A business can post strong revenue, hire aggressively, and still walk straight into a governance disaster. It usually starts with something ordinary. Two founders stop agreeing on major decisions. A senior executive approves a vendor contract without disclosing a personal relationship. A board approves compensation because nobody wants a difficult conversation. Then the dispute hardens, trust evaporates, and counsel gets called after the damage is already expensive.

That's how corporate governance issues show up in real life. Not as a philosophy problem. As a lawsuit, a regulatory inquiry, a frozen bank relationship, a broken cap table, a damaged Form U5 narrative, or a departing advisor fight that drags clients and staff into the mess.

Smaller private companies and financial advisory practices are especially vulnerable because they often assume governance is something public companies worry about. That's a mistake. Closely held companies, RIAs, broker-affiliated practices, family businesses, and founder-led firms face the same core risks with fewer buffers and less internal structure.

Introduction When Good Companies Face Bad Outcomes

A profitable company can still become ungovernable fast. One co-owner signs a side deal. Another claims the board never approved it. The CFO says the reporting package omitted key liabilities. Employees start asking who is in charge. Lenders and investors don't wait around for the adults to sort it out.

Governance failures rarely begin with obvious fraud. More often, they begin with neglected basics. No clear voting rules. No disciplined board process. No disclosure standard for conflicts. No real separation between owners, directors, and management. When the company is small and everyone knows each other, those gaps stay hidden until money, control, or succession puts pressure on them.

That pressure is exactly why governance matters. According to the Global Investor Sentiment Survey 2023 reported by Proxymity, 68% of investors worldwide consider effective corporate governance practices essential to a company's long-term success. Investors aren't treating governance as paperwork. They treat it as evidence that the business can make decisions, manage risk, and survive internal conflict.

Practical rule: If your company can't show who has authority, how decisions get approved, and how conflicts get disclosed, you don't have governance. You have optimism.

In financial practices, the same pattern appears in a different suit. Compensation arrangements get negotiated casually. Client transition rights aren't documented carefully. Supervisory responsibility gets blurred. A termination or investigation arrives, and everyone suddenly argues over duties that should have been written down years earlier.

Strong governance doesn't eliminate conflict. It contains it. It gives the company a process before a disagreement becomes a legal event.

The Foundation What Corporate Governance Means for Your Business

Corporate governance is your company's operating system. It decides who can act, who must approve, what gets disclosed, and how the business handles conflicts, compensation, reporting, and succession. If that operating system is weak, even a good management team will eventually produce bad outcomes.

At a practical level, governance rests on three groups:

| Group | Core role | Main risk if blurred |

|---|---|---|

| Owners or shareholders | Set high-level rights and economic expectations | Control fights and deadlock |

| Board of directors | Oversee strategy, accountability, and major decisions | Rubber-stamping management |

| Management | Run day-to-day operations | Acting beyond authority |

The trouble starts when those lines collapse. In founder-led businesses, owners often act like officers, directors, and controlling shareholders all at once. Sometimes that works during early growth. It fails when stress arrives. A dispute over dilution, compensation, distributions, hiring authority, or a sale of the business becomes impossible to unwind because nobody respected role boundaries in the first place.

What governance looks like in practice

Good governance isn't abstract. It means your company can answer basic questions without hesitation:

- Authority: Who can sign contracts, borrow funds, hire senior personnel, or approve related-party deals?

- Oversight: Who reviews management decisions and how is that review documented?

- Escalation: What happens when two principals disagree on a material issue?

- Disclosure: When must insiders disclose personal interests, outside business activity, or compensation changes?

For a useful primer on the legal structure behind those questions, see Kons Law's discussion of what corporate governance is.

Why the business case is stronger than most people admit

Governance isn't just defensive. It affects performance. Research analyzing 10,171 US companies between 2002 and 2014 found that in 85% of observed situations, a positive and significant correlation exists between high corporate governance scores and improved financial performance, specifically Return on Equity (ROE).

