Selling your business is far more than a simple transaction; it's the culmination of your life's work, dedication, and vision. A business sales attorney is the legal professional who safeguards that legacy, ensuring the deal is structured to protect your interests and shield you from future liabilities. They are the architect of your successful exit.

The Indispensable Role of a Business Sales Attorney

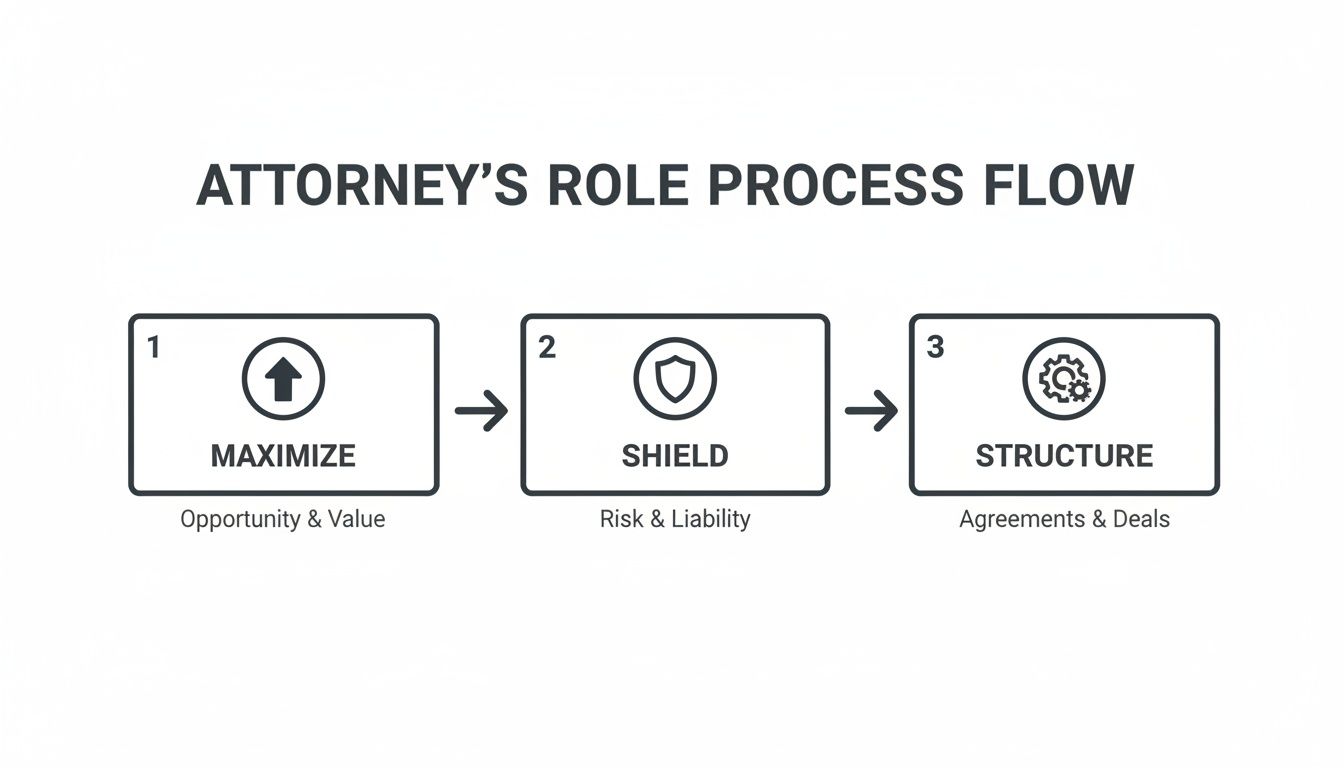

Selling a company is one of the most significant financial events an owner will ever experience. While a business broker focuses on finding a buyer, a business sales attorney’s role is to ensure the proposed deal is legally sound, financially optimized for you, and free of hidden risks. Going through this complex process without dedicated legal counsel is a gamble most entrepreneurs are wisely unwilling to take.

