So, you’re thinking about forming an LLC. The number one reason most entrepreneurs go this route? It’s all about the powerful shield of limited liability. Think of it as a financial firewall between your business and your personal life—your house, your savings, your car—keeping them safe if the business ever gets into hot water.

The LLC’s Financial Firewall: A Closer Look

Imagine building a fortress to protect everything you own personally. An LLC is that fortress. It establishes your business as its own legal entity, entirely separate from you, the owner.

This separation is the bedrock of asset protection and a huge reason why choosing the right business structure from the get-go is so important.

What does this legal distinction actually mean in the real world? It means that if your business racks up debt, signs a big commercial lease, or gets sued by a client, the claims are against the LLC's assets—not yours. Your potential loss is capped, or "limited," to whatever you've invested in the company itself.

What the Liability Shield Covers vs. What It Doesn’t

The protection an LLC offers is broad, but it’s not absolute. It's crucial to understand both its strengths and its limitations. Here’s a quick overview of what the liability shield typically guards against and where you might still be on the hook personally. We'll dive deeper into these exceptions in the sections to come.

| Typically Covered by LLC Shield | Potential Personal Liability (Exceptions) |

|---|---|

| Business Debts & Loans | Personal Guarantees on loans or leases |

| Vendor & Supplier Disputes | Piercing the Corporate Veil (mixing funds, fraud) |

| Lawsuits for Employee Actions | Personal Negligence or Torts you commit |

| Breach of Contract Claims | Failure to Pay Payroll Taxes (trust fund taxes) |

As you can see, the LLC structure is designed to handle the everyday financial risks of running a business, keeping your personal life out of the line of fire.

Common Scenarios Where the Shield Holds Strong

Let's break down some common business risks where that LLC firewall really proves its worth:

- Business Debts and Loans: If your LLC defaults on a business loan, the lender can generally only go after the company’s bank accounts and property. Your personal checking account is off-limits.

- Vendor and Supplier Disputes: A disagreement with a supplier over an unpaid invoice? Their legal claim is with the LLC, not with you.

- Lawsuits for Employee Actions: Say an employee gets into a car accident while making a delivery. The resulting lawsuit is filed against the business entity, not its owners.

- Breach of Contract Claims: If your company is sued for failing to deliver on a contract, a judgment would be against the LLC's assets, leaving your personal assets untouched.

This protective layer is a massive reason the LLC has become the go-to choice for so many entrepreneurs. In fact, as litigation concerns have grown, so has the LLC's popularity. The U.S. Census Bureau reported over 2.8 million active LLCs in 2023, which is more than 40% of all business entities—a huge jump from just 1.5 million back in 2015.

The core idea is simple but powerful: your business is its own "person" in the eyes of the law. Its debts belong to it, and your personal assets stay yours, safe behind that financial firewall.

But here’s the catch: that firewall isn't indestructible. It has to be built right and maintained properly to stand strong. Certain actions—or a lack of action—can punch holes in that wall, potentially exposing your personal assets to business liabilities. Understanding these exceptions is every bit as important as knowing about the protection itself.

When the LLC Shield Can Be Pierced

While the LLC liability shield is a powerful tool, it's not an unbreakable wall. Think of it less like a solid concrete barrier and more like a high-tech security fence; it’s incredibly effective, but only if you maintain it and follow the rules. If you get sloppy, a court can disregard the LLC's separate legal identity and hold you, the owner, personally responsible for its debts.

This legal process is known as "piercing the corporate veil." It’s a remedy courts use when they find that an LLC isn’t a legitimate, separate entity but merely an “alter ego” of its owner—often used to sidestep obligations or commit fraud.

Understanding when this can happen is crucial for any business owner relying on their LLC for asset protection. In Connecticut, courts look for specific behaviors that suggest the line between the business and its owner has been blurred beyond recognition.