That finding tracks with what lawyers and advisors see on the ground. Companies with disciplined approvals, credible oversight, and documented accountability usually make cleaner decisions. They also handle mistakes faster. Banks, investors, acquirers, and regulators notice that.

A company with strong governance is easier to diligence, easier to finance, and easier to defend.

For private companies and advisory firms, that matters even more. You may not face public company reporting burdens, but you still face lender scrutiny, partner disputes, employment claims, succession issues, and regulatory exposure. Governance is how you reduce the odds that an internal problem turns into an existential one.

Leadership Failures Board Composition and Executive Pay

A weak board can do real damage while appearing perfectly functional. Meetings happen. Minutes exist. Votes are unanimous. Nobody asks hard questions. That's not oversight. That's ceremonial approval.

In private companies, bad board composition is often obvious once you stop pretending otherwise. The board consists of the founder, the founder's friend, the founder's relative, and maybe an investor representative who only surfaces when a financing is pending. In financial practices, the equivalent problem shows up when senior producers dominate governance and nobody with compliance, operations, or risk authority has a real voice.

What a broken board looks like

The most common red flags are practical, not theoretical:

- Overcommitted directors: People who do not have time to prepare, challenge management, or follow through. The Council of Institutional Investors policy guidance recommends that directors employed full-time by a for-profit corporation should serve on no more than two total for-profit boards, while all other directors should serve on no more than four total for-profit boards.

- Dependency on management: Directors who rely on the CEO for information, strategy framing, and social access won't provide meaningful oversight.

- Missing skill coverage: A board discussing compensation, supervision, M&A, cybersecurity, or advisor departures needs directors who understand those risks in plain business terms.

- No committee discipline: Compensation and audit matters get discussed casually, without a defined process or independent review.

A board member's job isn't to be agreeable. It's to test assumptions, force disclosure, and document reasoning.

Executive pay is where bad governance becomes visible

Boards often defend weak compensation design by calling it market practice. That excuse doesn't hold up. The issue isn't that executives are paid well. The issue is whether the company can explain, in writing, why a compensation package rewards outcomes that matter to the business.

Research and governance guidance cited by Planful's analysis of common corporate governance problems states that effective governance requires CFOs and HR to anchor executive compensation to "established and clearly documented performance-based metrics." If your compensation committee can't point to those metrics, it isn't governing compensation. It's approving transfers of value.

That matters in every setting. In a manufacturing company, it can mean rewarding growth that destroys margin. In an advisory practice, it can mean paying on production while ignoring supervision failures, transition risk, retention quality, or unresolved compliance issues.

Board advice: If compensation goals can be rewritten midstream without disciplined disclosure and approval, they were never real goals.

Clawbacks belong in this conversation too, especially where incentive compensation, deferred comp, or separation disputes are part of the risk profile. This explanation of a clawback provision is useful because it frames the issue in business terms rather than slogans.

A direct recommendation

If you're a new board member or a practice owner, insist on three things within your first review cycle:

- A board matrix that identifies missing skills, independence issues, and committee assignments.

- A written compensation philosophy tied to documented business and risk objectives.

- A meeting process where management materials go out early enough for actual review, not day-of signature collection.

That isn't overengineering. It's basic self-protection.

Ethical Lapses Conflicts of Interest and Fiduciary Breaches

Most fiduciary breaches don't begin with a villain speech. They begin with rationalization. An executive says the company needed to move quickly. A director says everyone already knew about the relationship. A partner says the opportunity wasn't really the company's to begin with. Those explanations sound familiar because people use them every day right before litigation starts.

Directors and officers owe duties of care and loyalty. In plain English, that means they must make informed decisions, act in the company's interest, and avoid using their position for personal gain at the company's expense. Once a personal interest enters the room, governance has to get tighter, not looser.

Conflicts that boards and owners routinely miss

The easiest conflict to spot is a related-party transaction. The hardest one to catch is the transaction nobody labels as related because the relationship sits one step offstage. A spouse-owned vendor. A side investment with a client. A recruiting arrangement that benefits one principal personally. An office lease through an affiliate. A business opportunity diverted to a separate entity before the company can consider it.

