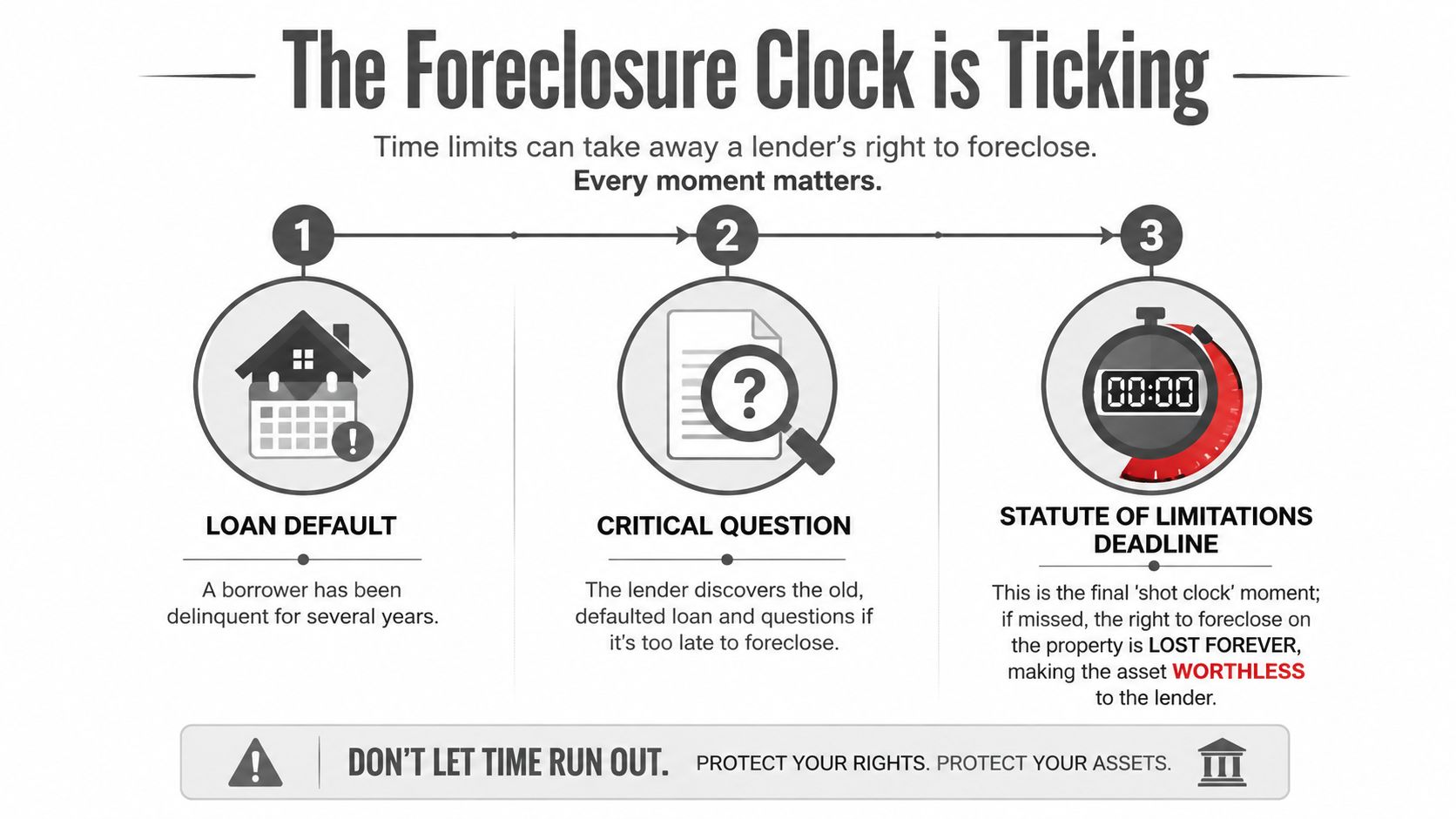

A lender reviews a legacy file, sees a loan that has been in default for years, and asks the only question that matters at that point: can we still enforce the mortgage, or has the deadline passed?

That question doesn't belong in the clean-up phase. It belongs at intake, at transfer, at every workout review, and before any dismissal decision. The foreclosure statute of limitations is not a technical side issue. It is the deadline that can convert a secured position into a litigation problem. In some circumstances, the debt may still exist while the foreclosure remedy is gone.