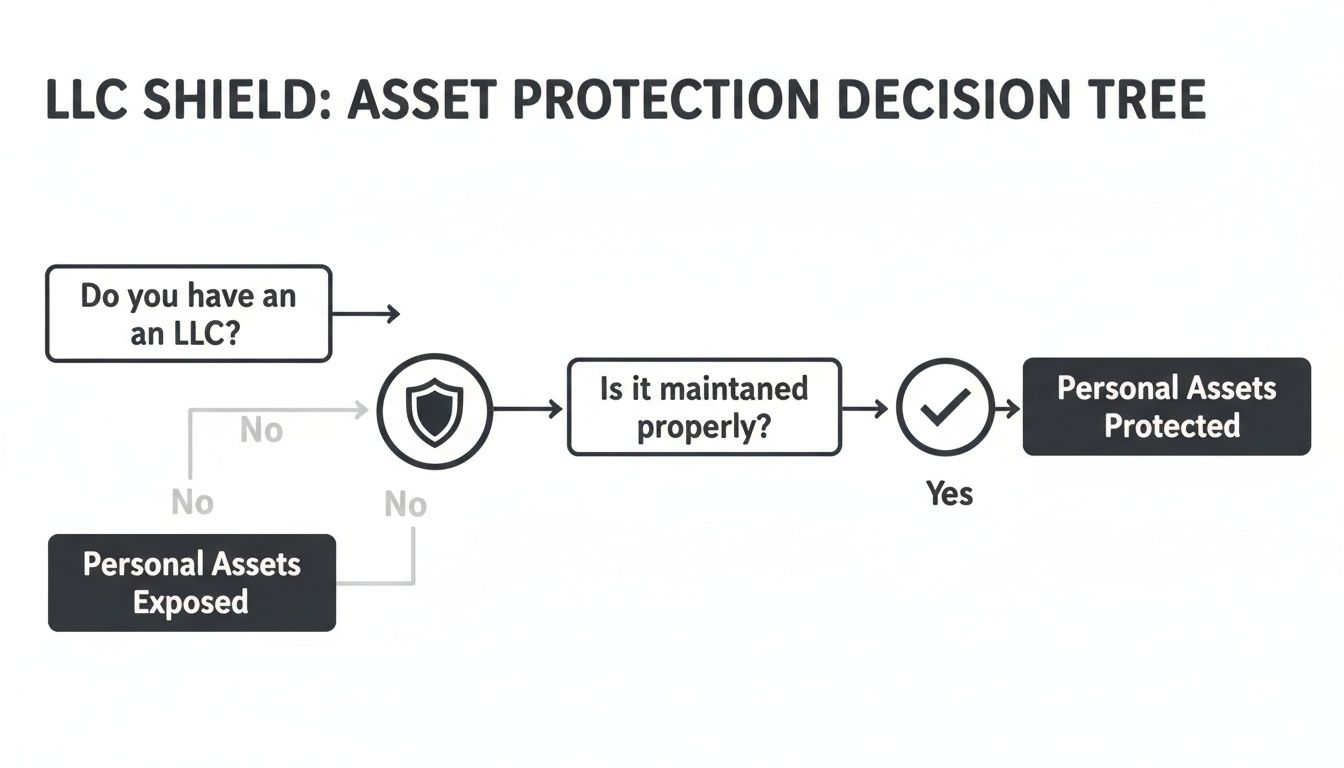

This decision tree gives you a quick visual of how proper maintenance preserves your liability shield.

As you can see, the path to protecting your personal assets hinges on how you operate the LLC after it’s formed.

Key Factors in a Veil Piercing Claim

Courts don't take piercing the veil lightly, but they won't hesitate if the circumstances justify it. Here are the most common ways owners put their personal assets at risk.

Commingling Funds

This is the cardinal sin of LLC ownership. Commingling is simply mixing your personal and business finances, and it’s a bright red flag for the courts.

- Using the LLC bank account to pay your mortgage or personal car payment.

- Depositing business revenue directly into your personal checking account.

- Swiping your personal credit card for business expenses without properly documenting it as a loan to the company.

These actions completely destroy the illusion of separateness. If you treat the company's money as your own, a court is much more likely to do the same.