Think of it this way: a broker brings a potential partner to the table, but your attorney ensures the terms of the partnership are fair, the agreement is solid, and you won’t face unexpected legal troubles down the road. Their strategic guidance transforms a potentially chaotic process into a structured, secure, and profitable conclusion.

Your Advocate in Negotiations

From the very start, your attorney acts as your chief advocate. They are essential in negotiating the Letter of Intent (LOI), the foundational document that outlines the deal's most important terms. A well-drafted LOI paves the way for a smooth transaction, while a weak one can lead to disputes or even a collapsed deal.

Your attorney makes sure the key terms are structured in your favor, including:

- Price and Payment Structure: How and when you get your money.

- Exclusivity Periods: Preventing you from being locked into a single offer for too long.

- Confidentiality: Protecting your sensitive business data during the process.

The Architect of the Deal Structure

One of the most critical functions of a business sales attorney is advising on the deal's structure—most commonly an asset sale or a stock sale. This single decision has massive implications for your tax obligations, the liabilities you may retain, and the overall complexity of the transaction.

An attorney doesn't just review documents; they engineer the transaction itself. Their expertise in structuring the sale can directly impact your net proceeds by tens or even hundreds of thousands of dollars, depending on the tax consequences and liability transfer.

They analyze your company's unique position to recommend the path that best protects your financial interests, ensuring you don’t leave money on the table or take on unnecessary risk.

Your Shield During Due Diligence

Once an LOI is signed, the buyer will start an exhaustive review of your company, a process known as due diligence. Your attorney manages this critical stage, organizing the disclosure of information and responding to the buyer's requests in a way that satisfies their needs without exposing you to undue liability. They act as a crucial gatekeeper, protecting you at every turn. Understanding the full scope of what a business lawyer does can provide even more context on their value.

A business sales attorney is not a cost; they are an investment in securing the full value of what you've built. Their guidance ensures you not only get the best possible price but also achieve a clean exit, allowing you to move on to your next chapter with confidence. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Your Legal Roadmap to Selling a Business

Selling the business you’ve poured your life into is a major milestone, but it’s rarely a simple handover of the keys. The process is a legal journey with specific, high-stakes stages. An experienced business sales attorney is your indispensable guide on this path, ensuring every move you make protects your wealth and minimizes your risk.

This guide breaks down that journey. We’ll walk through the entire legal process step-by-step, starting with the single most important decision you'll make—how to structure the sale itself. Knowing what’s ahead is the best way to stay in control.

Asset Sale vs Stock Sale: The Foundational Choice

Right out of the gate, you and your attorney will decide whether to structure the deal as an asset sale or a stock sale. This choice has massive implications for your taxes, the liabilities you carry forward, and how smoothly the deal closes.

Think of it this way:

- In an asset sale, the buyer is picking specific parts of your business they want to buy—like equipment, inventory, and customer contracts. You keep the legal shell of your company, along with any liabilities the buyer doesn’t explicitly agree to take on.

- In a stock sale, the buyer is purchasing the entire company, lock, stock, and barrel. They get all the assets and, crucially, all the liabilities, whether they’re known or not. You walk away clean.

An attorney’s job is to structure this decision to maximize your outcome while shielding you from future trouble. It's a strategic process, not just paperwork.

As a general rule, buyers lean toward asset sales so they can avoid inheriting hidden problems. Sellers, on the other hand, often prefer stock sales because they typically offer significant tax advantages and a much cleaner exit. Your attorney’s first job is to negotiate the structure that puts the most money in your pocket with the least amount of future risk.

Here’s a quick breakdown of the core differences.

Asset Sale vs. Stock Sale At a Glance

| Consideration | Asset Sale | Stock Sale |

|---|---|---|

| What is Sold | Individual assets and liabilities selected by the buyer (e.g., equipment, inventory, customer lists). | The entire legal entity, including all its assets and liabilities, known and unknown. |

| Seller Tax Impact | Potentially higher taxes due to "double taxation" on C-corps and ordinary income rates on certain assets. | Generally more favorable, with proceeds often taxed at lower capital gains rates. |

| Liability Transfer | Seller typically retains liabilities not explicitly assumed by the buyer. | Buyer inherits all company liabilities, offering the seller a cleaner exit. |

| Complexity | More complex, requiring transfer of individual titles, contracts, and permits. | Simpler, as only the ownership stock or membership interests are transferred. |

Understanding these trade-offs is fundamental, as this early decision sets the tone for the entire negotiation.

