You've found a business that looks promising. The seller seems reasonable, the financial story is attractive, and you can already picture yourself running the company.

Then the deal starts moving, and the easy part ends.

You're suddenly staring at an LOI, diligence requests, employment questions, contract assignment issues, lender requirements, and a purchase agreement full of terms that can shift real money and real risk. That's the point where many first-time buyers realize a business acquisition isn't a paperwork exercise. It's a controlled investigation followed by a negotiated transfer of risk.

A good small business acquisition lawyer helps you decide whether the deal should happen, how it should be structured, and what protections you need before you close. If you want a useful overview of what that role looks like in practice, this business acquisition attorney guide is a solid starting point.

Why a Great Lawyer Is Your Most Important Asset

Buyers often hire counsel too late. They wait until they have a signed LOI, a draft purchase agreement, and a seller who wants to move fast. By then, the lawyer is reacting instead of shaping the deal.

That's backwards.

A strong small business acquisition lawyer earns their place early by filtering noise from risk. They can tell you which issues are ordinary, which ones justify a price change, and which ones should stop the deal entirely. That matters most for first-time buyers, because sellers and brokers naturally frame problems as manageable. Some are. Some aren't.

The lawyer's job is not just to document the deal

A weak approach looks like this: the buyer agrees on price, gets emotionally committed, then sends closing documents to counsel and says, “Can you review this?” At that stage, your bargaining power is already diminishing.

A better approach starts with counsel helping you define the transaction before the paper gets heavy. That includes confidentiality, the scope of diligence, deal structure, negotiating power, and where the biggest post-closing disputes are likely to come from.

Practical rule: If your lawyer's value starts at the purchase agreement, they've probably entered the process too late.

What first-time buyers usually underestimate

The legal risk in an acquisition rarely sits in one dramatic issue. It usually shows up in a cluster of smaller problems:

- Transfer problems: Key contracts, permits, or licenses don't move cleanly to the buyer.

- Employment friction: The people who keep the business running may not stay after closing.

- Seller assumptions: The seller thinks a past practice is “how we've always done it,” but it may create compliance or liability exposure.

- Integration blind spots: You close the deal, then discover the business can't operate the way you expected on day one.

An experienced lawyer helps you see those issues while you still have choices. That's why, in practical terms, your attorney is less like a form reviewer and more like risk counsel for the entire transaction.

The Core Functions of Your Acquisition Lawyer

A serious acquisition lawyer does far more than mark up a purchase agreement. They work as strategist, investigator, negotiator, and coordinator. If you want a broader view of business counsel beyond M&A, this explanation of what a business lawyer does gives useful context.

Strategist on deal structure

One of the earliest legal decisions is also one of the most important. Should you buy assets or equity?

That choice changes liability exposure in a very practical way. As MacGregor Lyon notes in its discussion of small-business M&A, an asset purchase can reduce successor-liability risk, while a stock deal may be necessary to preserve critical licenses, contracts, or vendor relationships. Buyers who assume asset deals are always safer often miss the operational cost of not being able to carry over what keeps the business functioning.

A good lawyer won't reduce that decision to a slogan. They'll ask better questions. Which contracts require consent? Which licenses are tied to the entity? Which vendor or customer relationships depend on continuity? What obligations are you trying to avoid, and what business value would you lose in the process?

Investigator during diligence

A purchase agreement can allocate risk, but it can't fix risk you never identified.

At this stage, counsel acts as an investigator. They review governing documents, key contracts, employment arrangements, threatened claims, compliance records, permit issues, and title to important assets. They also pressure-test assumptions. If the seller says a contract is “assignable,” your lawyer should want to see the actual language.

Some buyers now use workflow technology to move faster through document review and issue spotting. That can help, especially when the data room fills up quickly. Used carefully, resources on AI tools for corporate law can give buyers a sense of how legal teams are speeding up review without replacing judgment. The point isn't automation for its own sake. The point is finding issues while they still matter.

The best diligence question is often not “What does this document say?” but “What problem does this create if the seller leaves tomorrow?”

Negotiator on the terms that actually matter

Price gets attention. Risk allocation decides whether the deal still makes sense after closing.

Your lawyer should negotiate the parts of the deal that buyers tend to overlook until there's a dispute: indemnities, escrows, working capital adjustments, holdbacks, non-competes, employment terms, transition services, and what happens if a seller representation turns out to be wrong. Those aren't side documents. They shape tax consequences, liability exposure, and operational continuity.