Best practices require that companies disclose all material related-party transactions so conflicts can be reviewed and handled on an arm's-length basis, as explained in this discussion of corporate governance best practices and regulatory challenges.

Here's the legal reality. A conflict isn't cured because the insider believes the deal was fair. It isn't cured because the company made money. It isn't cured because people had a general sense that the insider had outside interests. It gets managed only when the conflict is disclosed fully, reviewed by the right decision-makers, and approved through a process the company can defend later.

Fiduciary duty problems in advisory firms

Financial advisory businesses are especially exposed because personal relationships and compensation structures often overlap. One principal may control recruiting. Another may control payouts. A third may supervise books and records. When one of them steers clients, staff, or vendor business toward a personal interest, the line between aggressive business conduct and fiduciary breach gets thin fast.

If you need the legal framework in straightforward terms, Kons Law's overview of breach of fiduciary duty is a useful starting point.

A practical conflict process should include:

- Disclosure intake: A written requirement to report outside interests, family relationships tied to vendors, and overlapping business opportunities.

- Recusal rules: The interested person leaves the discussion and vote.

- Independent review: Someone without the conflict evaluates pricing, alternatives, and business justification.

- Written record: Minutes should reflect the disclosure, the review, and the approval basis.

If a deal would look bad in discovery, it probably needed more process before approval.

Companies using technology to track approvals and flag relationships should also think about proactive risk mitigation with ethical AI from Logical Commander Software Ltd. Not because software replaces judgment. It doesn't. But structured workflows can force disclosures and audit trails that humans otherwise skip.

