The call usually arrives when your desk is already busy. A volatile opening. A client with concentrated positions. An operations team watching debits and maintenance levels tighten. At that moment, “what is a margin call” stops being a retail glossary question and becomes a professional liability issue.

For financial advisors and brokerage professionals, a margin call touches more than client account math. It affects suitability analysis, supervision, documentation, complaint exposure, and in the wrong fact pattern, the language that ends up in an investigation file or on a Form U5. If you work with margin accounts, you need to understand not only when a call occurs, but also how fast it can escalate and what your firm is entitled to do once it does.

The Inevitable Call on a Volatile Day

You know the pattern. A client calls in the middle of a broad selloff and asks why the account is restricted, why the firm is demanding funds, or why a sale was executed before they could “decide what to do.” The client hears unfairness. The broker-dealer hears collateral impairment. Compliance hears a recordkeeping and disclosure problem developing in real time.

A margin call is the point at which the client's equity in a margin account falls below the amount required under the applicable rules and the firm's own standards. The immediate consequence is simple. The client must restore the account, or the firm may act to protect its loan exposure.

Why this matters for professionals

For an investor, a margin call is painful. For an advisor, it can become evidence. If the file doesn't show clear risk disclosure, a reasoned basis for using margin, and timely communication when stress hit the account, the dispute later won't be about market conditions alone. It will be about process, judgment, and whether the client fully understood what they authorized.

The practical issue is that margin problems rarely stay technical. They turn into questions such as:

- Was the recommendation suitable: Did the client's objectives, liquidity needs, and loss tolerance support a strategy involving borrowed funds?

- Was the concentration obvious: Did the account drift into a position mix that made a call predictable?

- Was the warning documented: Can the firm show more than a generic acknowledgment form?

Professional reality: A margin call often becomes the event that causes clients to reread every prior conversation through the lens of loss.

Advisors who want a client-friendly primer on preventing unexpected margin calls can use it as a supplemental educational piece. It doesn't replace firm disclosures or legal review, but it can help frame the operational risk in plain language before volatility does it for you.