Project manager for the whole team

An acquisition involves lawyers, accountants, lenders, brokers, and the business principals. Without someone managing the flow, issues surface late and everyone starts reacting.

The lawyer often becomes the hub. They keep requests organized, identify dependencies, coordinate drafts, and make sure legal work lines up with the CPA's findings and the lender's requirements. That function sounds administrative until it prevents a deal from drifting into confusion.

Mapping the Small Business Acquisition Journey

Buying a company feels like one decision, but in practice it's a sequence. Understanding the sequence helps you manage expectations and avoid rushing the wrong stage.

Industry guidance summarized by Acquisition Stars on the business acquisition process indicates that a small-business acquisition typically spans 6 to 9 months, with an average of 245 days. The same source notes that due diligence usually takes 30 to 90 days, and deals involving regulatory approvals, earnouts, or SBA financing can extend to 9 to 12 months.

If you're early in the process, it also helps to understand what a letter of intent does in a business deal, because the LOI often sets the framework for everything that follows.

Stage one through three

The front end is usually quieter than buyers expect, but it matters.

Pre-LOI scoping

You decide what you're buying, what assumptions need testing, and whether the target fits your goals.Confidentiality and information exchange

The NDA gets signed, the seller starts sharing information, and the buyer begins assessing whether a real transaction is possible.Letter of intent

The LOI outlines the major business terms and creates a roadmap for diligence and drafting. A sloppy LOI often produces expensive arguments later because the parties thought they agreed on the same thing when they didn't.

Stage four through closing

After the LOI, the deal gets real.

| Stage | What happens | Why it matters |

|---|---|---|

| Due diligence | Buyer and advisers test the seller's claims | This is where hidden problems usually surface |

| Purchase agreement negotiation | The parties convert business terms into binding obligations | Risk allocation gets written into enforceable language |

| Closing coordination | Consents, lender items, signatures, funds flow, and final deliveries come together | A missed deliverable can delay or derail the transaction |

What buyers get wrong about timing

First-time buyers often assume that if both sides are motivated, the deal should move quickly. Motivation helps. It doesn't eliminate dependencies.

A lender can delay closing. A landlord can hold up an assignment. A customer contract may require consent. A diligence issue may force repricing or a change in structure. The process slows down because unresolved issues need decisions, and those decisions affect risk.

A disciplined buyer doesn't ask, “How fast can we close?” The better question is, “What has to be confirmed before closing is safe?”

The stage after everyone stops paying attention

Closing is not the finish line in the practical sense.

The handoff after closing often determines whether the acquisition performs the way the buyer expected. Employee communication, vendor continuity, operational control, and seller transition obligations all matter immediately. Many legal problems that seem small before closing become expensive after the buyer takes over and has fewer remedies.