Failure to Maintain Corporate Formalities

An LLC has to act like a real, standalone business. That means keeping proper records and observing the necessary legal formalities.

A court will look for evidence that the LLC was consistently treated as a distinct entity. This includes maintaining separate financial records, keeping meeting minutes (yes, even for single-member LLCs), and making sure all contracts are signed in the LLC's name, not your personal name.

Dropping the ball here suggests the LLC is just a facade for your personal dealings, making it far easier for a creditor to argue for piercing the veil.

Intentional Underfunding or Fraud

Setting up an LLC with barely enough cash to cover its foreseeable debts can be seen as a deliberate attempt to duck responsibility. This is known as inadequate capitalization. If you form an LLC for a risky venture but put almost no money into it, a court might conclude the entire structure was designed to defraud creditors from the start.

Other Direct Paths to Personal Liability

Beyond piercing the veil, there are a few other situations where the LLC shield simply doesn’t apply, and you can be held personally liable directly.

1. Personal Guarantees

This is, by far, the most common way business owners voluntarily give up their liability protection. When you apply for a business loan, sign a commercial lease, or open a line of credit, the lender or landlord will almost always require you to sign a personal guarantee. By signing, you are contractually agreeing to be personally on the hook for the debt if the LLC can't pay. The LLC shield offers zero protection here.

2. Committing Personal Torts

The legal term "tort" just means a wrongful act that harms someone else. The LLC shield was never designed to protect you from the consequences of your own misconduct.

- If you personally commit fraud, a client can sue you directly.

- If your direct negligence causes an injury (like a slip-and-fall in your office), you can be held personally liable.

- If you engage in professional malpractice, your personal assets are at risk.

3. Failure to Pay Payroll Taxes

The government takes payroll taxes very seriously. If your LLC withholds taxes from employee paychecks but fails to send that money to the IRS, the government can—and will—come after the responsible individuals personally for the full amount. This is called the Trust Fund Recovery Penalty, and it’s not something you want to face.

Here in Connecticut, where Kons Law operates, state courts saw a 15% jump in business disputes from 2020-2024, many of which tested these very principles. While forming an LLC is a powerful first step, maintaining it is an ongoing responsibility that demands diligence. You can read our detailed guide on piercing the corporate veil to get a deeper understanding of this critical concept.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Understanding Your Internal Roles and Fiduciary Duties

When you think about liability in an LLC, your mind probably goes straight to outside threats—lawsuits from customers or disputes with vendors. But some of the biggest risks are internal, stemming from the duties that owners and managers owe to the LLC and to each other. How you define and manage your internal roles can be just as crucial as the liability shield that protects you from the outside world.

It all starts with your LLC's management structure. There are really only two ways to go:

- Member-Managed LLC: This is the default setting in Connecticut and most other states. Think of it as a direct democracy—all members (the owners) have a say in the day-to-day business. Every member can sign contracts and make binding decisions.

- Manager-Managed LLC: In this model, the members appoint a manager (or a team of managers) to run the show. The other members step back into a more passive, investor-like role. They can't bind the company to a deal.

This isn't just a simple choice; it fundamentally changes who is legally on the hook for upholding what are known as fiduciary duties.

The Core Fiduciary Duties Explained

Fiduciary duties are the highest standard of care the law recognizes. They demand that the people in charge—the managing members or appointed managers—act strictly in the best interests of the company and its other members. If you breach these duties, you can be sued by the LLC or other members and be held personally liable for any damage you caused.

There are two big ones you need to know: the Duty of Care and the Duty of Loyalty.

1. The Duty of Care

This is about competence. It requires managers to act with the same diligence that a reasonably prudent person would in a similar situation. You don't have to be perfect, but you can't be reckless or grossly negligent. Forgetting to do any research before sinking company funds into a major purchase? That could be a breach.

2. The Duty of Loyalty

This one is even more strict. It’s a simple but powerful command: put the LLC’s interests ahead of your own. Always.

The Duty of Loyalty is an unwavering obligation to avoid self-dealing and conflicts of interest. It ensures that decisions are made for the benefit of the company, not for personal enrichment at the company's expense.

