A deficiency judgment is a court order that can feel like a one-two punch after a foreclosure or repossession. It’s what happens when the sale of your property doesn't cover the full amount you owe on the loan. The court essentially says you are personally on the hook for that remaining balance.

This court order transforms the original secured debt—which was tied directly to your house or car—into an unsecured personal debt. Suddenly, the fight isn't about the property anymore; it's about your personal finances.

What Exactly is a Deficiency Judgment?

When you take out a loan for a major purchase like a home or a vehicle, the item itself acts as collateral. If you fall behind on payments, the lender has the right to take back that collateral through foreclosure or repossession to recoup their losses.

But what happens when the property's sale price at auction doesn't cover the outstanding loan balance, interest, and fees? That gap is called the "deficiency."

A lender can’t just send you a bill for this shortfall and call it a day. They have to go back to court and file a specific motion to get a deficiency judgment. This is a critical, separate legal step. Without it, the lender has no legal power to collect that remaining debt from you personally.

To give you a clearer picture, let's break down the key components.

Deficiency Judgment at a Glance

This table breaks down the core components of a deficiency judgment to provide a quick summary for readers.

| Component | Simple Explanation | Primary Scenarios |

|---|---|---|

| Deficiency | The financial shortfall when a repossessed or foreclosed asset sells for less than the total loan balance. | Real estate foreclosures, vehicle repossessions, and other secured loans. |

| Judgment | A separate court order making the debtor personally liable for the deficiency amount. | The lender must sue the debtor after the property is sold to obtain this. |

| Unsecured Debt | Once the judgment is granted, the debt is no longer tied to the original asset. | The creditor can now pursue the debtor's other assets, like bank accounts or wages. |

This process fundamentally changes the game for both the lender and the debtor, opening up new avenues for collection that weren't available before.

Common Scenarios Where Deficiencies Pop Up

You're most likely to encounter a deficiency judgment in two common, and often stressful, situations:

- Real Estate Foreclosure: Let's say you owe $300,000 on your mortgage. After a foreclosure, the home sells at auction for only $250,000 due to a downturn in the market. The lender can then go to court to get a deficiency judgment against you for that $50,000 difference.

- Vehicle Repossession: The same principle applies to your car loan. If you owe $15,000 and your repossessed car is sold for $10,000, the lender might sue you for the $5,000 deficiency.

A deficiency judgment effectively untethers the debt from the original property. The lender, now acting as a judgment creditor, can use various legal tools to collect the amount owed directly from your personal finances, not just the asset that secured the loan. To understand more about the powers a creditor has, you can learn more about what is a judgment creditor in our detailed article.

This legal shift from a secured mortgage to an unsecured personal liability is a massive distinction. It puts your other assets in the creditor’s crosshairs, which we’ll explore in more detail later. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How Deficiency Judgments Take Shape in Connecticut

A deficiency judgment isn't something that just appears out of thin air. It’s the final step in a very specific legal process that starts long before anyone sets foot in a courtroom. In Connecticut, this unfolds in a structured way, usually in the context of a real estate foreclosure or a vehicle repossession. Understanding this journey is key for both creditors and debtors.

It all begins when a borrower defaults on a secured loan. After trying other options, the lender will move to reclaim the collateral—whether that’s foreclosing on a house or repossessing a car. The next critical step is selling that asset to try and cover the loan balance. It's at this sale, often a public auction, that the possibility of a deficiency is born.

If the sale doesn't bring in enough money to cover the total amount owed—including the loan principal, interest, late fees, and legal costs—you're left with a financial gap. This is the "deficiency." But this shortfall isn't automatically the borrower's personal debt. The lender can't just send a bill for the difference. Instead, they have to start a new legal action.

The Critical Role of the Court

To turn that deficiency into a debt they can actually collect, the lender has to file a formal motion with the Connecticut courts. This is a mandatory step. The motion asks a judge to officially recognize the leftover debt and grant a deficiency judgment, which legally forces the borrower to pay up.

A judge doesn't just rubber-stamp these requests. The court digs into the entire process, including the details of the sale. They have to confirm the sale was handled properly and that the deficiency amount is accurate and fair. This oversight is a crucial protection for borrowers, making sure the lender’s claim is legitimate before it becomes a personal liability.

