A Connecticut business owner often reaches this issue at the same moment growth starts to feel real. You need another set of hands. A bookkeeper. A salesperson. A project manager. A developer. Someone says, “Just bring them on as a contractor for now,” and that sounds simple enough.

It usually isn't.

The definition of employee vs independent contractor affects taxes, payroll, overtime exposure, unemployment issues, workers' compensation, benefits disputes, and the way a state agency or court will view your business practices if a problem arises later. The mistake many owners make is treating classification as a paperwork choice. It's not. It's a legal conclusion based on how the relationship works in practice.

That's especially important in Connecticut, where federal guidance is only part of the analysis. A worker might look like a contractor under one framework and still be treated as an employee under a stricter state standard. That gap catches businesses off guard.

Before making hiring decisions, many owners also weigh whether to build internally or outsource specific functions. That broader business analysis matters because staffing structure and legal classification often overlap. A useful resource on that operational side is this discussion of analyzing corporate outsourcing and software development costs, particularly if you're deciding whether to engage outside talent at all.

The Critical Decision Every Business Faces

A common scenario looks like this. A company lands more work than its current team can handle. The owner wants flexibility, lower overhead, and less administrative burden, so classifying the new hire as an independent contractor seems like the efficient move.

Then the operational reality starts to change. The company sets the worker's hours. It gives the worker a company email address, internal systems access, and weekly reporting obligations. The worker does the same core work as existing staff and doesn't really have another client base. On paper, the agreement says “independent contractor.” In practice, the relationship may say something else.

Why this decision carries real risk

If the classification is wrong, the fallout can spread across several areas at once:

- Tax exposure means payroll withholding issues can surface after the fact.

- Wage claims can follow if the worker should have been treated as nonexempt staff.

- Benefits disputes may arise when a worker claims eligibility for programs reserved for employees.

- Agency review can force the business to defend not just a contract, but its day-to-day management of the worker.

Practical rule: If you control the person like staff, calling them a contractor usually won't solve the problem.

The Connecticut angle businesses miss

Generic online guidance usually focuses on federal rules. That's helpful, but incomplete for a Connecticut employer. State law can be stricter, and in many situations the state standard drives the practical result.

That's why business owners need more than a label, a template agreement, or a quick payroll decision. They need a working definition they can apply before the relationship starts, and they need to understand which legal test matters for the issue in front of them.

