The call usually feels routine until you hear the agency name. An SEC staff member wants documents. Or your branch manager forwards a letter asking for account files, emails, and notes tied to a client complaint you thought had already died. For most financial advisors, that moment triggers the same questions at once: Is this informal? Am I the target? What do I say? What do I preserve? What happens to my book if this grows?

The anxiety is understandable, but panic is the one response that almost always makes things worse. Securities and Exchange Commission investigations are serious, but they are also structured. Once you understand the sequence, the strategic points, and the common mistakes, the process becomes more manageable.

The SEC's enforcement machinery is active at scale. In FY 2025, the agency filed 456 enforcement actions, obtained $17.9 billion in monetary relief, and received a record 53,753 tips, complaints, and referrals according to the SEC's FY 2025 enforcement results. That doesn't mean every inquiry becomes a headline case. It does mean advisors should treat even an “informal” contact as the start of a process that can affect registration status, compensation, client relationships, and future mobility.

An Advisor's First Brush with the SEC

A common version of this starts subtly. An advisor gets an email from compliance saying the SEC has requested records about a product recommendation, outside business activity, private securities transaction, fee practice, or communication with a client. Nobody says “investigation” in the first sentence. The request may sound narrow. That can be misleading.

Early-stage SEC contact often arrives before you know the full theory the staff is testing. The agency may be comparing customer statements to account records. It may be evaluating whether disclosures matched actual practices. It may also be following a lead from another regulator, a tip, or a termination disclosure. Advisors who have dealt with difficult separation issues already know how a filing can shape what comes next. If your concern involves departure-related disclosures, a Form U5 and FINRA background issue can easily become part of the broader defense picture.

The first practical step is to stop treating the issue like an annoyance that can be cleared up with one quick phone call. Sometimes it can. Often it can't. The safer assumption is that every communication, every record, and every explanation from the first day forward may matter later.

Practical rule: Your first objective isn't to “clear things up.” It's to preserve facts, control communications, and avoid making a bad record.

Advisors usually get into trouble early for one of three reasons:

- They talk too soon: An unprepared conversation can lock you into facts you later need to clarify.

- They search too narrowly: Relevant material often sits in texts, personal devices, calendars, notes, and archived systems.

- They underestimate employment fallout: Even a nonpublic SEC matter can affect supervision, recruiting, and internal firm politics.

That's why the right mindset isn't fear. It's disciplined response.

