The envelope arrives by mail, or the call comes from your branch manager, compliance officer, or a lawyer who says the SEC wants documents. Most financial advisors have the same first reaction. They assume the worst, they want to explain everything immediately, and they start searching old emails before they've made a plan.

That's usually the first mistake.

An SEC inquiry is serious, but it isn't a finding of wrongdoing. In many securities and exchange commission investigations, the outcome turns less on the first allegation than on how the advisor responds in the first few days. Records get scattered, internal conversations create new problems, and inconsistent explanations harden into credibility issues that were avoidable.

The better approach is controlled, documented, and strategic. You need to know what kind of inquiry this is, what authority the staff has at this stage, what other regulators may already be involved, and how your answer today might affect a FINRA 8210 request or a Form U5 disclosure tomorrow.

Responding to an Inquiry from the SEC

A common version of this begins subtly. An advisor receives a letter requesting communications with a client, notes about a product recommendation, and documents tied to several transactions from months earlier. Nothing in the letter says “charges.” Nothing in it says “fraud.” But the scope is narrow enough to suggest the staff already has a theory.

That moment calls for discipline, not speed.

The first job is to stop informal damage. Don't call the client to “clear things up.” Don't send texts to former colleagues asking what they remember. Don't start rewriting chronology notes. And don't assume your firm's interests and your personal interests are identical just because you work under the same roof.

What to do in the first 48 hours

Three steps matter immediately:

- Preserve everything. Emails, texts, CRM notes, calendars, trade records, handwritten notes, and messages on personal devices if they relate to business activity.

- Identify the decision-makers. Know whether firm counsel, outside counsel, compliance, and your own attorney are speaking with one voice or protecting different interests.

- Build a timeline before making statements. Dates, products, customers, disclosures, supervisory contacts, and any prior complaint history need to be organized before you answer substantive questions.

Practical rule: Your first explanation is rarely your best explanation. Facts usually look different once documents are collected and placed in sequence.

A deposition-style mindset helps early, even before sworn testimony is on the table. If you need a practical sense of how preparation changes outcomes, this discussion of how to prepare for deposition is useful because the same habits apply here. Listen carefully, answer only what's asked, and never guess when a record can answer the question better than memory can.

What does not work

Advisors often hurt themselves by doing one of these:

- Overexplaining: A long narrative invites inconsistencies.

- Partial production: Producing some records while “cleaning up” others creates a far worse issue than the original inquiry.

- Internal gossip: Side conversations with coworkers can become evidence.

- Assuming it will go away: Silence can look evasive if deadlines pass.

An SEC inquiry can be managed. It just can't be handled casually.