Common ways people breach this duty include:

- Stealing a corporate opportunity by taking a business deal for yourself when it should have gone to the LLC.

- Directly competing with your own LLC's business.

- Engaging in self-dealing transactions, like selling personal property to the LLC at an inflated price without full disclosure.

Getting these duties wrong can create serious internal conflict. To see just how these situations play out in the real world, you can explore several breach of fiduciary duty examples in our detailed article.

Protecting Yourself with an Operating Agreement

The good news is you have a powerful tool to manage these internal risks: a well-drafted operating agreement. This is the foundational document for your LLC, and it can be used to clearly define everyone's roles, responsibilities, and the precise scope of their fiduciary duties. You can even limit liability for certain honest mistakes, as long as they don't involve intentional misconduct or breaking the law.

Your operating agreement can also include an indemnification clause. This is a critical provision that can require the LLC to pay the legal bills for a member or manager who gets sued for actions they took in good faith while running the business. It's a safety net that allows leaders to make bold decisions without constantly looking over their shoulder, fearing a lawsuit.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Proactive Strategies to Fortify Your Liability Shield

Forming an LLC is like putting up the frame of a house—it gives you the basic structure for protection. But a frame alone won't keep the rain out. To truly safeguard your personal assets and make your liability in an LLC meaningful, you have to build the walls, lock the doors, and actively maintain the property.

This means going beyond the initial paperwork. It requires consistent, proactive habits that prove your business is a legitimate, separate entity. These aren't just suggestions; they are the bedrock of your liability shield.

The Operating Agreement: Your LLC's Constitution

If there's one document that stands between your business and chaos, it's the operating agreement. Think of it as the constitution for your company. It lays down the law on governance, clarifies who does what, and provides a roadmap for making critical decisions.

Without a solid operating agreement, your LLC defaults to Connecticut's generic rules, which might be a terrible fit for your specific situation. A well-crafted agreement should nail down the specifics:

- Management Structure: Is the LLC run by its members or by appointed managers? Who has the final say on signing contracts or spending money?

- Profit and Loss Distribution: It dictates exactly how profits and losses are split among the members, heading off the kind of arguments that can tear a business apart.

- Fiduciary Duties: As we've covered, this document can define—and even limit—certain fiduciary duties, giving managers breathing room to make honest business judgments without fear of a lawsuit.

- Dispute Resolution: It establishes a clear process for handling disagreements, keeping internal squabbles from escalating into a full-blown court battle.

A strong operating agreement is your first line of defense. It creates an undeniable record of how your business operates, entirely separate from its owners.

Maintaining Strict Corporate Formalities

"Corporate formalities" sounds like stuffy boardroom jargon, but it really boils down to one simple idea: act like a real business. When things go sideways, courts look for consistent, professional conduct that proves you and your LLC are not one and the same. Getting lazy here is one of the quickest ways to see your liability shield pierced.

These aren't just details—they're the evidence that keeps your personal and business worlds separate. The table below outlines the essential practices.

Key Practices for Maintaining Your LLC Liability Shield

| Action Item | Why It's Critical | Potential Consequence of Failure |

|---|---|---|

| Maintain Separate Bank Accounts | This is the clearest line between your money and the company's money. | Commingling funds is the #1 reason courts pierce the veil. It suggests the LLC is just your alter ego. |

| Hold and Document Meetings | Creates a formal record of major business decisions, proving the LLC acts independently. | A lack of records can make the LLC look like a sham, managed by personal whim rather than corporate governance. |

| Ensure Adequate Capitalization | Provides the LLC with enough funds to operate and cover its foreseeable debts. | Starting an LLC with no money can be seen as a fraudulent attempt to avoid personal liability for debts. |

| Keep Meticulous Records | Includes financial statements, contracts, meeting minutes, and member resolutions. | Poor records weaken the argument that the LLC is a distinct legal entity, making it easier to pierce. |

| Sign Documents Correctly | Always sign contracts as a representative of the LLC (e.g., "John Smith, Manager, XYZ, LLC"). | Signing your name without your title and the LLC's name can create personal liability for that contract. |

Following these formalities isn't about creating busywork. It's about building a fortress around your personal assets, one brick at a time. Each action reinforces the legal separation that you created the LLC to achieve in the first place.

