the judgment, which connects directly to how long a judgment lasts in Connecticut.

What Happens With Partial Payments?

Now, let's tackle a more common scenario: the debtor makes a partial payment. This is where a critical rule comes into play. In Connecticut, any payment must first be applied to the accrued interest before it can touch the principal.

Let's use our $100,000 judgment from January 1, 2024, with its 10% annual interest rate. On July 1, 2024—exactly six months later—the debtor makes a $10,000 partial payment.

First, we calculate the interest that has built up over those six months (0.5 years):

- $100,000 x 0.10 x 0.5 = $5,000 in accrued interest.

Next, we apply the debtor's payment according to the rule:

- The $10,000 payment first wipes out the $5,000 in interest.

- The remaining $5,000 is then applied to the principal.

- The new principal balance is now $100,000 - $5,000 = $95,000.

From July 1, 2024, forward, the 10% annual interest now accrues on the new, reduced principal of $95,000. This method ensures you are always compensated for the delay in payment before the underlying debt is paid down.

Mastering these calculations isn’t just an accounting exercise. It’s about enforcing your rights and making sure you recover every dollar you are owed.

Enforcing Your Judgment and Collecting the Full Amount

Winning in court feels like the finish line, but it’s really just the beginning. That piece of paper—the judgment—is a powerful tool, but it doesn't automatically put money in your bank account. Too many creditors make the mistake of waiting for the debtor to pay up, but a judgment isn't a suggestion; it's an authorization to take action. You have to shift your mindset from passively waiting to actively pursuing what you're owed, including every last cent of interest after judgment.

This is the enforcement stage, and it’s where your legal victory becomes a real financial recovery. It means using the legal system to compel a debtor to pay when they won't do so willingly.

Shifting from Waiting to Actively Pursuing

The moment the judge’s gavel falls and a judgment is entered, the interest clock starts ticking in your favor. But that interest is meaningless if you never collect the underlying debt. Sending polite reminders is no longer the right move. It’s time to use the legal mechanisms available in Connecticut to seize assets and force the issue.

An effective enforcement strategy is all about knowing the debtor’s financial picture and picking the right tool for the job. Waiting for them to "do the right thing" is almost always a losing game. You have to be the one to take decisive action.

Key Enforcement Tools in Connecticut

Connecticut law gives creditors a powerful arsenal for collecting on a judgment. Each tool is designed for a specific purpose, and knowing which one to deploy can make all the difference in getting paid. Understanding how to enforce a judgment effectively is a critical piece of the puzzle.

Here are some of the most common and powerful tools at your disposal:

-

Bank Account Executions: This is often the quickest and most direct path to your money. A bank execution (or garnishment) is a court order sent straight to the debtor’s bank. The bank is then legally obligated to freeze funds up to the total amount you’re owed—principal judgment plus all accrued interest—and hand them over. It's the perfect tool when you know where the debtor keeps their cash.

-

Wage Garnishments: If your debtor has a job, a wage garnishment can create a steady, reliable stream of payments. With this court order, the debtor's employer must withhold a percentage of their paycheck and send it directly to you. It might take some time to collect the full amount, but it applies consistent pressure and ensures you’re making progress.

-

Property Liens: For larger judgments, putting a lien on the debtor's real estate is a fantastic long-term strategy. A property lien is a legal claim filed against their property, securing your debt. The debtor can’t sell or refinance the property without paying you first. This move effectively turns their real estate into collateral for what they owe you.

A judgment is not a self-executing document. It is a grant of authority—an authorization for the creditor to use the power of the state to seize the debtor’s assets to satisfy the debt. Without enforcement, it remains just an authorization.

The Importance of Post-Judgment Discovery

So, what happens if you don't know where the debtor banks, works, or owns property? This is a very common roadblock, but the law provides a way forward: post-judgment discovery. This legal process allows you to force the debtor to reveal their financial information under oath.

You can use several discovery tools to uncover those hidden assets:

- Interrogatories: These are formal written questions about the debtor's finances, assets, and income that they must answer in writing, under oath.

- Depositions: This is a face-to-face questioning session where you (or your attorney) can question the debtor under oath, allowing for real-time follow-up questions to dig into the details.

- Requests for Production: You can legally demand that the debtor turn over key documents like bank statements, tax returns, and property deeds.

Lying or failing to respond during discovery has serious legal consequences for the debtor, which makes it an incredibly effective tool for finding the resources needed to satisfy your judgment. By actively enforcing your rights, you can ensure your hard-won legal victory translates into a real financial recovery for your business.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Strategic Advice for Creditors and In-House Counsel

Winning a judgment is a major milestone, but it's not the finish line. In fact, for many, it’s where the real work begins. Now, the focus shifts to actually collecting the money you're owed, and interest after judgment is a powerful tool you can't afford to ignore.

Whether you're the creditor trying to collect or the in-house counsel advising a company on its next steps, having a clear strategy is everything. For creditors, it’s about turning that court order into cash. For debtors, it’s about preventing a manageable debt from spiraling out of control.

Best Practices for Creditors

As a creditor, you have to be proactive. Simply winning in court and waiting for a check to arrive is a recipe for frustration. To make sure you recover what you're owed, you need a disciplined, methodical approach from day one.

- Track Interest Religiously: Keep a detailed, running ledger of the interest as it accrues. This isn’t just for your own records—it’s the foundation for every demand letter and enforcement action you’ll take.