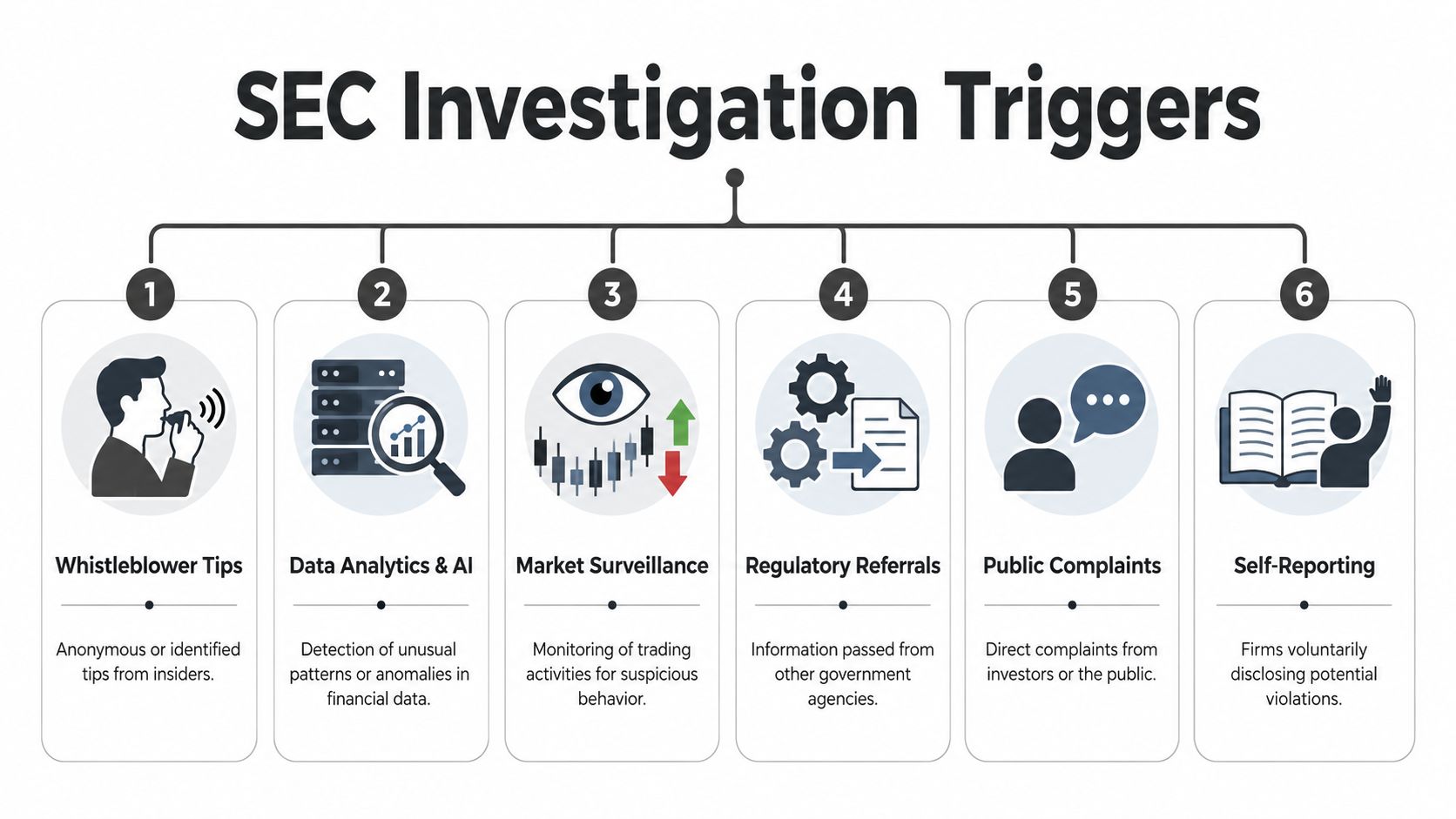

How SEC Investigations Begin Triggers and Inquiries

You get a call from compliance asking whether you remember a client rollover from eighteen months ago. Later that day, someone mentions the SEC asked for information. That is how many advisors first learn a government inquiry is in motion. The practical question is not just why the SEC looked. It is what likely triggered the look, and what that trigger says about the risk to you.

The starting point is usually identifiable. An SEC matter often begins with a pattern, a complaint, a referral, or a public event that gives staff a reason to ask whether the facts deserve closer attention. For advisors, that matters because the trigger often predicts the staff's first theory, the documents they want, and whether they are focused on the firm, the account activity, or your own communications.

Market signals and data reviews

Some inquiries start before any client complains. Trading around announcements, repeated allocations, unusual timing, common movement across related accounts, or patterns that do not fit the stated strategy can put an advisor on the radar. Staff may not know whether the activity reflects misconduct, poor documentation, or a coincidence. They still will want records that let them test the explanation.

Advisors make an early mistake. They assume a clean motive ends the issue. It does not. The SEC examines whether the file supports the motive you are offering, whether the recommendation record matches the trade, and whether emails, texts, and notes tell the same story.

Human sources and referrals

A large number of matters begin because a person reported something. The source may be a customer, former colleague, branch manager, operations employee, competitor, or another regulator. In practice, referral matters can be harder at the outset because the staff often receives the issue in a prepackaged form. Someone has already described what happened, named the suspected problem, and pointed to selected documents.

That creates a real defense problem for advisors. You are not responding only to facts. You are responding to a version of the facts that may already sound persuasive on paper. If FINRA, a state regulator, or your firm framed the conduct as unsuitable, misleading, off-channel, or supervisory, your response has to correct the record early and with documents, not indignation.