Layering Your Defense with Business Insurance

Finally, it's crucial to understand that your LLC shield and business insurance aren't an either/or proposition. They are two different layers of protection that work together. Your LLC protects your personal assets from business debts, while insurance protects the business's assets from lawsuits and claims.

For business owners, understanding the Best Insurance for Self Employed Professionals is a non-negotiable step in building a complete financial firewall.

While an LLC shields personal assets, corporate liability insurance is a vital second line of defense. The average U.S. general liability premium is around $360 annually and has been rising 5-10% each year. This underscores that even with an LLC, insurance is a necessary business expense.

A few types of insurance should be on every LLC's radar:

- General Liability Insurance: The workhorse policy that covers claims of bodily injury or property damage.

- Professional Liability Insurance (E&O): A must-have for any service business, protecting against claims of negligence or mistakes.

- Commercial Auto Insurance: If you or your employees use vehicles for work, personal auto policies won't cut it.

By combining a rock-solid operating agreement, disciplined formalities, and the right insurance coverage, you construct a defense that makes your LLC's liability shield incredibly tough to break.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

How Creditors Approach LLCs and Their Members

So far, we’ve looked at liability in an LLC from the owner’s side of the table. But to really grasp how powerful this business structure is, you need to see it through a creditor's eyes. When someone is trying to collect a debt, an LLC throws up some unique roadblocks, and the tools they can use change dramatically depending on one key question: who owes the money—the LLC itself, or one of its members?

This distinction is everything. If a creditor's claim is against your business, their path is pretty clear. But if their claim is against you personally, they’re about to run headfirst into the LLC’s formidable asset protection wall.

Collecting From the LLC Itself

When the LLC is the one in debt, the collection process is traditional. Let’s say your construction company fails to pay a lumber supplier. That supplier can sue the LLC directly. If they win a judgment, they can enforce it against the company's assets.

This means they can go after things like:

- Garnishing the LLC’s business bank accounts.

- Seizing company-owned vehicles and equipment.

- Placing a lien on any real estate the business owns.

In this situation, the limited liability shield is working exactly as designed. The creditor’s reach stops at the company's door. They can't cross that line to grab the personal homes, cars, or savings accounts of the LLC members. Your personal wealth stays safely out of it.

The Creditor’s Main Tool Against a Member: The Charging Order

Things get much more interesting when a creditor has a personal judgment against an LLC member. Maybe a member got into a car accident that had nothing to do with the business and now owes a huge personal debt. The creditor can't just storm in and seize that member's ownership stake in the LLC or force the company to sell off its assets to pay the bill.

Instead, in Connecticut, the creditor’s primary—and often only—remedy is what’s known as a charging order.

A charging order is a court-issued lien on a member's "transferable interest" in the LLC. In simple terms, it gives the creditor the right to receive any profit distributions that the LLC decides to pay out to that specific member. And that's it.

This is a massive limitation for the creditor. The charging order does not make them a new member of the LLC. It gives them zero voting rights, no say in how the business is run, and no ability to peek at the company's books. They are completely powerless to force the LLC to make a distribution or sell company property.

The creditor just has to sit and wait, hoping the LLC decides to distribute profits to the member they have the judgment against. As you can imagine, this powerfully protects the LLC and its other members from one person's private financial mess, letting the business carry on without disruption. It’s a perfect illustration of how a properly structured LLC masterfully separates business from personal.

If you want to dig deeper, our guide explains in detail what is a charging order and how it works in practice.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Protecting Your Business: A Connecticut Law Perspective

As a business owner in Connecticut, getting your head around LLC liability is one of the most important things you can do. The whole point of an LLC is to create a powerful shield that separates your business debts from your personal assets, like your home and savings. Think of it as a legal firewall designed to prevent a business lawsuit from turning into a personal financial catastrophe.