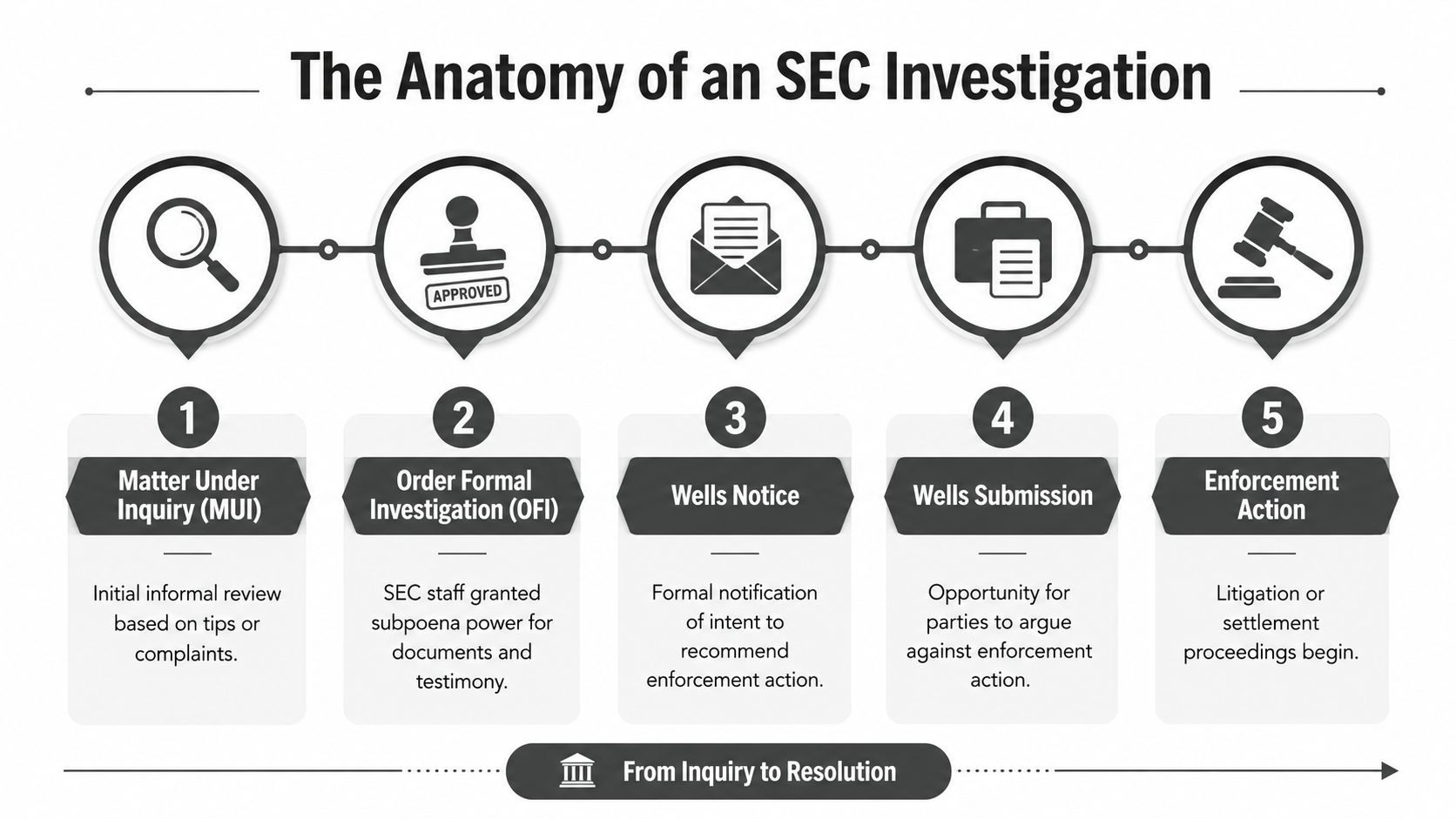

The Anatomy of an SEC Investigation

The most important distinction in SEC practice is whether you're dealing with an informal matter or a formal investigation. Many advisors don't realize the legal stakes change sharply at that line.

SEC investigations typically begin as informal Matters Under Investigation before escalating to formal investigations where the Enforcement Division obtains a Commission-delegated order granting subpoena power. This is the threshold where the process shifts from voluntary cooperation to legal compulsion. Without the formal order, the SEC cannot legally force a firm to produce records, as outlined in the SEC's discussion of enforcement procedure under Section 20(a) and formal investigative authority.

The informal stage

An informal inquiry often arrives as a request for documents, an invitation to speak voluntarily, or a request routed through your firm. Staff may be testing a complaint, a trading pattern, or a referral. At this point, people often make the mistake of treating the request as minor because the tone seems cooperative.

It isn't minor. It's preliminary.

The trade-off at this stage is simple. Early cooperation can help frame the facts before the staff settles on a theory, but uncontrolled cooperation can lock you into positions before you know what the SEC has. The right answer depends on the documents, the likely exposure, and whether parallel regulators are already circling.

The formal stage

Once the SEC obtains a formal order, the staff can compel records and sworn testimony. That changes everything. The process becomes less about whether to engage and more about how to engage without creating avoidable admissions.

Here's the practical difference:

| Stage | What it usually means for the advisor |

|---|---|

| Informal inquiry | The SEC requests cooperation, but compulsion hasn't attached |

| Formal investigation | The staff can issue subpoenas for documents and testimony |

| Testimony preparation | Every answer must be built against the record and the legal theory |

| Wells phase | You get a direct chance to argue against charges |

| Enforcement decision | The matter may close, settle, or proceed into litigation |

An advisor facing document demands in a formal matter also needs to think about books-and-records obligations, supervisory structure, and firm policy compliance. That's where a practical compliance review becomes useful. This overview of compliance for RIA practices is a good reference point because many SEC investigations turn on whether written procedures matched actual conduct.

Testimony and document production

Document production sounds mechanical. It isn't. Collection errors, inconsistent custodian lists, and sloppy privilege calls can define the case before testimony begins.

Sworn testimony, often called on-the-record testimony or OTR, carries even more risk. A witness who tries to persuade the staff usually performs worse than a witness who answers carefully, stays within personal knowledge, and refuses to speculate. The best preparation isn't memorizing scripts. It's mastering chronology, likely exhibits, and weak points the staff will probe.

The SEC staff often knows more of the document trail than the witness expects. Testimony should be precise, not expansive.