Public events and internal escalation

The SEC also pays attention to what becomes visible outside the file. Press coverage, civil lawsuits, arbitration allegations, restated disclosures, and internal reviews can all lead to questions. Advisors often enter the process after the firm has started collecting documents and interviewing personnel. By then, other people may already have described your conduct without the context you would have provided.

That timing matters. A firm's interests and an individual advisor's interests often overlap, but they are not always the same. A firm may focus on showing it had policies, escalation channels, and supervisory systems. An advisor may need to show what was disclosed, who approved the conduct, what training was given, and whether similar practices were common.

The SEC has also continued to bring cases against individuals, not just entities, as reflected in recent enforcement summaries from King & Spalding's review of SEC results and docket trends. For financial advisors, the practical lesson is straightforward. Do not assume the inquiry is only about firm controls. Staff may be assessing your statements, recommendations, certifications, and compensation from the beginning.

“My firm handled compliance” is a fact that may help. It is rarely a full defense.

From a career-protection standpoint, the trigger matters because it tells you where to look first. A trading-pattern inquiry calls for order records, account notes, allocation support, and comparable account data. A complaint-driven inquiry calls for communications, disclosures, suitability analysis, and a clean chronology. A referral from another regulator requires special care because inconsistent statements across forums can create a larger problem than the original issue.

If the subject touches recommendations, rollovers, private offerings, outside business activity, fees, books and records, or off-channel communications, treat the first inquiry as the start of a defense project. That approach gives you the best chance to protect both the case and your license.