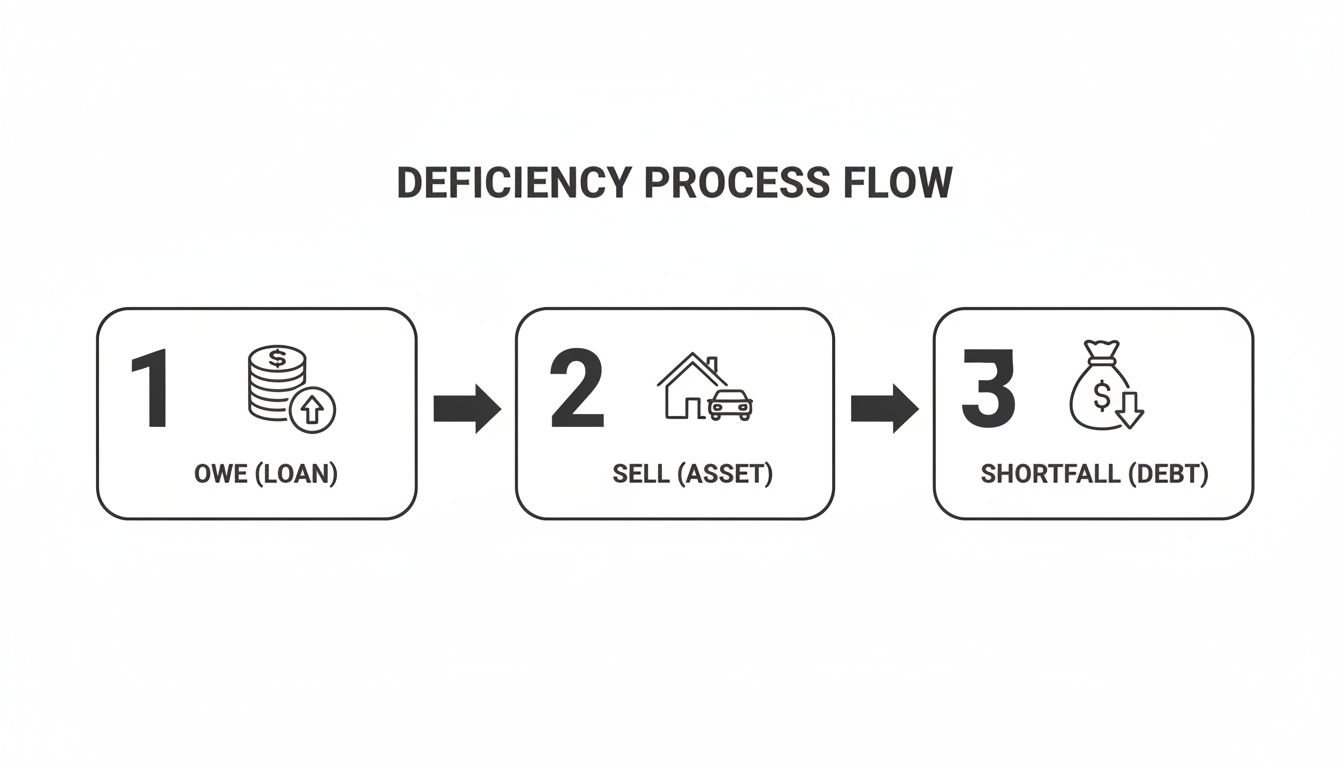

This infographic gives you a simple look at the flow from an unpaid loan to a potential shortfall.

As you can see, it's a straightforward but consequential path. The asset's sale price fails to cover the debt, creating the gap a lender might then take to court.

The Step-by-Step Legal Pathway

The road from default to judgment follows a clear progression. While the small details can shift from case to case, the general steps in Connecticut give you a good map of how it all works.

- Default and Foreclosure/Repossession: It starts when the borrower stops making payments. The lender then begins foreclosure or repossession to take back the secured asset.

- Sale of the Asset: The property or car is sold, usually at a public auction. The money from the sale is put toward the borrower's total debt.

- Calculation of the Deficiency: The lender subtracts the net sale proceeds from the total amount owed. If there's still a balance, that’s the deficiency.

- Filing a Motion for Deficiency Judgment: The lender's attorney files a motion in court, showing evidence of the original loan, the sale price, and the resulting shortfall.

- Judicial Review and Approval: A judge reviews everything to make sure all legal rules were followed. If the court agrees with the lender, it issues a deficiency judgment for the amount.