The Wells process

The Wells process is the decisive checkpoint before charges are filed. SEC staff gives a prospective respondent a Wells notice describing the alleged violations and offers the chance to submit a written Wells Submission arguing against enforcement. A successful submission can lead the staff to close the matter without charges, according to Investopedia's explanation of the SEC Division of Enforcement and the Wells process.

That phase is strategic, not ceremonial.

A strong Wells Submission usually does one or more of these well:

- Challenges the legal theory: The conduct doesn't fit the alleged rule or statute.

- Rebuilds intent evidence: The documents show supervision, disclosure, or good-faith conduct.

- Narrows the case: Even if some issue exists, the proposed charge is overstated.

- Frames consequences: Collateral effects on licensing, employment, and customer relationships can matter.

Weak Wells submissions tend to read like angry rebuttals. Strong ones are disciplined briefs anchored in the record.

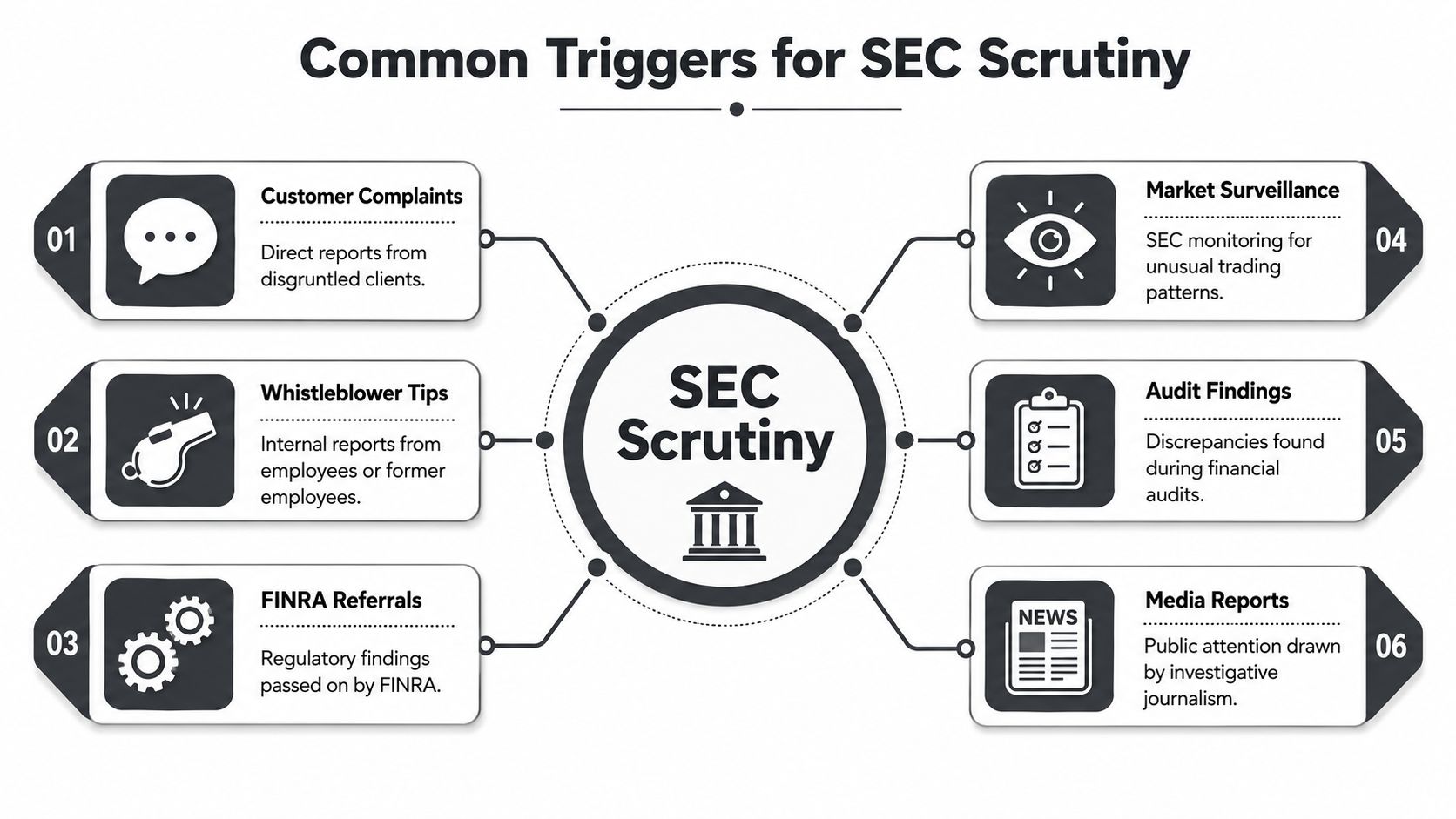

Common Triggers for SEC Scrutiny

Most advisors don't wake up one day under SEC scrutiny without some event placing them on the map. The trigger may be obvious, like a customer complaint, or indirect, like a referral from another regulator. What matters is that the SEC rarely sees the issue in isolation. It sees a pattern, or at least the possibility of one.