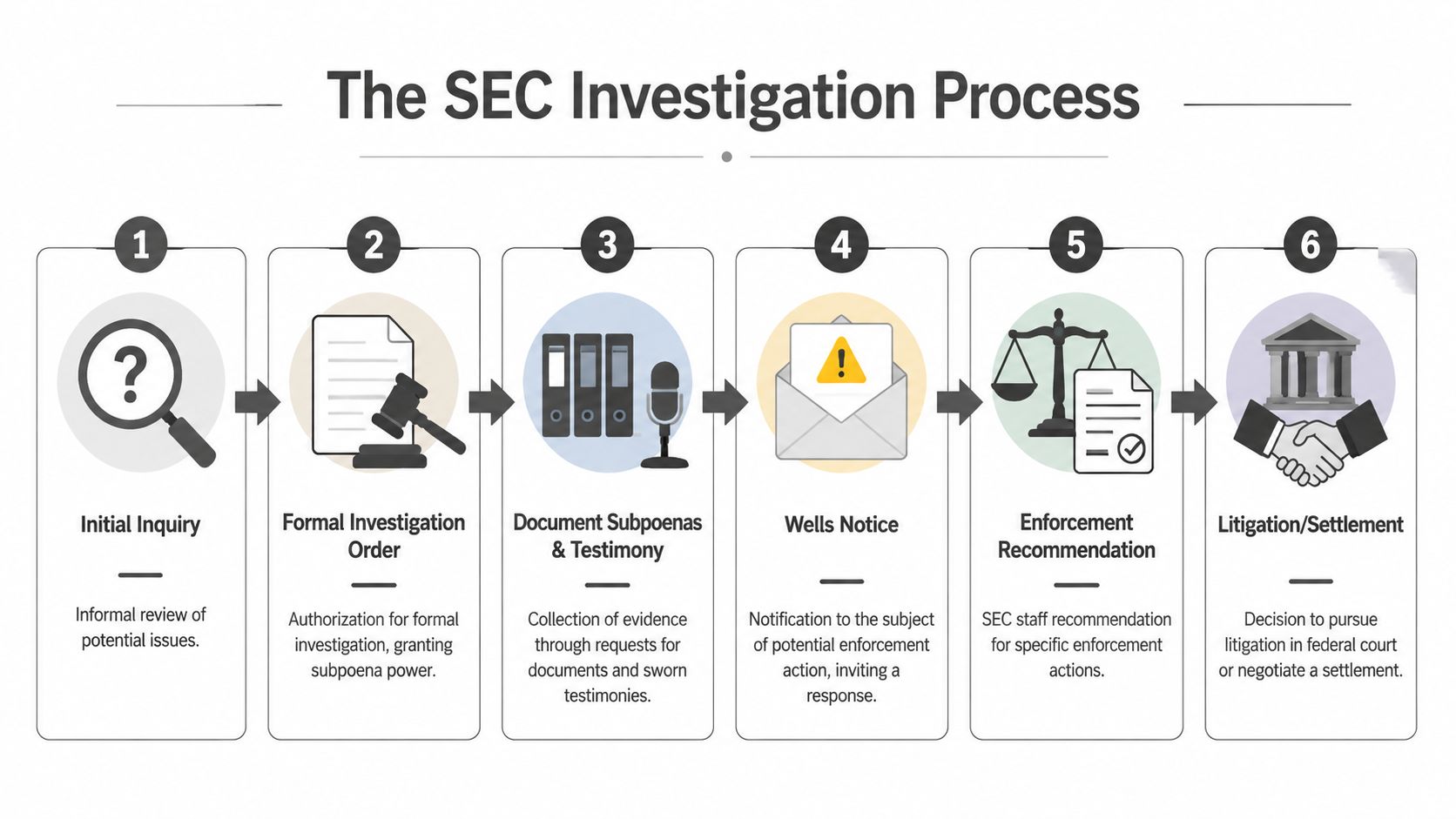

The Anatomy of an SEC Investigation From Inquiry to Enforcement

At 4:15 p.m. on a Tuesday, an examiner or enforcement attorney asks for a few documents and says the request is informal. For a financial advisor, that moment often feels ambiguous. It should be treated as the start of a staged process in which each response affects the next decision the SEC makes.

The practical mistake is treating the matter as a single event. SEC investigations develop in phases. Early requests shape the document record, the document record shapes testimony, and testimony often shapes settlement discussions or charging decisions. Advisors who understand that sequence make better decisions about preservation, messaging, and defense priorities.

Informal inquiry

An informal inquiry usually starts with voluntary requests for documents, background information, or interviews. Staff may be trying to confirm a complaint, test a trading pattern, or determine whether a recommendation, disclosure, or fee practice deserves closer review.

For advisors, the immediate question is not whether the request seems polite. The question is what theory the staff could be building from the material you provide. A short email production can expose off-channel communications. A casual explanation can harden into an admission if later records do not match it.

This stage is also where career protection begins. Preserve records, stop any routine deletion practices, and centralize responses. If the subject matter touches recommendations, valuation, private offerings, outside business activity, or anything that could be framed as securities fraud under federal law, assume the staff will test both the conduct and your intent.

Formal order of investigation

Once the SEC obtains a formal order, the case changes in a way advisors can feel immediately. The staff can use subpoenas to compel documents and sworn testimony. That changes deadlines, increases the volume of material in play, and gives the government more control over pace and pressure.

At this point, the matter needs to be run like litigation preparation, even if no case has been filed. Counsel should map custodians, likely issues, document gaps, and witness order. Advisors who wait until testimony is scheduled usually lose ground they could have held earlier.

Document subpoenas and testimony

The document phase is where many cases are won or lost. The SEC may request emails, text messages, CRM entries, order records, account forms, supervisory reviews, compensation data, marketing materials, and internal communications about the underlying conduct. The staff is not just collecting facts. It is looking for consistency, timing, and motive.

Three patterns show up often.

- Records frame the witness. If notes, emails, and forms tell different versions of the same event, your explanation gets narrower.

- Loose language creates avoidable risk. Advisors often write shorthand in emails or texts that reads badly outside the office.

- Preparation must be document-based. Testimony prep should focus on what exists in writing, what is missing, and where the staff is likely to press.

Sworn testimony deserves special care because small wording choices can affect exposure well beyond the interview itself. For advisors who want a clearer sense of how formal testimony is created and used, WhisperAI offers a helpful overview of deposition practice and transcript mechanics.

Wells notice and Wells submission

A Wells Notice means enforcement staff are considering recommending charges. It is one of the few points in the process where a disciplined written defense can still change the outcome, narrow the case, or improve settlement terms.