It’s important to remember that laws around these judgments change dramatically from state to state. A deficiency judgment is a court-ordered personal liability for the shortfall, but its availability has always varied across the U.S. Roughly half of the states are "recourse" states (where lenders can pursue them) and half are "non-recourse" (where they generally can't), with plenty of exceptions.

The move from a foreclosure to a deficiency judgment hearing is a major turning point. The legal focus shifts from the property itself to the borrower's personal financial situation. This also brings in new complexities, as other claims or liens on foreclosures can affect the proceedings and what’s ultimately owed.

Once a judgment is granted, the lender becomes a judgment creditor. They now hold a powerful legal tool to collect the unsecured debt. This court order lets them go after the borrower's other assets—like wages and bank accounts—to get their money back. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

The Real Financial Impact of a Deficiency Judgment

A deficiency judgment is much more than a number on a court filing. Think of it as a powerful legal tool that can have a deep and lasting impact on your entire financial life. Once a judge signs off on it, the debt changes completely. It’s no longer just a loan tied to your house or car; it becomes a personal, unsecured obligation.

This shift is a game-changer. It means the creditor isn't limited to the property they took back. With a judgment in hand, they now have the court's blessing to go after your other assets to get paid. And they won't be shy about it.

Powerful Tools Creditors Use for Enforcement

Once a creditor has a deficiency judgment, they gain access to some serious legal firepower to collect what you owe. These aren’t polite requests for payment—they are court-ordered actions that can directly tap into your income and assets.

- Wage Garnishment: The creditor can get a court order forcing your employer to take a chunk of your paycheck and send it straight to them. This doesn’t stop until the judgment, plus interest and fees, is fully paid.

- Bank Account Levy: A creditor can freeze your bank accounts and simply take the money out to cover the debt. This can happen suddenly, causing checks to bounce and other payments to get rejected.

- Property Liens: The judgment can be attached to any other real estate you own, like a second home or an investment property. This "lien" clouds the title, making it impossible for you to sell or refinance until the judgment is paid off.

These aggressive tactics show you what a deficiency judgment really is: a legal key that unlocks your broader financial world for a creditor.

From Secured Loan to Personal Liability

Let’s walk through a real-world example to see how this plays out. Say you had a $300,000 mortgage. After hitting hard times, you couldn't make payments, and the bank foreclosed. At the auction, your home only sold for $250,000, leaving a $50,000 gap.

The lender then heads back to court and gets a deficiency judgment for that $50,000. Suddenly, that $50,000 is your personal debt, no different than a credit card bill. The creditor can now use wage garnishment, bank levies, or property liens to collect every penny.

The judgment is the court's way of saying the original collateral wasn't enough, so it's giving the creditor permission to look elsewhere for their money. This is exactly why you have to be proactive if you see a deficiency on the horizon.

The pain doesn't stop with collection efforts, either. A deficiency judgment hammers your credit report and can crater your score for years. This makes it incredibly difficult to get new loans, qualify for good interest rates, or even get approved for an apartment rental. The ripple effects are huge. You can read more about the financial implications of these judgments on Bankrate.com.

This isn't a problem that just fades away. For more detail on how long these legal actions can follow you, check out our guide on how long a judgment lasts in Connecticut. It's a persistent financial weight, which makes having the right strategy absolutely critical.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Navigating Connecticut's Specific Deficiency Judgment Rules

When it comes to a foreclosure, state laws write the rulebook. And those rules make all the difference in what happens after the property is sold. While the basic idea of a deficiency judgment is the same everywhere, Connecticut has its own specific playbook that both lenders and borrowers need to follow.

Knowing these local rules is the key to understanding your rights and obligations.

First things first: Connecticut is what’s known as a “recourse” state. This simply means that lenders have the legal green light to pursue a borrower for the remaining balance after a foreclosure. But it's not a free-for-all. The state has put important guardrails in place to protect borrowers from unfair collection tactics.

The Critical 30-Day Clock

One of the biggest protections for borrowers in Connecticut is a very strict timeline. A lender doesn’t have forever to come after you for the remaining debt once the foreclosure sale is complete.

In Connecticut, a lender must file a motion for a deficiency judgment within 30 days of the foreclosure auction. That's it. If they miss that deadline, they lose their right to pursue the deficiency entirely. This tight window forces lenders to act fast and prevents them from blindsiding a former homeowner with a lawsuit months or even years down the road.