Experienced creditors usually know the broad rule that old claims become harder to enforce. The mistake is assuming foreclosure timing is simple. It usually isn't. The actual analysis turns on the governing state's law, the loan documents, whether and when the debt was accelerated, what happened in earlier litigation, and whether any stay, tolling doctrine, or saving statute applies.

The Time-Sensitive Nature of Foreclosure Rights

A servicing transfer lands on counsel's desk after years of delay. The borrower has been in default, there were workout discussions, someone may have sent a demand letter, and an earlier action may have been filed and dropped. Before anyone talks settlement, title strategy, or a new complaint, one question has to be answered. Is the foreclosure remedy still alive?

That question drives value. A mortgage that looks fully secured on a balance sheet can become far less useful if the limitations period has run or is close enough to create a serious defense. In that posture, the issue is not abstract procedure. It is enforceability, recoverability, and litigation risk.

For that reason, aged mortgage files should be triaged as deadline matters. They should not be treated as ordinary collections inventory waiting for the next outreach cycle.

Across the country, foreclosure limitations periods vary, and the controlling analysis is often more technical than business teams expect. The governing state law matters. The loan documents matter. The file history matters. Judicial and nonjudicial states can frame the remedy differently, and states also differ on whether the controlling period tracks the note, the mortgage, or both. Connecticut adds its own layer of discipline because counsel must evaluate the remedy under state-specific rules rather than rely on a generic national servicing timeline.

For Connecticut creditors and investors reviewing related enforcement rights, this discussion of the statute of limitations in Connecticut is a useful companion reference. The practical point is straightforward. A claim may look collectible in the abstract, yet still be impaired if the wrong deadline governs the chosen remedy.

Where creditors get into trouble

The expensive mistakes usually start in operations and then become legal problems:

- Legacy file reviews start too late: Aged defaults are left in special servicing or workout status without a documented limitations analysis.

- Prior enforcement activity is missed: Earlier complaints, dismissal orders, acceleration letters, bankruptcy stays, or reinstatement efforts are not assembled into one timeline.

- Teams track delinquency dates only: They can identify missed payments but cannot show the event that actually matters for limitations purposes.

- Exit decisions are made without limitations counsel: A discontinuance, withdrawal, or long pause in prosecution may affect later enforcement strategy.

Those risks are magnified after the last few years of moratoriums, court slowdowns, and shifting loss mitigation practices. Older files often contain mixed signals about default, acceleration, de-acceleration, tolling, and borrower communications. That is one reason I tell clients to build the timeline before they build the case.

If the borrower has a credible statute of limitations defense, the balance of power shifts quickly. Settlement ranges narrow. Title issues become more prominent. Reserve assumptions may need to be revisited. By the time that defense appears in a motion to dismiss or summary judgment briefing, the lender has already lost strategic ground.

What Really Starts the Clock Acceleration vs Default

The most common oversimplification in foreclosure timing is the statement that the clock starts with the first missed payment. Sometimes that installment default matters. But in many foreclosure matters, acceleration is the event that changes everything.

Acceleration means the lender elects to declare the entire debt immediately due, rather than pursuing only the missed installments as they come due. Once that election occurs, the legal analysis often shifts from a series of separate payment defaults to a single claim for the full balance.

Default is not always the trigger

A borrower may miss one payment, then another, then several more. That alone does not always mean the foreclosure statute of limitations on the full debt has started. The decisive event is often a formal act showing the lender has exercised its contractual right to accelerate.

That act can appear in several places:

- A notice of acceleration

- A default letter demanding the full balance

- A foreclosure complaint that calls the entire amount due

New York commentary highlights this point directly. A foreclosure action is generally subject to a six-year limitations period, and courts may treat the clock as starting when the lender accelerates the debt in the complaint, not merely when payments stop, as explained in this discussion of FAPA and acceleration-based limitations analysis.

Why this distinction changes case outcomes

Suppose a borrower stopped paying years ago, but the lender never clearly accelerated. The limitations analysis may look very different from a file where the lender sent a full-balance demand early and then did nothing. In the first file, some claims may still be viable. In the second, the lender may have started a single clock running on the whole debt.