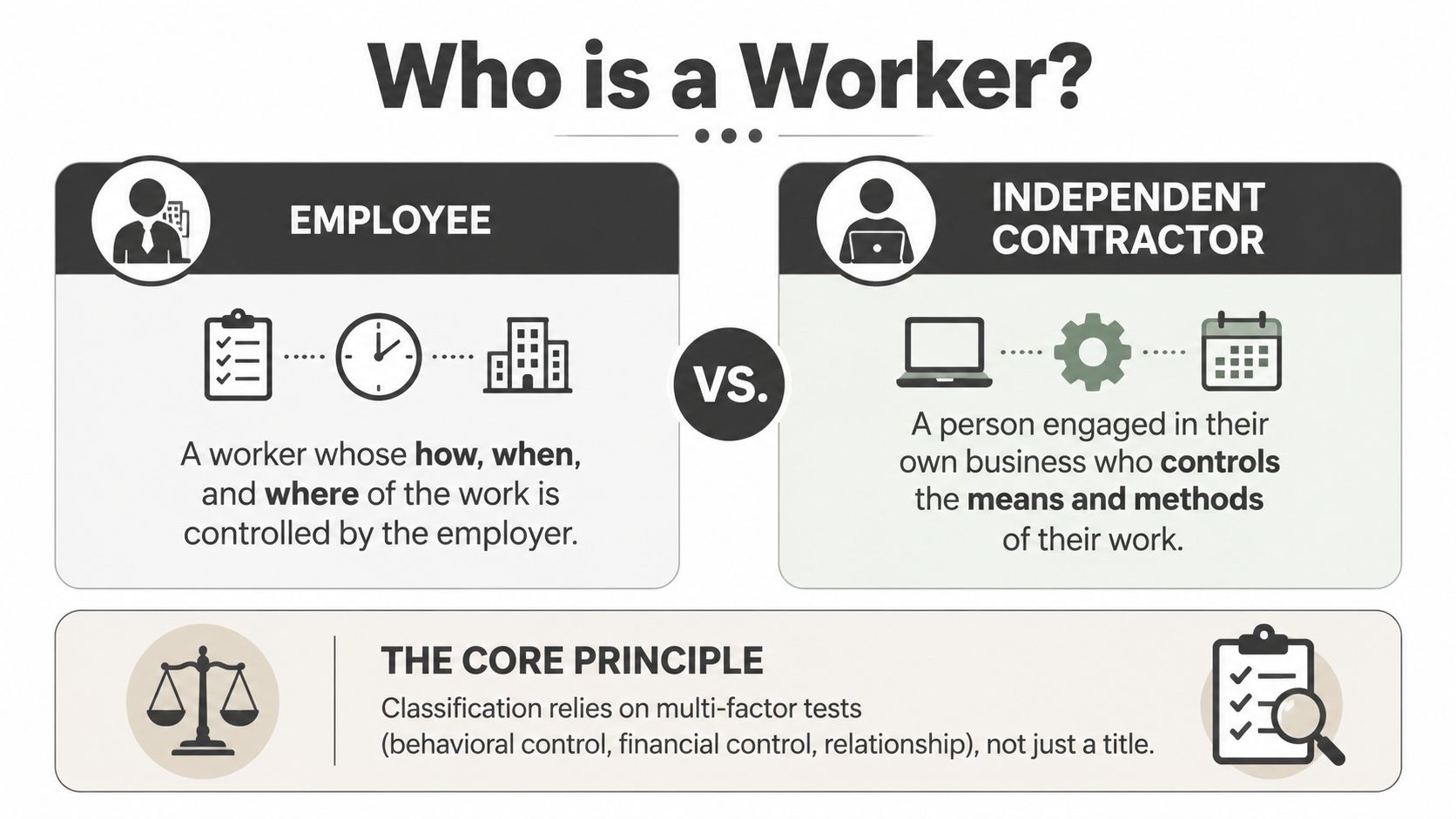

Defining Employee and Independent Contractor Status

At a practical level, an employee is a worker the business controls in meaningful ways. That control often shows up in the details of performance: when the work happens, how it gets done, what tools are used, and how closely the person is supervised.

An independent contractor is different. The contractor operates as a separate business, controls the means and methods of the work, and usually takes on some degree of business risk. The contractor is engaged to produce a result, not to function like in-house staff under routine direction.

Titles don't control the outcome

One of the most important points in this area is also one of the most overlooked. U.S. law has long treated classification as a multi-factor analysis, not a single checkbox exercise. The IRS explains that businesses must weigh behavioral control, financial control, and the relationship of the parties, and there is no “magic” number of factors that decides the issue. The same IRS guidance also notes an industry source stating that about 36% of the U.S. workforce is classified by the Department of Labor as independent contractors, which helps explain why this question comes up so often in modern business operations. See the IRS discussion of independent contractor or employee classification factors.

That framework matters because many businesses still rely too heavily on labels like these:

- “They signed a contractor agreement.”

- “We pay by invoice.”

- “They asked to be 1099.”

- “They work remotely.”

None of those facts settles the issue by itself.

What the categories usually look like in practice

A worker is more likely to look like an employee when the business directs the details, supplies the tools, integrates the person into ongoing operations, and expects a continuing relationship.

A worker is more likely to look like a contractor when the person offers services to the market, brings their own process, negotiates project scope, and has room to profit or lose based on how they run their work.

For owners who want a payroll-level explanation of forms and filing treatment, this overview helps compare 1099 and W4 worker classifications. It's useful for administration, but it shouldn't replace the legal classification analysis.

The right question isn't “What did we call this person?” The right question is “How does this relationship actually function?”

The Legal Tests Federal vs Connecticut Standards

The hardest part of the definition of employee vs independent contractor is that there isn't just one test. Different agencies and statutes ask different questions. For Connecticut businesses, that creates a compliance gap. Federal standards may feel familiar, but state law can be stricter and more outcome-determinative.

Here's the quick comparison.

| Test | Main focus | What businesses should watch |

|---|---|---|

| IRS common law approach | Behavioral control, financial control, and relationship of the parties | Who directs the work, who bears financial risk, and what the overall relationship looks like |

| DOL economic realities approach | Whether the worker is economically dependent on the business or operating an independent business | Profit or loss opportunity, investment, permanence, control, integration, skill and initiative |

| Connecticut ABC Test | Whether all three required elements are satisfied | Even one failed element can push the worker toward employee status |

Federal standards

The IRS approach asks whether the business has the right to control the details of the work. That analysis is usually grouped into three areas: behavioral control, financial control, and the nature of the relationship.