Connecticut's Fair Market Value Rule

Another powerful safeguard in Connecticut law is the “fair market value” rule. This rule tackles a common scenario where a property sells at a foreclosure auction for a rock-bottom price, far below what it’s actually worth. In many other states, the deficiency is simply the loan balance minus that low auction price, which can saddle the borrower with an unfairly massive debt.

Connecticut takes a more balanced approach.

When a lender seeks a deficiency judgment, the court doesn't just rubber-stamp the auction price. Instead, it determines the property's fair market value on the date of the sale. The deficiency is then calculated as the total debt minus this fair market value—not the auction price.

Here’s what that looks like in the real world:

- Total Debt: You owe $400,000 on your mortgage.

- Auction Sale Price: The house sells for only $300,000 at the auction.

- Fair Market Value: The court, based on an appraisal, determines the home was actually worth $375,000 that day.

In this case, the court ignores the lowball auction price and uses the $375,000 fair market value. Suddenly, the potential deficiency judgment drops from $100,000 all the way down to just $25,000. This rule is a powerful defense against an inflated deficiency claim and ensures the final number is grounded in the property's true value. Understanding the mechanics of foreclosing a lien is essential for both sides to navigate this process.

How Connecticut Stacks Up Against Other States

The differences between state laws really put these rules into perspective. Take California, a huge mortgage market with strong anti-deficiency laws. There, lenders are often completely barred from seeking deficiency judgments on primary home loans after a non-judicial foreclosure. For many homeowners, the foreclosure sale is the end of the story.

This comparison highlights why knowing Connecticut’s specific framework—its recourse status combined with powerful fair market value and timeline protections—is so important. It creates a more balanced legal playing field than you’ll find in states with fewer safeguards for borrowers.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How to Fight Back: Strategic Defenses Against a Deficiency Judgment

Getting hit with a motion for a deficiency judgment can feel like adding insult to injury after a foreclosure or repossession. But it's not the end of the line. A lender’s claim for more money isn't automatic—it's a legal request, and you absolutely have the right to challenge it.

Several powerful legal defenses can be used to fight the claim, slash the amount you owe, or even get the case thrown out completely. It’s critical to remember that the burden of proof is on the lender to show they followed every single rule perfectly. Any slip-up on their part opens the door for a strong defense.

Challenging the Fair Market Value

This is often the most potent defense in a debtor's playbook. Connecticut law is clear: the deficiency must be calculated based on the property's fair market value on the day of the foreclosure sale, not just what it sold for at auction. Lenders have an incentive to use a low appraisal to make the deficiency look as large as possible, but you can fight back.

An experienced attorney will bring in an independent, certified appraiser to give the court a true, unbiased valuation. This counter-appraisal can be powerful evidence showing the lender’s number is inflated. If the court sides with your appraiser, the judgment amount can plummet.

For instance, say the lender claims the property's fair market value was $320,000 against your $400,000 debt, leaving them chasing you for an $80,000 judgment. But if your appraiser proves the real value was $380,000, that potential deficiency shrinks to just $20,000. That's a huge difference.

Arguing the Sale Was "Commercially Unreasonable"

Here's another heavy hitter. You can argue that the lender failed to conduct the sale in a "commercially reasonable" manner. This isn't just a suggestion; it's a legal standard that requires the creditor to act in good faith and take proper steps to get a fair price.

So, what makes a sale commercially unreasonable?

- Lousy Advertising: The lender barely marketed the property, ensuring few, if any, serious bidders showed up.

- Wrong Place, Wrong Time: The sale was held at a weird time or in an out-of-the-way location that discouraged participation.

- Ignoring a Better Offer: The lender accepted a lowball bid when they knew the property was worth much more, without a good reason.

If you can prove the sale process was flawed and led to a low price, a judge might reduce or even eliminate the deficiency. The logic is simple: the lender's shoddy work contributed to the shortfall, and you shouldn't have to pay for their mistakes.

Finding Procedural Errors and Missed Deadlines

The foreclosure and deficiency judgment process is a minefield of strict rules and deadlines. Creditors have to follow them to the letter. Any misstep can blow up their case.

A surprisingly common and fatal error is improper notice. Lenders are legally required to notify you of the foreclosure, the sale, and their plan to seek a deficiency. If they sent a notice to the wrong address, served it improperly, or just forgot to send one, that can be grounds to dismiss their entire claim.