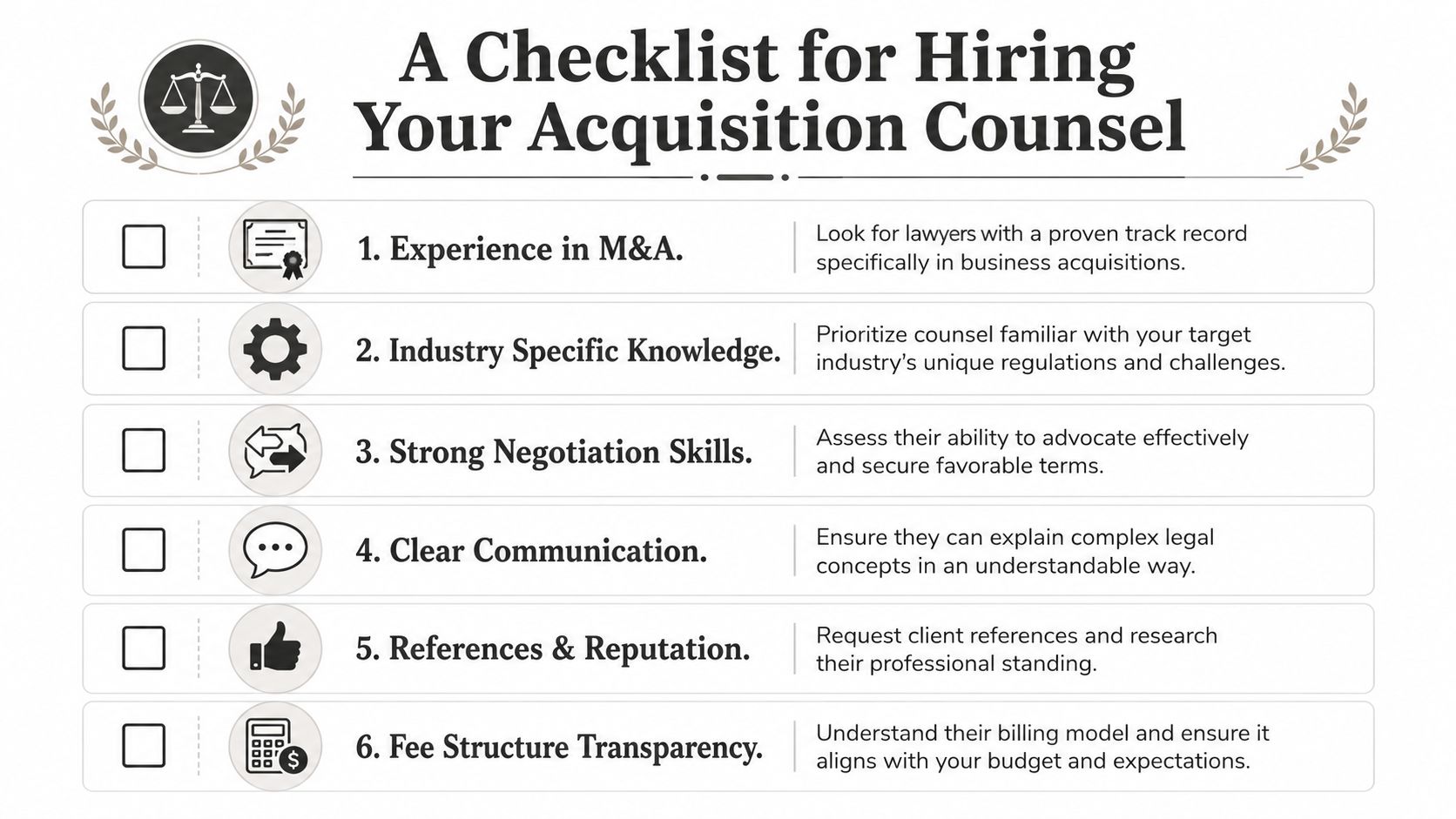

A Checklist for Hiring Your Acquisition Counsel

Most buyers interview lawyers too casually. They ask whether the attorney handles M&A, hear “yes,” and move on.

That's not enough.

The right small business acquisition lawyer should be able to reduce risk during diligence, not merely produce documents at the end. You're hiring judgment under pressure. You want someone who can spot a problem, explain the consequence in plain language, and tell you whether to renegotiate, accept the issue, or walk away.

Questions to ask before you hire

Start with direct questions. Don't ask for broad assurances. Ask how they work.

What kinds of acquisitions do you handle?

You want specific experience with business purchases, not general business law with occasional deal work.Who will run my matter day to day?

Sometimes the person you meet isn't the person who will do the work. That's not necessarily bad, but you need clarity.How do you handle diligence issues that surface late?

The answer should involve triage, risk ranking, and practical recommendations. If the response sounds like “we'll document whatever you decide,” keep looking.How do you communicate problems?

Some lawyers send long emails without a recommendation. Others call with a bottom-line view. You need a style that helps you make decisions.Have you worked with SBA-backed acquisitions or lender-driven closings?

If your deal involves financing, your lawyer should be comfortable coordinating with lending requirements rather than treating them as someone else's issue.

For buyers considering lender-backed acquisitions, industry commentary such as this Barlow Williams review for SBA buyers can help frame the kinds of service models and deal support structures that matter in smaller transactions.

Red flags that deserve attention

Some warning signs appear before engagement. Pay attention to them.

Vague answers

If a lawyer can't explain how they approach diligence, negotiation points, or closing coordination in simple language, they may not be the right fit for a first-time buyer.

Purely reactive posture

You don't want counsel who waits for the seller's draft and then comments line by line without discussing business consequences. Drafting matters, but timing and negotiating strength matter too.

No clear process

A good deal lawyer usually has a method. They know when to push diligence, when to bring in a CPA, when to flag assignment issues, and when to escalate a term because it could become a dispute later.