The Letter of Intent: A Critical First Step

Once you have a serious buyer, you’ll move to the Letter of Intent (LOI). While not the final, binding contract, the letter of intent (LOI) for business sales lays out the main terms of the agreement and shapes everything that follows.

The LOI is where the most critical deal points are often won or lost. Having a sharp business sales attorney involved here stops you from getting locked into bad terms before the real drafting even starts.

Your lawyer will make sure the LOI contains a fair price, a clear payment structure, and a reasonable exclusivity or "no-shop" clause. They’ll set you up for success. To learn more about this crucial document, you can explore our detailed article on what a Letter of Intent is and its role in a sale.

Surviving Due Diligence

With the LOI signed, the buyer begins due diligence. This is their deep-dive investigation into your company’s financial records, contracts, employee agreements, and legal history. It’s an exhaustive process that can feel intrusive, but it’s a non-negotiable step in every business sale.

Your attorney’s role here is to act as a gatekeeper. They’ll help you prepare and organize your documents in a secure "data room" while making sure you don’t accidentally disclose privileged information or open yourself up to unnecessary risk. They manage the buyer’s endless requests so you can continue running your business.

Drafting the Definitive Purchase Agreement

This is it—the final, legally binding contract that makes the sale official. The Purchase Agreement is a dense, highly detailed document that turns the general terms of the LOI into concrete legal obligations. This is where your attorney’s expertise truly shines.

They will fight for you on several key fronts:

- Representations and Warranties: These are the promises you make about the state of your business. If a "rep" proves to be untrue, the buyer can sue you after the closing. Your attorney’s job is to fiercely negotiate the scope and duration of these promises to protect your proceeds.

- Indemnification: This clause dictates who pays for what if something goes wrong after the sale. A good lawyer will negotiate strict limits (known as "caps" and "baskets") on your financial responsibility.

- Closing Conditions: These are the final hurdles that must be cleared for the deal to close, like getting key contracts assigned or landlords to approve the transfer. Your lawyer ensures these conditions are clear, fair, and achievable.

Navigating the Closing and Post-Closing

The closing is when all the documents are signed, ownership officially transfers, and the money hits your account. Your attorney orchestrates this event, making sure every ‘i’ is dotted, every ‘t’ is crossed, and the funds are wired securely.

But the work doesn’t always end there. Many deals include post-closing obligations, like transition services or final price adjustments based on closing-day financials. Your attorney stays with you to manage these final details, ensuring the other side holds up their end of the bargain and you achieve the clean exit you deserve.

Budgeting for Your Sale Timelines and Legal Fees

When you decide to sell your business, two questions immediately jump to mind: "How long is this going to take?" and "What will it really cost me?" There’s no simple, one-size-fits-all answer. However, understanding the factors that drive the timeline and how a business sales attorney structures their fees will give you the clarity you need to plan your exit with confidence.

A typical business sale, from the moment you sign a letter of intent to the day you close, often takes between three to six months. But that's just an average. The complexity of your company, how quickly the buyer moves, and the need for outside approvals (like a landlord’s consent) can stretch or shrink that timeline considerably.

Understanding the Typical Timeline

Selling a business isn't a straight line; it's a series of overlapping stages, each with its own hurdles. I've seen it time and again: a clean, well-organized company will always move through the process faster than one with tangled financials or lingering legal issues.

Several key factors will influence your sale timeline:

- Quality of Your Records: Organized financials and corporate documents can shave weeks, if not months, off the due diligence period.

- Deal Complexity: An asset sale with dozens of contracts to assign is naturally going to take longer than a straightforward stock sale.

- Buyer and Lender Responsiveness: A motivated buyer is great, but delays on their end—or from their lender—can stall momentum for weeks at a time.

- Third-Party Consents: Waiting for landlords, franchisors, or major suppliers to approve the transfer is one of the most common bottlenecks we see.