A useful Wells submission is selective and grounded in the record. It addresses the legal elements, corrects factual distortions, explains industry context where it helps, and deals forthrightly with bad documents or poor wording. It should also account for collateral effects on registration, Form U4 and U5 disclosures, employment, and client relationships. For an advisor, the goal is rarely abstract vindication. The goal is to protect the license, reduce allegations that imply intent, and preserve the ability to keep working.

Enforcement action or closure

Some investigations close without charges. Others end in a settlement, an administrative proceeding, or federal court litigation. By that stage, the result usually reflects the quality of the work done much earlier. Preservation decisions, witness preparation, internal communications, and the consistency of your narrative all matter.

Here is the practical sequence:

| Stage | Primary Purpose | Key SEC Actions | Your Position |

|---|---|---|---|

| Informal inquiry | Assess whether the issue warrants further investigation | Voluntary requests, background review, initial record collection | Preserve documents, retain counsel, and give controlled responses |

| Formal order | Expand investigative authority | Authorizes subpoenas for documents and testimony | Organize response strategy, custodians, and document review immediately |

| Document phase | Build the factual record | Collects communications, account records, supervisory materials, and compensation data | Create a chronology, test explanations against records, and identify exposure points |

| Testimony phase | Fix witness accounts in the record | Sworn testimony and follow-up questioning | Prepare carefully, answer precisely, and avoid guessing |

| Wells process | Evaluate whether charges should be recommended | Issues Wells Notice and reviews Wells submission | Present a disciplined defense that addresses law, facts, and collateral consequences |

| Resolution | Close the matter or bring charges | Closes file, negotiates settlement, or files an action | Manage licensing, employment, disclosure, and business continuity |

Your Legal Rights and Critical Obligations

An advisor often feels the pressure most acutely before anyone has set ground rules. The staff asks for documents. A branch manager wants updates. A client calls after hearing a rumor. Those first few days shape the record, and they often shape the outcome.

Counsel and preservation come first

You have the right to counsel. Use it before you answer substantive questions, hand over documents, or try to explain the situation informally to the SEC or your firm. Early counsel protects privilege, reduces inconsistent statements, and helps separate your interests from the firm's interests if they begin to diverge.

Preservation starts immediately. Keep emails, texts, CRM notes, calendars, handwritten notes, app messages, trading records, and anything else that may bear on the issues under review. Personal devices count. Home files count. Messages sent outside firm systems count.

Advisors get into trouble here because they treat preservation like an IT issue. It is a legal issue with career consequences. Deleting a few messages after an inquiry arrives can turn a difficult exam or investigation into a credibility problem that follows you through testimony, settlement talks, and licensing disclosures.

If the staff requests testimony, the transcript matters. Every answer is fixed in the record and compared against documents and later statements. For a basic explanation of how sworn testimony is recorded and used, WhisperAI offers a helpful overview of deposition transcription.

Disclosure requires judgment, not instinct

Advisors regularly ask whether they must disclose an SEC inquiry to clients, counterparties, recruiters, or the market. The answer depends on the setting. There is no universal rule that requires disclosure in every case, and there is no safe habit of saying nothing while selectively calming the people you want to keep close.

For public companies, the SEC's Division of Corporation Finance has addressed this issue in its guidance on disclosure of investigations and other contingencies. The practical point for advisors is straightforward. Disclosure analysis turns on materiality, existing public statements, firm policy, Form U4 and U5 obligations, contractual notice duties, and whether silence or partial disclosure would make another statement misleading.

That is why off-the-cuff reassurance is dangerous. Telling a favored client or recruiting firm that the matter is “nothing” can create a separate problem if the facts later develop differently.

Your rights are real, but so are your limits

You can assert privileges where they apply. You can ask that SEC requests be handled through counsel. You can take time to prepare for testimony. You can correct factual errors before they harden into the staff's working theory.

You cannot obstruct the process, destroy records, coach witnesses to adopt a story, or guess your way through an answer because silence feels uncomfortable.