The Department of Labor uses a different lens under the Fair Labor Standards Act. The DOL asks whether the worker is economically dependent on the business or is instead operating an independent business. The DOL identifies factors including opportunity for profit or loss, investment in equipment or materials, permanence of the relationship, degree of control, whether the work is integral to the business, and the worker's skill and initiative. The agency's summary appears in its fact sheet on the employment relationship under the FLSA.

That difference matters. A business can lose the argument even where it avoids direct micromanagement if the worker still looks economically tied to the company rather than in business for themself.

Connecticut's stricter ABC Test

Connecticut employers need to pay close attention here. For state-law purposes, the ABC Test is often the more demanding standard.

A business generally must satisfy all three parts:

- A means freedom from control and direction in how the service is performed, both under the contract and in actual practice.

- B means the service is outside the usual course of the business, or outside all the places of business of the enterprise, depending on the statutory setting and facts.

- C means the worker is customarily engaged in an independently established trade, occupation, profession, or business of the same nature as the service performed.

A worker can look like a contractor under a looser federal analysis and still fail Connecticut's ABC Test.

Part B causes problems for many companies. If you run a marketing agency and hire a “contractor” to do client marketing work, the business may struggle to argue that the work is outside its usual course. If you run a construction company and bring in a “contractor” to perform core field labor under your direction, the same issue appears quickly.

Part C creates a separate trap. A person who works only for your company, has no established business presence, and depends on your assignments may not look independently established, even if the contract says otherwise.

For a broader discussion of recurring classification disputes, this article on contractor employment law issues is a useful companion.

What actually works

Businesses usually make better classification decisions when they test the world facts, not just the draft agreement. Ask whether the worker can market services elsewhere, turn a profit through managerial decisions, bring their own business infrastructure, and stay outside your core operational chain.

If the answer is no, calling the person a contractor is often wishful thinking.

Key Implications of Worker Classification

After the legal label is set, the business consequences follow. Classification then becomes more than a doctrinal question. It affects payroll systems, insurance obligations, worker expectations, and dispute exposure.

Employee vs contractor at a glance

| Factor | Employee (W-2) | Independent Contractor (1099) |

|---|---|---|

| Tax handling | Employer generally withholds payroll taxes | Worker generally handles own tax payments |

| Work control | Employer typically controls schedule and methods to a greater degree | Worker typically controls how the job is performed |

| Benefits | May be eligible for employer-sponsored benefits | Usually not covered by employee benefit programs |

| Overtime issues | May raise wage and hour questions depending on exemption status | Usually outside ordinary employee overtime structure, but misclassification can trigger claims |

| Workers' compensation and unemployment | Employer usually carries related obligations | Business generally seeks to avoid those obligations, if classification is valid |

| Relationship style | Ongoing and integrated into operations | Project-based or business-to-business in character |

Taxes and payroll administration

For employees, the company generally handles withholding and payroll administration. That means the business carries routine compliance responsibilities from the start.

For contractors, the worker generally handles their own taxes. That can feel simpler on the front end, but only if the classification is right. If it isn't, what looked like administrative efficiency can become a retroactive cleanup project involving payroll treatment that should have been in place from day one.

Benefits and internal consistency

Employees may have access to health coverage, retirement plans, leave policies, handbooks, training requirements, and other company programs. Contractors usually should not be folded into those systems as if they were ordinary staff.

That operational separation matters. If a business gives a contractor the same onboarding, same manager chain, same performance review process, and same internal role as employees, the company weakens its own classification position.

If your contractor relationship looks identical to your employee relationship, a reviewer will notice.

Insurance, overtime, and related liability

Worker classification also affects how companies handle workers' compensation and unemployment exposure. Those issues often arise during separations, claims filings, or agency review rather than at the start of the relationship.

Wage and hour risk can be just as serious. If a worker was treated as a contractor but should have been classified as an employee, the company may face claims tied to hours worked, compensation practices, and overtime. Businesses dealing with compensation disputes should understand how these issues surface in practice. This discussion of overtime not being paid and related wage issues gives a practical example of where classification errors can lead.

Operational trade-offs business owners should weigh

Contractors can offer flexibility, specialized skills, and project-based scalability. That model often works well for discrete deliverables, temporary overflow, and clearly independent service providers.

Employees make more sense when the role is continuous, central to operations, closely supervised, or tied to internal systems and team management. In that setting, trying to preserve contractor status often creates more risk than value.