That is why I tell clients to stop asking only, "When did the borrower default?" and start asking, "What document proves the lender elected acceleration, and on what date?"

The file usually turns on the document trail, not on anyone's memory of what servicing intended.

A clean timeline often requires review of the loan file, correspondence, prior pleadings, and the underlying promissory note. If the note and mortgage authorize acceleration only after specific notice requirements, you need to know whether those steps were taken and documented.

What works and what doesn't

What works:

- Contemporaneous records that show exactly when acceleration occurred

- Uniform template language that distinguishes between a default notice and a full acceleration notice

- Litigation files tied to servicing records so the complaint date and demanded relief are easy to verify

What doesn't:

- Loose servicing shorthand that labels every serious default as "accelerated"

- Assuming dismissal erased the earlier election

- Relying on the first missed payment as a universal trigger

In foreclosure statute of limitations analysis, precision beats instinct. If your team can't identify the legally operative acceleration event, you are not managing timing risk. You are guessing.

Impact of Judicial vs Nonjudicial Foreclosure

The foreclosure process itself changes the timing analysis. A lender in a judicial foreclosure state is playing a different procedural game from a lender in a nonjudicial state. The same aged loan can present different statute issues depending on how state law requires the remedy to be pursued.

Judicial foreclosure

In a judicial state, the lender must commence a lawsuit. That means the filing of the complaint often becomes the event that matters most for deadline compliance. If the governing limitations period expires before suit is filed, the lender may be out of time regardless of how strong the payment default evidence is.

Judicial foreclosure also creates a richer record for limitations disputes. The complaint may show acceleration. The docket may show dismissal type. Prior actions become easier to track, but they also become easier for the borrower to use as a time-bar defense.

For creditors pursuing lien rights or related remedies, the underlying framework often overlaps with broader secured-creditor issues such as foreclosing a lien, where commencement rules and statutory prerequisites matter just as much as the merits.

Nonjudicial foreclosure

In a nonjudicial state, the lender may proceed under a deed of trust or power-of-sale framework without filing a standard foreclosure complaint first. That changes the operational question. Instead of asking whether the lawsuit was filed on time, counsel may need to ask whether the lender timely initiated the nonjudicial process through the correct statutory or recorded step.

That is where many national servicing assumptions fail. A file-management protocol built around complaint dates may not capture the controlling event in a nonjudicial jurisdiction.

Why one workflow doesn't fit both

Here is the practical comparison:

| Process type | Typical enforcement mechanism | Timing risk focus |

|---|---|---|

| Judicial foreclosure | Court action | Whether suit was commenced before the deadline |

| Nonjudicial foreclosure | Contract and statute-based sale process | Whether the required initiating step occurred before the deadline |

If your platform tracks only "date suit filed," it is incomplete for a multi-state foreclosure operation.

The strategic trade-off is straightforward. Judicial systems produce clearer litigation records but can create hard docket consequences when cases stall or are dismissed. Nonjudicial systems may move differently, but they demand close attention to statutory steps and the precise act that counts as commencement. Creditors who collapse those two systems into one generic workflow create avoidable limitations exposure.

State Law Variations with a Focus on Connecticut

A lender with a performing New York workflow can still mishandle a Connecticut file. The mistake usually starts with a bad assumption that one limitations rule, one trigger, and one enforcement playbook travel cleanly across state lines. They do not.

Foreclosure timing is controlled primarily by state law, and the differences are not cosmetic. State law determines which claim matters, which event starts the limitations analysis, and what procedural posture changes the risk. For a Connecticut loan, that means counsel must read the note, mortgage, modification history, and prior enforcement record together instead of importing a rule from another market.

Connecticut demands a file-level review

Connecticut is not a state where a creditor should rely on a shorthand answer. The analysis often separates the note from the mortgage remedy, then asks how Connecticut statutes, equitable foreclosure principles, and the loan documents interact in the actual case.

That changes strategy.

A creditor may have a colorable claim on the note and still face arguments about the foreclosure remedy, prior acceleration, abandonment of acceleration, maturity, or the effect of earlier litigation activity. Strict foreclosure and foreclosure by sale also bring procedural realities that business teams need to account for early, especially if the loan has already been through a workout, a dismissal, or a transfer between servicers.