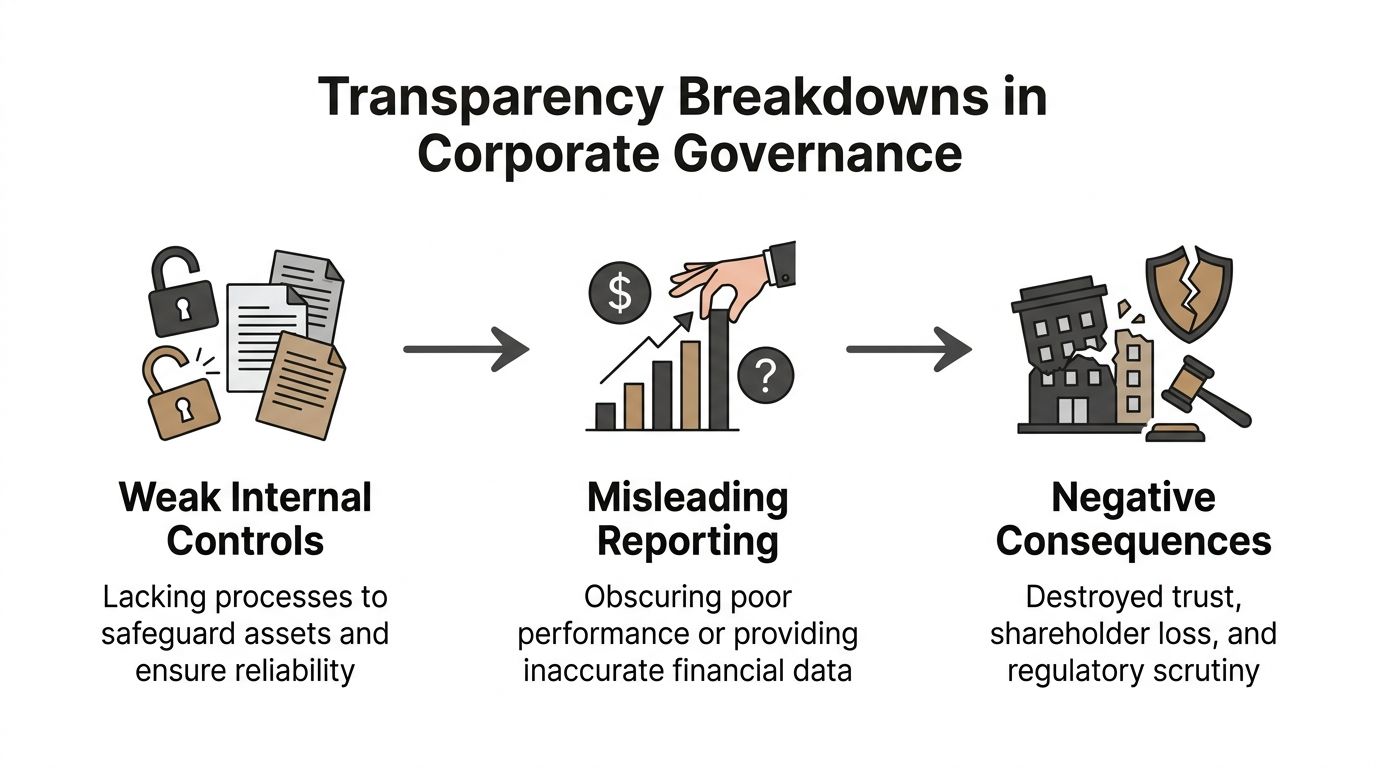

Transparency Breakdowns Disclosure Reporting and Internal Controls

A company cannot govern what it refuses to surface. When reporting is selective, delayed, or shaped to protect reputations instead of informing decisions, the board is blind and management is effectively unsupervised.

This problem doesn't only show up in public filings. It shows up in private board packets, compensation memos, compliance summaries, side letters, advisor transition reports, and internal budgets that leave out the ugly parts. In a privately held company, that kind of omission often goes unchecked longer because fewer people are looking.

Where transparency actually fails

Bad transparency usually comes from one of four habits:

- Selective reporting: Management highlights wins and soft-pedals legal, operational, or client retention problems.

- Compensation opacity: Decision-makers approve pay without a clean link between goals and outcomes.

- Weak internal controls: No consistent approval pathways, reconciliation steps, or review authority.

- Informal side deals: Key terms live in email threads, oral promises, or spreadsheets outside formal records.

The compensation point deserves blunt treatment. Effective governance requires CFOs and HR to anchor executive compensation to "established and clearly documented performance-based metrics," and weak disclosure around that link reduces accountability, as discussed in Planful's governance analysis. If compensation decisions can't be reconstructed clearly six months later, the process was broken when it happened.

Internal controls are governance, not just accounting

People hear "internal controls" and think of accountants. That's too narrow. Controls are the operating rules that protect assets, support reliable reporting, and make fraud or self-dealing harder to hide. Approval thresholds, segregation of duties, documentation standards, access restrictions, and exception reporting all sit inside governance.

For financial professionals, this lands close to home. If production credits, bonus calculations, client account authority, or expense approvals move through loose and undocumented processes, you'll eventually face a dispute that turns on records you don't have.

Good controls don't slow the business down. They stop the business from making expensive, avoidable mistakes at speed.

For broader context on how opacity creates downstream governance problems, this piece on policy insights on corporate transparency adds a useful policy lens.

A practical test for your reporting system

Ask these questions at the next board or ownership meeting:

| Question | If the answer is no |

|---|---|

| Can we trace major compensation decisions to written criteria? | Expect disputes over fairness and authority |

| Do material risks appear in regular reporting, not just crisis meetings? | Management is filtering what the board sees |

| Are related-party items flagged automatically for review? | Conflicts can pass as routine transactions |

| Can we prove who approved what and when? | Litigation risk rises sharply |

If your records don't answer those questions cleanly, your disclosure and control environment needs work now, not after a subpoena or partner split.