The High Cost of Worker Misclassification

Misclassification is expensive because it rarely stays in one lane. A single worker complaint can open multiple fronts at once, including tax issues, wage claims, unemployment disputes, and insurance questions. The business then has to defend not only the contract language, but also every practical detail of how the relationship operated.

Why the written agreement won't save a bad setup

A contract helps. It can define scope, payment terms, confidentiality, and ownership of work product. But it does not override reality.

In cross-border and multi-jurisdiction settings, that problem gets even sharper. As LEGlobal explains, labels in an agreement are not decisive, and a person may be drafted as a contractor under one regime yet still be treated as an employee under another because subordination, economic dependence, and the actual working relationship matter more than the title. The same discussion notes that this is a frequent source of surprise in disputes, audits, and benefit claims, particularly with remote work. See the analysis on employees versus independent contractors in multi-jurisdiction settings.

That matters for Connecticut businesses using remote talent in other states, out-of-state businesses engaging Connecticut workers, and companies hiring internationally while assuming the contract label will travel cleanly across legal systems.

Where the cost shows up

Misclassification problems often surface through one of these events:

- A separation goes badly and the worker files for unemployment.

- A pay dispute arises and the worker claims overtime or unpaid wages.

- An audit begins and the agency reviews similar roles across the business.

- A benefits issue develops after a long-term contractor arrangement starts to look permanent.

At that point, the company may face back taxes, wage exposure, penalties, administrative burden, and legal fees. Even when the business eventually resolves the dispute, the process can consume management time and internal records that owners didn't expect to produce.

Insurance helps, but it doesn't solve classification

Some businesses also look at risk transfer tools when reviewing their employment exposure. If you're evaluating that side of the equation, it helps to compare employment practices liability options and understand what those policies may or may not address. Insurance can be part of a broader strategy. It is not a substitute for getting worker classification right at the outset.

Remote work has made old classification mistakes easier to make and harder to defend.

A Practical Checklist for Classifying Workers

The most useful self-audit starts with operational questions, not legal conclusions. If you answer these truthfully, you'll usually see whether the relationship leans toward employee status or contractor status.

Ask these questions before onboarding

Who controls the schedule

If you set fixed hours, require attendance at routine internal meetings, or expect ongoing day-to-day availability, the relationship starts to look more like employment.Who decides how the work gets done

A contractor should usually control methods and workflow. If your managers direct the details step by step, that points the other way.Who provides tools and systems

Company-issued software access alone doesn't settle the issue, but if the worker depends on your equipment, platforms, and internal processes to perform the job, that weakens the contractor position.How is the worker paid

Project-based pricing often fits contractor status better than a recurring hourly or salary-like structure tied to indefinite service.Is the work part of your core business

This question is especially important in Connecticut. If the worker performs the same kind of service your company sells or routinely depends on, state-law risk increases.Can the worker serve other clients

A true contractor usually has room to build a business beyond your company. Exclusivity, especially informal exclusivity, can be a red flag.

Review the relationship after the contract is signed

Classification doesn't freeze when the agreement is executed. Businesses often start with a narrow contractor engagement and then drift into an employee-style relationship over time.

That's why periodic review matters. If the role expands, the control level changes, or the contractor becomes integrated into daily operations, reassess. Companies that use recurring contractor relationships should also review their documentation and agreements regularly. This guide to employment agreement review and related contract issues is a useful reminder that papering the relationship correctly is only part of the job.

Ask whether the worker could walk away tomorrow and continue operating the same business for other clients. If the answer is no, take a harder look.

Best Practices and When to Seek Legal Counsel

The best contractor relationships are built to look and function like real business-to-business arrangements. That usually means a written agreement with clear scope, defined deliverables, payment terms tied to the project, confidentiality language, and provisions that support actual independence in day-to-day work.

Operational discipline matters just as much. Don't run contractors through the same supervision model you use for employees. Don't assign them a manager who controls daily activity as if they were staff. Don't keep expanding a short-term engagement until it becomes an indefinite core role without revisiting classification.

Red flags that deserve a legal review

Some situations deserve extra caution:

- Former employees rehired as contractors

- Workers performing the company's core service

- Long-term exclusive engagements

- Roles with fixed schedules and close supervision

- Remote or multi-state arrangements

- Teams using contractor status as a default cost-saving measure

A business compliance review should also include worker classification as part of a broader legal housekeeping process. This small business compliance checklist is a useful starting point for spotting areas where an operational shortcut can become a legal issue.

Self-audits are helpful. They are not a substitute for legal analysis where the facts are close, the role is important, or Connecticut law may impose a stricter result than the federal framework suggests.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.