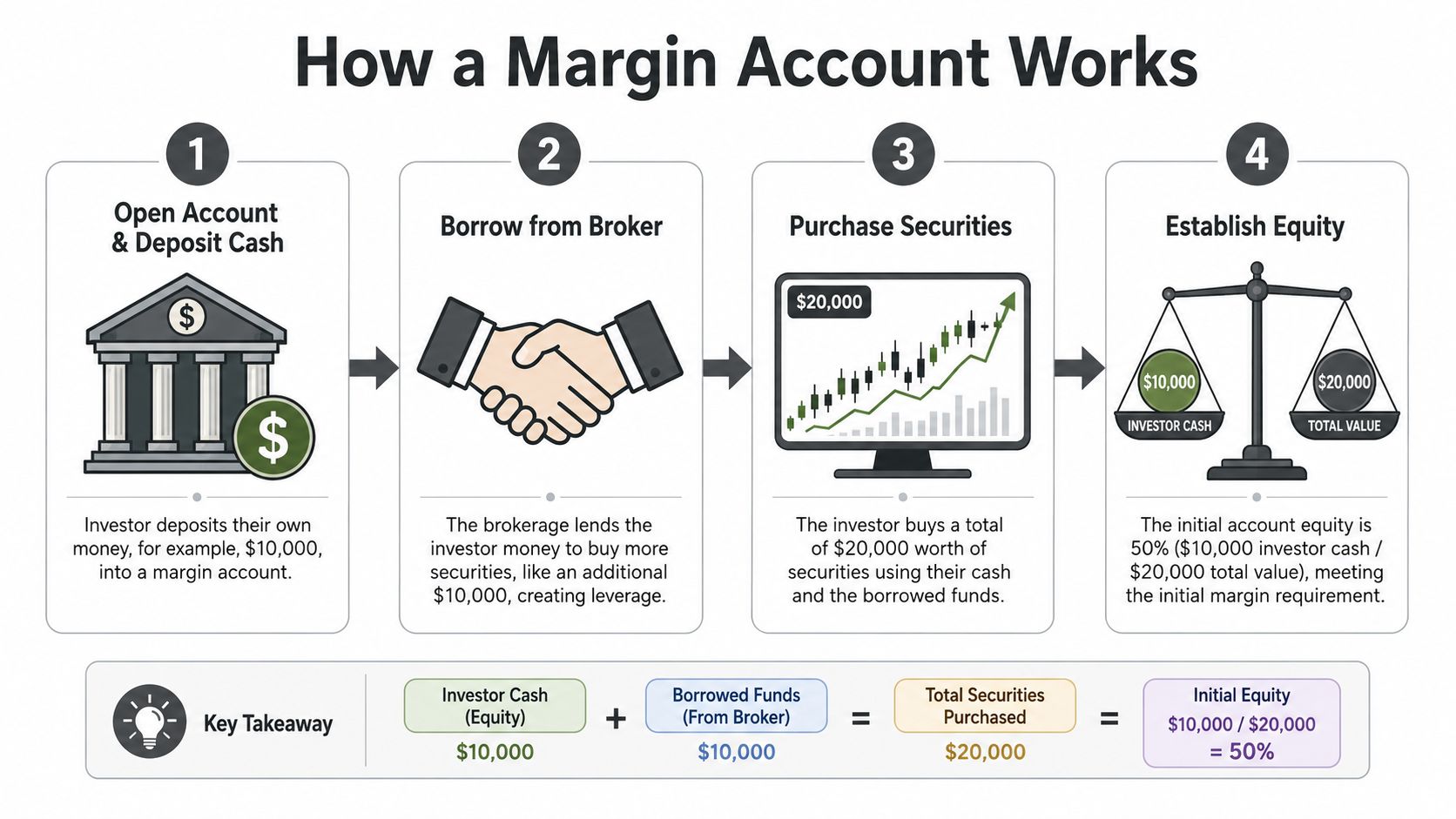

The Core Mechanics of Margin Trading and Equity

The legal risk starts with the math. If the advisor can't explain margin account equity in a sentence or two, the client probably didn't understand it either.

Under FINRA's guidance on margin calls, Federal Reserve Regulation T generally allows a broker to initially lend up to 50% of the purchase price of an eligible stock, and FINRA maintenance rules generally require equity to remain at or above 25% of the current market value of long securities. FINRA's example states that if an investor buys $10,000 of stock on margin, the broker may initially lend up to $5,000. If later losses push equity below the maintenance threshold, the investor must add cash or securities or face liquidation. FINRA also notes that a broker may impose higher house requirements, so a call can occur even without a new trade or a fresh price decline.

Start with the account structure

A margin account has three moving parts:

- The securities value. This is what the holdings are worth at current market prices.

- The loan balance. This is what the client owes the firm.

- The client's equity. This is the value of the account minus the loan.

At the start, the numbers may look stable because the client contributes capital and the firm advances the rest. But relying on borrowed funds changes how losses behave. The borrowed portion doesn't shrink just because the market does. That means the client's equity absorbs the decline faster than it would in a cash account.

The basic example advisors should be able to explain

Use the standard example because it's clear and defensible.

| Account element | Amount |

|---|---|

| Securities purchased | $10,000 |

| Client contribution | $5,000 |

| Broker loan | $5,000 |

| Starting equity | $5,000 |

The client controls a larger position than they could buy with cash alone. At opening, the equity looks healthy because the client funded half the position.

That's the easy part. The harder part is helping the client understand that maintenance is measured against the current market value, not the original purchase price. Once prices fall, the same loan sits against a smaller collateral base.

A client who says “I only borrowed half” may still be badly exposed if the account is concentrated or the firm applies stricter house maintenance.

Where professionals get into trouble

The common failure isn't the existence of margin. It's poor framing. Advisors sometimes describe margin as added flexibility or short-term liquidity without making clear that the account is governed by shifting maintenance thresholds and liquidation rights. That gap in explanation is where many later disputes begin.

How a Margin Call Is Triggered and Calculated

The trigger point is not mysterious, but clients often experience it as a surprise because they focus on losses in dollars while firms monitor equity as a ratio. That difference matters.

The core calculation

The equity percentage in a margin account is:

Equity ÷ current market value of securities

Equity itself is:

Current market value minus the margin loan

Using the same account structure from above, the analysis runs in sequence:

- Step one: Identify the current market value of the holdings after the decline.

- Step two: Subtract the outstanding loan balance.

- Step three: Divide the remaining equity by the current market value.

- Step four: Compare that result to the applicable maintenance requirement.

If the result falls below the required level, the account is subject to a margin call.

Why house requirements change the legal conversation

Many client disputes arise because the investor has heard the regulatory minimum and assumes that's the operative standard in all conditions. It often isn't. The actual control point is usually the broker-dealer's house maintenance schedule, applied at the account level and often tightened by security type, concentration, volatility, or firm risk posture.

That creates two professional obligations. First, the advisor needs to know the firm's current internal standards, not just the baseline rule. Second, the advisor needs to communicate that those standards can move in stressed conditions. If that disclosure is buried in fine print and never reinforced in conversation, the client will often say they were blindsided.