Complaints and referrals

A customer complaint doesn't need to be well written to create trouble. If it alleges unsuitable recommendations, unauthorized trading, misleading performance discussions, or undisclosed conflicts, the complaint may move beyond the firm's internal process and into a regulatory channel.

FINRA referrals also matter. An issue that starts as a books-and-records concern, an outside business activity question, or a sales practice review can migrate quickly. That's one reason advisors should understand the conduct regulators often classify as securities violations. This overview of what is securities fraud is helpful because the label regulators use can shape the entire defense posture.

Trading patterns and internal tips

Some investigations begin because the SEC sees activity that doesn't fit the surrounding market facts. Unusual timing, concentrated transactions, trading around corporate events, or account activity inconsistent with the customer profile can all draw attention. The advisor may believe the pattern has an innocent explanation. The staff may believe the pattern deserves records first and explanations later.

Whistleblower complaints create a different problem. Former assistants, junior advisors, branch staff, and compliance personnel often know where emails, CRM notes, and calendars live. Even when the underlying accusation is exaggerated, the whistleblower may still provide a roadmap to documents.

A weak accusation can still produce a strong investigative file if the records are messy.

Form U5 language and public signals

One of the most underestimated triggers is the language used in a departure disclosure. Firms sometimes draft broad, defensive, or loaded Form U5 language to protect themselves. That wording can invite questions far beyond the original employment dispute.

Examples that often create downstream risk include:

- Conduct-based phrasing: References to policy violations, client complaints, or review of trading activity

- Ambiguous separation language: Statements that imply unresolved compliance concerns

- Timing problems: A termination that closely follows a complaint, audit, or product review

- Supporting material: Internal memos or emails that don't align with the wording chosen for the filing

The Wells process may come much later, but it matters even at the trigger stage. The SEC's staff can issue a Wells notice outlining specific alleged violations and allow a written Wells Submission arguing against enforcement, and a successful submission can result in the matter closing without charges, as noted in the earlier section.

The Regulatory Web of SEC FINRA and Form U5

The biggest mistake advisors make is treating the SEC, FINRA, and state regulators as separate lanes. In practice, one event often triggers all three.

An SEC document request can lead to a FINRA 8210 request. A FINRA inquiry can influence how the firm drafts a Form U5. A Form U5 disclosure can then shape how state regulators or future employers view the same conduct. By the time the advisor realizes there are multiple fronts, each statement made in one forum has already created consequences in the others.

Why parallel matters are so dangerous

A 2017 SEC review called for eliminating “duplicative and overlapping enforcement responses” against the same individuals for the same conduct, yet that risk remains a live problem for financial advisors, especially as SEC actions charging individuals have increased year over year, according to the review collected in Examining US SEC Enforcement recommendations and current practices.

That concern isn't academic. It changes defense strategy from day one.

If the SEC asks for documents about product recommendations and FINRA asks about supervision of the same accounts, you don't have two unrelated matters. You have one fact pattern moving through different rulebooks. A statement that sounds harmless in one response can become an admission in the other.

The Form U5 cascade

The U5 is often the career-defining document in the background. Firms use it to explain separation. Regulators read it. Future employers read it. Claimants' lawyers read it.

A practical response requires looking at all three layers at once:

| Layer | What the advisor should ask |

|---|---|

| SEC inquiry | What theory is the staff testing, and what records support or defeat it? |

| FINRA 8210 request | Are the requests broader, narrower, or differently framed than the SEC's? |

| Form U5 issue | Does the language overstate facts, imply misconduct, or create future licensing damage? |

For a grounded discussion of how these disclosures affect later disputes, see this article on Form U5 and FINRA issues. The practical point is that U5 language shouldn't be treated as a clerical afterthought. It's often the bridge between an employment conflict and a regulatory case.

Reputation and unified defense

Parallel investigations create legal exposure, but they also create search-result exposure, client anxiety, and recruiting damage. Advisors dealing with public-facing fallout often need to think beyond the regulatory file itself. A useful companion resource is Navigating FINRA rules and reputation, which addresses how reputation issues intersect with the regulatory framework financial professionals operate under.

The best defense is unified. One chronology, one document strategy, one theory of the case, applied consistently across every regulator and every disclosure.