A disciplined response sounds simple, but it takes work. Answer what was asked. Do not volunteer extra facts to sound helpful. Do not speculate about client intent, firm policy, or what someone else “must have meant.” If you do not know, say so. If you do not remember, say that truthfully and stop there.

Parallel exposure changes the strategy

An SEC matter can trigger pressure from several directions at once. Your firm may open an internal review. FINRA may ask for information. State regulators may become involved. Employment issues may surface if supervision, compensation, or transition plans are implicated.

Those tracks need coordination. A statement that seems useful in an internal HR interview can create problems in sworn SEC testimony later. Allegations that sound like poor supervision or disclosure failures can also overlap with what investors describe as securities fraud, even though the legal standards, available defenses, and settlement consequences differ.

The practical rule is to keep one accurate factual position across every audience. That protects credibility, which is often your most valuable asset once the investigation is underway.

Building Your Proactive Defense Strategy

Good defense work in SEC matters is not reactive. It is built. The advisor who waits for the next letter before thinking strategically usually concedes too much ground. The better approach is to build the factual and legal record before the staff decides what your conduct means.

Start with a case map

Counsel should help assemble a working map of the matter early. That usually includes the likely theory, key dates, products involved, customer files, communications channels, supervisory structure, compensation issues, and any known complaints or internal reviews. The point is not to create a perfect narrative on day one. The point is to identify where the vulnerabilities sit.

A useful internal case map often includes:

- Chronology: When recommendations, disclosures, transfers, approvals, and complaints occurred.

- Document families: Emails, texts, CRM notes, subscription documents, account forms, trade confirmations, and supervisory reviews.

- Witness list: Clients, supervisors, assistants, compliance personnel, product sponsors, and former colleagues.

- Pressure points: Gaps in notes, inconsistent explanations, off-channel messages, or compensation evidence that may look bad without context.

Treat subpoenas as strategy opportunities

A subpoena is not just a burden. It is a preview of the staff's thinking. The scope tells you what period matters, what conduct matters, and which people matter. Advisors often focus on production volume and miss the analytical value of the request itself.

Responses work best when counsel and the client do more than collect paper. They should test assumptions. Why is this date range included? Why are certain customers grouped together? Why did the staff ask for notes but not certain advertising materials? The request often reveals the suspected theory before the testimony does.

Key takeaway: Every production should be accurate, complete, and intentional. Sloppy overproduction can be as damaging as an incomplete response.

Prepare for testimony like a trial witness

On-the-record testimony is not the place to “tell your side casually.” It is a formal proceeding in which precision matters more than persuasiveness. Advisors do best when they understand the file, the likely themes, and the difference between memory and reconstruction.

Preparation should cover documents, not just talking points. If an email uses shorthand, you need to know how it reads to someone outside your business. If a note is sparse, you need to understand what other records support it. If your recommendation process was sound but poorly documented, the testimony must address that carefully without overstating certainty.

Use the Wells process deliberately

The Wells stage is often the best formal chance to shape outcome before charges are filed. A well-crafted Wells submission can challenge legal theories, explain industry context, correct chronology errors, and present mitigating facts in a way that is hard to accomplish through piecemeal correspondence.

Not every case should fight every point. Sometimes the smart move is to narrow the battlefield. That may mean arguing against scienter while conceding an immaterial recordkeeping issue. It may mean separating firm-level failures from advisor-level conduct. It may mean highlighting remedial steps and cooperation without making unnecessary admissions.

If you need counsel for the broader regulatory side, Kons Law's securities regulation practice is one example of the type of representation advisors look for when a matter touches investigations, licensing, and business continuity at the same time.

Understanding Investigation Timelines and Potential Outcomes

An advisor gets a document request in the spring, answers it by summer, and hears almost nothing for months. Then a new subpoena arrives with a short deadline, a former employer asks questions, and a client dispute starts pulling on the same set of facts. That pattern is common in SEC matters. They rarely move in a straight line, and the uneven pace creates its own risk for advisors trying to protect licenses, compensation, and client relationships.