An experienced attorney helps manage this timeline by seeing those potential delays from a mile away and proactively tackling issues before they become serious roadblocks.

Demystifying Legal Fee Structures

Legal fees are a crucial part of your budget, and you deserve total transparency. The cost reflects the immense value and protection a good attorney provides during one of the most significant transactions of your life. In a healthy legal market—the Business Lawyers & Attorneys segment in the US was valued at $191.8 billion in 2024—you absolutely have options. You can find more details on the business law market size on IBISWorld.com.

Attorneys generally use one of three fee structures for a business sale:

Hourly Billing: This is the traditional model where you pay for the actual time your attorney spends on your file. While it’s transparent, the final cost can be unpredictable, which makes precise budgeting a challenge. This approach is often best for deals where the complexity is still an unknown.

Flat Fees: For more predictable transactions, some attorneys offer a flat fee that covers the entire sale process or specific stages. This model gives you cost certainty, which is a huge relief for many sellers. You know the exact legal cost from day one, no matter how many hours it takes.

Success-Based Arrangements: Sometimes called a contingency or partial contingency, this model directly aligns your attorney’s compensation with the successful closing of your deal. It might involve a smaller upfront retainer paired with a percentage of the final sale price. This structure ensures your attorney is just as motivated as you are to get the deal done on the best possible terms.

The right fee structure really depends on your comfort with risk and the unique details of your sale. The best thing you can do is have an open conversation with potential attorneys about their models to find a fit that aligns with your goals. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Avoiding Costly Mistakes in Your Business Sale

When you sell your business, what you don’t know can absolutely hurt you. A small oversight can easily mushroom into a deal-killing conflict or, worse, a post-closing lawsuit that snatches back the proceeds you worked so hard to earn. An experienced business sales attorney is your early warning system, helping you spot these landmines long before you step on them.

Many sellers start making mistakes years before a buyer is even in the picture. The most common—and costly—is simply a lack of preparation, which often starts with disorganized financial records.

Imagine a buyer’s due diligence team asking for three years of detailed financials, and all you have are jumbled bank statements and a shoebox full of receipts. This isn't just an inconvenience; it’s a massive red flag that slows down the deal, erodes trust, and gives the buyer leverage to lower their offer.

Inadequate Preparation and Unresolved Liabilities

Good preparation goes far beyond just having clean books. A critical first step is separating business and personal finances. When you’ve been paying for business inventory with your personal credit card, it’s impossible for a buyer to see the company's true profitability. This commingling of funds is one of the fastest ways to scare a serious buyer away.

Another common pitfall is leaving outstanding liabilities unresolved. Before you go to market, you have to clean house. This includes:

- Unresolved Employee Issues: Lingering disputes over unpaid overtime, arguments about employee classifications, or unresolved HR complaints can become a buyer’s problem—and they will price that risk into their offer.

- Pending Lawsuits or Tax Issues: Any open legal claims or unresolved tax audits must be disclosed and managed. Attempting to hide them is a recipe for disaster and can lead to fraud claims.

- Environmental Concerns: For any business with a physical footprint, potential environmental contamination from past operations can be a deal-killer if not addressed proactively.

Critical Legal and Contractual Oversights

Beyond the prep work, several major legal oversights can derail a deal right before the finish line. One of the most frequent is failing to get necessary third-party consents. You might have a signed purchase agreement, but if your landlord won’t consent to assigning the lease to the new owner, your deal is dead in the water.

Many sellers mistakenly believe that the deal is "done" once the purchase agreement is signed. In reality, the most dangerous risks often lie within the fine print of that agreement, specifically in the "representations and warranties" section.

These "reps and warranties" are legally binding promises you make about the state of your business. If a buyer discovers after closing that you breached a promise—for example, that a key customer contract wasn't as secure as you claimed—they can sue you. A sharp business sales attorney will fiercely negotiate these terms to limit your exposure, capping the total dollar amount you could be forced to pay back and shortening the time frame for a claim.