A disciplined Connecticut review usually focuses on four questions:

- Which obligation is being enforced? The note, the mortgage lien, a guaranty, or more than one at the same time.

- Which date matters under the documents and the procedural history? Maturity, an acceleration notice, a prior complaint, or another operative event.

- What happened in earlier cases or loss-mitigation periods? Withdrawals, dismissals, bankruptcy stays, payment arrangements, and modifications can all affect the analysis.

- What remedy makes business sense now? Filing immediately is not always the best move if the record on acceleration or standing needs repair first.

That last point is often missed. Speed helps only if the file can survive scrutiny.

Other states show why shortcuts fail

Connecticut stands out, but the broader national comparison matters because many servicing platforms and investor reports still reduce limitations analysis to a single field. That is unsafe in a multi-state portfolio.

New York remains the clearest example of an acceleration-centered system. Foreclosure actions are generally subject to a six-year limitations period under CPLR 213(4), and disputes often turn on whether and when the debt was accelerated, then whether later conduct changed that result. Recent legislative and appellate developments have made that framework less forgiving for lenders that once relied on dismissal and refiling strategies, as noted earlier.

New Jersey creates a different problem. Legal Services of New Jersey's summary of the current statute explains that the state now applies a six-year filing limit in many foreclosure matters under N.J.S.A. 2A:50-56.1, while older loans can still raise different timing questions based on origination date and statutory fit. For a creditor, that means loan vintage is not a background fact. It is part of the limitations analysis.

Florida also resists simplification. Safeguard Properties' discussion of time-barred foreclosures and acceleration issues reflects the common lender-side view that mortgage foreclosure claims are often analyzed through a five-year contract limitations framework, with acceleration frequently driving the timing dispute. A servicing team that treats Florida, New York, and Connecticut as versions of the same problem will misclassify risk.

Foreclosure statute of limitations in selected states

| State | General limitation period | Practical point |

|---|---|---|

| Connecticut | Varies by claim and remedy | Review the note, mortgage, acceleration history, prior cases, and Connecticut foreclosure procedure together |

| New York | 6 years | Acceleration usually drives the limitations fight |

| New Jersey | 6 years in many current cases, with older loans raising different issues | Loan vintage can change the analysis |

| Florida | 5 years in many contract-based foreclosure analyses | Timing disputes often focus on acceleration and subsequent defaults |

For legal departments supervising a national foreclosure inventory, process control matters almost as much as legal analysis. Some teams use real estate law software to track prior accelerations, dismissal dates, maturity dates, and state-specific milestones across portfolios. The software does not answer the legal question, but it can prevent the operational errors that create avoidable statute defenses.

The Connecticut takeaway is practical. Ask for a Connecticut answer based on the actual file, not a national summary dressed up as local advice.

Tolling Rules and Modern Post-Pandemic Issues

Even after you identify the likely trigger and applicable period, the analysis may not be finished. Borrowers and lenders often fight over whether something paused the clock, extended it, or preserved rights long enough to permit a later filing.

That inquiry is dangerous because many business teams treat delay events as self-explanatory. Courts usually don't.

Traditional tolling questions

Several events commonly raise tolling or preservation arguments:

- Bankruptcy filings: The automatic stay can affect what the lender may do during the stay period.

- Written acknowledgments or later agreements: In some jurisdictions, those facts can matter, but only if they satisfy the governing legal standard.

- Partial payments: These are heavily state-specific and should never be assumed to revive or extend a claim.

- Prior litigation stays or injunctions: The legal effect depends on the source of the stay and the governing statute or case law.

The practical lesson is that tolling arguments are document-intensive. If a creditor plans to rely on one, the file must show the event, the dates, and why that event legally alters the running of time.

Moratoriums created a hidden risk

The post-pandemic foreclosure environment made this more complicated. Many lenders delayed enforcement because they were subject to executive, judicial, or regulatory holds. That felt protective at the time. It may not prove protective in later statute litigation.

Recent lender-side commentary warns that foreclosure moratoriums at the regulatory, executive, and judicial level may not protect servicers from later statute-of-limitations challenges, meaning delay can create hidden lien-enforcement risk even when the lender was complying with a hold. That analysis emphasizes that whether the stay was mandatory and whether the note had already been accelerated before the pause can become critical, as discussed in this review of foreclosure holds and limitations exposure.