But here’s the thing: that shield isn't automatic or indestructible. It's conditional. It only works if you work at it. The most critical lesson we see clients learn is that the liability protection holds up only when you consistently respect the boundary between you and your business. Small mistakes—like paying for personal groceries with the company debit card or forgetting to sign a contract in the LLC's name—can start to create cracks in that firewall. That’s when a court might step in and "pierce the veil."

Key Pillars of Protection

Want to keep that liability shield strong and intact? You have to focus on a few non-negotiable fundamentals:

- A Strong Operating Agreement: This is the constitution for your LLC. It sets the rules for how the business is run, who is in charge, and proves to the world that you’re a legitimate, separate entity.

- Strict Corporate Formalities: Always keep your business finances in a separate bank account. No exceptions. You also need to keep clear records of major decisions and sign every document on behalf of the company, not as yourself.

- Adequate Business Insurance: Your LLC protects your personal assets from the business. Insurance protects the business's assets. When you have both, you create a layered defense that is incredibly difficult for anyone to get through.

Navigating the complexities of commercial law and making sure your business is properly structured isn't something to leave to chance. Getting proactive legal guidance is the best way to fortify your business for whatever comes its way.

Managing these pieces correctly is what ensures your LLC actually does its job: protecting the personal wealth you’re working so hard to build. The rules are pretty straightforward, but it's the consistent, disciplined application of them that truly matters.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.

Common Questions We Hear About LLC Liability

When you're running a business, the legal theory is one thing, but how it plays out in the real world is what really matters. Let's tackle some of the most frequent questions business owners ask about what LLC liability means for them day-to-day.

Does My Single-Member LLC Really Protect Me?

Yes, it absolutely can. A single-member LLC (or SMLLC) is designed to provide the same powerful liability shield as a multi-member LLC. That means your personal assets are, by law, separate from the business's financial obligations.

But here’s the catch: courts often look at SMLLCs with a bit more skepticism. Why? Because with only one person at the helm, it's incredibly easy to blur the lines between business and personal finances. To keep your liability shield strong and intact, you must be disciplined. Always use a separate business bank account, keep clean financial records, and make sure every contract is signed in the name of your LLC, not your own.

What If My Business Partner Commits Fraud? Am I Liable?

Generally, no. The LLC structure is built to protect you from being held personally responsible for the independent fraudulent or wrongful acts of your partners. If another member goes rogue, a lawsuit would target that individual and the LLC's assets—not your personal savings or home.

However, this protection isn't absolute. If you were involved in the fraud, knew it was happening and looked the other way, or were grossly negligent in your oversight, a court could potentially hold you accountable.

This is exactly why a well-written operating agreement is non-negotiable. It should spell out everyone's duties, authority, and responsibilities, creating a clear record that can protect innocent members when someone else acts improperly.

What Happens to Liability If I Close My LLC?

Shutting down an LLC isn't as simple as just closing the doors. You have to go through a formal "winding up" process. This means you use the company's assets to pay off any known debts and creditors before you distribute any leftover money to the members.

Your limited liability protection typically holds for debts the LLC incurred while it was operating legally. But if you skip the proper steps—say, you drain the business bank account for yourself and ignore a pile of vendor invoices—creditors can come after you personally. This is called a "wrongful distribution," and it's a critical mistake to avoid by following Connecticut's dissolution rules to the letter.

Will Running My Business From Home Put My House at Risk?

Using a home office, by itself, does not expose your house to business liabilities. Your LLC's protective shield still separates your personal property from company debts.

What it does do is make that separation more important than ever. You need to maintain a strict "church and state" divide between your home life and your business operations. This means:

- Designating a specific area of your home exclusively for business.

- Never mixing funds. Use a business credit card for office supplies and a personal one for groceries.

- Ensuring your official business address is properly registered with the state.

The real danger to your home isn't the home office itself, but the exceptions to liability protection. If you personally guarantee a business loan and use your house as collateral, or if someone gets hurt on your property due to your personal negligence (which is often a homeowner's insurance issue anyway), that's when your personal assets could be on the line.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.