Another classic error is a weak or unenforceable non-compete clause. Without a carefully drafted agreement that is reasonable in scope, duration, and geography, you could find your buyer competing against you with the very business you just sold them. For a deeper look at what buyers inspect, check out our mergers and acquisitions due diligence checklist.

By understanding these common traps, you and your attorney can build a protective legal strategy from day one. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Connecticut Rules for Selling Your Business

While many aspects of selling a business are governed by broad federal laws, you can't overlook the specifics of state law. For anyone selling a business in Connecticut, these local rules aren't just minor details—they are critical requirements for a successful and legally sound sale.

Getting these details wrong can cause serious delays or, even worse, leave you on the hook for legal and financial problems long after you think the deal is done.

This is exactly why having a business sales attorney with deep Connecticut experience is so valuable. They know the precise filings and procedures our state requires, turning a potentially confusing process into a smooth, predictable closing.

State Filings and UCC Lien Clearances

When your business is sold, particularly in an asset sale, the transfer of ownership has to be officially recorded with the Connecticut Secretary of the State. This isn't just paperwork; it creates a public record that legally cements the change.

At the same time, we have to address any Uniform Commercial Code (UCC) liens filed against your business assets. These are legal claims from lenders, vendors, or other creditors who have a financial interest in your equipment, inventory, or receivables.

Before any closing can happen, these liens must be cleared. Your attorney will run a UCC search to find every claim and then work with each creditor to get them to file a UCC-3 termination statement. Without this crucial step, the buyer can’t receive clean title to the assets, and the deal will grind to a halt.

A buyer simply will not close on a purchase if the assets they are acquiring are still encumbered by the seller's old debts. A Connecticut-based business sales attorney knows precisely how to search for and systematically clear these liens with the Secretary of the State, ensuring a clean transfer of title.

Transferring Commercial Real Estate in Connecticut

If your business owns its building or land, the sale gets another layer of state-specific rules. Transferring commercial property in Connecticut involves much more than just signing over a deed.

An attorney familiar with Connecticut real estate law will manage several key steps:

- Deed Preparation: Drafting the correct deed—like a Warranty or Quitclaim Deed—that meets all state and local recording standards.

- State and Local Transfer Taxes: Calculating and paying Connecticut's Real Estate Conveyance Tax to both the state and the town where the property sits.

- Title Insurance: Coordinating with a title company to confirm the property title is clear of any hidden claims and to secure a new policy for the buyer.

Mishandling the real estate portion of the sale can create enormous title headaches for the buyer and expose you to future liability. For a deeper look at the fundamentals, you can check out our guide on how to transfer business ownership.

Obtaining a Tax Good Standing Certificate

Of all the Connecticut-specific requirements, the most important is arguably the Tax Good Standing Certificate from the Department of Revenue Services (DRS).

This document proves your business is current on all state taxes, including sales tax, use tax, and employee withholding. Buyers will almost always demand this certificate before closing because they need absolute certainty that they aren't inheriting your past tax liabilities.

Getting this certificate involves a formal request and a full review by the DRS, a process that can easily take several weeks. A smart attorney anticipates this and starts the application early, preventing a last-minute scramble that could delay your closing day.

There's a clear demand for focused, responsive legal counsel, especially from midsize firms. Recent analysis shows that midsize law firms saw a 6.1% revenue increase, outpacing larger competitors and showing that the market values personalized commercial guidance. You can find more detailed statistics on the legal services market from Grandview Research. An attorney who truly understands state-level compliance is a powerful asset.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How to Choose the Right Attorney for Your Sale

Selecting legal counsel is one of the most critical decisions you will make when selling your business. This isn't just about finding someone to review documents; it's about partnering with a strategic advisor who understands what's at stake and is committed to protecting your financial future. The right business sales attorney is your advocate, your negotiator, and your shield.

Making the wrong choice can have serious consequences. A deal can fall apart over preventable mistakes, you might get locked into unfavorable terms, or you could face post-closing liabilities that linger for years. To avoid this, you need to know what to look for and what questions to ask when vetting potential attorneys. It’s about gauging their real-world experience and strategic mindset.