On top of that, Connecticut's 30-day deadline to file for a deficiency judgment is ironclad. If the lender files on day 31, they're out of luck. A good attorney will comb through every document and date, looking for these kinds of procedural tripwires. Often, they provide a complete defense.

If you are facing a deficiency judgment and want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Exploring Your Options and When to Seek Legal Help

When you’re facing a potential deficiency judgment, the best defense is a good offense. Being proactive can help you sidestep a judgment entirely, but even if one has already been entered against you, practical solutions are still on the table. The key is to act quickly, because time is not on your side.

Long before a foreclosure sale is even scheduled, you have the power to work with your lender for a better outcome. One common strategy is negotiating a short sale. This allows you to sell the property for less than what you owe, but you absolutely must get a deficiency waiver in writing. Without that specific piece of paper, the lender can still come after you for the difference.

Another path is a deed in lieu of foreclosure. Here, you voluntarily hand over the property title to the lender, satisfying the debt. Just like a short sale, you have to make sure the agreement explicitly releases you from any future deficiency claims.

Practical Solutions After a Judgment

If a deficiency judgment is already a reality, don't assume the fight is over. Most creditors would rather get a guaranteed partial payment today than chase an uncertain, full payment over months or years. That reality opens the door for negotiation.

An attorney can often step in and negotiate a lump-sum settlement for a fraction of what you owe. If a lump sum isn't feasible, you might be able to work out a structured payment plan that fits your budget. This can stop more aggressive collection tactics like wage garnishment or a bank levy in their tracks.

The most critical takeaway is this: the sooner you engage a legal professional, the more leverage you have. An attorney can assess the validity of the lender's claim, identify potential defenses you may have missed, and negotiate from a position of strength on your behalf.

Waiting until your wages are being garnished or your bank account is frozen puts you at a severe disadvantage. Taking control of the situation early is everything. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Your Questions on Deficiency Judgments, Answered

Even with a clear overview, it's natural to have questions about how a deficiency judgment might play out in your own life. Let's tackle some of the most common concerns we hear from clients in Connecticut, breaking down what these legal actions mean in practical terms.

Can Bankruptcy Wipe Out a Deficiency Judgment?

Yes, it often can. This is a powerful tool for debtors. The legal system classifies a deficiency judgment as an unsecured debt—the same kind as a credit card bill or a hospital invoice. Because it’s not tied to any specific collateral anymore, it’s exactly the type of debt that bankruptcy is designed to address.

- Chapter 7 Bankruptcy: Think of this as a reset button. In many cases, a Chapter 7 filing can discharge the deficiency judgment entirely, wiping the slate clean and freeing you from the legal obligation to pay.

- Chapter 13 Bankruptcy: If Chapter 7 isn't the right fit, Chapter 13 offers a path to reorganize. Your deficiency judgment would get rolled into a consolidated, court-approved repayment plan lasting three to five years. You'd likely pay back only a fraction of what you originally owed.

Will I Get Sued for a Deficiency After My Car is Repossessed?

It’s not just possible; it’s incredibly common. When a vehicle is repossessed, the process is a lot like a miniature foreclosure. The lender takes the car back, sells it at auction, and puts that money toward what you owe on the loan.

The problem is that cars lose value fast. The auction price almost never covers the full loan balance. The lender then has the right to come after you in court for the shortfall, plus any costs they paid for the repossession and auction process.

Let’s say you still owe $18,000 on your auto loan. The car sells at auction for just $11,000. The lender can—and likely will—sue you for a deficiency judgment to recover that $7,000 gap, plus their fees. It's standard operating procedure in the auto finance world.

How Long Does a Creditor Have to Collect on a Deficiency Judgment in Connecticut?

A very, very long time. In Connecticut, a creditor has years to enforce a judgment, but it doesn't stop there. They can also renew the judgment, extending the collection window even further. In theory, they could legally pursue the debt for decades after the court first ruled in their favor.

This is exactly why you can't just ignore a deficiency judgment and hope it goes away. It won't. The debt can sit dormant for years, quietly racking up interest, only to resurface when you're trying to buy a house or get another loan. Tackling it head-on is always the smarter move.

Navigating the complexities of a deficiency judgment requires a clear understanding of your rights and options. If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.