Explain it in business terms, not just formulas

Clients understand balance-sheet pressure better than margin jargon. One useful way to frame it is this: the account has assets, a debt to the firm, and a required equity cushion. If the asset side weakens and the debt remains, the cushion shrinks. For advisors who need a simple accounting analogy, this overview on how to read a balance sheet helps explain why equity is always the first thing pressure hits.

For traders and advisors who want a practical calculator to protect your trading account, external tools can help illustrate sensitivity to price moves. Use them carefully. They're educational aids, not substitutes for your firm's own margin methodology, disclosures, or supervisory procedures.

When a margin dispute gets reviewed later, the record that matters is rarely “the client knew borrowing was risky.” It's whether the file shows the client understood how quickly equity can fail once maintenance rules tighten.

The Brokerage Firm Playbook for Enforcing Margin Calls

Once a call exists, the firm's rights become the center of the analysis. At this point, investor expectations and contractual reality separate sharply.

The U.S. Securities and Exchange Commission's margin call guidance states that if securities purchased on margin decline, a brokerage firm may require immediate cash or securities, or sell positions to cover the shortfall without informing the customer in advance. The SEC also states that brokerage firms may change the threshold for when customers become subject to a margin call at any time. That same guidance notes that while many marginable stocks carry a 25% maintenance requirement, some securities may require 75% or even 100%, which materially tightens funding pressure.

What the client can do

In operational terms, the client usually has only a few ways to respond:

- Deposit cash: The fastest path if the client has liquidity and wants to preserve the position.

- Deposit marginable securities: Sometimes viable, but only if the assets are eligible and transferred in time.

- Sell positions: This may be voluntary at first, but it often happens into weakness and under time pressure.

The key point is that none of these options restores bargaining power. They only address the deficiency.

What the firm can do

The firm's margin agreement typically gives it broad discretion. That usually includes the right to liquidate without waiting for the client's consent, without honoring the client's preferred sale sequence, and without preserving a tax or strategy preference the client hoped to maintain.

That's why advisors should stop using soft language when they discuss margin maintenance. A call isn't a courtesy reminder. It is an enforceable demand backed by the firm's contractual right to protect its credit exposure.

The broker-dealer's job in a margin event is to secure the loan. It is not to optimize the client's timing, basis, or long-term investment thesis.

Why this becomes a dispute file

Clients often complain that they “weren't given a chance” or that the firm sold the wrong securities. Sometimes those complaints become customer disputes, internal reviews, or formal claims. When they do, the underlying questions often overlap with the issues that appear in the FINRA arbitration process, including account documentation, disclosure practices, supervision, and whether the recommendation to use margin was properly grounded from the outset.

For advisors, the compliance lesson is blunt. You cannot control the market, but you can control whether the file shows the client was told the firm could act first and ask questions later.

Real World Scenarios and Financial Consequences

The most dangerous feature of a margin call is that the remedy often requires selling more than the client expects. That disconnect fuels panic and complaints.

Fidelity's discussion of avoiding and managing margin calls describes margin calls as a forced deleveraging mechanism. The investor must deposit cash or marginable securities, or sell positions to restore required equity. If they don't, the broker may liquidate holdings. Fidelity's example shows that meeting a $2,000 margin call can require selling about $6,670 of stock when the remaining position carries a 30% maintenance requirement.

Scenario one with a concentrated position

An advisor has a client who used margin to increase exposure to a single volatile name the client strongly believed in. The stock drops hard over a short period. The client still wants to hold because they view the decline as temporary.

The account, however, doesn't care about conviction. If the security is subject to heightened maintenance, the call can arrive before the client is psychologically ready to fund it. If the client can't add capital, the position gets reduced into a falling market. The client then feels harmed twice. First by the loss. Second by the forced sale that prevented any later recovery.

Scenario two with broad but correlated risk

A different client holds several positions across sectors and assumes the account is diversified enough to handle the amplified risk. In calm periods, that assumption feels reasonable. In a broad market shock, correlation rises, multiple positions fall together, and the portfolio behaves much more like a single risk trade than the client expected.

That's when advisors hear, “But I wasn't concentrated.” Technically maybe not. Economically, the account still moved as one.

What forced selling does to the client relationship

Three practical consequences show up repeatedly:

- Losses become realized: The client can no longer decide to wait.

- Cash planning gets disrupted: Funds that were earmarked for taxes, business operations, or personal obligations may have to move into the account.

- Blame shifts quickly: Clients often recast prior margin discussions as incomplete once liquidation happens.

A manageable paper loss can become an unmanageable professional problem the moment liquidation removes the client's sense of control.

Proactive Risk Mitigation and Advisor Best Practices

A volatile opening bell is not the time to decide whether a client ever should have been on margin. That decision should already be supported by the file, the account profile, and a supervision record that shows judgment rather than sales momentum.