Buyer's test: Ask, “How would you help me decide whether a problem is fixable or a deal breaker?” The quality of that answer tells you a lot.

Fee structures and what they mean

Legal fees aren't just about price. They affect behavior.

| Fee approach | What it can work well for | What to ask |

|---|---|---|

| Hourly | Deals with uncertain scope or changing issues | How often will I receive updates and budget check-ins? |

| Flat fee for defined phases | Standardized work like an LOI or a limited review | What is included, and what triggers extra billing? |

| Hybrid or phased model | Transactions where early diligence may determine whether to proceed | Which tasks belong to each phase? |

The best fee conversation is concrete. You should understand what work is included, what assumptions the estimate depends on, and what kinds of events typically increase cost.

Fit matters as much as credentials

You need competence, but you also need alignment. If your lawyer is overly aggressive, they can create friction where none is needed. If they're too passive, they can miss the moment to improve terms.

Some buyers also want counsel with broad commercial capability beyond the deal itself. That can matter when the acquisition raises follow-on issues involving contracts, governance, or disputes. Firms like Kons Law handle business transactions and related commercial matters, which can be relevant if the acquisition evolves into post-closing contract, governance, or litigation questions.

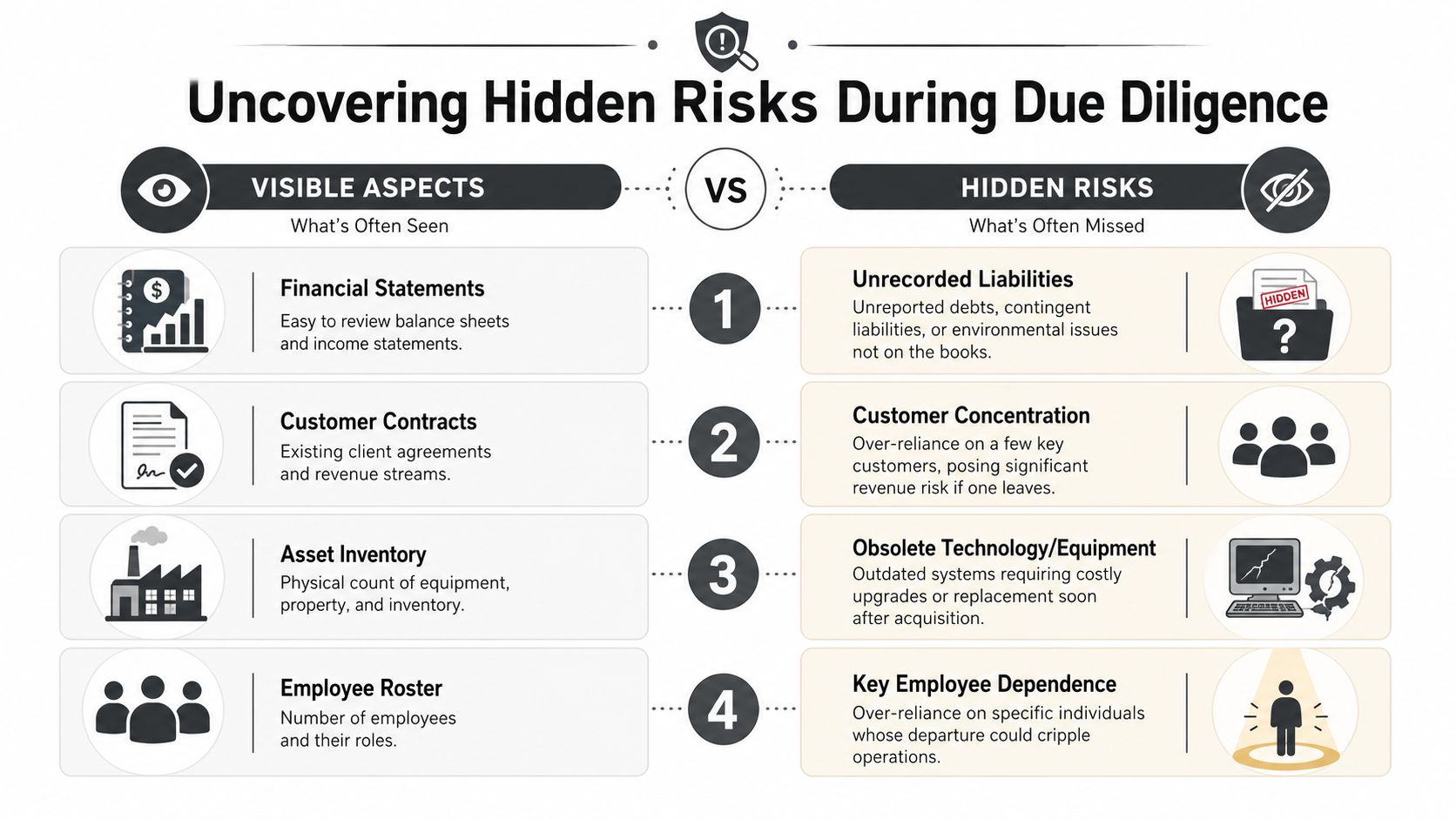

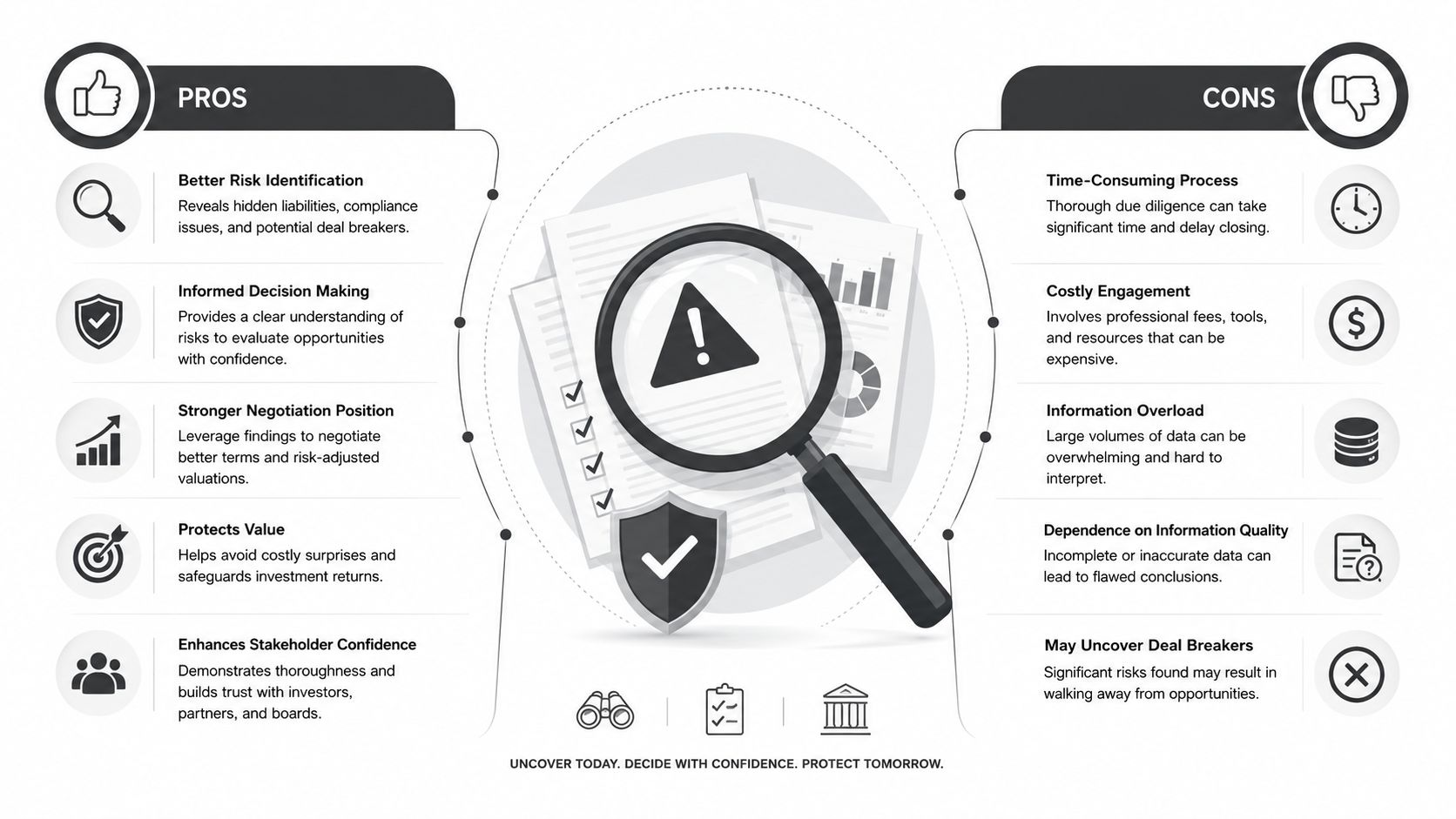

Uncovering Hidden Risks During Due Diligence

Financial diligence gets attention because it's easier to visualize. Revenue trends, margins, and EBITDA feel measurable. But many acquisition problems come from operational and legal issues that don't show up neatly in a spreadsheet.