When the defense is fragmented, the advisor ends up solving yesterday's problem in one forum while creating tomorrow's problem in another.

Building Your Defense and Proactive Compliance

If you've received an SEC inquiry, the most important move is immediate and critical. Get specialized securities counsel before responding on substance. Not general business counsel. Not a colleague's employment lawyer. Not only firm counsel if your interests may diverge from the firm's.

That doesn't mean stonewalling. It means controlling the process before the process controls you.

The first defensive moves

A sound defense usually starts with five workstreams happening at once.

- Preservation comes first. Issue a legal hold broadly enough to capture email, text messages, CRM entries, cloud storage, trade blotters, notebooks, and home-office records tied to business activity.

- Build a document map. Identify custodians, systems, date ranges, and likely hot documents before production starts.

- Create a clean chronology. Dates matter more than opinions. Put transactions, client calls, disclosures, supervisory reviews, and complaint events in order.

- Separate personal from firm interests. The firm may want a quick institutional answer. The advisor may need a different strategy.

- Prepare for testimony early. You don't wait for the notice to start witness preparation. You prepare while reviewing documents so memory gets tested against records.

Handling productions securely also matters. Advisors and small firms often underestimate how much risk they create by passing investigative files around casually. For a practical overview of safer workflows, this guide to secure file sharing for accountants is useful beyond the accounting world because the same confidentiality and version-control issues apply to regulatory responses.

Cooperation versus overcooperation

Many clients ask whether they should cooperate. The better question is how to cooperate.

Useful cooperation is organized, credible, and deliberate. Overcooperation happens when a witness volunteers interpretations, guesses about other people's motives, or broad statements that go beyond the documents. That kind of “helpfulness” often gives the staff more theories to test.

Here's a practical comparison:

| Approach | Usually helps | Usually hurts |

|---|---|---|

| Document production | Complete, timely, reviewed for accuracy and privilege | Incomplete, disorganized, or inconsistent productions |

| Witness communication | Narrow, truthful, prepared answers | Narrative advocacy and speculation |

| Internal review | Quiet fact gathering with counsel direction | Group chatter and informal side investigations |

| Remediation | Thoughtful corrective action tied to actual issues | Cosmetic fixes adopted only for appearances |

Working rule: Regulators often forgive a problem more readily than they forgive a cover-up, a sloppy production, or a shifting story.

Proactive compliance after the immediate crisis

Good defense work should improve the business going forward. Advisors and firms reduce future risk when they tighten the points where most cases start.

Focus on operational habits that hold up under scrutiny:

Supervisory and communication controls

Review how recommendations are documented, how client objectives are updated, and how exceptions are escalated. If a recommendation was suitable, the file should show why. If a client insisted on a higher-risk position, the notes should say so clearly.

Training and policy reality

Written procedures matter only if people follow them. Compare policy language to what happens in real client interactions, product sales, outside business activity reporting, and electronic communications. Most enforcement risk lives in the gap between handbook language and daily practice.

Periodic internal audits

Firms should test areas that historically create exposure. Off-channel communications, concentration issues, rollovers, fee disclosures, private securities transactions, and advertising claims all deserve periodic review. The goal isn't perfect paperwork. It's a record that can withstand skeptical reading by someone outside the firm.

Potential Outcomes and Finding the Right Counsel

Not every SEC matter ends in charges. Some are closed. Others resolve through negotiated terms. Some become litigation or administrative proceedings. The path depends on the facts, the documents, the witness performance, and whether the defense gives the staff a persuasive reason to stop.

Possible outcomes generally include:

- No action or closure: The staff ends the matter without bringing an enforcement case.

- Settlement: The respondent resolves the matter without fully litigating it.

- Civil enforcement or administrative action: The SEC seeks formal remedies through court or administrative process.

- Collateral consequences: Industry bars, reputational damage, employment loss, and disclosure complications can outlast the case itself.

What to look for in counsel

The right lawyer for securities and exchange commission investigations should understand more than the SEC file. Advisors need counsel who sees the linked consequences across FINRA, state inquiries, employment disputes, compensation issues, and Form U5 wording.

Ask practical questions:

- Have you handled SEC investigations involving financial advisors, not just public companies?

- Do you regularly deal with FINRA 8210 requests and U5 disputes tied to the same facts?

- How do you prepare clients for sworn testimony?

- Who manages the document strategy and privilege review?

- How do you coordinate when the firm's interests differ from the advisor's?

A good defense lawyer doesn't promise a painless process. A good defense lawyer gives you a controlled process, realistic expectations, and a strategy that holds together across every forum where your name may appear.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.