What creditors should document now

When a file includes a hold period, counsel should pin down:

- Who imposed the hold

- Whether it was mandatory or internal

- The exact start and end dates

- Whether acceleration predated the pause

- What steps, if any, were taken to preserve rights

Delay for compliance purposes and delay that tolls a statute are not the same thing.

What works in these files is disciplined chronology. Build a timeline that includes default, acceleration, stays, workout activity, bankruptcy events, and prior dismissals. What doesn't work is assuming a court will view every pandemic-era pause as a legal extension. Some will not.

Creditor Strategies for Managing Enforcement Deadlines

The best foreclosure statute of limitations defense is the one your borrower never gets to raise because your file management prevented the issue. That requires process, not just good instincts.

Track the dates that actually matter

Many lenders track payment delinquency well and litigation deadlines poorly. That is backwards for aging loans. The file should identify the dates that could control enforceability, not just collections performance.

At a minimum, your system should capture:

- Acceleration date

- Complaint filing date

- Dismissal date and dismissal reason

- Any stay period

- Any later event claimed to toll or preserve the action

For legal departments exploring technology-enabled workflows, broader conversations about streamlining corporate law with AI can be useful. The value isn't in replacing legal judgment. It is in reducing missed triggers, inconsistent data entry, and fragmented matter records.

Dismissals are not administrative details

One of the most costly assumptions in foreclosure practice is that a dismissed case can be refiled later. Sometimes it can. Sometimes the dismissal itself defines the next move. Sometimes it ends the remedy.

New York provides a sharp illustration. CPLR 205(a) is a limited saving statute that can allow a second foreclosure action within six months of termination of the first action, but not if the earlier case ended by voluntary discontinuance, lack of personal jurisdiction, or neglect to prosecute, as explained in this analysis of strict foreclosure timing and CPLR 205(a).

That rule captures a larger point that applies well beyond New York. The reason a case ended matters.

A practical enforcement checklist

Use a checklist before any closure, discontinuance, transfer, or refile decision:

- Reconstruct the full litigation history: Search prior dockets, old counsel files, and servicing notes.

- Confirm whether acceleration occurred: Don't assume. Verify the operative document.

- Classify the dismissal correctly: Voluntary, jurisdictional, prosecution-related, merits-based, or procedural.

- Test the refile theory before filing: Saving statutes are narrow and heavily conditioned.

- Align litigation and servicing teams: A date known to one group but not the other can sink the file.

For businesses active in collections and enforcement, these practices fit naturally within a broader creditor rights law framework. The same discipline that protects judgments and liens also protects foreclosure rights.

A foreclosure file rarely fails because the debt disappeared. It fails because the dates were handled casually.

What works is early lawyer review of aged defaults, disciplined trigger-date tracking, and formal approval before dismissal. What doesn't work is treating foreclosure as a recoverable remedy no matter how long the file has been sitting.

FAQs and Your Next Steps

Can a borrower raise the foreclosure statute of limitations even if the debt is still unpaid

Yes. As a practical matter, the defense attacks the enforceability of the foreclosure remedy. An unpaid debt doesn't automatically preserve the right to foreclose forever.

If a borrower makes a partial payment later, does that revive the lender's rights

Maybe, maybe not. That depends on state law, the timing, and the form of the payment or acknowledgment. Creditors should not assume a late payment revives an expired foreclosure claim.

Can a dismissed foreclosure case be refiled

Sometimes. The answer usually turns on the applicable state rule, the reason for dismissal, and whether any saving statute applies. A creditor should evaluate the dismissal order before assuming refiling is available.

Does a pandemic-era hold automatically stop the clock

No. Some hold periods may support a tolling or preservation argument, but that issue is highly jurisdiction-specific and fact-specific. A mandatory stay is different from an internal delay or a voluntary pause in enforcement.

What is the first document counsel should review in an aged foreclosure file

Usually the chronology should begin with the note, mortgage, any modification documents, and the earliest record that may show acceleration. After that, review prior complaints, notices, dismissal orders, and bankruptcy filings.

The core lesson is simple. The foreclosure statute of limitations is unforgiving, state-specific, and heavily dependent on the file history. Lenders who treat it as a routine back-office issue often discover the problem when the borrower raises it as a complete defense. By then, the available options may be narrow.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.