- Make Calculated Demands: When you contact the debtor, don't just ask for the original amount. Your demand should always include the up-to-the-minute total, showing both the principal and the interest. This removes any confusion and underscores the real-time cost of their delay.

- Know When to Escalate: Don't let your demands go unanswered for months on end. If the debtor isn't responding, it’s time to move on to more aggressive enforcement actions, like bank levies or property liens. Time is on their side if you let them drag their feet.

The Debtor’s Peril: Acknowledging the Financial Risk

For a business that owes money, ignoring a judgment is one of the worst financial mistakes you can make. Post-judgment interest acts like fuel on a fire, relentlessly turning a manageable debt into a crushing one. Here in Connecticut, that growth is predictable and unforgiving.

An unpaid judgment isn't a static number on a balance sheet. It's a dynamic liability that grows larger every single day, putting company assets at direct risk of seizure.

The longer you wait, the worse it gets. As the total debt swells, the creditor becomes more motivated to use aggressive collection tactics. What could have been settled with a simple payment can quickly escalate into frozen bank accounts, garnished revenues, and liens on company property—disrupting your operations and cratering your creditworthiness.

Strategic Counsel for In-House Legal Teams

If you're in-house counsel, post-judgment interest is a critical piece of your risk management puzzle. Your job is to guide the business toward the most financially sound decision, and that means running the numbers.

The conversation often boils down to a simple question: do we pay now, or do we appeal?

- The Appeal vs. Interest Calculation: An appeal can take years. All the while, interest is ticking away on that original judgment. You have to weigh the odds of winning the appeal against the guaranteed cost of interest if you lose. It's a high-stakes bet.

- The "Cost of Waiting": Give your executive team a clear projection. Show them exactly how much that judgment will grow in one year, then two, and so on. This turns an abstract legal problem into a concrete financial liability they can understand.

In some situations, it might even make sense to pay the judgment right away—even if you plan to appeal. This stops the interest from piling up. Of course, that comes with its own risk: if you win the appeal, you have to be sure the creditor is financially stable enough to pay you back. This is where your guidance is absolutely vital.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Taking the Next Step in Judgment Recovery

We've walked through how post-judgment interest works, and it's clear this isn't just some minor detail in your case. Think of it as an active financial tool that protects the value of your legal victory, compensating you for delays and giving debtors a very real reason to pay up sooner rather than later. From understanding Connecticut's specific interest rate to calculating what you're owed and enforcing your rights, you now have the roadmap.

But a roadmap is useless if you don't start the journey. Letting a hard-won judgment sit idle is like leaving money on the table—its value can slowly erode over time. The key is to take decisive, strategic action now to turn that court order into actual cash for your business. The longer you wait, the greater the risk that a debtor might move assets or simply become harder to find.

Securing a judgment is only half the battle. The true victory comes when you have the funds in hand. Prompt and knowledgeable action is essential to securing the full amount you are rightfully owed.

If you're ready to enforce a judgment or simply need clear guidance on a business law matter, it's time to bring in a professional.

To discuss your business law matter, contact Kons Law at (860) 920-5181.

A Few Common Questions About Interest After Judgment

Once a legal judgment is handed down, a lot of questions pop up, especially around the money. Getting a handle on interest after judgment is a must—for creditors trying to collect what they're owed and for debtors who need to know the full extent of their liability.

Let's clear up some of the most common questions that come up here in Connecticut.

Can the Judgment Interest Rate Change in Connecticut?

This is one of those questions where Connecticut law is crystal clear. Unlike the federal system where rates can bounce around with the market, Connecticut's statutory interest rate is fixed the moment the judgment is entered.

This creates a stable, predictable playing field for everyone involved. Once the court finalizes the judgment, that interest rate is locked in for the long haul, taking any guesswork out of future calculations.

What Happens If the Debtor Makes a Partial Payment?

Partial payments are pretty common, but how they're applied is governed by a strict rule. It's a critical concept for creditors to track everything accurately and for debtors to understand how their payments are actually chipping away at the total balance.

Standard practice follows a specific order:

- First, it goes to accrued interest. The payment has to cover all the interest that has built up since the judgment date or the last payment.

- Then, it goes to the principal. Only after all the outstanding interest is paid off does any leftover money start reducing the original judgment amount.

This "interest-first" approach makes sure the creditor is compensated for the delay in getting paid before the core debt is touched.

Is the Interest I Collect Considered Taxable Income?

Yes, in almost every case, it is. From an accounting standpoint, the interest you collect on a judgment is treated as income.

While the original judgment might just be a return of your own capital, tax authorities generally see the post-judgment interest as earned income. It's always a smart move to talk with a tax professional to get advice tailored to your specific financial situation.

You'll want to account for this income properly to stay compliant and sidestep any future headaches with the IRS.

How Long Do I Have to Collect a Judgment in Connecticut?

There’s definitely a time limit. Connecticut has a statute of limitations for enforcing judgments, which sets the clock on how long you have to take legal action to collect your money.

While the window is fairly generous, it's not endless. Procrastination is the biggest enemy of a successful collection. The best game plan is always to act fast and decisively to enforce your judgment. Moving quickly gives you the best shot at a full recovery before a debtor’s assets get moved, spent, or just disappear. Don't let your legal win expire on a technicality.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.