Recent public commentary on transaction practice has emphasized that many deals break because non-financial operational issues are missed during diligence, including contract assignability, employee onboarding, regulatory compliance, and post-closing integration. It also notes that as timelines tighten, lawyers are increasingly expected to identify these surprises before closing rather than merely paper the deal afterward, as discussed in this market commentary on diligence and legal risk.

If you're evaluating a target now, this guide on buying a business due diligence is a useful companion to the legal issues below.

Contracts that don't move the way you expect

A customer contract can look valuable and still fail you after closing.

In an asset deal, many contracts must be assigned. That often requires consent. If consent is withheld, delayed, or conditioned on new terms, the contract you thought you were buying may not be available on the same economics. The same issue can affect supplier agreements, leases, software licenses, and distribution arrangements.

Your lawyer should identify not only whether assignment is allowed, but also whether a change of control clause creates trouble in an equity transaction. Those details affect continuity on day one.

Employees and the practical problem of continuity

The employee roster rarely tells the full story.

The issue isn't just who is on payroll. It's who knows the customers, who manages the systems, who controls vendor relationships, and whether they're likely to remain after the seller exits. Employment agreements, restrictive covenants, classification issues, accrued obligations, and onboarding requirements all deserve review.

For transactions involving outsourced HR arrangements or co-employment structures, specialized resources on conducting PEO due diligence can help buyers understand employment-related exposure that doesn't always appear in standard diligence checklists.

Miss an employee issue, and the business may close on schedule but stumble in operation immediately.

Compliance, licenses, and post-closing friction

Some businesses operate with informal habits that worked for the seller but won't work for the buyer.

Regulatory compliance problems can remain undetected until ownership changes. A permit may be out of date. A license may not transfer. A required policy may exist only on paper. These aren't abstract legal defects. They can interrupt operations, trigger remediation costs, or give counterparties an advantage after closing.

Integration problems that start before closing

Post-closing integration is often treated like an operational detail. It isn't. It starts during diligence.

A lawyer helps define what the seller must deliver at closing and after closing. That can include transition services, employee handoffs, access to systems, introductions to key counterparties, and cooperation on consents. If those items are left vague, the buyer may own the company but still struggle to operate it.

Preparing for Your First Call with a Business Lawyer

A productive first call saves time and sharpens the advice you receive. It also tells the lawyer that you're approaching the acquisition with discipline rather than momentum alone.

Practical guidance from the U.S. Chamber on preparing for a small-business acquisition stresses that buyers should assemble an M&A attorney plus a CPA and financial adviser, verify financials early, and keep the process confidential. It also frames a useful benchmark for counsel selection: choose a lawyer who can reduce deal risk during diligence rather than only paper the closing.

What to have ready

Bring order to the first conversation. You don't need a perfect file, but you should have the basic materials organized.

The seller materials you already have

That may include a teaser, offering memorandum, draft LOI, or financial package.Your objectives

Are you buying for cash flow, strategic fit, industry entry, or owner-operator transition? The legal advice changes depending on the goal.Your known deal terms

Price is only part of it. Note whether financing, seller rollover, earnout concepts, employment transition, or real estate are part of the discussion.Your concern list

Write down what already worries you. Customer concentration, lease issues, key employees, licensing, pending disputes, or seller involvement after closing.

What to ask on the call

Use the consultation to test how the lawyer thinks.

Ask where they see immediate risk. Ask what documents they want first. Ask how they would sequence diligence. Ask what could force a repricing, a structural change, or a decision not to proceed.

You're not looking for guarantees. You're looking for judgment.

Confidentiality and team discipline

Loose communication creates unnecessary risk in acquisitions. Limit who knows about the transaction, keep documents centralized, and involve your CPA early so legal and financial diligence develop together rather than in separate tracks.

That coordination often determines whether issues surface in time to matter.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.