The SEC's own enforcement process makes that point. Investigations can begin with informal requests, proceed under a Formal Order, and end in closure, settlement, an administrative proceeding, or federal court action, as described in the SEC's How Investigations Work. For advisors, the practical takeaway is simple. Build a defense that can hold up over time, because the matter may last far longer than the first call or subpoena suggests.

Time changes the case.

A long investigation affects witness memory, device retention, insurance notice issues, transitions between firms, and how a book of business is valued or sold. It can also change the government's theory. Staff may start with one concern and later focus on supervision, disclosures, valuation, off-channel communications, or recordkeeping because those issues are easier to prove from the documents.

That overlap matters if you are also dealing with a customer claim, a promissory note case, or a separation dispute. Testimony, production decisions, and position statements in one forum can complicate the other. Advisors in that position often need to assess FINRA and securities arbitration strategy at the same time they are handling the SEC file.

Possible outcomes vary more than many advisors expect. Some investigations close without action. Some resolve through settlement with undertakings, penalties, censures, suspensions, or bars. Others go to litigation, where cost, publicity, and collateral consequences usually increase.

Common remedies include:

- Cease-and-desist orders

- Civil penalties

- Disgorgement

- Industry bars or suspensions

- Registration-based sanctions

- Undertakings such as compliance reviews, retention measures, or certification requirements

The forum matters because the procedure and pressure points differ. The SEC has explained that it may bring contested matters either in federal court or, where authorized, in an administrative proceeding through the Office of Administrative Law Judges, as outlined on the agency's Administrative Proceedings page. An advisor deciding whether to settle, litigate, or narrow issues needs to evaluate more than the headline charge. Ultimately, the question is how the chosen path affects licensing, Form U4 and U5 disclosures, future employment, and the economics of keeping the practice intact.

There is also a business-preservation point that gets missed. Long investigations create operational mistakes. Phones are replaced, text messages disappear, cloud accounts change, and personal devices become harder to collect cleanly. If your records may sit in compromised systems or mixed-use devices, basic preservation and incident-response discipline matters. GoSafe's data breach guidance is a useful outside reference on securing systems while preserving relevant evidence.

The right mindset is measured, not passive. Advisors do better when they plan for several endings at once, early closure, negotiated resolution, or contested charges, and make decisions that preserve credibility in each of those paths.