Key Questions to Ask a Potential Business Sales Attorney

During your initial consultations, don’t hold back. A confident, experienced attorney will welcome your questions because their answers are a chance to demonstrate their expertise. Pay close attention to how they respond—it reveals their depth of knowledge and how they manage client relationships under pressure.

Here is a practical checklist to guide your conversations:

- “Can you describe a recent deal you handled that’s similar to my situation?” You need to hear about experience that matches your industry, business size, and deal structure (asset vs. stock). A generic answer is a major red flag.

- “How do you structure your fees for a sale like mine?” Ask about hourly rates versus flat fees and whether any portion is success-based. The goal is complete transparency and a fee structure that makes sense for your transaction.

- “Who will be my day-to-day contact on your team?” It’s important to know if you will be working directly with the senior attorney you’re meeting or if a junior associate will be handling most of the work.

- “What is your process for keeping me updated during due diligence?” This phase can be intense. Clear, consistent communication is essential, so you need to understand their system for managing the flow of information.

The global legal services market is projected to reach $717.7 billion by 2035, and private practicing attorneys make up a significant 34.7% of this market. You can learn more about the growing legal services market on KentleyInsights.com. This growth means you have options, making it even more important to choose wisely.

Your attorney should be more than a legal technician; they should be a business advisor. Listen to how they discuss the deal. Are they focused only on legal clauses, or do they also bring up tax implications, business risks, and your long-term financial security?

Remember, hiring an attorney is a two-way interview. While you are assessing their skills, they are determining if they can guide you successfully. Keep asking questions until you find a legal partner who gives you total confidence in their ability to get the deal done right.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Answering Your Questions About Selling a Business

Selling the business you’ve built is a major milestone, but the process can bring up a lot of questions. It's a landscape filled with legal complexities where a single misstep can have long-term consequences. Let's walk through some of the most common concerns we hear from business owners just like you.

Do I Really Need a Business Broker and an Attorney?

Yes, almost always. Think of it this way: they are two essential specialists on your team, and their roles don't overlap. Your business broker is the deal-finder. They’re a sales and marketing pro focused on valuing your company, finding qualified buyers, and getting you the best price.

Your business sales attorney, on the other hand, is your legal shield and strategist. While the broker finds the who (the buyer) and the what (the price), your attorney handles the how. We structure the deal to protect you from future liability, negotiate the fine print that can cost you dearly, and ensure the transaction closes smoothly and legally.

Why Is Everyone So Focused on Reps and Warranties?

Representations and warranties are the backbone of the purchase agreement. They are a series of legally binding promises you make about the state of your business—everything from your financials being accurate to your key contracts being in good standing. They are the buyer's assurance that they're getting what they paid for.

This is where your legal protection is truly won or lost. If a buyer discovers after closing that one of your "reps" was inaccurate, they have the right to sue you for their losses. A sharp attorney will fight to limit the scope of these promises, cap your financial exposure, and shorten the time window a buyer has to bring a claim against you.

How Do We Keep the Sale a Secret?

Confidentiality is absolutely critical. The last thing you want is for employees to get nervous, customers to lose confidence, or competitors to get wind of the sale before it’s a done deal. Premature news can destabilize the very asset you’re trying to sell.

Your attorney is your gatekeeper for confidentiality. We accomplish this by:

- Insisting that every single interested party signs a rock-solid Non-Disclosure Agreement (NDA) before they see any sensitive information.

- Managing the flow of documents through a secure virtual data room, not messy email chains.

- Advising you on the right time and the right way to communicate the sale to your team and customers after the ink is dry.

What If the Buyer Finds a Problem During Due Diligence?

First, don't panic. It's actually pretty common for buyers to turn up minor issues during their deep-dive investigation—maybe an old, unreleased lien, a vague clause in an employment agreement, or an overlooked permit. This rarely kills a deal on its own.

When an issue surfaces, our job as your attorney is to get ahead of it. We'll assess the real-world risk, explain your potential liability in plain English, and then get on the phone with the buyer’s lawyer to negotiate a practical solution. That might mean a small price adjustment, setting aside some funds in escrow, or simply agreeing to fix the issue before the closing. An experienced lawyer can turn a potential deal-breaker into a simple, manageable problem to be solved.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.