Your Governance Playbook Prevention and Remediation

Most companies don't need a glossy governance manual. They need a system that fits their ownership structure, industry risk, and actual decision patterns. The one-size-fits-all approach is overrated and often dangerous. The Directors & Boards discussion of the illusion of corporate governance best practices notes that 30% of firms adopting standardized models still face significant ethical breaches due to a lack of contextual adaptation. That makes sense. A private advisory practice with three equity owners doesn't need the same structure as a large public issuer, but it does need real controls.

Build the system around your real risks

Start with the issues most likely to injure your business, not the issues that look impressive in a policy binder.

For a founder-led company, the biggest governance risks may be deadlock, succession, owner compensation, and affiliate transactions. For an advisory practice, the risk map may center on supervision, compensation credits, restrictive covenants, advisor departures, books and records, and client communication authority.

A workable governance package usually includes:

- Clear governing documents. Bylaws, operating agreements, shareholder agreements, and buy-sell provisions should define voting thresholds, transfer restrictions, dispute mechanisms, and authority limits.

- Defined approval lanes. Spell out which decisions management can make, which require board action, and which require owner consent.

- Targeted committees or review groups. You may need an audit or compensation committee. You may also need something more specific, such as a conflicts review process or a succession committee.

- A written conduct and disclosure framework. Conflicts, gifts, outside business activities, and related-party transactions need disclosure rules that people can follow.

- Periodic review. Governance documents should be revisited when ownership, staffing, regulation, or strategy changes.

For additional guidance on the legal side of structuring those systems, Kons Law's corporate governance best practices materials are relevant to businesses reviewing their governance architecture.

What to do when a governance problem is already live

Once a problem surfaces, speed matters. Sloppiness at that stage compounds liability.

Use this triage sequence:

- Stabilize authority first. Decide who speaks for the company, who preserves records, and who controls internal communications.

- Preserve documents immediately. Emails, texts, board materials, compensation files, and transaction records must be retained.

- Separate the conflicted actor from the review. That may mean recusal, leave, or temporary limits on authority.

- Investigate with discipline. Not every issue requires a full outside investigation, but every material issue requires a reliable fact-gathering process.

- Assess disclosure obligations. In regulated environments, silence can create a second problem.

- Prepare the external messaging. If employees, clients, investors, or regulators may hear about the issue, use a structured approach. This crisis communications guide is a useful reference for handling the messaging side without inflaming legal risk.

Governance remediation fails when companies focus on optics first and facts second.

Tailored solutions beat borrowed templates

A small private company shouldn't copy a public company checklist and call it done. A financial practice shouldn't adopt generic board language while ignoring compensation disputes, transition risk, or supervision authority. Governance has to match the business you've built.

That means asking unpleasant questions directly:

- Who can block a sale?

- What happens if a rainmaker is terminated?

- How are ownership units valued on exit?

- When does an outside interest become disqualifying?

- Who reviews related-party arrangements?

- What records would we need tomorrow if litigation started today?

If those answers aren't written down, the company is relying on memory and informal advantage. That's not governance.

One practical option for businesses facing live governance disputes is to involve outside counsel early enough to shape the record instead of merely reacting to it later. In that role, a firm like Kons Law can help with governance review, dispute strategy, document drafting, investigations, and litigation positioning, depending on what the matter requires.

Conclusion Building a Foundation for Lasting Success

Corporate governance issues don't stay confined to meeting minutes. They show up as lawsuits, broken partnerships, regulatory scrutiny, disputed compensation, lost investor confidence, and expensive distractions that pull management away from the business. The pattern is consistent. Weak board oversight, unmanaged conflicts, and poor transparency create legal and operational problems that stronger governance could have contained.

Good governance is not bureaucracy for its own sake. It's a business control system. It protects decision-making, sharpens accountability, and gives owners, directors, and managers a structure they can rely on when pressure rises. That matters for public companies, but it matters just as much for closely held businesses, family-owned companies, and financial advisory practices where informal habits often replace clear rules.

The cheapest time to fix governance is before the dispute, the investigation, or the departure of a key producer. After that, every missing policy and every undocumented decision becomes evidence.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.