Build the margin case before the first trade

For advisors and branch personnel, margin approval is a risk decision with client, firm, and personal consequences. A client's interest in “more buying power” is not a sufficient basis. The record should show why borrowed funds fit the client's finances, liquidity, investment objective, and ability to tolerate a forced sale without impairing other obligations.

In practice, that means asking questions some producers avoid because the answers can slow or stop the trade:

- Where would the client get cash if house maintenance increases or equity falls fast?

- Is the account exposed to one issuer, one sector, or one correlated theme that can break together?

- Would a forced liquidation create tax, business, or personal stress the client cannot absorb?

- Has the client handled prior drawdowns rationally, or does behavior suggest panic under pressure?

Those questions protect more than portfolio performance. They help establish that the recommendation process was grounded in suitability and care, not convenience. Advisors reviewing similar process failures often benefit from this discussion of breach of fiduciary duty examples, especially where a claimant later argues that disclosure, monitoring, or account approval fell short.

Test the account the way the firm will

Firms do not evaluate risk based on a client's optimism. They evaluate collateral, concentration, liquidity, and exposure to rapid repricing. Advisors should review margin accounts the same way before problems start.

A simple review framework works well:

| Review question | Why it matters |

|---|---|

| Can the client satisfy a call with available cash or readily marketable assets? | If not, the likely outcome is liquidation under firm control |

| Does the account depend on securities that can face higher house requirements without much notice? | Reaction time shrinks when maintenance terms tighten |

| Are several positions likely to decline together in a broad selloff? | Apparent diversification can fail under stress |

Outside reading can sharpen that analysis. For professionals who want a trading-focused framework, mastering trading risk offers a useful perspective on position discipline and exposure management.

Document the conversations that matter

A signed margin agreement helps the firm. It rarely resolves the actual dispute. The cases that become expensive usually turn on whether the file shows clear warnings, specific funding discussions, and timely communication once risk increased.

Good documentation is concrete:

- Why margin was appropriate for this client at this time

- What sources of liquidity were identified before trading

- What was explained about the firm's right to liquidate without prior consent

- What contact was made when equity deteriorated or concentration increased

- What the client said in response

Short, dated notes often carry more weight than polished summaries written after the account has already broken down.

Written records preserve what was said before losses changed the client's memory and the firm's litigation posture.

Practices that create exposure

Some habits look diligent but fail under scrutiny.

- Relying on boilerplate disclosures. Generic forms do not show that the advisor explained how margin works in the client's actual account.

- Treating approval as a one-time event. A suitable use of margin can become unsuitable after concentration grows, liquidity changes, or the client's circumstances deteriorate.

- Using reassurance instead of instructions. Telling a client to stay patient does not solve an equity deficiency or document a funding plan.

- Assuming stop orders solve the problem. Gaps, volatility halts, and house maintenance changes can make that assumption costly.

From a supervision and U5 perspective, the best practice is straightforward. Approve margin sparingly, review it repeatedly, and document it like a future regulator, arbitration panel, or plaintiff's counsel will read every line.

Legal and Regulatory Implications for Professionals

Margin calls often become the event that turns an unhappy client into a claimant. The legal issue usually isn't limited to whether the account fell below maintenance. It expands into whether margin was recommended appropriately, whether risks were explained in a way the client could understand, and whether the account was supervised when conditions changed.

That makes suitability central. If the client lacked the financial ability or risk tolerance to withstand forced deleveraging, the use of margin may be attacked as an unsuitable recommendation. If the account involved concentration, liquidity mismatch, or aggressive strategy drift, the exposure grows. If the communication record is thin, the advisor may have little evidence to counter the client's narrative.

Where this can land professionally

A margin dispute can trigger multiple layers of review:

- Customer complaint exposure: The initial grievance often focuses on forced liquidation or alleged failure to warn.

- Regulatory inquiry: Supervisory systems, notes, and account approvals may be scrutinized.

- Employment consequences: Internal discipline or separation events can create downstream disclosure concerns.

For professionals already dealing with complaint or investigation risk, issues tied to margin accounts can overlap with topics discussed in what is securities fraud, particularly where the dispute alleges misrepresentation, omission, or unsuitable recommendations rather than simple market loss.

Risk education also matters on the front end. Broader trading discipline resources, including mastering trading risk, can be helpful as supplemental reading for understanding why magnified positions convert ordinary volatility into operational and legal stress. But for regulated professionals, education alone isn't enough. The record must show informed recommendations, proper supervision, and timely communication.

A margin call is never just an account event for an advisor. It can become a complaint file, an arbitration claim, a supervisory issue, or a Form U5 problem depending on how the account was opened, monitored, and explained.

If you want to discuss your business law matter, contact Kons Law at (860) 920-5181.