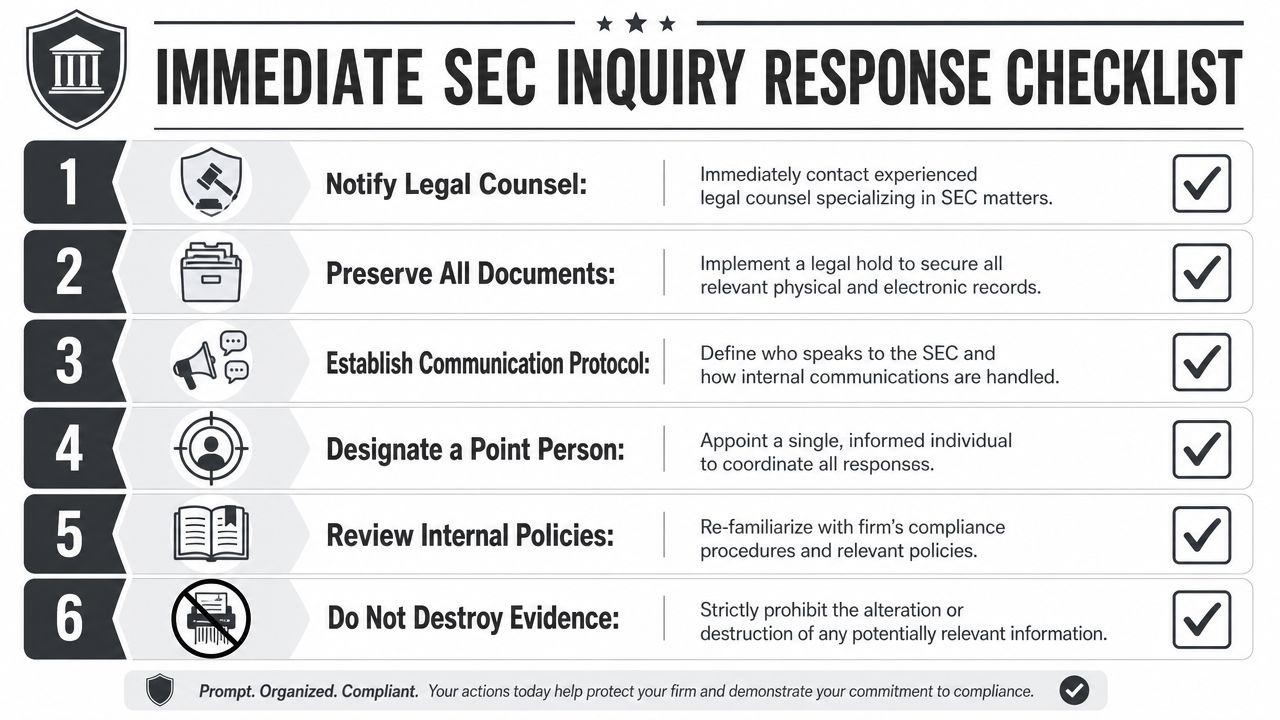

An Immediate Response Checklist for Advisors and Firms

The first day matters. The first week matters more than most advisors realize.

Keep the initial response simple and disciplined:

- Call counsel immediately: Don't try to gauge seriousness by yourself based on tone or wording.

- Issue a preservation hold: Secure email, texts, notes, calendars, CRM entries, cloud files, and paper records.

- Name one response coordinator: One informed point person reduces conflicting messages and missed deadlines.

- Freeze informal explanations: Don't call the SEC staff casually. Don't “clarify” facts in side conversations.

- Review firm policies: Check communications, outside business activity, product approval, books and records, and supervision procedures.

- Separate legal from operational communications: People who need to know should know. Gossip and speculation should stop.

Also address digital hygiene quickly. If relevant material may sit in compromised systems, personal devices, or cloud tools, basic incident-response discipline helps preserve evidence and avoid secondary problems. A practical outside reference is GoSafe's data breach guidance, which is useful for understanding how to stabilize records and communications after a security-related event.

A few early mistakes cause outsized damage:

- Deleting “unimportant” messages

- Texting coworkers about what to say

- Assuming the firm's lawyer represents you personally

- Contacting clients to align recollections

- Guessing when you don't know

Taking Control of the Investigation Narrative

The call, subpoena, or testimony notice is not just a legal event. For a financial advisor, it is a career event. How you respond in the first days often shapes how the staff views your judgment, your credibility, and your ability to supervise your business.

Control starts with discipline. The SEC staff will build a story from documents, emails, texts, client files, trading records, and witness interviews. Your job is to make sure the record is accurate, organized, and placed in the right context before assumptions harden into allegations.

That means doing more than reacting to requests. Build a defensible chronology. Identify the trades, recommendations, disclosures, approvals, and communications that matter most. Separate bad facts from misunderstood facts. Some documents will be unhelpful. Good defense work does not hide that. It explains them, tests whether they are complete, and places them beside the records that show process, supervision, intent, and client communication.

Advisors who protect their licenses and business usually focus on three practical goals. First, keep the facts clean by avoiding loose explanations, speculation, and off-the-record conversations. Second, present a consistent account that matches the documents. Third, make strategic decisions early about testimony, document production, client contact, and Wells advocacy rather than treating each step as an isolated event.

This is also where individual and firm interests can separate. The firm may want speed, containment, and a message that protects the enterprise. You may need advice focused on your Form U4, your compensation, your client relationships, and whether the firm's position leaves too much blame at the advisor level. That is a common tension, and it should be assessed early.

As noted earlier, shifts in enforcement doctrine and remedies do not change the practical point for advisors. Individual exposure remains real. Selective enforcement does not mean softer enforcement.

A strong narrative is not spin. It is a documented, credible explanation of what happened, why it happened, what policies governed the conduct, who knew what at the time, and where the staff may be drawing the wrong inference. When that work starts early, you are in a better position to respond to testimony, settlement discussions, or a Wells notice from a position of strength.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.